.svg)

Earnings season has started for the coverage ecosystem. You can find the confirmed dates for all companies in the quarterly Discord thread.

Starting this earnings season, I'll provide a preview for every company in the coverage ecosystem – even if formal coverage hasn't been introduced yet.

Potential High-Impact Updates

A high-impact update for a pipeline or portfolio has the potential to de-risk a business by removing uncertainty or forcing analysts to adjust expectations. These could be accompanied by larger stock moves or revised fair valuation estimates – in either direction.

Arrowhead Pharma

- Fiscal full-year 2025 earnings date not yet scheduled, but it will be later in November because it's a full-year update.

Biotech stocks are thawing from the biotech winter as investors begin dreaming of what interest rate cuts might mean for capital flows into the sector. The depth of the biotech winter, combined with a looming patent cliff for large pharma, has rapidly sprung high-quality precommercial drug developers to triple-digit gains in recent months. Arrowhead Pharma is one of the largest beneficiaries of the market's new biotech math.

The RNA interference drug developer spent most of 2025 laying the groundwork for its neurology pipeline. Deals with Sarepta Therapeutics and Novartis have generated $1.325 billion in upfront cash payments (including an upcoming $200 million payment from the former), while Arrowhead retained full rights to a next-generation asset for Alzheimer's disease. ARO-MAPT can be dosed subcutaneously and cross the blood-brain barrier, providing an intriguing convenience advantage over existing genetic medicines that require brain surgery or lumbar puncture to administer.

That would've been a stellar year for any drug developer, but I'm just catching my breath.

Arrowhead has important updates on the way for its complement-mediated diseases portfolio (CM-specialist Alexion Pharma was acquired for $39 billion in 2021), has yet to share details for its lead drug candidate in lung diseases, and has a next-generation asset for metabolic-associated steatohepatitis (MASH) that investors seem to have forgotten about. I wouldn't be surprised to see the latter two assets terminated or shelved for licensing.

Meanwhile, initial data readouts for obesity candidates ARO-ALK7 and ARO-INHBE should be ready before the end of 2025, although the preliminary data are unlikely to be very meaningful if we're being objective. The company made a great strategic decision to evaluate combinations with Eli Lilly's Mounjaro, which is a superior weight-loss drug to Novo Nordisk's Wegovy. Eli Lilly also hasn't been shy about deploying capital for acquisitions in genetic medicines. It passed on Dicerna Pharmaceuticals, so perhaps it takes the plunge to acquire Arrowhead in the coming years.

Still not done.

Recent stumbles in the alpha-1 antitrypsin (A1AT) disease landscape might resurrect the fortunes for fazirsiran, which is partnered with Takeda. Wave Life Sciences delivered underwhelming data for its RNA editing candidate that suggest higher doses might not deliver more benefit, a completely normal result for such a new therapeutic modality. As for gene editing approaches, Intellia Therapeutics spooked investors with a single case of grade 4 liver inflammation, forcing it to pause two studies. These developments don't change the fact that fazirsiran isn't an ideal treatment for A1AT, and negative reactions are likely an overreaction by investors, but they could change competitive dynamics to be more favorable for Arrowhead and Takeda. Fazirsiran continues to be excluded from my model.

Big breath.

Finally, Arrowhead is on track to earn its first-ever FDA approval before Thanksgiving. Plozasiran's application for treating familial chylomicronemia syndrome (FCS) has a PDUFA date of November 15. The application was submitted earlier this year, which should allow it to avoid any delays from the government shutdown, but investors cannot rule it out entirely.

The only other FCS treatment on the market, Tryngolza from Ionis Pharmaceuticals, generated Q3 2025 revenue of $31.8 million for an annualized run rate of $128 million. It's dosed every 4 weeks, whereas plozasiran is dosed every 12 weeks and has slightly better efficacy to boot.

The wrinkle is that Tryngolza is being prescribed off label for similar indications, which could also help plozasiran's commercial ramp in 2026, but the initial market opportunity is only so large. Although Arrowhead will still burn considerable sums of money next year, having a commercial product in the market – and building commercial infrastructure for future launches – will help change the narrative for the investment.

