.svg)

Most investors and analysts get bubbles wrong. I don't mean that no one sees them coming. Bubbles are not difficult to see, they're difficult to time.

Most investors and analysts err by focusing on valuations. These are a symptom of bubbles, not the driving force. This misplaced focus inevitably leads to arguments attempting to justify or refute valuations. "If the ACME Corp just grows earnings X% for Y years…" or "new technology Z will change the world."

But valuations don't stop or pop a bubble. In fact, rising valuations usually feed bubbles and cause them to grow ever larger. In the history of markets, asset valuations have caused bubbles to pop exactly zero times.

That's because bubbles are driven by human psychology, emotions, and narratives.

Margot Robbie and Selena Gomez didn't answer my texts, so here's Nobel Laureate Robert Shiller to define it:

Irrational exuberance is the psychological basis of a speculative bubble. I define a speculative bubble as a situation in which news of price increases spurs investor enthusiasm, which spreads by psychological contagion from person to person, and, in the process, amplifies stories that might justify the price increase and brings in a larger and larger class of investors, which despite doubts about the real value of the investment, are drawn to it partly through the envy of others' successes and partly through a gambler's excitement.

It's difficult to read that definition, look around today in October 2025, and argue we're not in a bubble.

How many companies issue press releases that the investing crowd holds up as execution against a commercial strategy, when in reality these are just a nice press release with little real-world substance to back it up? From satellite internet companies to small modular reactors, quantum computing to crypto, there's relatively little real-world execution supporting valuations for speculative stocks.

I've seen all the same press releases in biotech, especially industrial biotech. Press releases are nice. Signing up blue-chip partners is nice. Delivering is difficult. It's really, really difficult. Few if any of these trendy companies are delivering or executing where it matters.

So, what the hell do we do now?

Trigger Warnings and Scenario Analysis

Bubbles are driven by human emotion, valuations are the most obvious symptom, and the inevitable fall back to reality requires a trigger. That trigger is usually something financial, like lower-than-expected earnings expectations or increasing rates of fraudulent behavior.

What event(s) will shift the narrative from greed to fear this time?

How did we get here?

I'd argue we've experienced two distinct bubbles in the last five years: the pandemic bubble and the AI bubble. It was interrupted by a brief correction in 2022, then everyone lost their marbles when ChatGPT became a verb in early 2023.

It's easy to forget now, but investors were growing concerned about the stock market being overvalued (not a bubble) in 2019. Then the coronavirus pandemic flipped the script.

The United States flooded markets with stimulus. It dropped interest rates to near-zero, offered hundreds of billions of dollars in no-questions-asked PPP loans that were largely abused, bought tens of billions of dollars per month of mortgage-backed securities (MBS) well into 2022 (inflating a housing bubble and freezing real estate markets through at least 2025), and used yesterday's playbook to dismiss inflation as transitory. Oopsies.

The S&P 500 returned 16.3% in 2020 and 26.9% in 2021. While both were above the long-term average, the other important detail is that these returns were stacked on top of a 28.9% return in 2019.

Rage against the machine learning

Today, we have the AI bubble.

There are real uses of machine learning and large language models (LLMs), including when they can be repurposed for biotech R&D. These tools can augment capabilities or automate mundane tasks, although automation tools existed before ChatGPT et al.

But the bubble is obvious because we're throwing LLMs at every problem and holding up any results as groundbreaking. In simple terms, we're not yet properly matching the tools to the applications.

Generalized LLMs are cool, but they're not the future. Niche models fined-tuned for specific applications, including many smaller opportunities that aren't profitable for Google and Meta and OpenAI to pursue, could amplify the productivity of individual workers. But those workers will still need to be competent in their respective domains, especially because working with the tools is more about supervision than acting like every output was handed down from the heavens on stone tablets.

