.svg)

My lords! My ladies. *turns to cheap seats* And everybody else here NOT sitting on a cushion.

Today, today, you find yourselves equals. For you are all equally blessed. For I have the pride, the privilege, nay, the pleasure, of introducing to you a Knight, sired by Knights. A Knight who can trace his lineage back beyond Charlemagne.

I first met him atop a mountain near Jerusalem praying to God, asking His forgiveness for the Saracen blood spilt by his sword.

Next, he amazed me still further in Italy when he saved a fatherless beauty from the would-be ravishings of her dreadful Turkish uncle.

In Greece, he spent a year in silence… Just to better understand the sound... ... ... of a whisper.

And so, without further gilding the lily, and with no more ado, I give to you the Seeker of Serenity, The Protector of Italian Virginity, The Enforcer of our Lord God, The One! The Only! Sirrrrr Ulrich Von Lichtenstein!!!

-Chaucer (Paul Bettany), A Knight's Tale

Much like Paul Bettany's character in A Knight's Tale, I've tried to rally a weary, beaten-down gang of investors around an underdog. The business has very good potential for a revival next year on the heels of its pipeline. It'd be a shame for all the little guys to miss the potential opportunity now just because the privileged few institutional investors have turned away.

The opportunity for CCR8 inhibitors is beginning to attract global attention. If half of existing global programs from the likes of Bristol Myers Squibb and Amgen advance, then the drug class could see over $15 billion in cumulative R&D investments by 2030 – easily becoming one of the largest active opportunities in drug development.

Meanwhile, casdozo remains the only IL-27 inhibitor in the global pipeline. If the ongoing phase 2 study can replicate findings from the previous mid-stage study, then it potentially opens a market opportunity worth up to $4 billion in peak annual sales that no other company can access.

Management also strongly hinted there could be both U.S. and ex-U.S. licensing deals in the next six to 18 months as well as new clinical collaborations, which could break up the monotony of Loqtorzi's slow and steady ramp.

But I wouldn't be doing my job if I didn't properly set expectations. Coherus Oncology might have given me hemorrhoids in recent years, but the next few quarters are likely to be accompanied by a different reality: Boredom. Similar to Sir Ulrich Von Lichtenstein, investors hoping for a durably higher share price will need to sit in (mostly) silence as they await up to six internal data readouts in 2026.

By the Numbers

The Udenyca divestiture was finalized in April, which allowed the business to pay off substantially all outstanding debt. Although there are some lingering items on the balance sheet from the transaction, most activity is now tucked away under "discontinued operations" in financial statements.

There's not much else for investors to get excited about in terms of commercial performance in the next few quarters. I'll be simply checking in on the cash balance and gradual ramp of Loqtorzi, then combing through pipeline updates.