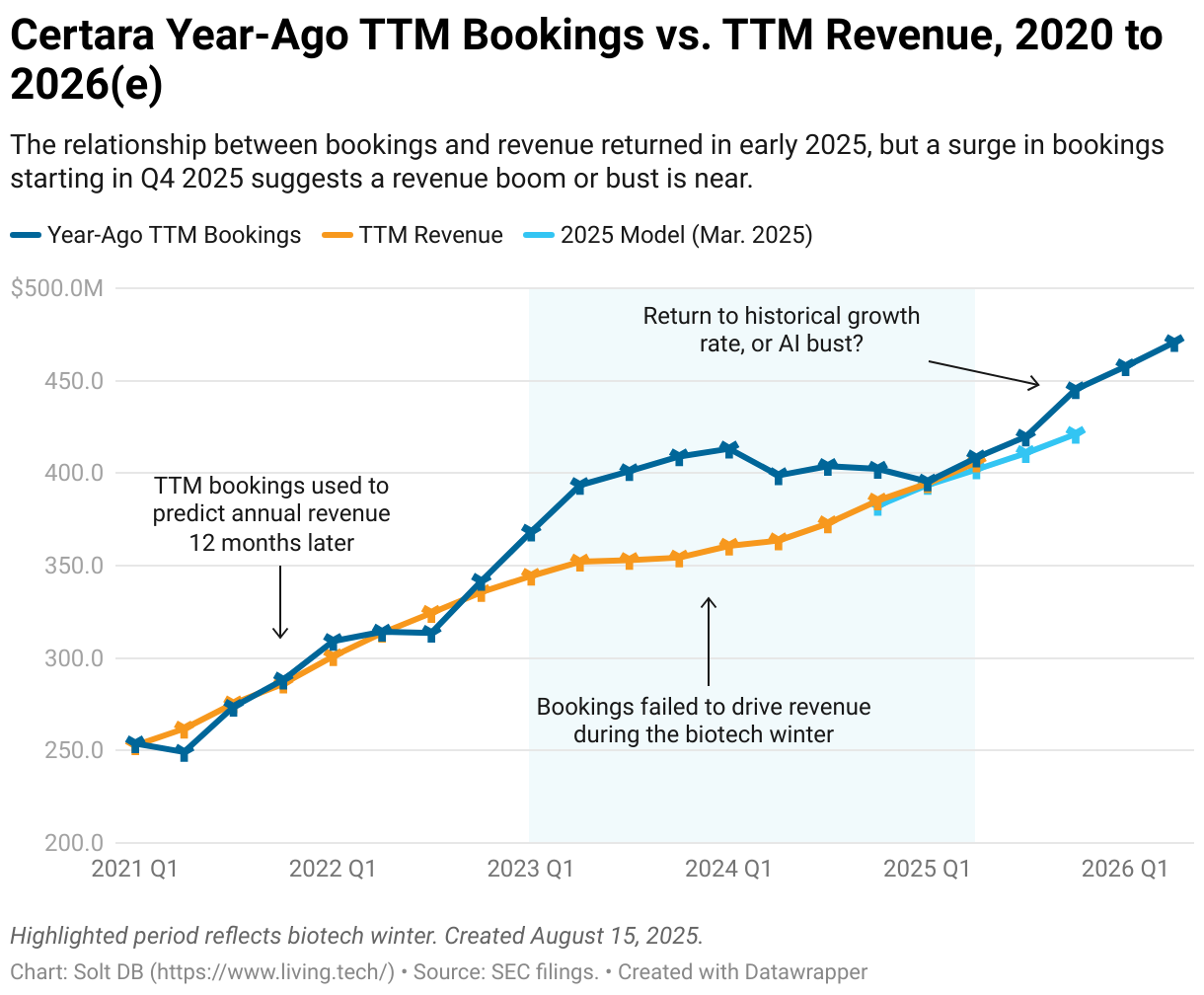

Certara

- Reports Thursday, November 6 after market close

- Good potential for an opportunistic earnings play

Whereas growth stocks have been surging on rate-cut optimism, Certara has already begun coughing up gains from an early-autumn ascent. Investors might be forgetting that all the biosimulation leader's customers are the ones benefitting from rate cuts.

As discussed last quarter, there appears to be a mismatch between full-year 2025 revenue guidance and the revenue predicted by bookings. A sizable mismatch.

First-half revenue trended meaningfully above guidance and my model. Management is either being conservative, needs to write-off an uncomfortable chunk of bookings from the Chemaxon acquisition, or investors are about to relive the pain of 2022.

Certara appears to be firmly on pace to at least meet full-year 2025 revenue guidance. It's important not to confuse the recent surge in biotech stock prices with a surge in biotech spending – that is definitely not happening yet. Still, third-quarter updates are usually when conservative management teams choose to increase guidance. It makes sense. By November, businesses have a good idea of performance for the calendar year.

I wouldn't be surprised to see Certara raise guidance and potentially demonstrate surging momentum as 2025 draws to a close. It could present a favorable risk-reward for investors looking for a short-term opportunistic trade, especially from current levels.

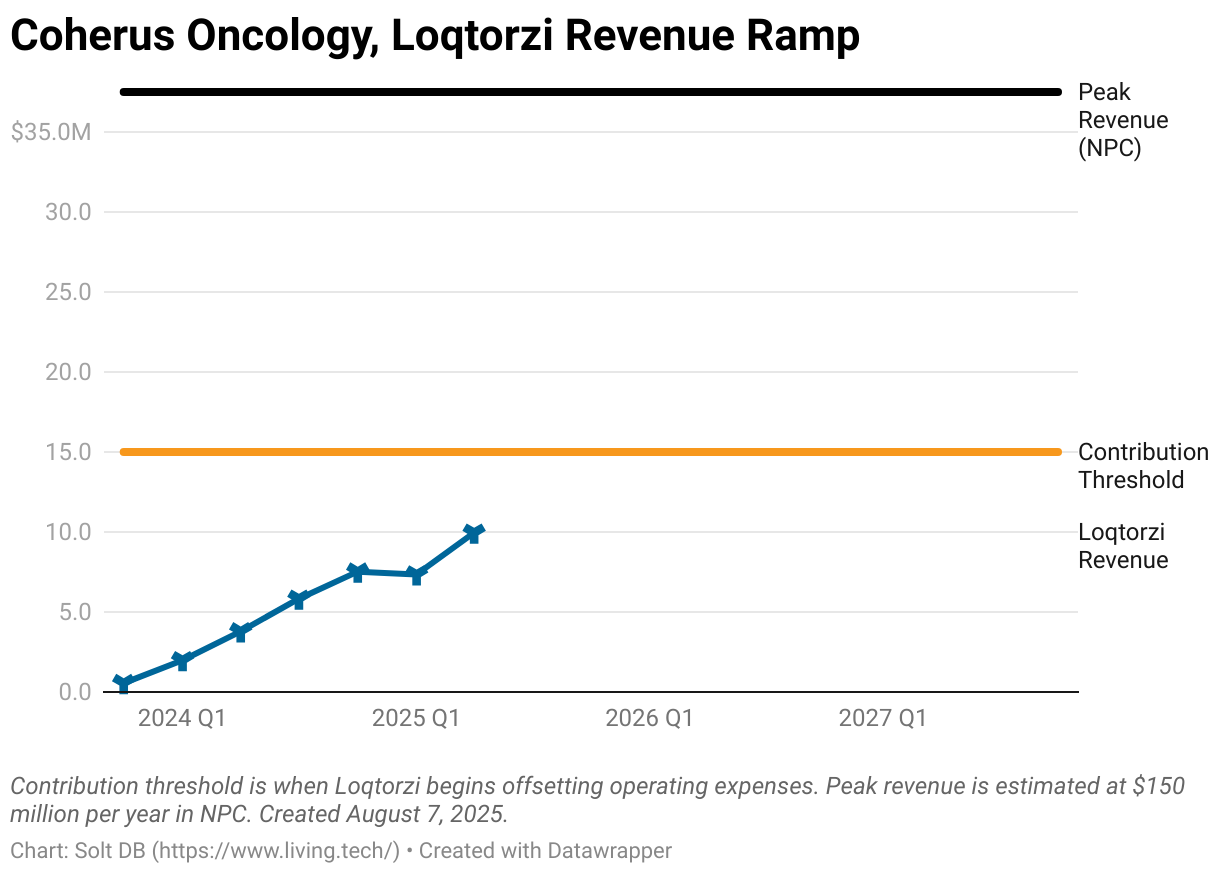

Coherus Oncology

- Earnings date not yet scheduled

Despite having oh-so-obvious short squeeze potential, shares of Coherus Oncology stubbornly refuse to blow off the emergency release valve. A licensing deal might do the trick.