For some reason, until recently no one seemed to be calling bullshit on the limitations of the technology, or promises for $1 trillion investments, or really questioning anything. Heck, the fact we refer to fancy text prediction algorithms as "artificial intelligence" is a big part of the problem. People out there really think these algorithms can reason and think. These people drive cars and reproduce. Their kids are friends with your kids. It's scary.

As the joke goes:

When you're fundraising, it's artificial intelligence. When you're hiring, it's machine learning. When you're implementing, it's linear regression.

As for markets, by almost every valuation metric U.S. stocks are near the most expensive they've ever been. Valuations may not cause bubbles to stop or pop, but they are the single-most important factor determining future returns. That matters to investors.

It's not just stocks.

Housing prices continue to set new records, while affordability has only been worse in two years since 1990. Gold, silver, and platinum-group metals are regularly clinching new records. There's $3.6 trillion parked in cryptocurrencies. Prices of modern commodities like chocolate and coffee are lurching ahead due to a combination of tariffs, climate change, and slavery concerns.

American households have record asset allocations to equities (one of the single-best predictors of bubbles), while fund managers have the lowest level of cash on record. U.S. equities have a record valuation gap over international peers – and most international stock markets are actually outperforming U.S. indexes this year.

It is a little weird that so many are talking about an AI bubble suddenly. During the pandemic bubble of 2020 and 2021, I used to regularly perform Google searches for terms like "stock market bubble" and see who else thought similarly to me. There were hardly any articles being published on the topic. It was a lonely experience (video from mid-2021). I re-read Irrational Exuberance for comfort. I felt like I was crazy. I felt similarly this year, until recently. I've re-read Irrational Exuberance again.

Here's the thing: I'm not sure the AI bubble is going to stop anytime soon. We're rolling into earnings season, and unless the largest companies in the world reel-in future expectations, there's no reason they shouldn't deliver great performance. If they crush it in the next few weeks, then I'd bet that silences the recent bubble talk – and might even catalyze another run higher through the end of 2025.

Unfortunately, gravity will matter eventually. Two things that will seem obvious in hindsight:

