.svg)

It's that time of the every-three-months again: earnings season.

Some shuffling of the coverage ecosystem has increased the average market cap and maturity of companies covered. The addition of Blueprint Medicines, Guardant Health, Harmony Biosciences, and SpringWorks Therapeutics introduces a crop of commercial-stage businesses. The deletion of 10x Genomics, IGM Biosciences, LanzaTech, PacBio, and Schrodinger removes more volatile and less sustainable businesses.

Meanwhile, several precommercial companies are maturing with time. Arcus Biosciences has a slew of late-stage clinical trials ongoing, Arrowhead Pharma could earn its first regulatory approval by the end of 2025, Coherus BioSciences has finally begun combination studies for assets acquired from Surface Oncology 24 months ago, Krystal Biotech is barreling ahead with a strong launch for Vyjuvek, Recursion Pharma swallowed Exscientia, and Relay Therapeutics expects to enroll its first pivotal study soon.

I'll be introducing coverage of the new crop (and the old crop without coverage) after first-quarter 2025 earnings so models are the most up to date. In the meantime, let's start a new tradition with a quick distillation of what to watch.

Potential High-Impact Updates

A high-impact update for a pipeline or portfolio has the potential to de-risk a business by removing uncertainty or forcing analysts to adjust expectations. These could be accompanied by larger stock moves or revised fair valuation estimates – in either direction.

Blueprint Medicines (new)

- Modeled fair value: N/A

- Last close (April 25, 2025): $87.66 per share / $5.60 billion

- What to Watch: Commercial ramp of Ayvakit

Blueprint Medicines is the most mature drug developer in the coverage ecosystem. It found a valuable niche treating mast cell diseases, which occur when the cells that comprise connective tissues degrade. Although most individuals have a normal life expectancy, there's no cure and the symptoms can have a severe negative quality of life impact. That means an effective treatment with a solid tolerability profile can generate many years of revenue from each patient.

The company expects its lead drug product, Ayvakit, will generate $695 million in full-year 2025 revenue – up 45% from last year. It sees the overall franchise, including a next-generation molecule called elenestinib, generating peak annual revenue of at least $4 billion. It expects Ayvakit alone to reach $2 billion in annual revenue by 2030. That represents the largest commercial opportunity of any drug asset in the coverage ecosystem outside of RLY-2608.

The business has struggled to grow into a premium valuation for most of the last seven years as investors priced in years of commercial success before Ayvakit was even approved, but that could be about to change. Blueprint Medicine is in the sweet spot of its growth trajectory – when drug developers tend to provide the best returns and opportunities for compounding long-held positions – and should turn cash flow positive in 2025 and profitable in 2026.

It might be difficult to surprise to the upside when guidance calls for 45% year-over-year growth, but that might be an underestimate. Investors can also lean on valuation contributions from the pipeline. Specifically, there are three next-generation breast cancer assets taking aim at CDK2 and CDK4 inhibition and degradation. They're prime candidates for large licensing deals as the global industry races to develop more effective breast cancer treatments.

Certara

- Modeled fair value: $11.62 per share / $2.053 billion

- Last close (April 25, 2025): $14.17 per share / $2.328 billion

- What to Watch: Strategic review of regulatory services unit

Certara has maintained a conservative outlook for 2025, but tailwinds are starting to build.

The U.S. Food and Drug Administration (FDA) announced long-awaited plans to begin phasing out animal studies where possible, beginning in monoclonal antibodies. The FDA Modernization Act 2.0 required the regulator to develop such a strategy when it became law in late 2022. That's all good news for Certara, which provides biosimulation and predictive analytics that have already been used to avoid or supplement animal studies.

Management pounced on the announcement by launching a new software tool, appropriately named Non-Animal Navigator. It also surprised markets by announcing the authorization of a $100 million share repurchase program; a sign the business is healthy and the board believes the stock is undervalued. Despite being unveiled simultaneously, these two events aren't linked.

Instead, Certara will only be able to complete a share repurchase program if it divests its Regulatory Services business unit, which has single-handedly dragged down revenue for the Services segment. The Regulatory Services business unit generated revenue of $60.5 million in 2023 and $54.7 million in 2024 – a decline of 10%. The price of an acquisition would be determined by earnings, which the company hasn't broken out, but investors can expect a fair value in the ballpark of $50 million.