Management has hinted at the potential to announce additional clinical trial collaborations and/or licensing deals for pipeline assets before the end of 2025. The former would seed future commercial potential without any upfront monetary value. For example, toripalimab is being supplied to STORM Therapeutics at cost, but that doesn't immediately benefit Coherus. The latter would be a more traditional partnership or licensing deal. For example, CHS-114 could be licensed internationally or for specific tumor types, while casdozo could be licensed in liver cancer internationally or globally.

It's important to be objective.

In drug development, the United States is the most lucrative market. Coherus wouldn't be expected to haul in giant upfront payments if it chooses to sell international rights to CHS-114. To be blunt, the early-stage maturity of the asset means it's not favorable to license any of its rights in the near term. This isn't Arrowhead or RNAi – it's very unlikely to expect upfront payments above $50 million.

A larger drug developer could be interested in taking a flyer on casdozo. Roche wields the standard of care treatment for liver cancer; a combination of Tecentriq (PD-1) and Avastin (VEGF) generates over $1.3 billion in annual revenue. Coherus is hopeful a new combination of Loqtorzi (PD-1), Avastin (VEGF), and casdozo (IL-27) may provide significant improvements. The one headwind in late 2025 is that casdozo doesn't have a robust data package.

Considering Coherus has enough cash to fund itself through multiple data readouts for CHS-114 and casdozo, rushing to sell rights to pipeline assets wouldn't be favorable for investors. It seems to me like management just wants to sell the whole company in 2H 2026.

This is really a pipeline story now, but I suppose we should all keep an eye on Loqtorzi's ramp. The sooner it gets to $15 million in quarterly revenue, the sooner it'll begin providing cash flow to offset operating expenses. Investors can expect that milestone by Q4 2025, but patient dynamics could lead to a surprising surge in Q3 2025 revenue.

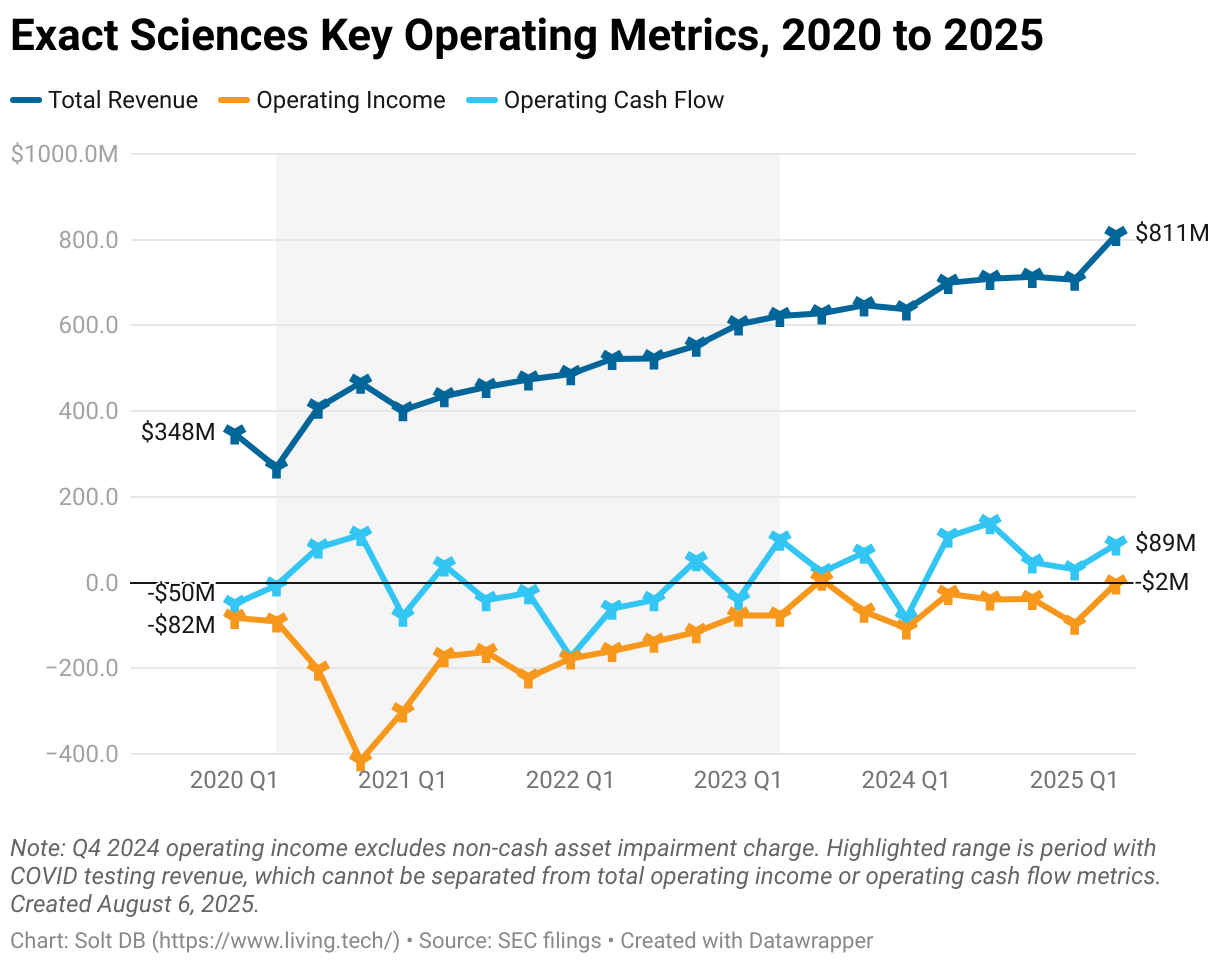

Exact Sciences

- Reports Monday, November 3 after market close

Investors are currently more interested in the home-grown technology platforms of Guardant Health and Natera. If we're being objective, then Exact Sciences is a step behind peers when it comes to technology development. At the same time, investors seem to be ignoring fundamentals and commercial dynamics.

For example, Guardant Health expects to grow revenue at least 30% to $1 billion in 2025. That's a meaningful growth rate. But, um, when Exact Sciences crossed the $1 billion mark in 2020, it was growing at a 43% clip – and I excluded $236 million in COVID testing revenue.

Natera expects to grow revenue roughly 24% to $2.1 billion in 2025. That's also a meaningful growth rate. But Exact Sciences reached that milestone in 2022 by growing 30%.