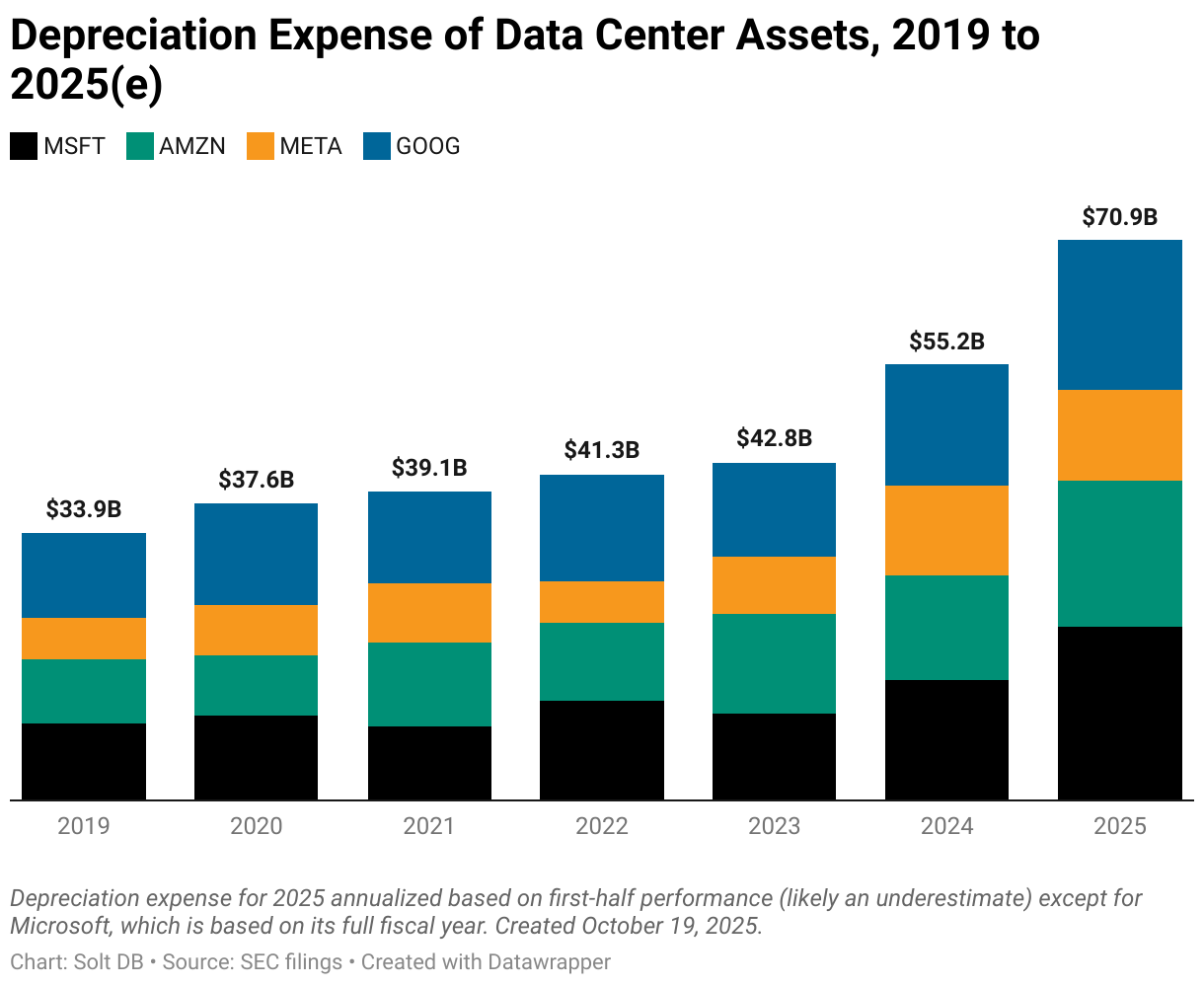

Depreciation expenses from data centers will eat tech earnings. In 2022, Alphabet reported depreciation expense on property and equipment of $13.5 billion. In 2023, that declined to $11.9 billion. Then the capex from the AI boom began to kick in. In 2024, this line item jumped 28% to $15.3 billion. In the first half of 2025, it increased 33% from the prior year and will likely end the year with even higher growth as more recent investments begin contributing.

This makes perfect sense. Data centers aren't long-lived assets; they have a useful life of three to five years. Companies building data centers are collectively spending hundreds of billions of dollars and likely overbuilding in the near term. What happens when it all has to be depreciated – and the ROI falls well short of expectations, meaning expenses grow faster than earnings?

It's a snowball rolling downhill.

Cloud segment booms will turn to busts. Although Microsoft, Google, Amazon, and others are being powered by strong earnings growth in their cloud computing business units, how much of that growth is sustainable in the near term?

