.svg)

When Coherus BioSciences reported first-quarter 2023 operating results, investors headed for the exits. Revenue tanked, expenses soared, and cash burn necessitated a painful capital raise at a depressed valuation. But the poor performance was expected. More importantly, it occurred just before an expected multi-year growth trajectory enabled by the launch of multiple products.

We wrote a research note with the headline, "Coherus BioSciences Just Hit the Bottom (Literally)." The first two sentences were blunt, but calming for investors with an eye on what was just over the horizon:

The first-quarter 2023 performance wasn't pretty, but it should mark the lowest quarterly revenue total of this decade. Cimerli sales began accelerating in April, the second pegfilgrastim formulation launches at the end of May, and the launches of Yusimry (July 1, 2023) and toripalimab (expected in the third quarter) will jumpstart a multi-year growth trajectory.

Turns out, the first quarter performance really did mark the bottom – but the recovery was much faster than expected.

Investors shouldn't get cocky just yet. A higher-than-average amount of uncertainty remains, but that's not unexpected in the context of a business ramping multiple products in multiple markets. If the team continues to execute, then this is a potential career making investment for individual investors in the years ahead.

By the Numbers

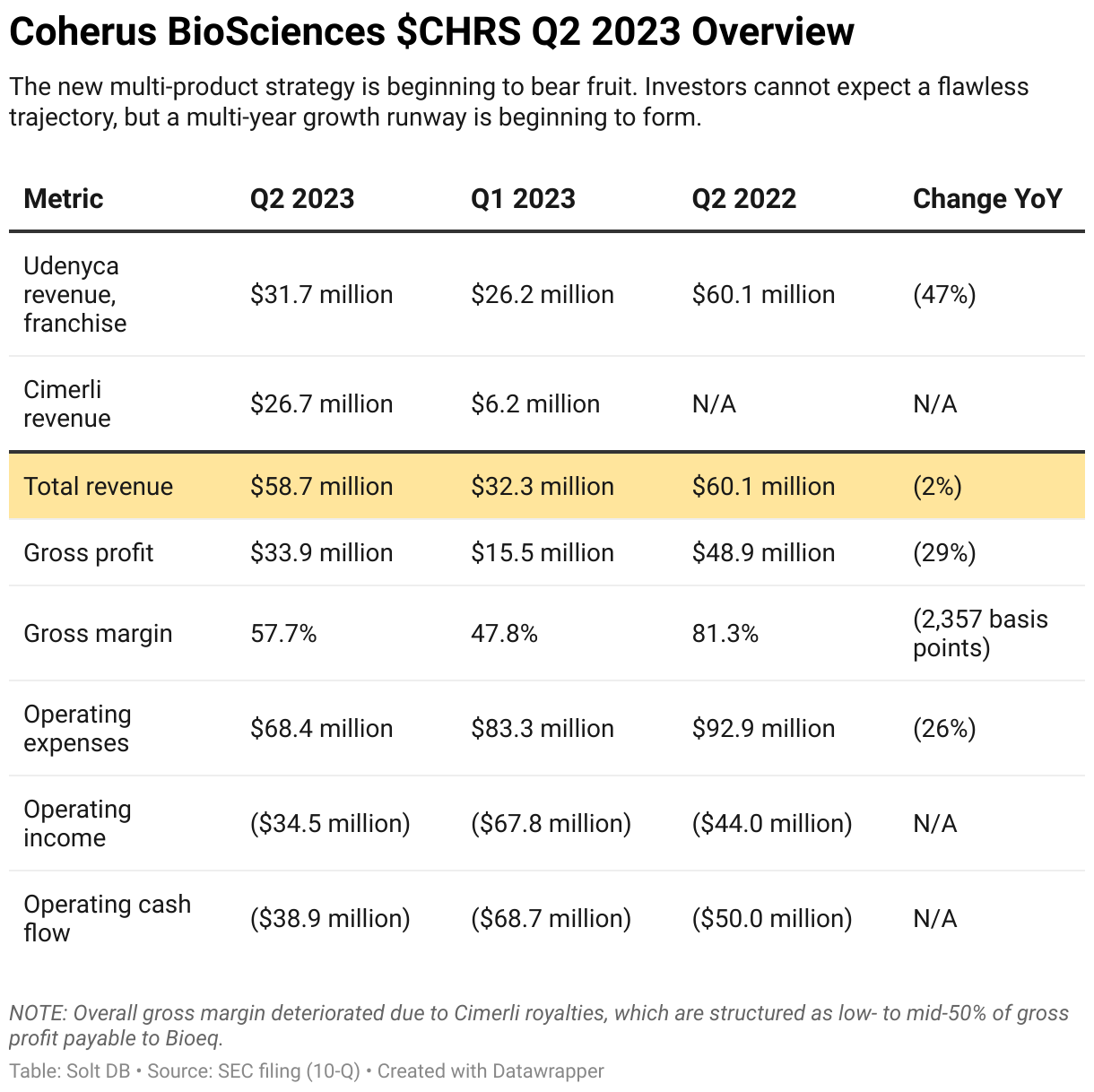

Coherus BioSciences emphatically put the first three months of the year behind it with a solid second-quarter 2023 performance. Total revenue jumped 81% in the second quarter compared to the first quarter. That was driven by a 333% leap in Cimerli revenue enabled by a new product-specific Q-code that went into effect on April 1. The Q-code enables faster reimbursement for ophthalmology offices, which helps doctors manage cash flow and makes them more likely to use a given product. (Fun fact: Coherus BioSciences owns the SEO term "Q-code reimbursement" from its Cimerli press release in early 2023.)