Why is an asset sale virtually required to buyback shares? The business is cash flow positive, but it exited 2024 with only $179 million in cash. It'll need to keep some dry powder to add to its two-dozen historical acquisitions, especially if an economic downturn creates a target-rich environment.

Coherus BioSciences

- Modeled fair value: $2.78 per share / $119 million

- Last close (April 25, 2025): $1.03 per share / $339 million

- What to Watch: Clinical trials remaining on track, potential competition for Loqtorzi in NPC

Coherus BioSciences announced the all-stock acquisition of Surface Oncology in June 2023. The $65 million transaction added two clinical-stage assets with solid potential in Loqtorzi combinations. However, the company had to see existing clinical trials to completion before getting the opportunity to march forward with internally-designed studies. The time has finally come.

A phase 2 study evaluating a triplet of Loqtorzi, Avastin, and casdozo in first-line hepatocellular carcinoma (1L HCC) is now enrolling patients. Coherus more than doubled the number of participating medical centers in April alone.

A phase 2 study evaluating a doublet of Loqtorzi and CHS-114 in various solid tumors (primarily gastric cancer and head and neck squamous cell carcinoma) began recruiting patients in April. Investors can expect data readouts from the anti-CCR8 competitive landscape during ASCO from May 30 to June 3, which could increase interest in Coherus.

Additionally, investors should keep an eye on a new source of competition for Loqtorzi. Chinese drug developer Akeso Bio earned FDA approval for one of its PD-1 assets, penpulimab, in nasopharyngeal carcinoma (NPC) last week. To reiterate, competition is omnipresent in drug development. That's the point of drug development – to improve quality of life for patients while getting your slice of the pie.

On the one hand, the reason Loqtorzi was the first treatment approved by the FDA for NPC is because it's a rare cancer in the United States. There are over a dozen approved PD-1 / L1 inhibitors, but the commercial opportunity is relatively meaningless to Merck (Keytruda), Bristol Myers Squibb (Opdivo), Roche (Tecentriq), and others.

The reason Loqtorzi and penpulimab originated in China are because NPC primarily affects individuals of Asian descent. That's also why the FDA has adopted "regulatory flexibility" for this specific indication – there's not much to gain from forcing companies to conduct a new study with U.S. patients.

On the other hand, the NPC pie isn't that large. The relatively limited commercial opportunity means competition could ding the peak annual sales potential of Loqtorzi. The company projects up to $200 million, whereas I model closer to $150 million. Neither is large enough to fund operations.

I see no evidence Akeso has a commercial footprint in the United States, which means penpulimab might not launch despite being approved. It's difficult to license rights to assets with limited market opportunities, especially since the innovator will demand royalties, further limiting the financial benefit. Investors might hear management's thoughts on this development on the earnings call, but a broad development strategy for Loqtorzi insulates the business from potential competition in NPC.

Exact Sciences

- Modeled fair value: $87.88 per share / $16.488 billion

- Last close (April 25, 2025): $45.46 per share / $8.47 billion

- What to Watch: Progress toward achieving profitable operations in 2025

The stars are aligned for Exact Sciences to thaw from the biotech winter this year.

The business has the same valuation today as it did two years ago – despite expecting to grow revenue 50% from 2022 to 2025. More importantly, it should generate at least $450 million in cash from operations this year and is likely to turn profitable. Those are exactly the characteristics investors value during economic downturns.

Wall Street expects Q1 2025 revenue to be 3.5% lower than the final frame of 2024. While lower revenue to start a calendar year isn't unusual in the healthcare sector as customers manage inventory and spend down budgets at year-end, that would mark a historically steep drop.

Exact Sciences will also need to provide an update on tariff-related costs. The business manufactures and processes all tests in the United States (or Europe for tests administered on the continent), but some consumables originate from China. Still, I wouldn't be surprised to see shares jump by double-digits – maybe in the ballpark of 20% -- as analysts are reminded of what really matters in business.

Guardant Health (new)

- Modeled fair value: N/A

- Last close (April 25, 2025): $48.30 per share / $5.96 billion

- What to Watch: Increased guidance, potential for valuation risk to whack shares

Speaking of what really matters in business, shares of Guardant Health have gained 181% in the last year and 58% year to date. Investors might want to pinch themselves though, as operating results now or in the near future don't support the current valuation.