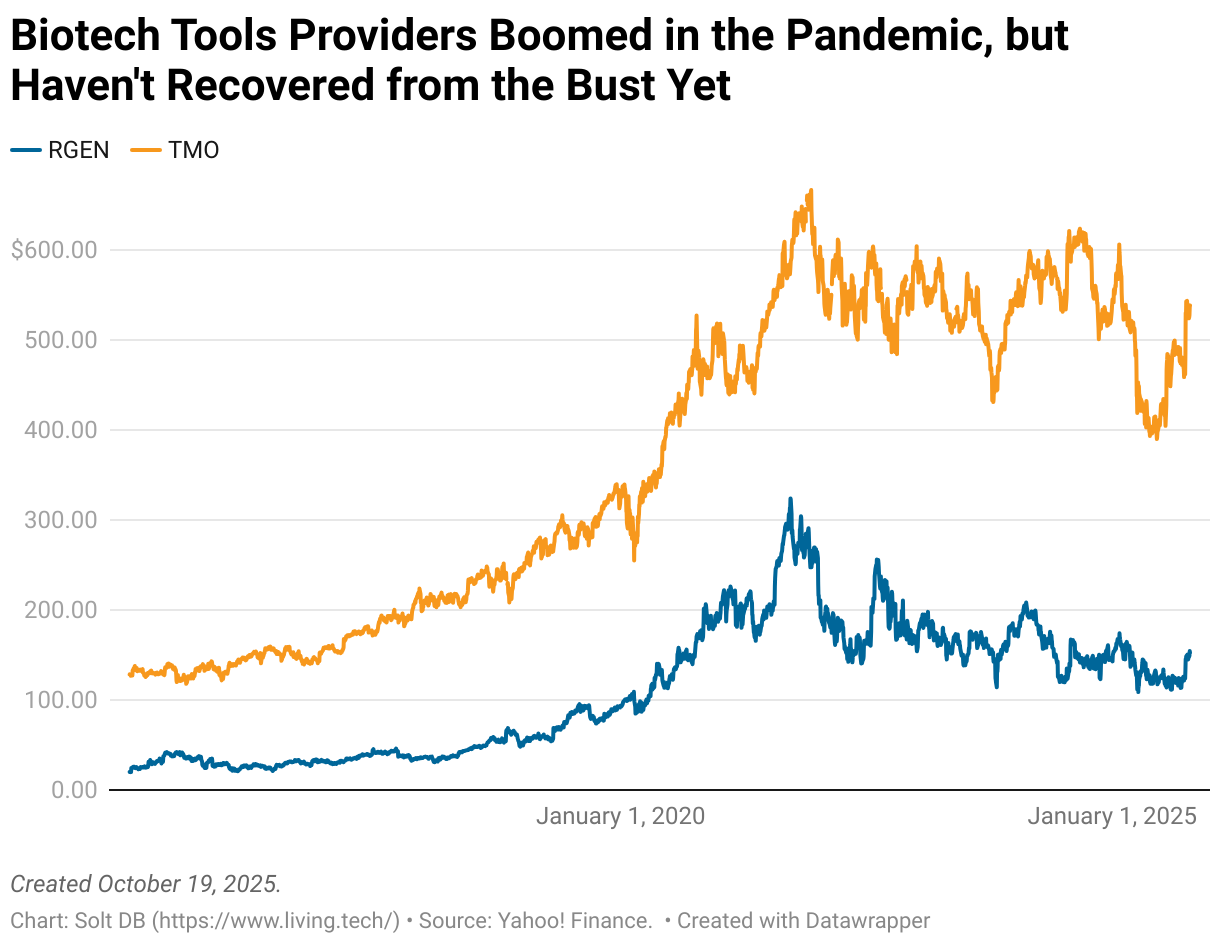

The current boom has eerie parallels to the pandemic bubble in biotech. Venture capital flooded markets, companies with a few mouse studies went public at excessive valuations, and the tools providers absolutely raked. When the music stopped and those companies ran out of Other People's Money (OPM), it decimated the startups and precommercial companies, but it also weighed on tools providers.

The latter group didn't go bankrupt. The sky wasn't falling. But they still haven't clawed back the lost revenue or reclaimed the record valuations of 2021. In fact, the speculative pandemic bubble was the worst thing that happened to them – over a decade of steady stock price increases has stalled out since 2020.

Cloud computing businesses will be more resilient than the Thermo Fishers and Repligens of the world, but how many artificial intelligence startups spending hundreds of millions of dollars of OPM (and juicing OpenAI revenue in the process) will be around in 2027? That'll weigh on a key profit engine for tech companies. It'll take time to squeeze out the excess.

Even if companies elect to take the largest-ever one-time charges in the history of capitalism, it'll take 12 to 24 months to normalize. Not cataclysmic, but quite different from the last decade of "stonks only go up." Importantly, it'll significantly reduce multiples from current levels. The stock market could drop over 30% from its peak.