Guardant Health and Natera have more and better potential for future growth in emerging precision oncology markets than Exact Sciences, but multi-cancer early detection (MCED) and molecular residual disease (MRD) are smaller and vastly more crowded than the cash cow opportunity represented by Cologuard Plus. It really is that simple: In Cologuard we trust.

Exact Sciences is on pace to generate full-year 2025 revenue of at least $3.16 billion and operating cash flow of over $300 million, while notching net income in Q3 and/or Q4. It has a valuation of $11.9 billion. Guardant Health (one-third of the revenue, burning cash, nowhere near profitability) is valued at $12 billion, while Natera (two-thirds of the revenue, recently cash flow positive, and nowhere near profitability) is valued at $26 billion.

Krystal Biotech

- Reports Monday, November 3 before market open

Investors are pricing Krystal Biotech based on its epic earnings efficiency. That's not crazy. Vyjuvek has generated $359 million in revenue in the last 12 months, while the business has converted 41% of that into net income. That's crazy.

Of course, the company's research austerity is juicing the numbers. The gene therapy developer has spent just $55 million on R&D expenses in the last 12 months. Arrowhead Pharmaceuticals spends that every 31 days. Most companies lucky enough to breeze through clinical trials, earn an FDA approval, and ramp in an uncontested competitive landscape would happily redeploy cash flow and earnings into the next wave of growth products. Not so for the Pittsburgh drug developer.

If we squint our eyes and tilt our heads just so, then it's not difficult to see above-average acquisition potential, too. Krystal Biotech is unusual in that the husband-and-wife founders are the largest shareholders. Executives rarely own more than 1% of a drug developer. That means a lot is riding on data readouts for inhaled KB707, especially after the company nixed the intratumoral (injected directly into a tumor) formulation following some safety scares in the competitive landscape.

Investors also need to remain vigilant of Vyjuvek's ramp, which has notably slowed in the last three quarters. International expansions should drive another leg of growth, but shares would be severely punished if revenue growth in the United States stalls.

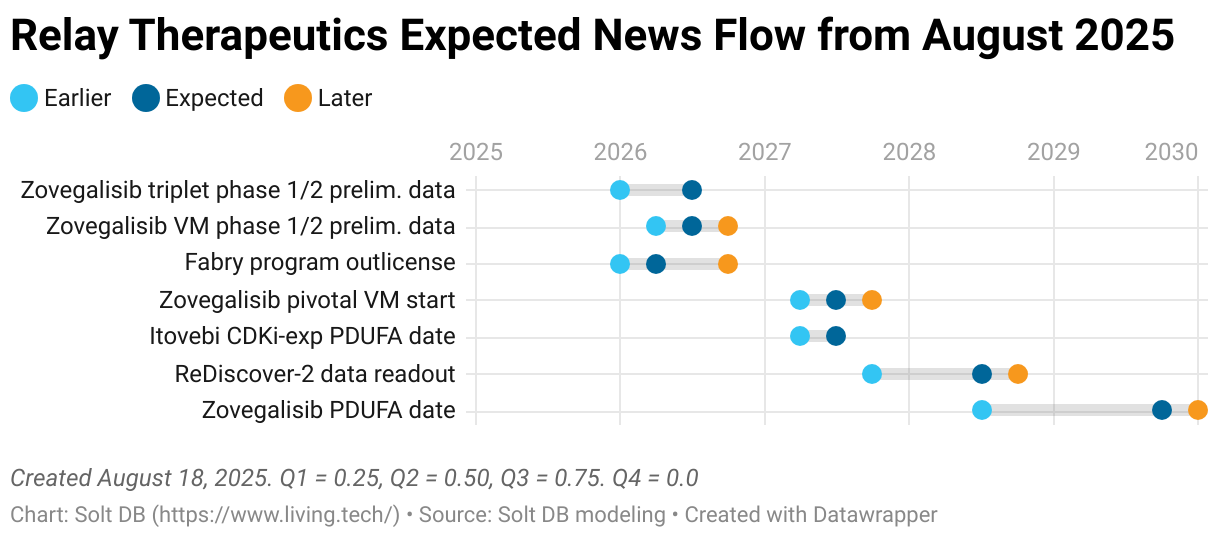

Relay Therapeutics

- Earnings date not yet scheduled (it usually doesn't schedule earnings because it never hosts conference calls)

Relay Therapeutics has been one of the better performers in recent months, but most signs point to it simply being driven by momentum and technicals. Case in depressing point: the business has added $700 million in market cap since early May, whereas Recursion Pharmaceuticals has added $900 million. Investors are still more eager to reward hype than properly value assets.

But that could change – maybe as soon as today.

The San Antonio Breast Cancer Symposium (SABCS) is the world's largest and most important conference for sharing developments in breast cancer treatments. This year it will run from December 9-12. Although the deadline for presentations passed this summer, the deadline for late-breaking presentations was September 30. Abstract titles will go live on Thursday, October 30. That's today.

Relay Therapeutics is more conservative with its approach to investor relations, to put it mildly. If it snuck into SABCS this year with a late-breaker for zovegalisib, then we'll get a press release this morning. That means investors might learn new data. What could that include?

Well, the protein motion pioneer could share updated data for fed-dosing of zovegalisib with fulvestrant to set the tone for the pivotal ReDiscover-2 study that's now underway. It could also be ready to share the first-ever data for zovegalisib triplets with Kisqali (CDK4/6) or atirmociclib (CDK4). If it snuck into SABCS, then a data readout might have a data cutoff of sometime in late July or early August. That's a reasonable checkpoint for preliminary data given when the company began evaluating triplets.

One problem is triplets will take a very long time to accrue data. Investors might expect the zovegalisib triplet with Kisqali to have a median progression-free survival (mPFS) of 18 months or more. Preliminary data would likely be shorter since dosing wouldn't be optimized. Triplets with atirmociclib could be over 24 months. Both would easily lead the competitive landscape, although Eli Lilly could eventually have an edge over the Kisqali combo since it gets to use the leading CDK4/6 inhibitor Verzenio, which it owns.

Management has made it clear it will wait until data are interpretable before sharing. It's much more difficult to optimize dosing of triplet combinations, and zovegalisib pivoted to fed-dosing this year, which could delay readouts. Nonetheless, investors might expect preliminary data near the end of 2025, which lines up perfectly with SABCS.