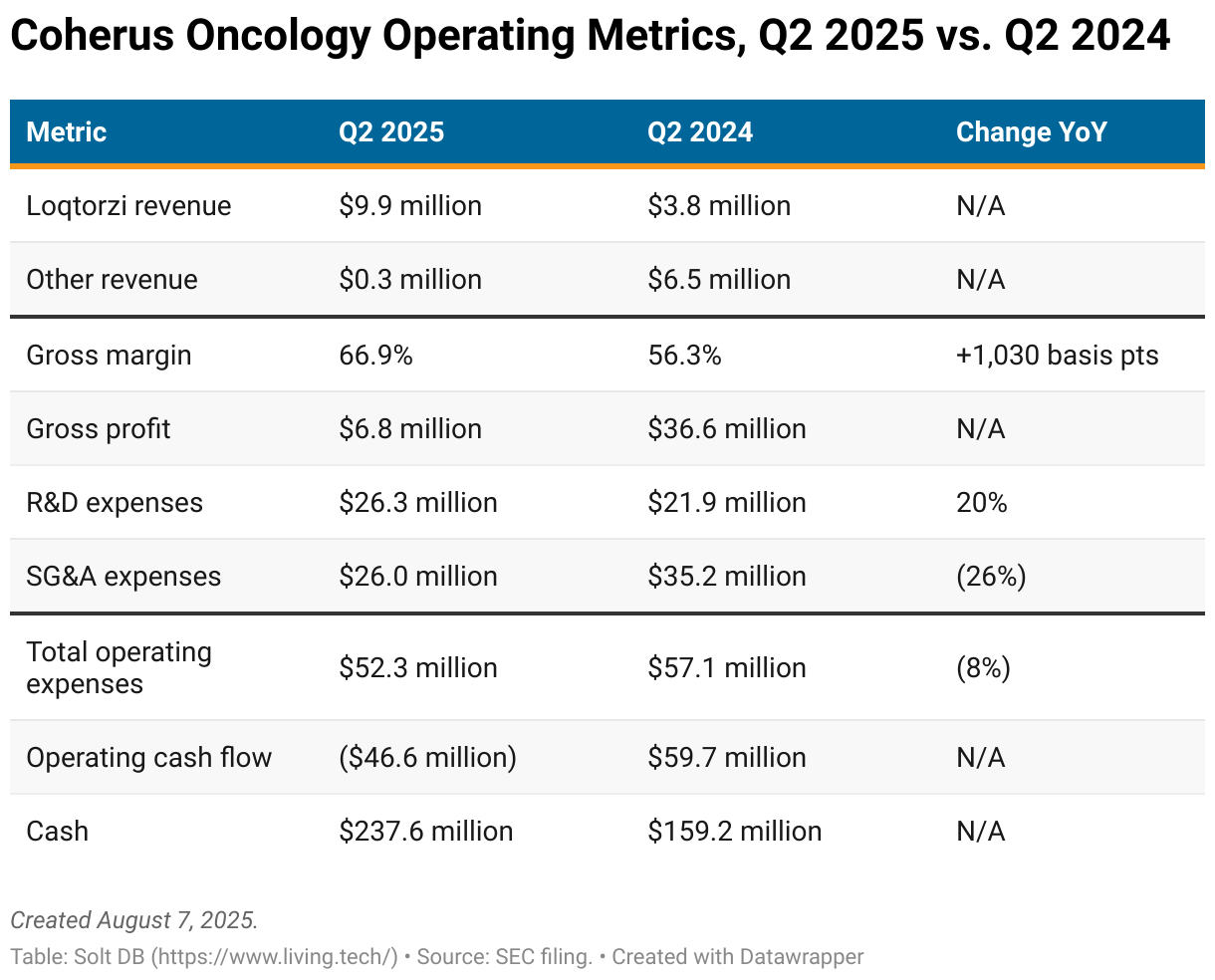

Coherus reported second-quarter 2025 revenue of $10 million for Loqtorzi, up 36% from the first quarter. Gross margin and total operating expenses improved in the year-over-year period, although operating cash flow was thrashed by the timing of divestment transactions.

Importantly, the business ended June 2025 with $237.6 million in cash and cash equivalents. That's enough to fund operations into early 2027 – well past up to a half dozen data readouts and after a potential $37.5 million cash milestone that can be earned for Udenyca sales targets.

