.svg)

Finch Trades are posted to Discord as soon as they happen. Want an email alert every time a Finch Trade article like this goes live? Sign up in your profile.

One thing members value about Solt DB Invest is the transparency involved with my research and modeling. To build upon that, I'm introducing Finch Trades, where I'll update members on every trade I make in my personal portfolios. I'll also provide snapshots of my overall portfolio each month starting in May 2024.

For the first Finch Trade, I opened a new Roth IRA and funded it with the maximum-allowable annual contribution of $7,000. I intend for this portfolio to be my most-actively traded, especially since returns accrued in Roth IRA accounts aren't subjected to capital gains taxes.

I allocated the full amount to Coherus BioSciences on April 25, 2024. I've been waiting for a few years for the company's multi-product strategy to kick in – and it has finally arrived. That means this is a make-or-break year for the investing thesis.

The Trade

Coherus BioSciences is considered a Growth (Quality) position. I purchased 3,625 shares at $1.93 per share on April 25, 2024.

Scenario Analysis

My modeling is based on valuing assets, contextualizing competitive landscape dynamics, and weighing the probabilities of favorable and unfavorable scenarios. This trade was driven by the following considerations.

A Low-Risk Valuation (Positive)

Although shares have crumbled since *gestures broadly at historical stock chart*, investors haven't yet been able to test the thesis: a multi-product portfolio combined with the company's proven track record in commercial execution can return the business to permanent profitability and operational flexibility.

The wait has been brutal, but the thesis remains intact.

Since quality revenue, income, and cash flows can be assigned valuation premiums relatively easily on Wall Street, a little execution can significantly revalue the stock in a short time. And since the valuation of the company doesn't properly value even a mediocre level of execution, I think this entry point makes a relatively low-risk investment.

An Awesome Commercial Track Record (Positive)

Coherus BioSciences has an excellent track record of commercial execution. If you give the team something to sell, then they don't disappoint.

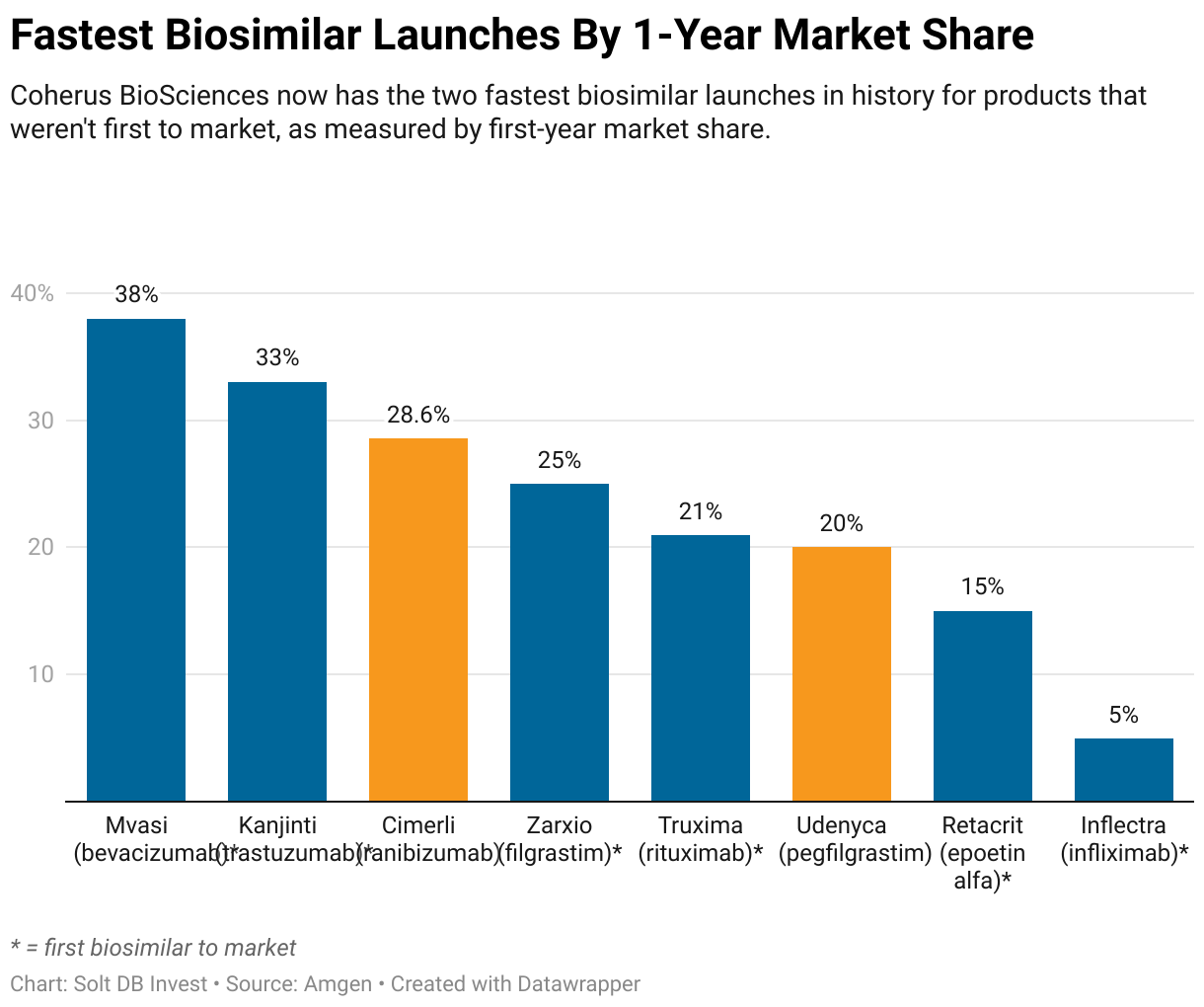

- As of the end of 2023, the company had launched two drug products: Udenyca and Cimerli. Both were the second biosimilars to launch in their respective markets.