Aside from zovegalisib, investors will want to keep an eye on the cash balance and potentially any licensing agreements. Selling global rights to the Fabry disease asset could allow Relay Therapeutics to fully fund zovegalisib doublets, triplets, and vascular malformations studies – representing an annual revenue opportunity of up to $10 billion.

We Have Questions

The future can never be predicted with perfect accuracy, but sometimes the world moves faster (or companies move slower) than investors like. Some investments require a little more babysitting and objective criticisms, especially when management provides infrequent updates or uncertainty creeps in on previously communicated timelines.

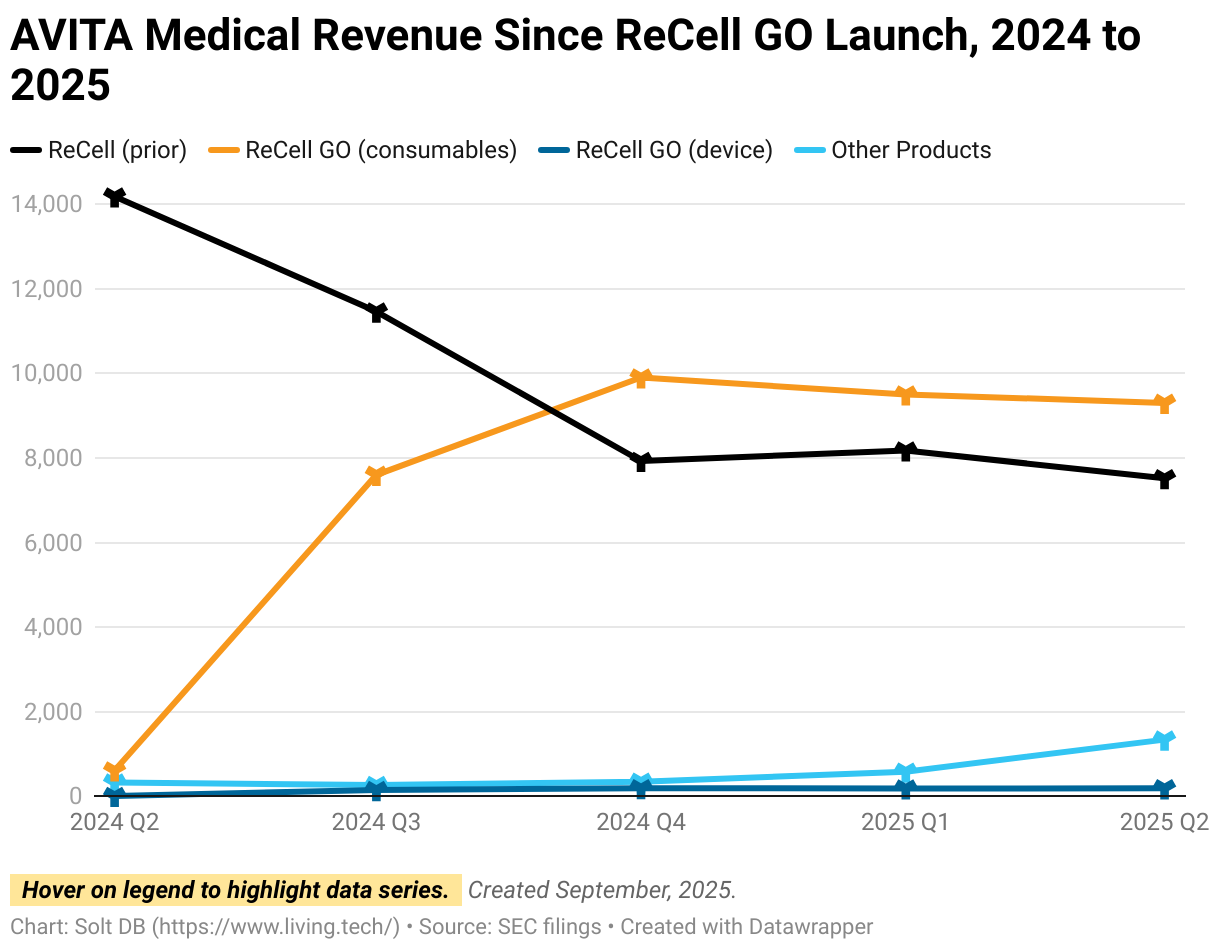

AVITA Medical

- Reports Thursday, November 6 after markets close

AVITA Medical is circling the drain and about to be pelted by analysts on its quarterly conference call.

It desperately needs capital and has no good way to snag it. The wound care specialist cannot easily issue shares without tragic dilution, while it's difficult to believe many creditors would be willing to extend a lifeline. Adding more debt isn't impossible, but the terms definitely wouldn't be favorable. OrbiMed might want to come to the rescue to protect its prior investment.

Success in investing doesn't come from buying good things. It comes from buying things well. A down-on-its-luck business could represent a great investment opportunity if you enter at the right price. Similarly, a great business at the wrong price could leave you underwater.

While I'm open-minded to opportunistic investments in biotech, especially in the aftermath of kneejerk reactions, AVITA Medical is facing more of an existential crisis. Those are much riskier to "buy well."

What will the new CEO have to say about current affairs? Can the business secure financing of any type and give itself one last desperate chance to turn things around?

Bicycle Therapeutics

- Earnings date not yet scheduled

Bicycle Therapeutics is developing a rival drug to Padcev. That's the blockbuster treatment for metastatic urothelial cancer that spurred Pfizer to overpay for SeaGen in a $43 billion acquisition. The antibody-drug conjugate generated $967 million in first-half 2025 revenue, and SeaGen also brought with it Adcetris, another potential blockbuster (that's stalling out).

Unfortunately for the coverage ecosystem newcomer, its crown jewel coughed up underwhelming preliminary results last year. Zelenectide pevedotin appears to be in the ballpark of Padcev on efficacy. However, whole point of the company's technology platform – based on Nobel-Prize winning chemistry called phage display, which enables novel drug discovery – is to spur more selective targeting of molecular targets. Investors thought the hype would translate to better safety and efficacy.

From a clinical data standpoint, it's difficult to tell if Bicycle Therapeutics will flop with longer-duration data or if investors are simply being impatient. Recent steps to terminate expansion trials in multiple tumor types, as well as a huge round of layoffs, don't instill much confidence. The drug developer promises to provide an update before the end of 2025. It will be a rare binary event for the coverage ecosystem – a go or no-go for a lead drug candidate. I try to avoid those.