Of course, for the AI bubble to deflate, it'll require a trigger – the Magnificent 7 reducing future expectations, unexpected failures in the financial system, economic hardship from a brutally difficult job market that's significantly worse than official numbers have let on since 2023, China's excess exports finally catch up to global economies, government debt crises, Elon Musk slips on a banana peel and falls into a recently-bored tunnel in Las Vegas… who knows!

Position Management During a Melt Up

The biotech ecosystem has been in a bear market since 2022. I launched Solt DB in May 2022 #nailedit. Interest rates increased in a very short period, which had derivative effects on capital flows in the bioeconomy. Those headwinds are still dragging the sector four years later.

The mere promise of lower interest rates has reawakened biotech stock prices in the last month or two. That makes sense – to a point.

On the one hand, biotech stocks are still generally undervalued. Coherus Oncology isn't worth $90 million. Arrowhead Pharma isn't worth less than $2 billion. Exact Sciences isn't worth less than Guardant Health.

On the other hand, if the Fed is cutting interest rates into a recession and/or deflation of the AI bubble forces a stock market correction, then biotech stocks aren't going to hold onto their gains from the ongoing melt up.

I won't be panic selling or going all cash like a luddite, but it might make sense to trim positions, lock-in gains at specific levels, take a breather, and reinvest when valuations drop during a correction. Here's how I'm thinking of current Finch Trades positions in chronological order from the start date.

To be clear, I would transparently communicate any trades I make – same as always.

Coherus Oncology

- When would I consider downsizing my position?: Above $4 per share in the near-term, potentially triggered by a short squeeze

- How much would I downsize?: Up to 50% of my total position

- Would I re-enter?: Yes, I want Coherus to be one of my core positions, especially ahead of data readouts in 2026. An acquisition of up to $1 billion is plausible in late 2026 or early 2027.

Shares of Coherus have suddenly reawakened after years of slumber and are now trading roughly at cash. The current valuation of $190 million would significantly undervalue the pipeline if enthusiasm for CCR8 inhibitors continues to rise, especially as a trickle of data readouts becomes a steady flow. The company should benefit from both external data readouts and its own.

Yet, somehow, short interest in the stock has barely budged. At the end of September 2025, roughly 28% of all available shares were sold short. The short ratio is an astronomical 22.5x – anything over 5x is considered high. This is how short squeezes are born.

There's not an identifiable trigger to unlock a short squeeze before data readouts in 2026, but licensing deals could do the trick. Comments from management hint that licensing deals could be announced before the end of 2025.

I would consider significantly downsizing my position in Coherus during a short squeeze. A share price over $4 apiece would be tempting, although given the short interest shares could leap significantly higher. To be clear, I'd plan on re-building the position, potentially much larger.

If enthusiasm for CCR8 assets grows in the next 12 months, then Coherus could be acquired for up to $1 billion ($8.33 per share on a fully-diluted basis). The fact the business is one of only four with an approved PD-1 inhibitor and a developmental CCR8 asset could introduce an even larger premium. Meanwhile, investors should temper their expectations for casdozo in liver cancer, but if the asset replicates prior results, then this could potentially rise to or be acquired for $2 billion or $3 billion.

Relay Therapeutics

- When would I consider downsizing my position?: This might be the only position I don't f*nch with.

- How much would I downsize?: Likely 0%

- Would I re-enter?: I would like to own as many shares as possible before mid-2027 – right before ReDiscover-2 might be stopped early for ethical concerns.

To be blunt, you don't find opportunities like Relay Therapeutics very often in your investing career. It's difficult to identify a precommercial drug developer that has the potential to grow into one of the largest on the planet. It's impossibly difficult to find one that trades at such a disrespectful valuation.

