.svg)

Half of my job is to provide objective analysis for investors. The other half is hand holding, squeezing you tightly, and telling you how pretty you are in a soft, comforting voice.

You are so beautiful today.

Is it disappointing that Coherus BioSciences declined to provide full-year 2024 revenue guidance on the year-opening call with analysts? Absolutely.

On the one hand, being cautious makes sense. The pegfilgrastim market is in flux from multiple angles. After being fiercely competitive in recent years, the seven-product market is turning into a three-horse race. Meanwhile, the Udenyca franchise has twice the insurance coverage in 2024 compared to 2023, and the launch of Udenyca Onbody will scramble pricing for 40% of total units sold. The new formulation launched on February 21, while Loqtorzi launched on January 2 and needs time to gain insurance coverage and be vetted by major hospital systems. It can be difficult to make meaningful projections with only weeks of data for the two most important products.

Management might also be a little shy after issuing its infamous full-year 2026 revenue guidance of at least $1.2 billion two years ago and walking back full-year 2023 revenue guidance at the end of last year.

On the other hand, the stock will be driven by commercial execution in 2024. Without revenue guidance, analysts and investors might find it difficult to justify a meaningfully higher share price, especially given the low levels of confidence in the business by Mr. Market.

Alas, fear not my beautiful investors. The core business exited 2023 with healthy momentum, while a slew of painful one-time decisions in recent months will ensure Coherus BioSciences exits 2024 on solid footing. More patience is required, but I do expect an inflection point in the share price this year.

By the Numbers

Investors need a heavy dose of context and nuance to parse through the year-over-year financial comparison.