The business is expected to report worse margins in 2025 compared to last year. It has 70% of the market cap of Exact Sciences despite having only 28% of the revenue. It's not growing much faster. Guardant Health burned $228 million in cash from operations last year, whereas Exact Sciences generated $210 million (and $293 million in the final nine months).

Guardant Health has a solid technology platform with different offerings than its larger peer, it has a comfortable cash position, and has earned surprisingly favorable Medicare reimbursement rates for the blood-based colon cancer screening tool Shield. But the valuation isn't attractive right now.

Despite the excitement for Shield, investors should remember management expects the new test to generate less than $30 million in full-year 2025 revenue – just 3% of total expected sales this year. Cologuard will eclipse $2,400 million in revenue. I do think initial guidance for Shield was very conservative, so investors can expect increased outlooks throughout the year. But this is not (yet) a $6 billion business.

Harmony Biosciences (new)

- Modeled fair value: $62.84 per share / $3.498 billion

- Last close (April 25, 2025): $29.61 per share / $1.70 billion

- What to Watch: Commercial progress for Wakix, timelines for a maturing pipeline

No technology pipeline, so-so internal R&D capabilities, and looming competitive threats should weigh on the valuation of Harmony Biosciences. But even a sorry S.O.B. can admit there are limits to pessimism.

The ongoing commercial ramp of Wakix drove the business to full-year 2024 revenue and net income of $714 million and $145 million, respectively. A market valuation of only $1.7 billion means the business trades at a price-to-earnings (PE) ratio of 11.7x last year's earnings. Couple expectations for double-digit revenue growth this year with a respectable share repurchase program, and shares should push their way to a more reasonable valuation in time.

At the very least, it's difficult to see Harmony Biosciences falling precipitously in an economic downturn or market correction.

A number of catalysts could force the coiled spring to pop in 2025. Next-generation formulations of Wakix promise to extend patent protections to 2044, address tolerability issues of the current formulation, and help mitigate competitive risks posed by orexin-2 receptor (OX2R) agonists. The company has an OX2R asset of its own – licensed from the Japanese scientist who discovered the role of OX2R and OX1R in narcolepsy – but it doesn't appear competitive against more mature assets from Centessa Pharmaceuticals and Takeda.

Shares are lower to start the year after the FDA rejected its request to approve Wakix in pediatric cataplexy, but management said it won't impact revenue guidance. The company will try again after conducting a new pivotal study with next-gen formulations of Wakix. More importantly, that was a silly reason to sour on an otherwise commercially dominant business. And there's no tariff risk, as inventory can meet demand into Q1 2027 and the company has enough raw materials to manufacture another 24 months of supply.

I think shares are likely to jump by double digits after strong operating results remind analysts cash flow and profits are pretty valuable in the current environment.

SpringWorks Therapeutics

- Modeled fair value: $67.79 per share / $5.093 billion

- Last close (April 25, 2025): $44.72 per share / $3.37 billion

- What to Watch: Commercial ramp of Osgiveo and Gomekli

It appears SpringWorks Therapeutics could get acquired by Merck KGaA (the German company, not to be confused with the U.S. company Merck like me on Discord). The Wall Street Journal reported a deal could come as early as, well, by the time you read this.

An acquisition certainly qualifies as a high-impact update, but the commercial trajectory of Ogsiveo and the newly-launched Gomekli are where I want to fix your gaze. These will become crucial if an acquisition falls through. If the ramps are healthy and Merck KGaA walks away, then investors could be given a no-brainer entry point.

SpringWorks Therapeutics expects to turn profitable in the first half of 2026. To achieve that, Ogsiveo needs to remain on its solid trajectory and Gomekli needs to take advantage of a broad label. My model expects full-year 2025 revenue of $376.75 million, which is 7.5% above the Wall Street consensus. A strong start to the year could force analysts to recalibrate.

One thing to keep in mind: a meaningful supply of Ogsiveo and Gomekli is manufactured in China. That will ding gross margin and could delay the arrival of profitable operations, but I expect the impact to be relatively small.

We Have Questions

The future can never be predicted with perfect accuracy, but sometimes the world moves faster (or companies move slower) than investors like. Some investments require a little more babysitting and objective criticisms, especially when management provides infrequent updates or uncertainty creeps in on previously communicated timelines.