Fear not, finch followers.

Bicycle Therapeutics ended June 2025 with $721 million in cash, which is enough to fund operations into 2028. Importantly, it has a promising radiopharmaceutical technology platform, albeit in the earliest stages of development. It also has an interesting twist on T-cell engagers that could be valuable components of immuno-oncology combinations.

If the company terminates the Padcev challenger and pivots to other pipeline assets, then shares would be absolutely crushed. But that could represent a good opportunity. The cash runway would be extended by default, data from the first immuno-oncology combination (with PD-1 drug Opdivo) are due before the end of 2025, and the first radiopharmaceutical drug candidate would enter the clinic in 2026. It's near the top of my watchlist.

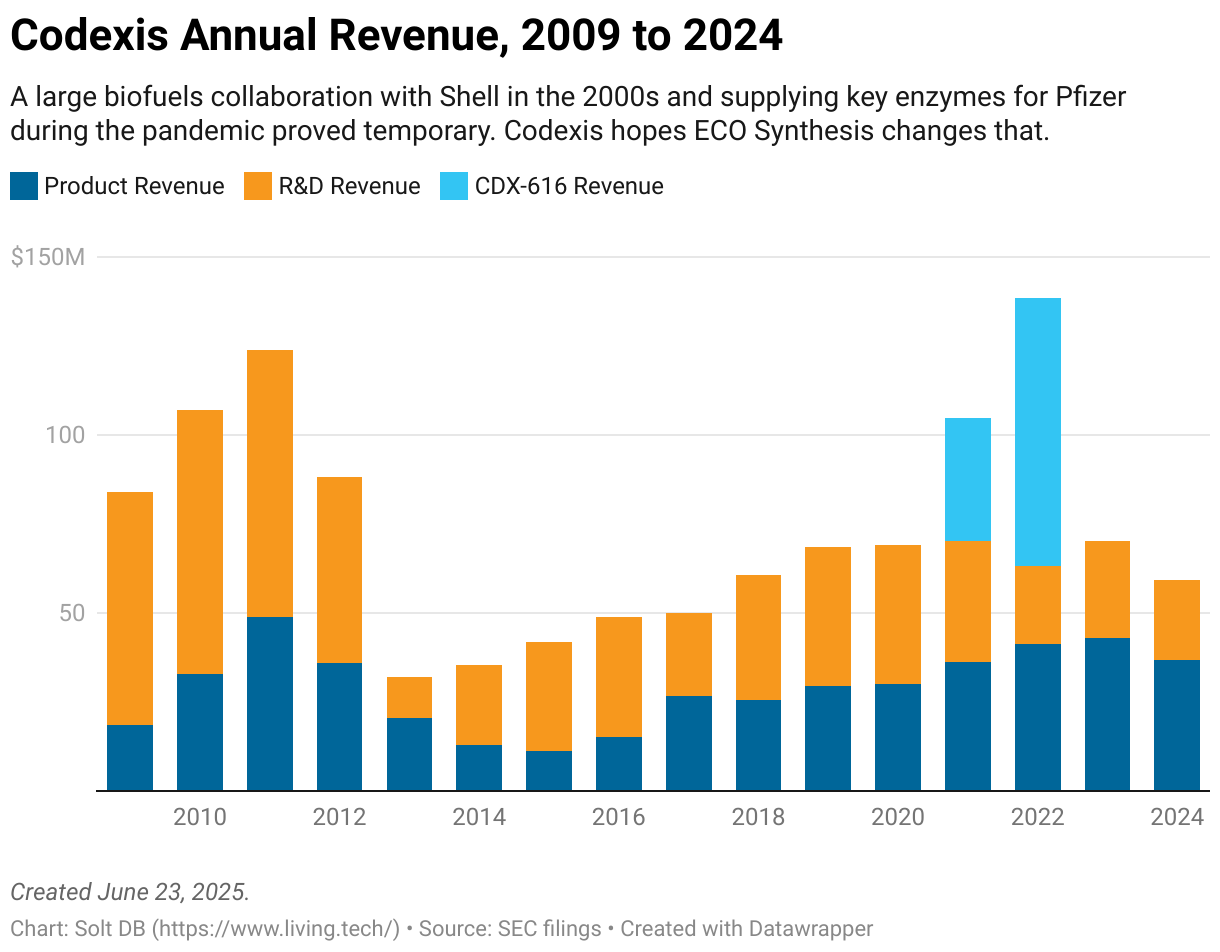

Codexis

- Reports Thursday, November 6 after markets close

Industrial enzymes have failed to capture the imagination of investors thanks to choppy, unpredictable revenue. That's why Codexis is pivoting to focus on enzymatic synthesis of the short-interfering RNA (siRNA) molecules that power RNAi drugs. Progress has been… slower than investors would like, but that's how it goes when commercializing novel living technologies.

Codexis recently announced an agreement to explore getting its ECO Synthesis platform into the hands of drug developers with the contract development and manufacturing organization (CDMO) Nitto Denko Avecia ("Nitto Avecia"). The partner will evaluate the novel technology platform and, if it likey, then it will consider deploying it for its own customers.

That's not exactly the homerun investors were clamoring for, but Nitto Avecia is a leading CDMO for RNA medicines. In the next few years, Codexis is likely to license its technology platform to other CDMOs and possibly tap their expertise to build a facility of its own. There's only so much it can do with limited capital.

However, the emergence of RNAi as an established therapeutic modality bodes well for Codexis if it can continue knocking out technical milestones. Alnylam Pharmaceuticals is now valued at over $60 billion and Arrowhead is racing ahead with multiple next-generation platforms. Meanwhile, if Wave Life Sciences proves that stereopure sequences enable less frequent dosing, then ECO Synthesis – which spits out stereopure sequences by default – will get more than a few phone calls.

Day One Bio

- Reports Tuesday, November 4 after markets close

Brain cancer treatment Ojemda doesn't have the largest market opportunity, which made its formidable launch out of the gate all the more curious. The commercial ramp immediately stalled during Q2 2025 as revenue roughly matched that from Q1 2025, restoring order in the world.

Although I don't want to sound like choosing to develop much-needed medicines for children with cancer is fruitless, Ojemda isn't a high-impact asset from a commercial perspective. So, predictably, the company's share price reflects that reality.

Luckily for Day One Bio, the value of Ojemda is more about mitigating operating losses than thrusting the business to profitability. It hasn't peaked yet and can expand its label with approvals for adult patients.