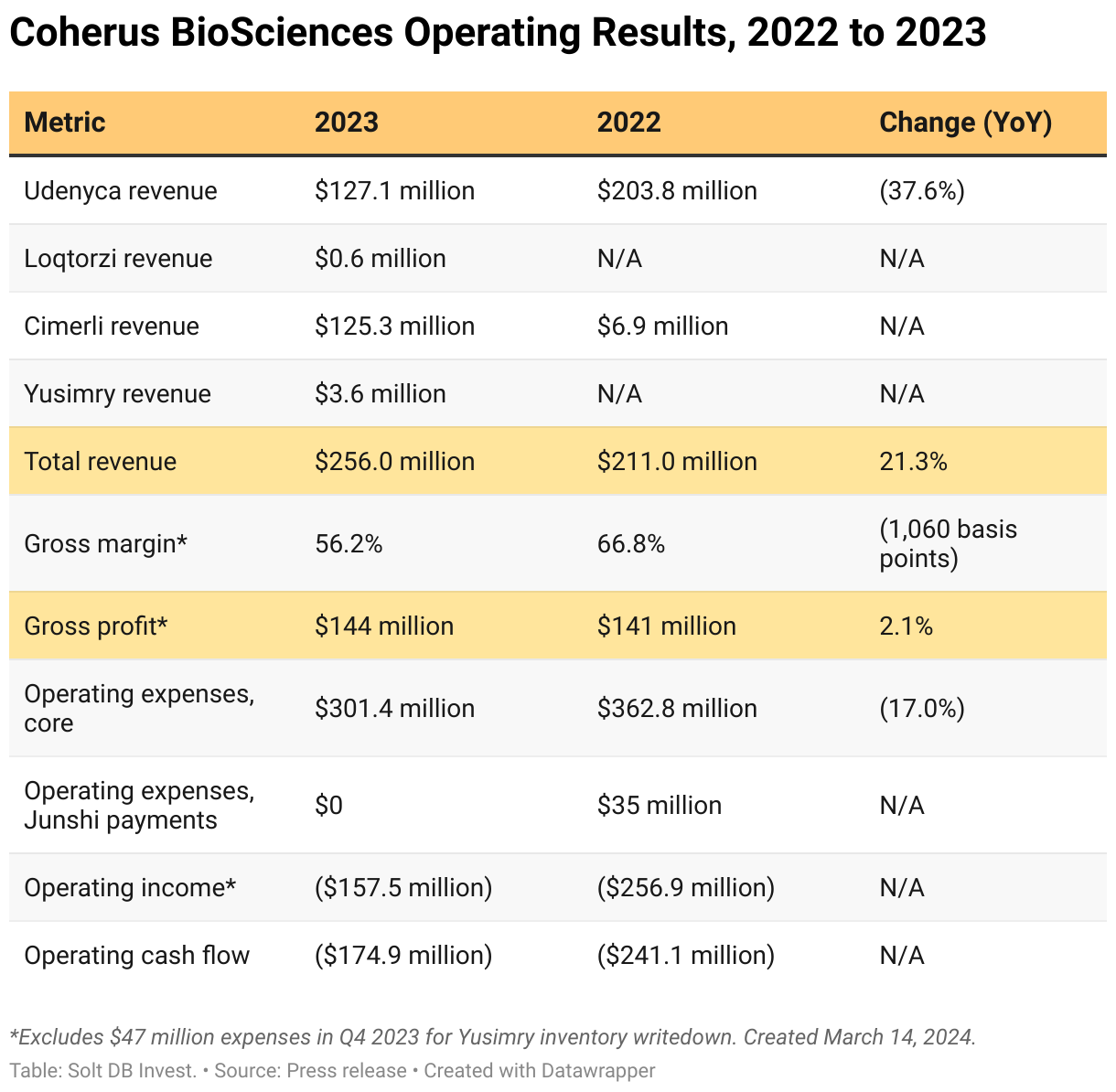

Coherus BioSciences delivered full-year 2023 revenue of $256 million, up 21% from $211 million in the prior year. Of course, that masks contributions from individual products. Revenue from the Udenyca franchise dropped by $76.7 million while revenue from Cimerli increased by $118.4 million.

The business delivered full-year 2023 gross profit of $144 million, up just 2% from $141 million in the prior year. That's because overall revenue growth masks the quality of revenue from individual products. Cimerli contributed a gross margin of about 42% last year, compared to 85% for Udenyca.

The gross profit and gross margin figures above and below exclude a one-time $47 million charge in the fourth quarter of 2023 related to Yusimry, primarily driven by a write-off of inventory (bad) and partial recognition of supply commitments for the year ahead (good). Excluding this charge provides a clearer picture of the underlying business.