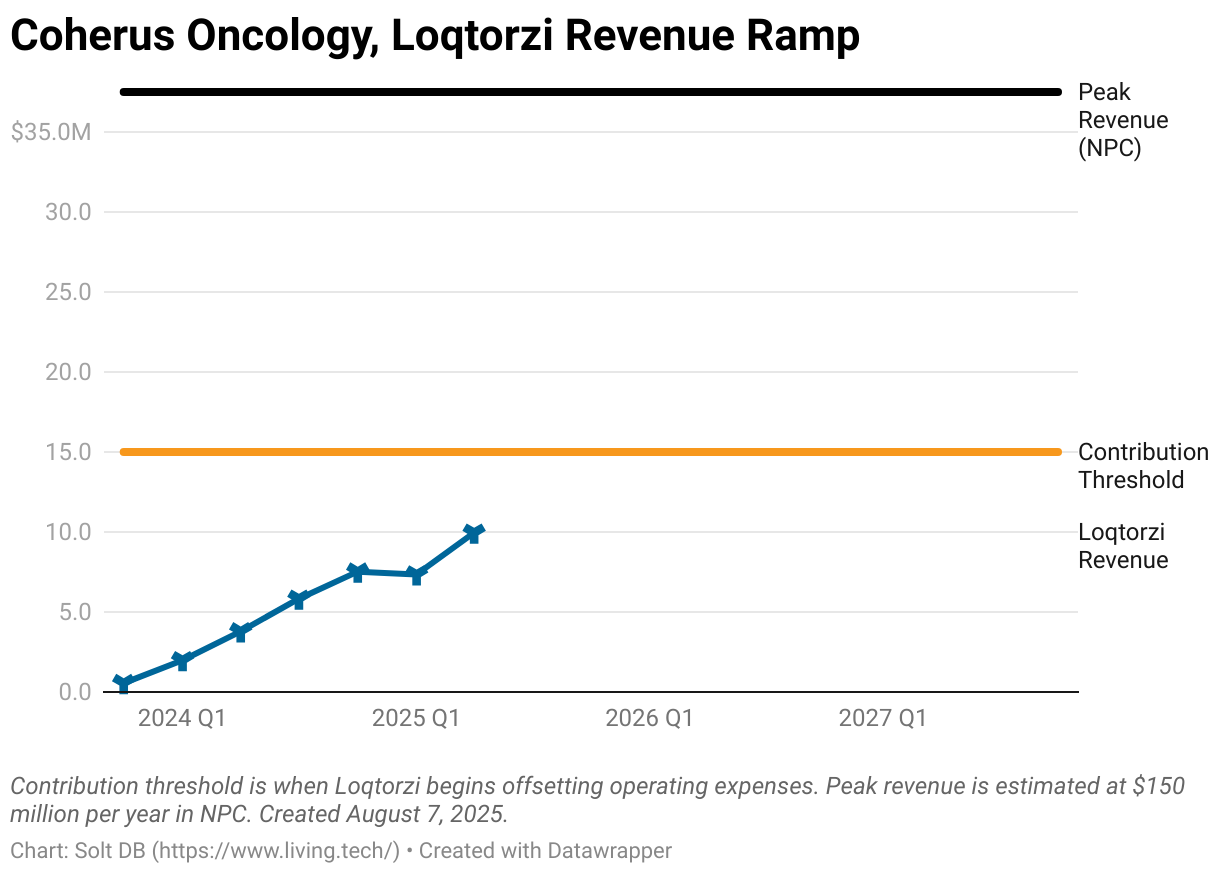

The slow-and-steady ramp of Loqtorzi continues toward its peak annual sales opportunity of $150 million, or roughly $37.5 million in peak quarterly sales. Management thinks the opportunity could be as high as $200 million per year or $50 million per quarter. In either case, peak revenue is expected to be achieved in 2027 – I model it as an exit rate, meaning Q4 2027 revenue of roughly $37.5 million.

The second-quarter haul represents two-thirds of the cash breakeven rate for the franchise. Once quarterly revenue exceeds the $15 million mark it'll begin to offset operating expenses. Loqtorzi sales in the nasopharyngeal carcinoma (NPC) indication will never be enough to fully fund the business, even at their peak, but it should slow cash burn and build brand awareness.

Management plans to increase digital marketing spend beginning in Q3 2025 to drive awareness of Loqtorzi. That'll be important for capturing the opportunity in community hospitals, which have 3x as many physicians as represented by National Comprehensive Cancer Network (NCCN) facilities.

Although community hospitals treat up to 80% of all cancer patients broadly, rare cancers like NPC are primarily treated at specialty hospitals. Specifically for this commercial ramp, the 25% of physicians at NCCN facilities treat 67% of all NPC cases in the United States.

Therefore, for a small company like Coherus, it makes sense to continue focusing on NCCN facilities directly. Indirect channels like digital marketing and content represent a more capital-efficient way to reach the other third of the market for now.

Around the Horn

The fate of Coherus previously rested on commercial execution for the Udenyca franchise. After the divestiture to clean up the balance sheet, the company's ability to earn a durably higher valuation (or get acquired) rests primarily on data readouts from the pipeline.