The drug developer's fortunes more heavily rest with the PTK7 inhibitor DAY301. Past attempts to target PTK7, overexpressed in many solid tumors but intriguingly absent on healthy tissues, have failed due to toxicity issues. These weren't tiny startups flailing around either; AbbVie and Genmab were among the companies whose ambitions bit the dust.

DAY301 uses a tweaked linker-payload chemistry that could overcome past safety issues. Adding to the thesis, unrelated ADCs using similar chemistry have largely succeeded in clinical trials, but few have an opportunity as large as PTK7. There's no timeline for sharing preliminary data from an ongoing phase 1 study, but based on regulatory timelines investors could see an update before the end of 2025.

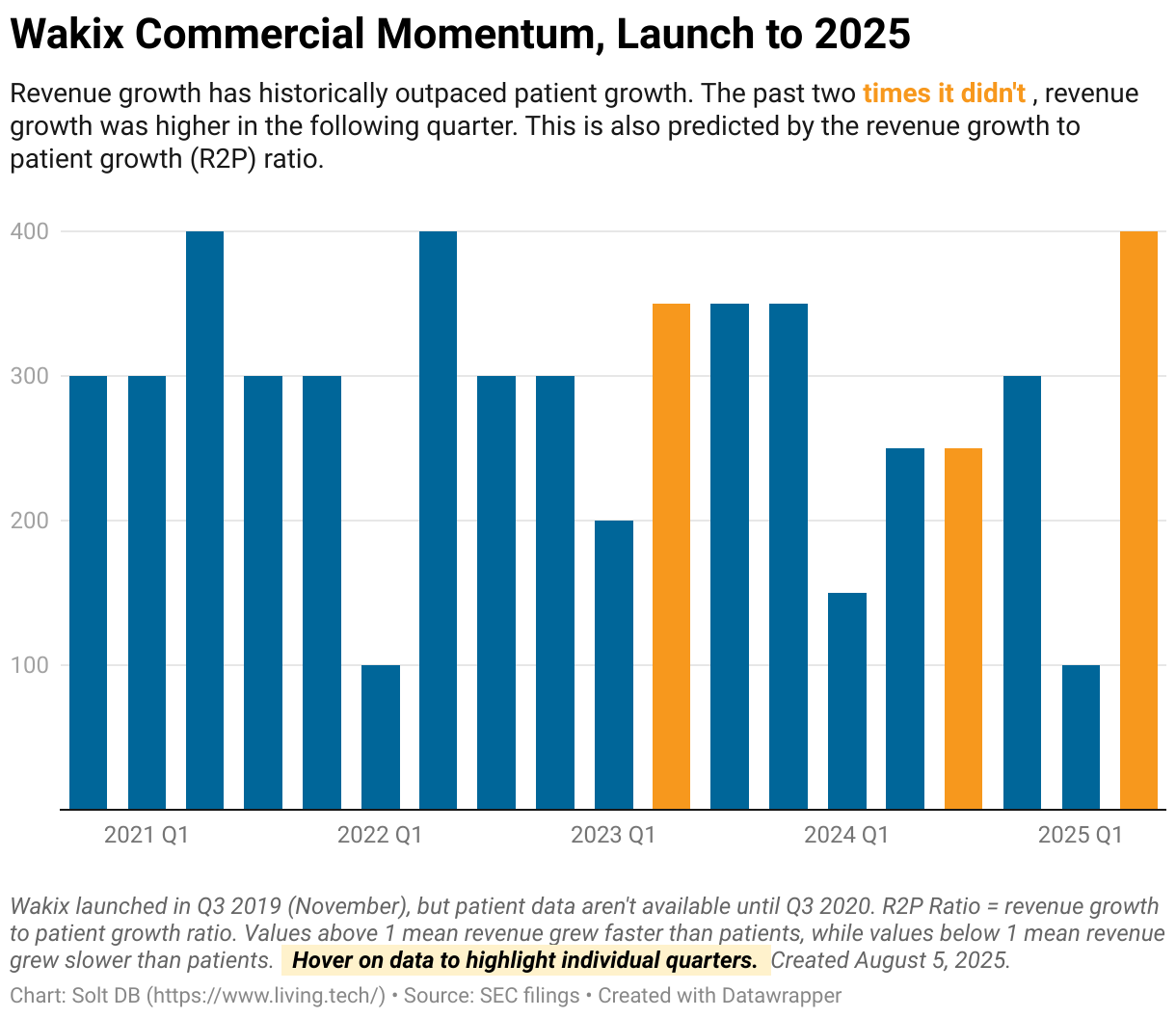

Harmony Biosciences

- Reports Tuesday, November 4 before markets open

Management provided preliminary Q3 2025 revenue when announcing the date of the earnings conference call. It wasn't a difficult decision.

Quarterly revenue for Wakix grew 29% from the prior-year period to roughly $239 million. That would represent the first growth rate of over 20% in the last year, which was powered by the first-ever quarter with 500 net patient starts (the company's rounding of patient starts has been controversial in the past). This is promising because the commercial metrics I track and use for modeling predicted a rebound in third-quarter revenue, as explained in last quarter's research note.

Harmony Biosciences also raised full-year 2025 revenue guidance to a midpoint of $855 million, up from a previous midpoint of $840 million. That's almost certainly conservative.

To reach the new midpoint, the business would need to generate revenue of $231 million in the final three months of the year, but Q4 revenue has never been lower than Q3 revenue. That would also be unusual given the seasonality trends in the industry, as wholesalers usually build up inventory in the final quarter of the year to beat price increases that go into effect every January 1.

I'll wait for official numbers to be reported before updating my model, but Harmony Biosciences is likely to generate full-year 2025 revenue of nearly $870 million – a $30 million increase from the current model. That could push annual net income to roughly $200 million, up from my current model of $178 million. This makes the current valuation more absurd than it already is, makes it easier for management to potentially sell the business, and also justifies a share repurchase.

Will management pull the trigger on a share buyback, or spend money on low-level acquisitions?

Recursion Pharma

- Earnings date not yet scheduled

TechBio companies don't host mere earnings calls. They host (L)earnings calls, bro.

As easy as it is to poke fun at the investor relations antics of Recursion Pharma, at least it tries. Investors just need it to try to develop drugs with a high probability of success. The model-informed drug developer has never successfully cleared a phase 2 clinical trial or delivered improved efficacy over competing treatments.