If zovegalisib lives up to my and the company's expectations, then it could be one of the fastest oncology drug launches ever. The asset could reach over $1 billion in revenue during its first full year on the market. You can count the number of drugs that have accomplished that on one hand – Keytruda, Ozempic, and Biktarvy aren't on the list. Achieving that in the second or third year would be rare, too.

This is a position I want to hold into the 2030s. I don't care what the share price is in 2025 or 2027. I just want to own a lot of shares; compounding will take care of the rest.

The best-case scenario in the long term is the worst-case scenario in the short term. If management stubbornly retains full economic rights to zovegalisib, then shares of Relay Therapeutics could get clobbered during a prolonged stock market and economic downturn. It would likely trade closer to cash, which will fall below $600 million by the end of 2025 and below $400 million by early 2027.

There's too much optionality though. The company still must announce data in the CDK-inhibitor naïve patient population (zovegalisib triplets). It has zero partnerships in place, which is highly unusual. It has two additional assets that can't be funded with cash on hand now, but represent meaningful potential given the clinical and commercial hypotheses. Relay has proven its strategy so far with its first two assets.

It would make sense to license the Fabry disease asset, which is the only asset outside of oncology. That would provide more breathing room to invest in pivotal studies for CDK inhibitor naïve patients (triplets), programs for vascular malformations, and the NRAS inhibitor asset. I would also expect the company to secure a large credit facility closer to the data readout for ReDiscover-2, but one could come sooner.

Exact Sciences

- When would I consider downsizing my position?: Above $70 per share. Exact Sciences is starting to bump up against my modeled fair value, but flipping to profitability and excitement for GRAIL's multi-cancer early detection tool could spur a significant run by the end of 2025.

- How much would I downsize?: Up to 100%

- Would I re-enter?: Exact Sciences would be a great position to re-enter or rebuild if shares fall sharply during a downturn.

Exact Sciences is one of my smallest Finch Trades positions, but shares have rallied in recent months closer to fair value. The business is strong, I see no signs that it'll weaken in 2026, and ample cash flow and (soon) profitability could be highly valued during a downturn.

Exiting this position has the highest potential to backfire. This is exactly the type of defensive position investors might value during a downturn. Cologuard is immune to a recession.

Then again, investors have demonstrated they have relatively loose trust or confidence in the business multiple times in the last 24 months. There have been multiple kneejerk reactions after earnings reports, only for investors to slowly move back in. Is everyone going to act rationally during a stock market crash? Yeah right.

The business has significantly less valuation risk than peers like Natera or Guardant Health, but it's objectively a step behind other MCED and liquid biopsy tools in the competitive landscape. That said, I wouldn't hesitate to re-enter during a correction.

Arrowhead Pharma

- When would I consider downsizing my position?: Above $45 per share would be tempting, or if there's a short-term pop on plozasiran's FDA approval in mid-November.

- How much would I downsize?: Up to 50%

- Would I re-enter?: Yes, this is one of the most promising drug developers on the planet. I would like it to be one of my core portfolio positions for the rest of the decade.

When you wield an RNA interference platform you can name your own price. Arrowhead has demonstrated the ability to secure upfront cash payments of over $100 million for assets across cardiometabolic diseases, neurology, muscular diseases, and rare diseases. It can target genes in tissues including liver, lungs, brain, muscles, and adipose tissues. It's about to begin a clinical trial for the first-ever bispecific RNAi drug, which could reset expectations for how cardiovascular disease is treated and one-day prevented.

I would find it very difficult to downsize my position.

At the same time, shares of Arrowhead Pharma have a bit too much momentum recently. If you zoom out, then it's obvious at least some of that is being driven by insatiable demand for Alnylam Pharmaceuticals. The big brother is now valued at an astounding $63 billion. Arrowhead Pharma looks pretty cheap by comparison even if it doesn't yet have the same commercial heft. If you want exposure to RNAi, then you don't have too many options.