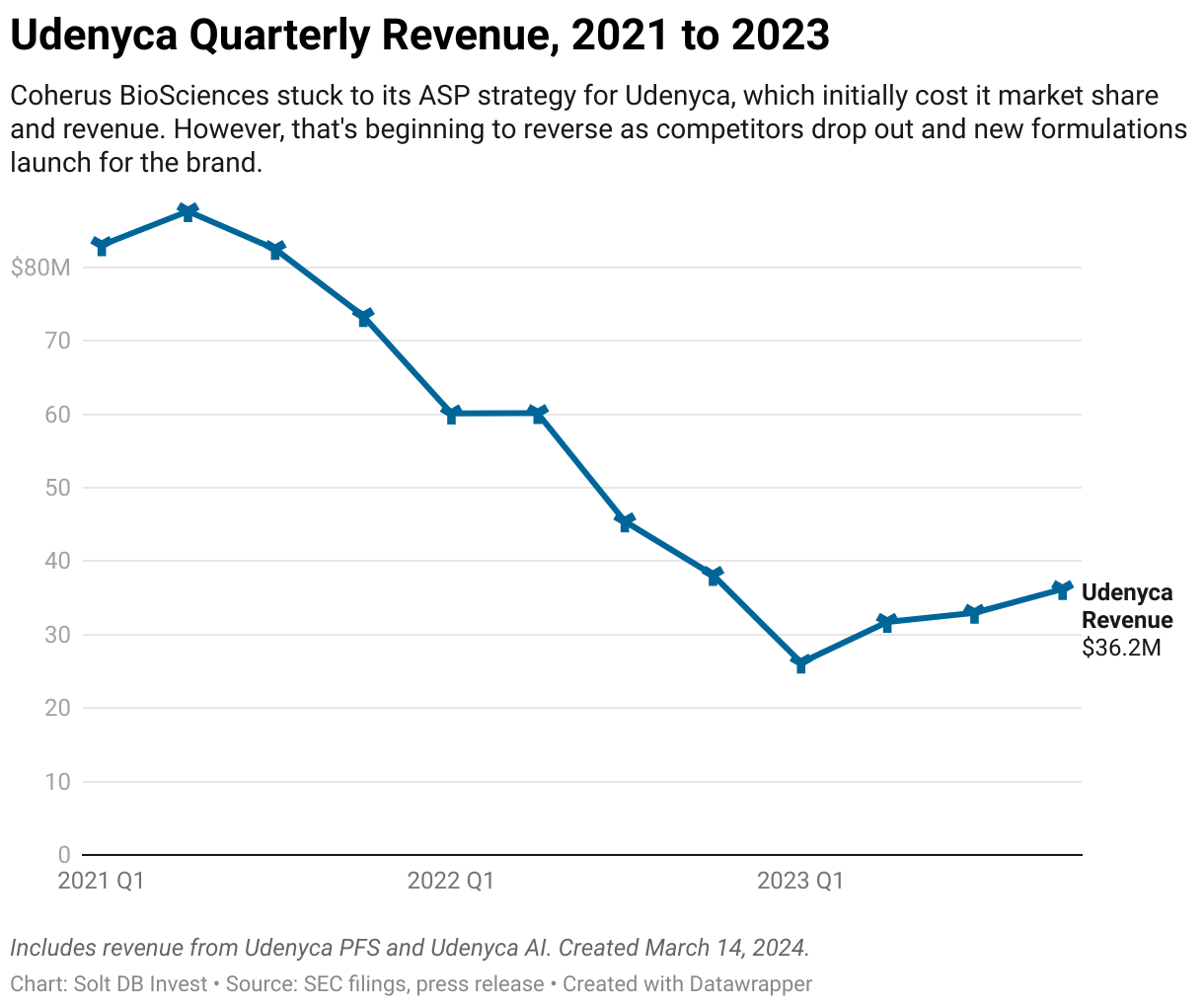

The full-year comparison also masks the trajectory of the Udenyca franchise over the course of 2023, as revenue grew by double digits each quarter. The franchise grew its market share from 11.5% at the end of March to 17.3% at the end of December. I estimate a market share of at least 28% by the end of March 2024. Meanwhile, total revenue grew 10% from the third quarter to the fourth quarter although total units sold increased only 7% in that span, signaling an increase in average selling price (ASP) ahead of the launch of Udenyca Onbody.

Around the Horn

Coherus BioSciences completed the sale of the Cimerli franchise and commercial infrastructure on March 1, which netted the company $170 million plus $17.8 million for inventory. An estimated $175 million will be used to paydown its $250 million term loan, leaving the business with a $12.5 million increase in cash. That essentially neutralizes the $12.9 million operating cash burn from the fourth quarter.

Management also announced a reduction in force of 30% that began in March 2024, which includes individuals dedicated to ophthalmology assets such as Cimerli.

The business began 2024 with $117.8 million in cash, which suggests it will likely need to raise additional capital as products ramp. Available options include a public offering, a private placement, drawing against an available $100 million credit facility, selling international rights to drug candidates such as Casdozo, or some combination. If Udenyca Onbody launches unimpeded, then it will be possible to not raise capital, but that would be cutting it dangerously close.

Udenyca franchise (pegfilgrastim biosimilar)

Discussed in detail in the next section, including insights into our expectations for and the market dynamics of Udenyca Onbody.

Loqtorzi (toripalimab, anti-PD-1/L1)

Management said Loqtorzi has met expectations through the first eight weeks of launch, although the launch seems a little slow according to my analysis. New drug launches are predictably unpredictable.

Coherus BioSciences noted 59 accounts have ordered Loqtorzi since launch on January 2. For perspective, 80% of the product's revenue potential will come from roughly 2,200 accounts.

There are no alarm bells going off. It's only been eight weeks and this is a relatively rare cancer. Loqtorzi is still acquiring insurance and reimbursement coverage and being vetted by hospital systems. It'll take two to three quarters to begin seeing meaningful progress and revenue generation. Those decisions are more procedural at this point, especially considering the product's preferred status in treatment guidelines.

The National Comprehensive Cancer Network (NCCN) establishes guidelines for various oncology treatments. Loqtorzi plus chemotherapy is the only immunotherapy with a Preferred Category 1 status for first-line nasopharyngeal carcinoma (NPC), while Loqtorzi monotherapy is the only treatment option (among any possible treatment) with Preferred Category 1 status for later lines of therapy.

The expectation is still for Loqtorzi to leverage the company's existing commercial infrastructure, including account overlap with Udenyca, and the internally-built NPC patient network developed prior to launch. Solt DB Invest expects Loqtorzi to generate full-year 2024 revenue of $35 million to $45 million ($40 million midpoint).