Arrowhead Pharma

- Modeled fair value: $27.77 per share / $3.871 billion

- Last close (April 25, 2025): $13.25 per share / $1.83 billion

- What to Watch: Is plozasiran's November PDUFA date jeopardized by staffing cuts at the FDA?, potential phase 1 data readout for ARO-RAGE with earnings (or an expected date)

Arrowhead Pharma had struggled to earn a fair valuation in recent years due to fast-growing R&D spend and cash burn. However, investors now know a meaningful chunk was driven by the seven assets since licensed to Sarepta Therapeutics. The RNAi specialist will earn $1.125 billion in cash by March 2026 and see at least slowing R&D expense growth, yet the valuation still hasn't recalibrated.

The business has a cash runway into 2028 that could likely be extended an additional 12 months relatively easily, if absolutely needed. We'll see if management comments on its cushy balance sheet in the current environment. It might have to.

Reports of drug developers encountering disruptions to regulatory timelines are beginning to suggest the poorly thought-out staffing cuts at the FDA aren't just impacting a company or two. That could spell trouble for plozasiran's PDUFA date scheduled for November. Although the asset's initial approval won't be a major source of revenue, beginning to build commercial infrastructure today will help support expanded approvals in much larger markets tomorrow. Delaying that would be a little more painful than kicking back launch.

Luckily, Arrowhead Pharma isn't a one-trick pony. The next reminder will be ARO-RAGE. A data readout for the first part of a phase 1/2 study in asthma is expected any day. It's another massive market. And better yet, one where existing treatments have already de-risked the commercial opportunity for biologics. By acting on a new genetic target and providing more favorable dosing, ARO-RAGE has the potential to be a big commercial success – if the next data readout is favorable.

Arvinas

- Modeled fair value: N/A

- Last close (April 25, 2025): $9.05 per share / $628 million

- What to Watch: Pfizer potentially terminating vepdeg, timelines for the wholly-owned pipeline

Vepdeg whiffed on its first pivotal trial. Long live vepdeg.

The valuation has fallen back to earth, although it's still overvalued without the commercial contributions of the lead asset. Despite the high-profile failure, investors should remember that Arvinas management struck when the iron was hot and licensed partial rights to vepdeg for $1 billion during the pandemic bubble. That was one of the more lopsided monetization transactions a small drug developer pulled on large pharma in recent memory, especially considering it retained 50/50 rights.

Arvinas entered the year armed with $1.04 billion in cash, which provides a sufficient runway to generate initial results from wholly-owned assets. The oncology and neuroscience pipelines are loaded with high-value targets that are uniquely suited for protein degradation, ranging from MYC and HPK1 in cancer to LRRK2 and mutant huntingtin in neuro.

The primary issue is that only two of eight pipeline assets are in clinical trials. It will be expensive, in both time and money, to generate meaningful results. This isn't the best market environment to tell investors they'll need to wait a few years. Nonetheless, management will provide a major post-vepdeg update this quarter. Don't be surprised if Pfizer chooses to walk away from the collaboration altogether.

AVITA Medical

- Modeled fair value: $18.73 per share / $568 million

- Last close (April 25, 2025): $10.07 per share / $266 million

- What to Watch: Can these knuckleheads deliver in 2025?, a dwindling cash balance

Management wisely decided against providing quarterly revenue guidance in 2025. That reduces the pressure each quarter to hit a specific number and allows the team to focus on hitting the full-year target. But that's still a big number – $103 million in sales represents year-over-year growth of 61%.

AVITA Medical is still growing at a healthy clip, but really the only thing that can stop the business is itself. Investors will want to watch for progress on sluggish sales in international markets and, more importantly, from the product portfolio surrounding ReCell.

Hitting the ambitious growth target is doubly important not just to rebuild trust with investors, but to eek out cash flow positive operations before the cash runway expires. Considering the business entered the year with only $35.9 million in cash, that could be very soon. Hopefully management has backup plans for debt on favorable terms or, better yet, takes advantage of any near-term rise in shares with a public stock offering – just in case.