The clock is ticking.

The acquisition of Exscientia added a few promising drug candidates to the pipeline, but it also significantly increased expenses. Recursion shouldn't have an issue raising more capital in the near term, although investors and analysts might start cranking up the pressure to deliver wins.

Eli Lilly and Nvidia just announced a partnership to build the world's largest supercomputer owned by a drug developer – a claim currently held by Recursion (which also tapped Nvidia). At the other end of the spectrum, a wave of newer, leaner startups has built upon the vision of Recursion to score quick wins in drug discovery. Then again, discovery has never been the real limitation. Drug development – long, expensive clinical trials – has enforced the speed limits.

At this point, Recursion has probably hitched its wagon too closely to AI drug discovery to pull off a pivot to humility. What investors don't want to happen is for the business to become a casualty of the AI bubble. Surging investments and profits from Big Tech companies may have kicked that can down the road for at least another quarter, but time is never on the side of drug developers.

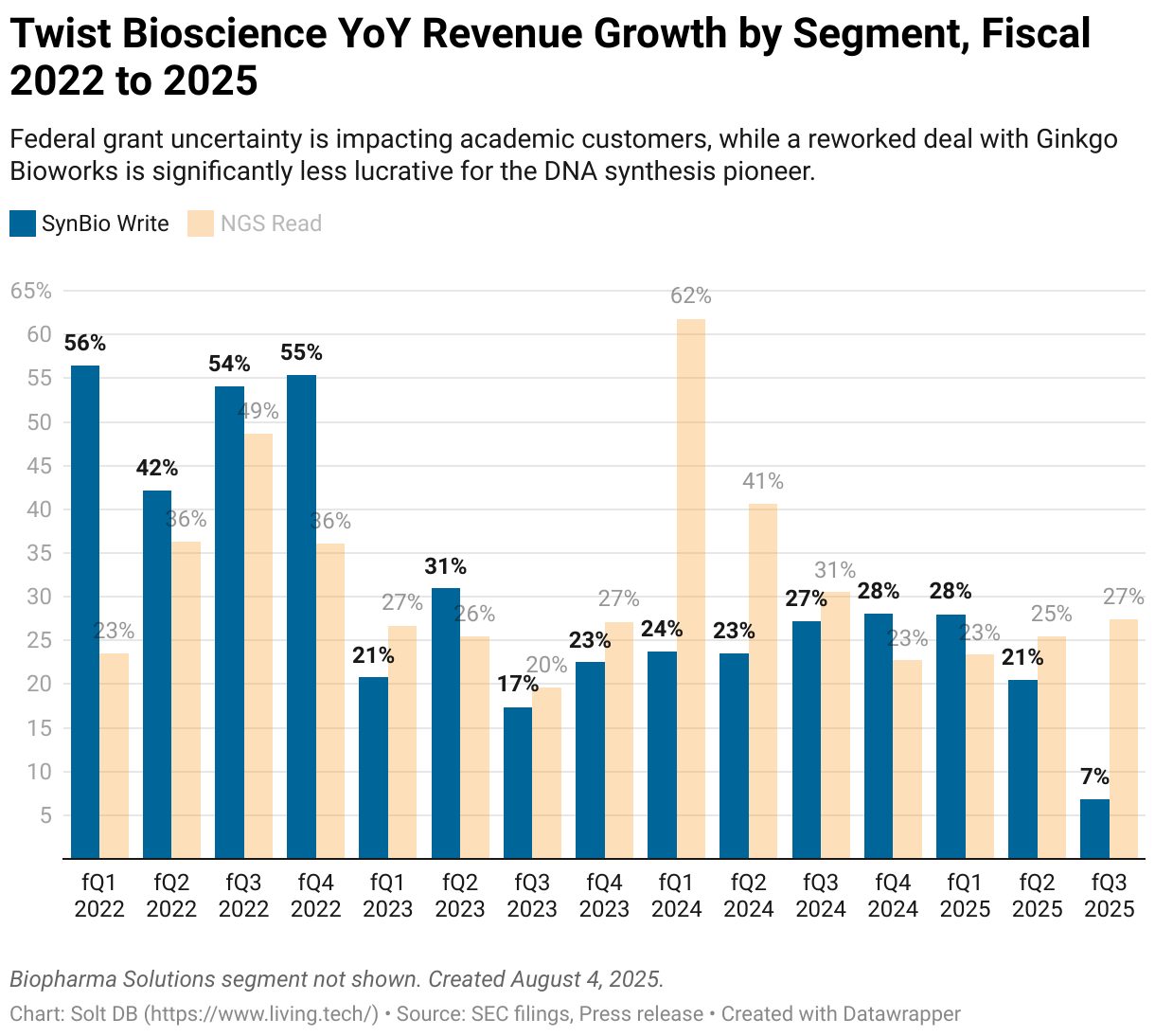

Twist Bioscience

- Fiscal full-year 2025 earnings scheduled for Friday, November 14 before the market opens

Investors are driving through the fog when evaluating Twist Bioscience right now. It's usually a good idea to slow down when that happens.

On the one hand, the DNA synthesis pioneer has a pretty solid business. Growth has been generally good, margins are improving, and there are no signs that NGS customers are slowing their appetite for quality oligos.

On the other hand, Twist Bioscience is facing a few headwinds. The gutting of American science funding has stalled orders from academic customers, which have generated declining revenue for two consecutive quarters. The duration of the biotech winter has roughed up key partner Ginkgo Bioworks, which resulted in a reworked supply deal that spreads out purchase commitments over a longer period of time.

And there's always the looming threat of competition. DNA synthesis is a race to the bottom for a commodity product. China's Genscript is no laughingstock, nor is Iowa's IDT. A slew of startups are making big claims about disruptive platforms, although I don't see much evidence of commercial traction (yet).

Will the business end its fiscal 2025 with a whimper? Perhaps more importantly, will full-year 2026 guidance disappoint Wall Street? I don't see CEO Emily Leproust trying to obscure weakness or uncertainty – she's usually a straightshooter.

Results Are In

A trio of companies reported before I had a chance to write this preview. Arcus Biosciences is quickly becoming a premium precommercial drug developer – and top acquisition target for large pharmas staring down the patent cliff. Meanwhile, Incyte raised guidance and still got whacked, while Kiniksa Pharma is running away with the opportunity in recurrent pericarditis.

.svg)

.svg)

.svg)

.png)

.svg)

.svg)

.svg)