That said, it wouldn't be surprising to see shares pop on FDA approval for plozasiran in mid-November. If Big Tech earnings shred any talk of an AI bubble, then the stock's momentum could continue. That could push shares beyond a reasonable valuation. Depending on the flow of economic data or speculative fervor, then I may sell half my position to lock-in the gains. Maybe.

Harmony Biosciences

- When would I consider downsizing my position?: After Q3 2025 earnings are reported in November

- How much would I downsize?: 100% (full exit)

- Would I re-enter?: No thanks.

The RECONNECT study didn't have the outcome we wanted, but being positioned in Harmony Biosciences before the data readout was an intelligent risk to take.

The commercial strength of Wakix wasn't being properly valued by Wall Street, while the odds of a positive outcome from RECONNECT were pretty good. My assessment was based on multiple independent studies showing the benefits of cannabidiol across autism, behavioral symptoms, pain, epilepsies, and of course the prior CONNECT study. The placebo effect was always the biggest risk, but running a meaningfully larger study in the patient population most likely to benefit should have reduced that risk. Management didn't even share results, so that all went out the window!

Nonetheless, the circumstances favored an investment. If the study was positive, then my position could've doubled or more. The study failed, but my position is down 14%. I will happily risk capital if I find opportunities like that again.

For example, when Dicerna Pharmaceuticals delivered mixed results for its first phase 3 study, shares fell 50% from their peak. That drug eventually earned FDA approval, the pipeline was stocked full of high-impact assets, and the company counted partnerships with Roche, Eli Lilly, Novo Nordisk, Boehringer Ingelheim, and others.

By comparison, Harmony Biosciences has cobbled together a questionable pipeline, has no blue-chip partners, and ZYN002 has no chance of reaching market. It's not often you get the insurance on a phase 3 study that Wakix provided.

I'm not too enthusiastic about the rest of the pipeline aside from the potent orexin-2 receptor (OX2R) agonist candidate, but that hasn't even entered clinical trials yet. Luckily, the business is trading near 9x earnings and 6x operating cash flow. It has a PEG ratio of 0.45. If Wakix doesn't implode for some unknown reason through the end of the year, then the stock will recover eventually.

Unlike the other positions above, shares of Harmony Biosciences are likely to perform better when markets are volatile. I expect to exit near my cost basis of $30 per share after Q3 earnings are reported in November. If I'm lucky, then maybe management can sell the business for a respectable premium – maybe $40 to $50 per share (below the modeled fair value).

Finch Trades Review

The Margin of Safety Dashboard is how I communicate the attractiveness of biotech stocks based on my research and modeling. Finch Trades is how I put my research into action with real money and 100% transparency.

As of market close on October 17, 2025, Finch Trades are underperforming the S&P 500 by 3.8%.

Of the 20 individual transactions in Finch Trades, 55% (11/20) are outperforming the S&P 500 and 75% (15/20) have a positive return. I haven't been able to invest consistently (the Margin of Safety Dashboard is designed for investing steady amounts each month), but am working on finding more income stability.

I've deployed $53,153 of capital in Finch Trades since initiation in April 2024, which has increased 15.5% to $61,403. Annualized returns are 10.2%.

Comparisons had I invested in other benchmarks:

- S&P 500 ($SPY): +19.3% to $63,411

- Nasdaq 100 ($QQQ): +25.6% to $66,748

- SPDR S&P Biotech ETF ($XBI): +22.0% to $64,859

- Ark Genomic Revolution Fund ETF ($ARKG): +30.0% to $69,108

I track benchmark comparisons for each individual transaction as if I had entered or exited that benchmark on the same day.

The timing and size of my Harmony Biosciences position has collided with the recent surge in value for the Ark Genomic Revolution Fund. Since entering my position in Harmony Biosciences, ARKG is up 37% and my position is down 14%. I expect this comparison will normalize with time as the recent surge in ARKG names fade with valuation concerns and Harmony recovers ground.

.svg)

.svg)

.svg)

.png)

.svg)

.svg)

.svg)