Yusimry (adalimumab biosimilar)

Management has designated Yusimry a non-core asset, primarily because it falls outside of oncology. The drug product generated fourth-quarter 2024 revenue of $2.2 million, bringing its total to $3.56 million since launching on July 1.

Coherus BioSciences took a one-time charge of $47 million during the fourth quarter (accounted for in the cost of goods sold), which included a write-down of inventory due to the slower-than-expected mechanics of the adalimumab market. The company had 500,000 units ready to go at market launch, but has sold just 12,200 units through the end of 2023, according to our analysis.

It may not be comforting, but everyone has been caught off guard by AbbVie's stranglehold on the market and pharmacy benefit managers (PBM). There were eight adalimumab biosimilars on the market in 2023. The product with the highest market share was Amgen's Amjevita at a whopping 0.99% of all units sold, representing full-year 2023 revenue of $126 million. Amjevita launched six months before most other biosimilars and was the only biosimilar available for the full calendar year.

Solt DB Invest expects Yusimry to generate full-year 2024 revenue of roughly $15 million, which could be somewhat conservative given the current trajectory. It's also important to note the $47 million charge taken in the fourth quarter also accounted for partial recognition of firm purchase commitments, meaning buyers securing supply for 2024.

I expect Yusimry will be divested or outlicensed eventually, although that'll be difficult to do until revenue begins ramping significantly in 2025. A partnership with Walmart, Kroger, Albertsons, Publix, or even Amazon, all keen to develop direct pharmacy alternatives to PBMs, is an option. Sandoz pulled off a similar partnership with its adalimumab biosimilar, Hyrimoz, with a new CVS Health subsidiary called Cordavis. To simplify the potential strategy going forward, it would be similar to how small molecule drugs -- like allergy medicines or pain medications -- are sold by store brands, just for more complex biologic drugs.

Cimerli (ranibizumab biosimilar)

Although Cimerli has been divested, it's another example of the company's excellent track record of commercial execution.

Coherus BioSciences guided for full-year 2023 revenue of at least $100 million for the product, but delivered $125.3 million in revenue. Solt DB Invest expects Cimerli to generate full-year 2024 revenue of roughly $30 million, all recorded during January and February. This will be accounted for as non-core revenue going forward in our analysis of the business, and likely from the company itself.

Forecast & Modeling Insights

(No change.)

If the goal is to return to profitability and positive cash flow, then Coherus BioSciences needs to ruthlessly prioritize operating efficiency. That can be accomplished by focusing on the quality of revenue, growing gross profit, and optimizing operating expenses against the backdrop of clinical trial requirements for the emerging pipeline.

The business made meaningful progress improving operating efficiency last year, although 2022 was a particularly inefficient year, which makes comparisons more favorable. From 2022 to 2023:

- Gross profit increased by $3 million

- Operating expenses (excluding the $35 million payment to Junshi Biosciences in 2022) decreased by $61.4 million

- That's an improvement of $64.4 million.

The trend is no fluke, however. Investors can expect significant progress once again in 2024. From 2023 to 2024, using our current 2024 model that assumes Udenyca Onbody generates no revenue:

- Total revenue will be essentially flat at $260 million, compared to $257 million in 2023

- Gross profit will increase by $38.9 million, due to higher quality of revenue in the absence of Cimerli

- Operating expenses (including a $12.5 million payment to Junshi Biosciences in Q2 2024) will decrease by $31 million.

- That's a modeled improvement of $69.9 million.

To be clear, our current 2024 model as of this writing excludes contributions from Udenyca Onbody. If we include our projections for Udenyca Onbody, then the improvement in operating efficiency is more striking.

- Total revenue will grow at least 25% to at least $322 million, compared to $257 million in 2023

- Gross profit will increase by at least $88 million, due to higher quality of revenue in the absence of Cimerli

- Operating expenses (including a $12.5 million payment to Junshi Biosciences in Q2 2024) will decrease by $31 million.

- That's a modeled improvement of at least $119 million.

In this scenario, Coherus BioSciences would achieve profitability by the fourth quarter of 2024. The milestone would be driven by the advantageous setup for Udenyca Onbody, although there is some uncertainty about how quickly it can ramp.