That's not to say commercial execution for Loqtorzi is unimportant, but a peak sales opportunity of just $150 million per year in NPC isn't enough to singlehandedly salvage respect from investors or analysts. Data readouts hold the key to significantly increasing the peak sales opportunity by expanding beyond the rare cancer.

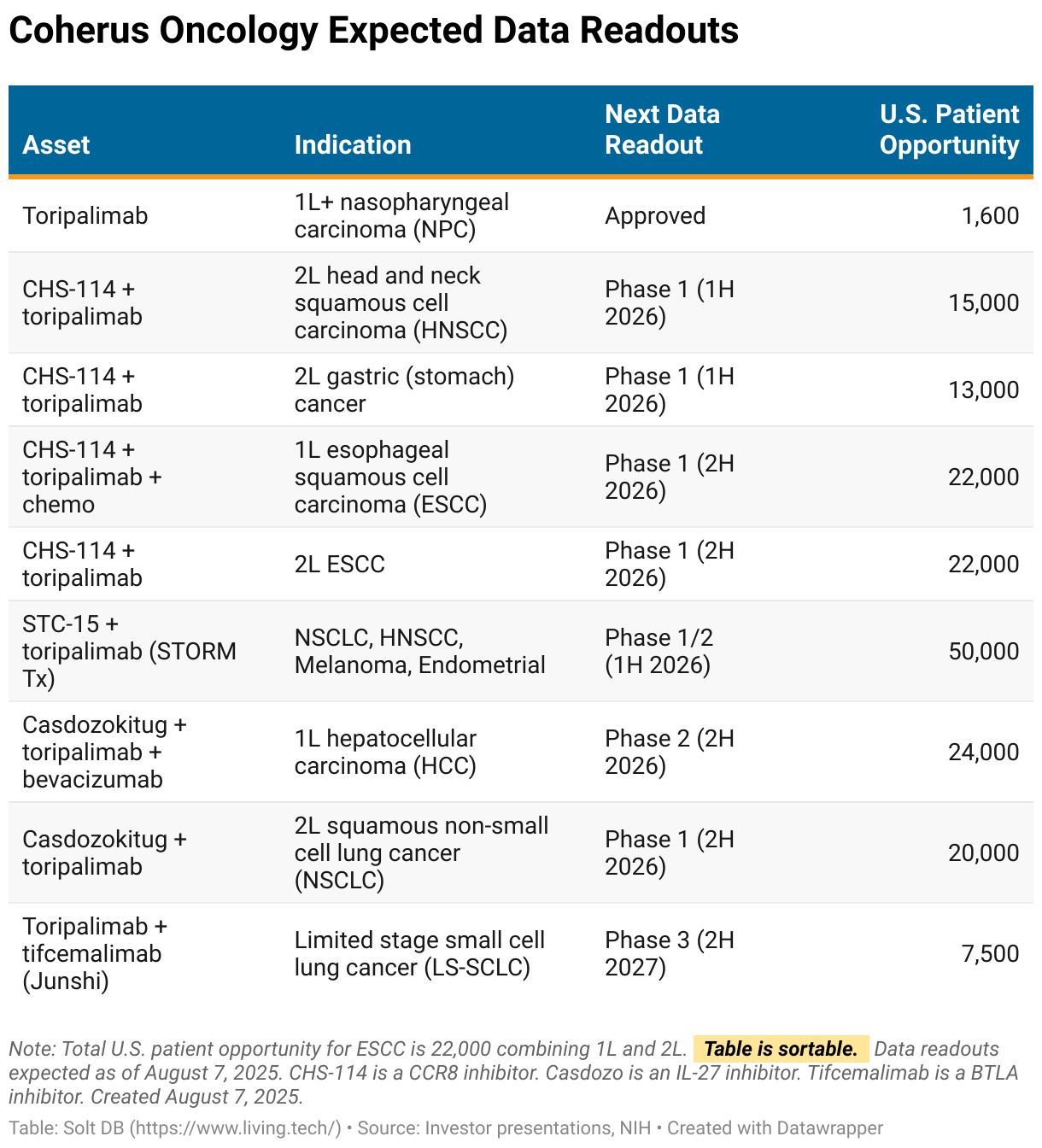

Let's walk through updates from pipeline assets. I've updated the table below with more realistic patient populations than communicated by Coherus.