Codexis

- Modeled fair value: $5.25 per share / $463 million

- Last close (April 25, 2025): $2.26 per share / $190 million

- What to Watch: Commercial timelines for ECO Synthesis

The enzyme engineering pioneer had a good showing months ago at TIDES. Codexis unveiled data from a collaboration with Bachem, one of the world's largest contract development and manufacturing organizations (CDMOs) for RNAi, demonstrating promising proof of concept for manufacturing Leqvio. The asset will become the first blockbuster RNAi product.

That was quickly followed by the ECO Synthesis platform's first revenue-generating contract in March 2025. Unfortunately, Codexis couldn't name the customer, likely because there's a large size difference or for competitive reasons. Alnylam Pharma discussed progress with an enzymatic synthesis pilot around the same time, but didn't name Codexis either.

Will management share any additional details about expectations for revenue or ramps into 2026 or beyond?

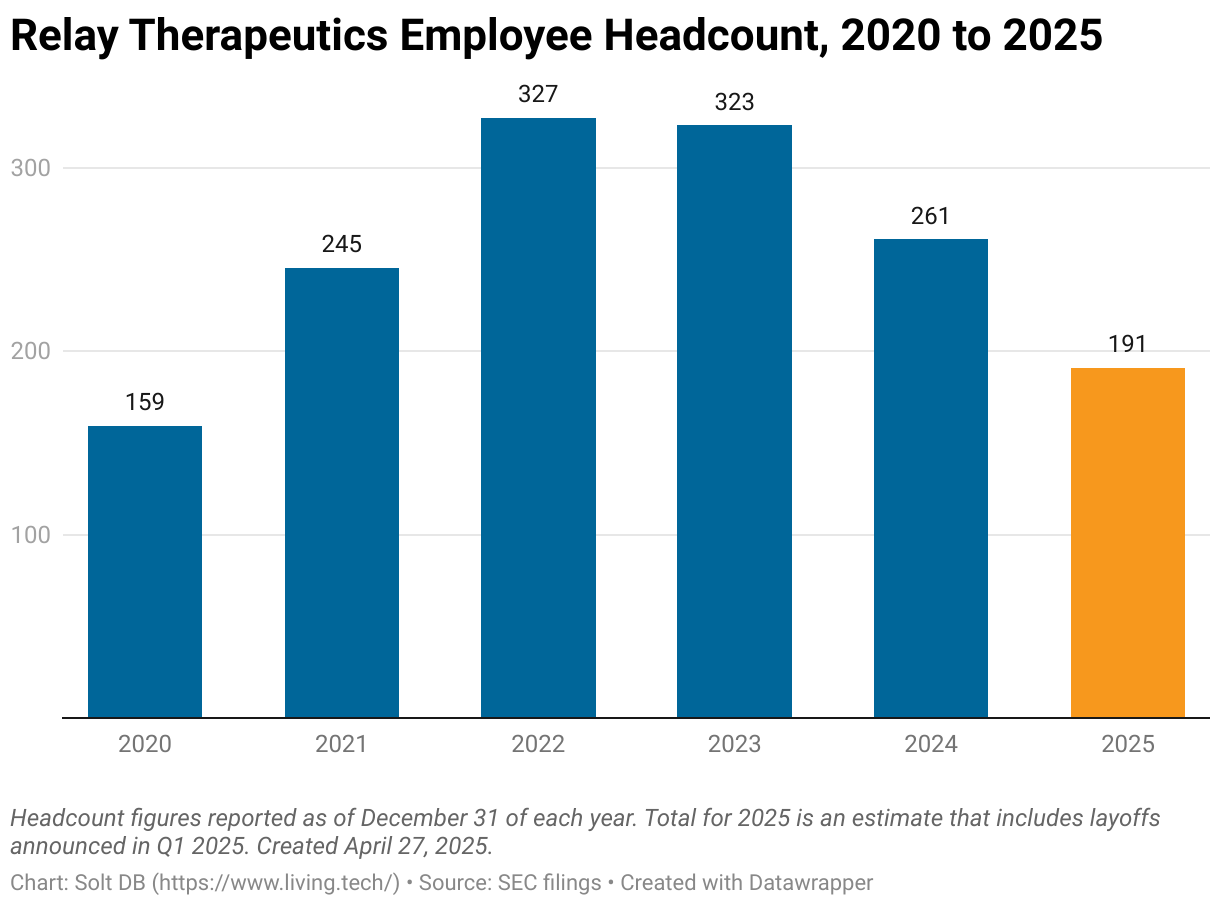

Relay Therapeutics

- Modeled fair value: $16.75 per share / $2.981 billion

- Last close (April 25, 2025): $3.20 per share / $545 million

- What to Watch: Pivotal start for RLY-2608 doublet in breast cancer, preliminary data for RLY-2608 triplets, enrollment of RLY-2608 in vascular malformations, recent layoffs

Investors need clarity on four events.