Udenyca Onbody strategy is a first among biosimilars

Solt DB Invest estimates the U.S. market opportunity for pegfilgrastim products – prefilled syringe (PFS), autoinjector (AI), and on-body injector (OBI) formulations – at roughly $1.29 billion in 2024. This is significantly lower than the bullshit market research reports you can Google, but those suck anyway.

Of the nearly 1.2 million total pegfilgrastim units sold each year, roughly 480,000 units are OBI formulations. All these unit sales have historically went to Amgen's Neulasta Onpro product, which was the only OBI formulation available through the end of 2023.

The launch of Udenyca Onbody will scramble the market for good. Although it's technically a biosimilar, it will be viewed by patients and doctors as a novel product thanks to a key device innovation: administration time.

Whereas Neulasta Onpro administers pegfilgrastim in 45 minutes, Udenyca Onbody administers pegfilgrastim in 5 minutes. That's a significant convenience advantage. It's also the first time a biosimilar improves upon an originator product.

We're in uncharted territory. However, the uncertainty arises because Udenyca Onbody has a higher selling price than Neulasta Onpro. That's not new; all Udenyca formulations have a higher selling price than Neulasta. But it could impede the launch trajectory.

How quickly Udenyca Onbody captures market share will be determined by the success of management's strategy, which is to compete on the brand rather than the price. That's also a first for biosimilars, so it's difficult to predict the outcome or pace of progress. As of this writing, the strategy appears to be working – quite well.