CHS-114 (CCR8 inhibitor)

- Modeled valuation contribution: $32 million

Coherus is now planning to evaluate CHS-114 in four programs. That includes second-line (2L) head and neck squamous cell carcinoma (HNSCC), 2L gastric cancer, and 1L and 2L esophageal squamous cell carcinoma (ESCC). This development strategy focuses on a niche of head and neck cancers – a category that often includes NPC – that could collectively be worth over $1 billion in peak annual sales for Loqtorzi and CHS-114.

Management said it wants to explore additional tumor types with high CCR8 activity, but likely only with a collaboration partner. That includes colon cancer, which has proven difficult to reach with immuno-oncology combinations to date.

CCR8 opportunity to be driven by competitive landscape

It's important to keep in mind that all data readouts for CHS-114 will be from early-stage, dose-finding phase 1 studies. These programs will not demonstrate their peak efficacy or duration of response (DOR) in 2026. That could lead to volatility or a lack of excitement once data readouts cross the news wires.

This is why an escalating barrage of data readouts from the competitive landscape will be very important. Between now and the annual American Society of Clinical Oncology (ASCO) meeting in late May 2026, investors should see data readouts from over half a dozen competitor programs. LaNova Medicines, Bristol Myers Squibb, AbbVie, Bayer, Roche, Gilead Sciences, and Amgen are among those chasing the opportunity.

If data readouts from the competitive landscape are mostly favorable, then Coherus – the only independent company with a CCR8 inhibitor and PD-1 inhibitor – will be valued significantly higher than $100 million on sympathy alone.

Licensing opportunities

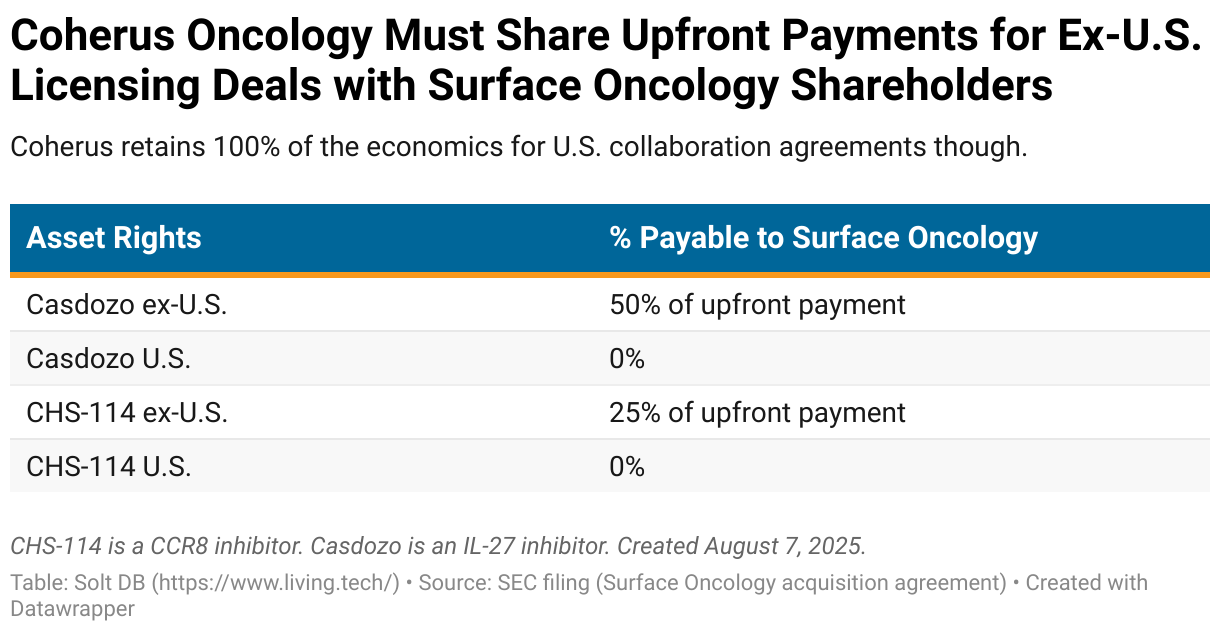

Both CHS-114 and casdozo have great licensing potential in the United States and internationally. The economic potential of any licensing deals will be dictated by geography and tumor type.