- Udenyca (20%) and Cimerli (28.6%) were the sixth and third best biosimilar launches ever, respectively, when ranked by market share 12 months after launch. Every other biosimilar in the top 10 of this metric was the first to market.

- Udenyca was the best drug launch of 2019 and the best-ever biosimilar launch by first-year revenue.

This is even more impressive when investors consider the size of Coherus BioSciences in comparison to the competitive landscape.

Profitability and Cash Flow Positive Operations (Positive)

Modeling Coherus BioSciences is a little hazy right now, specifically meaning prior to the first-quarter 2024 operating results update.

I can argue the business will squeak out a profitable third quarter when the Udenyca franchise's royalty payments expire (the company pays Amgen a 5% royalty on all Udenyca revenue through June 30), or perhaps as late as the first quarter of 2025.

In either scenario, the trajectory will be clear before this milestone arrives and management should be able to set expectations accordingly before then. The next time Coherus BioSciences delivers a profitable quarter it won't return to losses, barring one-time write offs that might be necessary to refocus the portfolio or pipeline in 2025 or later. That doesn't matter right now or in the context of this trade.

How This Could Backfire (Negative)

There's a timing component to investing, but there's a timing component to running a business, too. It's called the cash runway – and Coherus is cutting it close.

It will need to raise more capital in 2024. A stock offering would be very unfavorable at current prices, debt isn't attractive, and Yusimry could be monetized but it has a relatively low value. I can see the business raising $10 to $25 million in cash by outlicensing the international rights to Casdozo, or crafting a creative royalty agreement for Yusimry that has a healthy upfront cash component.

The best option is execution. That would revalue the business higher, which would provide more options for fundraising.

As is always the case in drug development, portfolios and pipelines exist in a constant state of flux.

Portfolio

- The odds of Yusimry being an uncompetitive asset are rising. On the day I made this trade, insurance provider Cigna announced it will be offering interchangeable biosimilars Cyltezo (Boehringer Ingelheim) and Simlandi (Teva, Alvotech) instead of Humira. Coherus BioSciences has argued interchangeability status isn't as important as supply volumes and citrate-free formulations in this specific market, but that internal market research might already be outdated.

- I'm still not 100% confident Udenyca Onbody will escape a legal challenge from Amgen, although the window for that is closing. The launch of Udenyca Onbody is the single-most important driver for 2024.

- Meanwhile, Loqtorzi is well-positioned as the preferred treatment option in national guidelines, but it might be getting off to a uncharacteristically and un-Coherus slow start. Wall Street wouldn't handle that well.

Pipeline

- Certain oncology targets in the pipeline, such as IL-27 (phase 2 data are available) and ILT4 (preclinical data are available), have been duds in the competitive landscape.

- Casdozo (IL-27) delivered very competitive data in its small phase 2 study, which I found surprising since inhibiting IL-27 should make tumors grow faster.

- CHS-114 (CCR8) will have a preliminary phase 1 data readout at ASCO on June 1. This is becoming an increasing attractive oncology target, but there's relatively little data. Prior results from CHS-114 were inconclusive.

- CHS-1000 (ILT4) only has preclinical data, but all other industry attempts have failed.

Keep in mind the pipeline isn't really factored into the valuation yet. Investors are more concerned in balancing upside (favorable clinical readouts) and cash burn (the need to fund clinical trials). That's what makes commercial execution so important -- everything else falls into place with it.

Holding Period

I'm targeting an exit for this Roth IRA position in the range of $10 to $15 per share, which equates to a holding period of 6 to 18 months.

I've stuck with Coherus BioSciences, which comprises 25% of my personal brokerage at $4.95 per share (the entire position reaches a tax-advantaged holding period at the end of 2024), because it still has the potential for a market-beating return at my cost basis and for my entire holding period. But there is a time component to investing.

I might decide to exit all positions in all portfolios in the $10 to $15 per share range. I'd be thrilled to redeploy the capital to other positions in late 2024 or early 2025, especially with the timing of de-risking events for Arrowhead Pharmaceuticals, Arvinas, Codexis, and Relay Therapeutics.

Just to be clear Finch Trades will cover my buys, sells, and options trades. I'll always provide updates.

The important thing to remember is this is a make-or-break year for the investment thesis. Investors will have a definitive answer on the direction of the business in 2024. In other words, if it's December 31 and the business hasn't put the pieces together, then Coherus BioSciences probably isn't in your portfolio. The thesis would've broken, and I would've been proved wrong.

Margin of Safety & Allocation

Coherus BioSciences is considered a Growth (Quality) position. The current modeled fair valuation for the company based on our 2024 model is below:

- Market close April 25: $1.93 per share

- Modeled Fair Valuation: $10.58 per share

- Allocation Range: Up to 15%

Coherus BioSciences reported 112.714 million shares outstanding as of February 29, 2024. The modeled fair valuation above assumes 118.350 million shares outstanding, which is equivalent to 5% dilution.

.svg)

.svg)

.avif)

.png)

.svg)

.svg)

.svg)