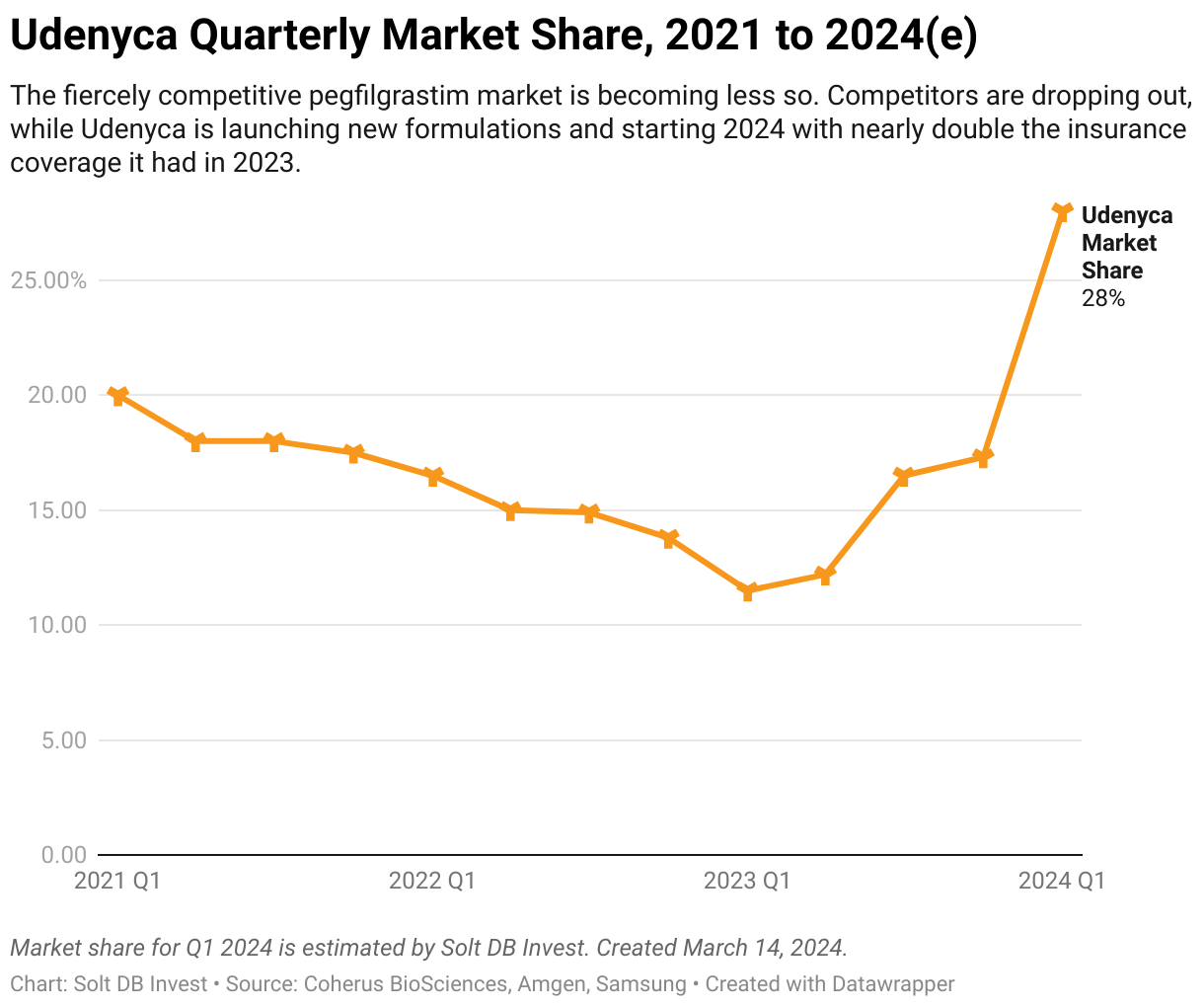

Coherus BioSciences resisted reducing the average selling price (ASP) of Udenyca products from 2021 through 2023 despite fierce competition. The idea was to protect the long-term value of the brand as it awaited the launch of Udenyca Onbody.

But it had a devastating cost: Udenyca's market share dropped from over 20% in the first quarter of 2021 to just 11.5% in the first quarter of 2023. That turned out to be the low-water mark. According to market data, the Udenyca franchise had a 26% market share as of March 1, 2024. This was driven by increased market share for Udenyca PFS, an increase in uptake for Udenyca AI, and possibly from initial orders for Udenyca Onbody (although it only contributed for nine of 28 days in this market share calculation).

Management was also proven correct that competing on price was unsustainable.

- Ziextenzo from Sandoz was the third pegfilgrastim biosimilar to launch in late 2019. It did so with an aggressive ASP strategy that saw it become the market share leader during 2022 at 18%. However, it ended 2023 with a market share of 1.2%.

- Nyvepria from Pfizer was the fourth pegfilgrastim biosimilar to launch in early 2021. It initially had a much higher ASP than any other product available, but ended 2023 with the third-lowest ASP of seven total products and a market share of just 6%.

- Stimufend from Frensenius Kabi and Fylentra from Amneal Pharma each launched in 2023, but ended the year with just 1.2% market share combined.

The only products that realized market share growth in 2023 were Neulasta from Amgen, Fulphilia from Mylan, and Udenyca – the first three pegfilgrastim products to launch. The two leading products by market share are Fulphilia and Udenyca, which have the highest ASP among widely available pegfilgrastim products. The bend-don't-break strategy worked for the trio, it just took a couple of years to see it through. The pegfilgrastim market is now a three-horse race.

In other words, pricing is an important factor in biosimilar markets, but not the only or most important factor.

As for Udenyca Onbody's trajectory, Solt DB Invest estimates that every 1% market share is equivalent to $9.33 million in annual revenue.

- If Udenyca Onbody captures 25% of the 480,000 unit opportunity for OBI formulations (representing 10% of the total market among all formulations), then it could generate $93.3 million in annual revenue.

- If Udenyca Onbody captures 50% of the 480,000 unit opportunity for OBI formulations (representing 20% of the total market), then it could generate $186.7 million in annual revenue.

I estimate Udenyca Onbody could end 2024 with 40% to 50% market share among OBI formulations, which would be equivalent to $62.2 million to $93.3 million accounting for the ramp up. The product would generate full-year 2025 revenue in excess of $125 million at a gross margin near 90%.

Margin of Safety & Allocation

Coherus BioSciences is considered a Growth (Quality) position. The current modeled fair valuation for the company based on our 2024 model is below:

- Market close March 13: $2.30 per share

- Modeled Fair Valuation: $10.71 per share

- Allocation Range: Up to 15%

Coherus BioSciences reported 111.364 million shares outstanding as of October 31, 2023. The modeled fair valuation above assumes 129.471 million shares outstanding, which is equivalent to 5% dilution.

Further Reading

- March 2024 press release announcing full-year 2023 operating results

- January 2024 research note discussing the sale of Cimerli to Sandoz

- January 2024 research note discussing the potential of Loqtorzi in combination studies

- December 2023 research note discussing the rationale for excluding Udenyca Onbody from our 2024 model

.svg)

.svg)

.svg)

.svg)

.png)

.svg)

.png)

.svg)

.svg)

.svg)