For example, international licensing agreements are generally not very lucrative. Less so for earlier-stage assets like CHS-114. That's because revenue opportunities tend to be significantly lower outside of the United States. There are caveats.

The development and commercial opportunity for CHS-114 could be very large even outside of the United States, which could result in meaningful upfront economics for Coherus. Similarly, casdozo is being developed for liver cancer, which is much more prevalent outside of the United States, potentially increasing the value of an international license.

Investors need to keep in mind that Coherus must pay a portion of upfront milestone payments for international licensing rights to former Surface Oncology shareholders: 50% for casdozo and 25% for CHS-114.

There's a catch.

Coherus does not have to pay any portion of domestic licensing deals, which will be more lucrative anyway. In other words, selling the U.S. rights to CHS-114 in colon cancer could generate meaningful upfront cash. Same for casdozo in pancreatic cancer or triple-negative breast cancer. These are large opportunities – exceeding over $1 billion in peak annual revenue – that the company cannot access on its own.

It wouldn't be in good faith, but Coherus could also structure the deals with a lower upfront milestone payment (shared with Surface Oncology) and load up on near-term development milestones like enrollment levels (not shared with Surface Oncology).

Management seemed to indicate interest in finding a collaboration partner to complete pivotal programs for casdozo in liver cancer, too.

I view these dynamics as potentially supportive of a higher valuation, but my base case is that Coherus will be acquired in full in 2026 if data readouts are favorable. Still, the ability to co-develop either or both assets would also be attractive to a potential acquirer.

Udenyca sales milestones

Coherus can earn two $37.5 million ($75 million total) milestone payments from Intas Pharma if Udenyca reaches certain cumulative sales levels.

- $37.5 million if cumulative net sales of Udenyca reach at least $300 million in four consecutive quarters from Q3 2025 to Q3 2026. There are five quarters in that span.

- $37.5 million if cumulative net sales of Udenyca reach at least $350 million in four consecutive quarters from Q3 2025 to Q1 2027. There are seven quarters in that span.

I think the first milestone payment is possible to achieve, which would result in an extra $37.5 million in cash available by the end of 2026. That won't be enough to fund further development of the pipeline, but it would buy time to find partners or suitors and lessen dilution risk -- at a fortuitous time.

News Flow & Modeling Insights

(Refined with minor adjustments.)

The current model makes the following assumptions:

- Full-year 2025 Loqtorzi revenue of $44.280 million (previous: $45.462 million).

- The pipeline contributes $206 million to the modeled valuation, including $184 million from casdozo and $32 million from CHS-114. The value of the latter can rise from data readouts in the competitive landscape in the near future.

Margin of Safety & Conviction

Coherus Oncology is considered a Future Compounder position with the following Conviction rating.

- 1 = High

- 2 = Above Average

- 3 = Average

- 4 = Below Average

The estimated fair valuation based on my current model is below:

- Market close August 7: $0.88 per share

- Modeled Fair Valuation: $3.20 per share

- Allocation Range: Up to 10%

Coherus Oncology reported 116.227 million shares outstanding as of July 31, 2025. The modeled fair valuation above assumes 118.726 million shares outstanding, which is equivalent to 2.1% dilution.

The fully-diluted basis for Coherus BioSciences (the share count used to determine the share price for an acquisition) is 148.674 million shares.

Further Reading

- August 2025 press release announcing Q2 2025 operating results

- August 2025 regulatory filing (10-Q) detailing Q2 2025 operating results

- July 2025 research note previewing Q2 2025 earnings across the coverage ecosystem

- May 2025 research note analyzing Q1 2025 operating results

.svg)

.svg)

.svg)

.svg)

.png)

.svg)

.png)

.svg)

.svg)

.svg)