The Udenyca franchise also enjoyed a 21% increase in revenue from the first quarter. Although the autoinjector (AI) formulation launched in June, the prefilled syringe (PFS) formulation drove the growth with a surprising 10% increase in prescription volumes.

This is an early and encouraging sign that the company's controversial strategy to maintain pricing power, which cost it significant market share, was the correct move. Udenyca PFS had the highest average selling price (ASP) in recent years – even higher than Neulasta, the originator product – so Coherus BioSciences could charge even higher prices when Udenyca AI and Udenyca On-Body Injector (OBI) launched in the future. Well, the future is now, and the strategy appears to have worked. The Udenyca franchise saw its market share increase to 12.2% in the second quarter vs. 11.5% in the first quarter, marking the first significant increase in almost two years.

The business outperformed Solt DB Invest models for revenue with $58.7 million (vs. $45.3 million) and operating expenses with $68.4 million (vs. our lazy estimate of $75 million) during the quarter. That led to sharply improved operating losses and operating cash outflows.

On the conference call management toyed with analysts who asked if Coherus BioSciences would increase revenue guidance, which it left unchanged at "more than" $275 million for 2023. Solt DB Invest now expects at least $301 million in revenue for the year vs. $266 million across estimates from Wall Street analysts.

Those poor bastards.

Odds and Ends

There are a handful of new or refined data points guiding our updated modeling:

Cimerli (ranibizumab)

- The asset is absolutely crushing the competitive landscape thanks to excellent commercial penetration, near-perfect execution of the commercial strategy, and interchangeability status (it matters more in ophthalmology markets).

- Over 65,000 doses of Cimerli have been administered since market launch in October 2022.

- Coherus BioSciences ended June with 321 accounts, which marked a 75% increase from the prior quarter. It ended July with 412 accounts.

- The product went from 4.1% share of prescriptions in the first quarter to over 17% in the second quarter.

- Most importantly, the accounts ordering have a combined market share of 42% of prescriptions, which is a strong indication that revenue growth will continue for the foreseeable future. That might wobble a bit when exclusive interchangeability status expires in 2024 and more ranibizumab biosimilars (not necessarily interchangeable) enter the market, but revenue could grow by healthy double-digit rates next year.

Yusimry (adalimumab)

- Yusimry launched on July 3 into a highly competitive landscape.

- It's still too early to gauge how market formation will shake out between biosimilars and Humira, low-priced biosimilars and high-priced biosimilars, and so on.

- Management pleaded for patience. It expects a linear ramp of revenue (no exponential ramp like Cimerli) in 2023 and 2024, sees significant growth potential in 2025 if the drug pricing aspect of the Inflation Reduction Act (IRA) becomes law, and expects to achieve 10% market share by 2026 or 2027.

- Solt DB Invest might be a little too optimistic with an expectation of $108 million in full-year 2023 revenue for Yusimry. Depending on traction with the initial part of the launch strategy with Mark Cuban's Cost Plus Drug and specialty pharmacies, revenue could be as low as $49.8 million or as high as $108 million. Our 2024 model is likely to be reduced from the $274 million previously communicated to between $150 million and $200 million.

Toripalimab

- The U.S. Food and Drug Administration (FDA) has scheduled clinical trial site inspections in China for the second half of August. There is no approval decision date in place, but approval could be awarded in September or October.

- Junshi Biosciences will soon begin a multi-regional (global) phase 3 study of toripalimab in small-cell lung cancer (SCLC), which will include U.S. patients – a first for the asset. The data generated would be sufficient for FDA submission.

Immuno-oncology pipeline shuffling

- Coherus BioSciences expects to make multiple go / no-go decisions across its immuno-oncology pipeline in the next several months. Several assets are likely to be terminated as the company refocuses on SRF388 and SRF114 from the pending Surface Oncology acquisition.

- Importantly, once toripalimab earns FDA approval there will be significant new strategic space. The company will be able to shop toripalimab around for combination trials with external assets (to be completed by external companies) to begin building the foundation for a long-term expansion of the market opportunity.

Further Reading

- August 2023 press release announcing quarterly operating results

- August 2023 SEC filing (10-Q) detailing quarterly operating results

- June 2023 research note describing the company's low PD-L1 strategy for its immuno-oncology pipeline

- May 2023 research note analyzing first-quarter 2023 operating results

.svg)

.png)

.svg)

.png)

-cropped.svg)