First, the RLY-2608 doublet. At recent investor conferences, CEO Dr. Sanjiv Patel kept using the term "sprint toward approval" when referring to the upcoming pivotal study of RLY-2608 in breast cancer, which is expected to begin in mid-2025. However, the pivotal study still isn't listed in the public NIH database at the end of April.

Second, the RLY-2608 triplet. Investors now know that a preliminary data readout was delayed when Relay Therapeutics moved to fed-dosing. Will any data be available? If not in a separate press release, then at least in a section of the quarterly update announcement. Management has also publicly acknowledged the potential to find a partner for the triplet(s). Swiss-based Novartis is under pressure after coughing up its commercial lead with Piqray in breast cancer and Vijoice in vascular malformations (regulators revoked an accelerated approval in late 2024). Tariffs crank up the heat even more.

Third, the first clinical trial of RLY-2608 in vascular malformations opened for enrollment on April 17 – a little later than the first-quarter target, but not concerning considering the funding disruptions for hospitals triggered by the Trump administration. Either way, companies with functioning investor relations teams usually issue a press release for these milestones, especially considering this starts in phase 2.

Finally, another round of layoffs reduced headcount 42% below the peak set in 2022. Unfortunately, this isn't alarming given the landscape. Over half of precommercial drug developers have announced layoffs in the last 12 months, often stacking on top of previous headcount reductions. Case in point: I was laid off from my day job at Emerald Cloud Lab in April, too.

But I don't see the point. On the one hand, it's encouraging to see management protect RLY-2608 at all costs. On the other hand, the recent layoffs might only save $45 million in total cash burn in the next 36 months. That might only extend the cash runway by one quarter. Is losing talent worth it? Is my math wrong?

Repligen

- Modeled fair value: N/A

- Last close (April 25, 2025): $144.75 per share / $8.16 billion

- What to Watch: Tariff impacts, inventory management

Repligen provides tools and inputs for scaling and manufacturing biologic drugs like antibodies and cell therapies. Although it manufactures and assembles many products in its growing portfolio from U.S. facilities, many of the raw materials originate from China.

Investors will want clarity on the impact of tariffs. Fellow bioprocessing stalwart Avantor was crushed when it reported earnings last week thanks largely to a sharp decline in activity from academic customers (negatively impacted by funding woes induced by the Trump administration). Repligen primarily serves commercial customers, like drug developers and CDMOs, so it shouldn't face that headwind at least. But its stock cratered when tariffs were first announced in early April.

Did investors get ahead of themselves with the rapid recovery in the share price? I expect many companies have several months or quarters of inventory on hand, which can buy time to reroute supply chains and find alternatives. Repligen's unique exposure to electrical components, raw materials and chemical consumables, and certain types of semiconductors inject a little more uncertainty into the mix – an uncomfortable new reality for one of the positions I never have to babysit. Well, never had to.

Twist Bioscience

- Modeled fair value: $36.74 per share / $2.260 billion

- Last close (April 25, 2025): $40.11 per share / $2.40 billion

- What to Watch: Tariff impact on input costs

Twist Bioscience is one of the few companies in the coverage ecosystem with an obvious tariff risk. Although its products are assembled and manufactured in the United States, the plastics and chemical reagents used in its kits primarily originate in China. I'm not sure where the nucleotide raw materials that drive DNA synthesis originate from, but that could be a more significant risk if tariffs aren't resolved before inventory is exhausted.

The business also leans on international customers for 38% of revenue, including 30% in the Europe, Middle East, and Africa (EMEA) region and 8% in the Asia-Pacific region. If customers reside in countries that have placed tariffs on their own American imports, then they'll need to pay more for Twist Bioscience's products. That could create a growth headwind.

The DNA synthesis pioneer is a little riskier than a relatively stable stock price suggests.

.svg)

.svg)

.svg)

.png)

.svg)

.svg)

.svg)