.svg)

Earnings season starts today for the coverage ecosystem. You can find the confirmed dates for all companies in the quarterly Discord thread.

You'll notice a few new logos. Blueprint Medicines, SpringWorks Therapeutics, and Verve Therapeutics were acquired. Oxford Nanopore was booted due to my waning interest in covering a struggling tools provider against a backdrop of uncertainty, especially since U.K.-based companies only report twice a year. That creates potential blind spots. I think it's a bad time to have blind spots.

The graduates were replaced by four new companies:

Bicycle Therapeutics (Nasdaq: BCYC)

Bicycle Therapeutics brings a Nobel-prize winning technology to life with better drug delivery. Although its lead drug candidate is likely to deliver mixed results across a whopping 14 clinical programs, a preclinical radiopharmaceutical pipeline set to enter the clinic in 2026 has my attention.

Incyte (Nasdaq: INCY)

Incyte is easily the most experienced drug developer to draw interest from the Finch; responsible for almost half (124/257) of all lifetime clinical programs in the coverage ecosystem. Pipeline woes have consistently delayed its goal of achieving diverse growth in the last decade, but investors might be underestimating the near-term prospects. Oh, and it just hired Bill Meury as CEO. He helmed Karuna Therapeutics before it was acquired for $14 billion in March 2024, left to lead Anthos Therapeutic, then that was acquired for $3.1 billion in April 2025. Circle your calendars for May 2026 I guess!

Kiniksa Pharmaceuticals (Nasdaq: KNSA)

Kiniksa Pharma licensed Arcalyst from Regeneron, earned the first-ever approval in recurrent pericarditis, and expects full-year 2025 revenue of roughly $600 million. So naturally, the investment thesis hinges on ditching Regeneron and making Arcalyst obsolete. If it fails, then it still has Arcalyst. If it succeeds, then it'll be significantly more valuable. Investors will likely learn all they need to know from a data readout slated for 2026.

Kymera Therapeutics (Nasdaq: KYMR)

Kymera Tx brings an all-of-the-above approach to protein degradation, with pipeline programs spanning PROTAC protein degradation and molecular glues. Shares rocketed higher on an early data readout suggesting it might have a better, oral version of Dupixent, which is the 3rd-bestselling drug on the planet. A single high-impact asset can change everything, but Kymera is by far the least effective drug developer in the coverage ecosystem – a red flag potentially suggesting protein degraders have problems that aren't yet publicly known or being focused on.

Let's make a quick around the horn for what I'm looking for in this quarter's updates.

Potential High-Impact Updates

A high-impact update for a pipeline or portfolio has the potential to de-risk a business by removing uncertainty or forcing analysts to adjust expectations. These could be accompanied by larger stock moves or revised fair valuation estimates – in either direction.

AVITA Medical

- Modeled fair value: $6.48 per share / $225 million

- Last close (July 29, 2025): $5.80 per share / $154 million

- What to Watch: Commercial ramp, cash runway, and new sources of capital

Investors find themselves in a familiar (and uncomfortable) position heading into Q2 2025 earnings: a business update after a weak prior quarter.

That's not entirely true. The business is relatively strong and growing at a healthy clip, but management has set full-year 2025 revenue guidance at seemingly unrealistic levels. Missing sales guidance isn't an existential threat to a business. But it can be when management runs the business as if unrealistic guidance is possible, then runs out of cash.

AVITA Medical desperately needs capital to float itself to positive cash flow operations. It can't issue shares without stupid levels of dilution. It already has debt from OrbiMed and curiously rejected more credit from the financer. Unfortunately, I'm not confident a stellar business performance in Q2 will be enough to alleviate concerns about the cash runway, so any information about accessing more capital – in one of the worst times to need it – would be top of mind for investors.

Arrowhead Pharmaceuticals

- Modeled fair value: $27.75 per share / $3.871 billion

- Last close (July 29, 2025): $16.20 per share / $2.237 billion

- What to Watch: ARO-RAGE data, PDUFA date for plozasiran on track, updates on expected readouts for SHASTA and MUIR studies

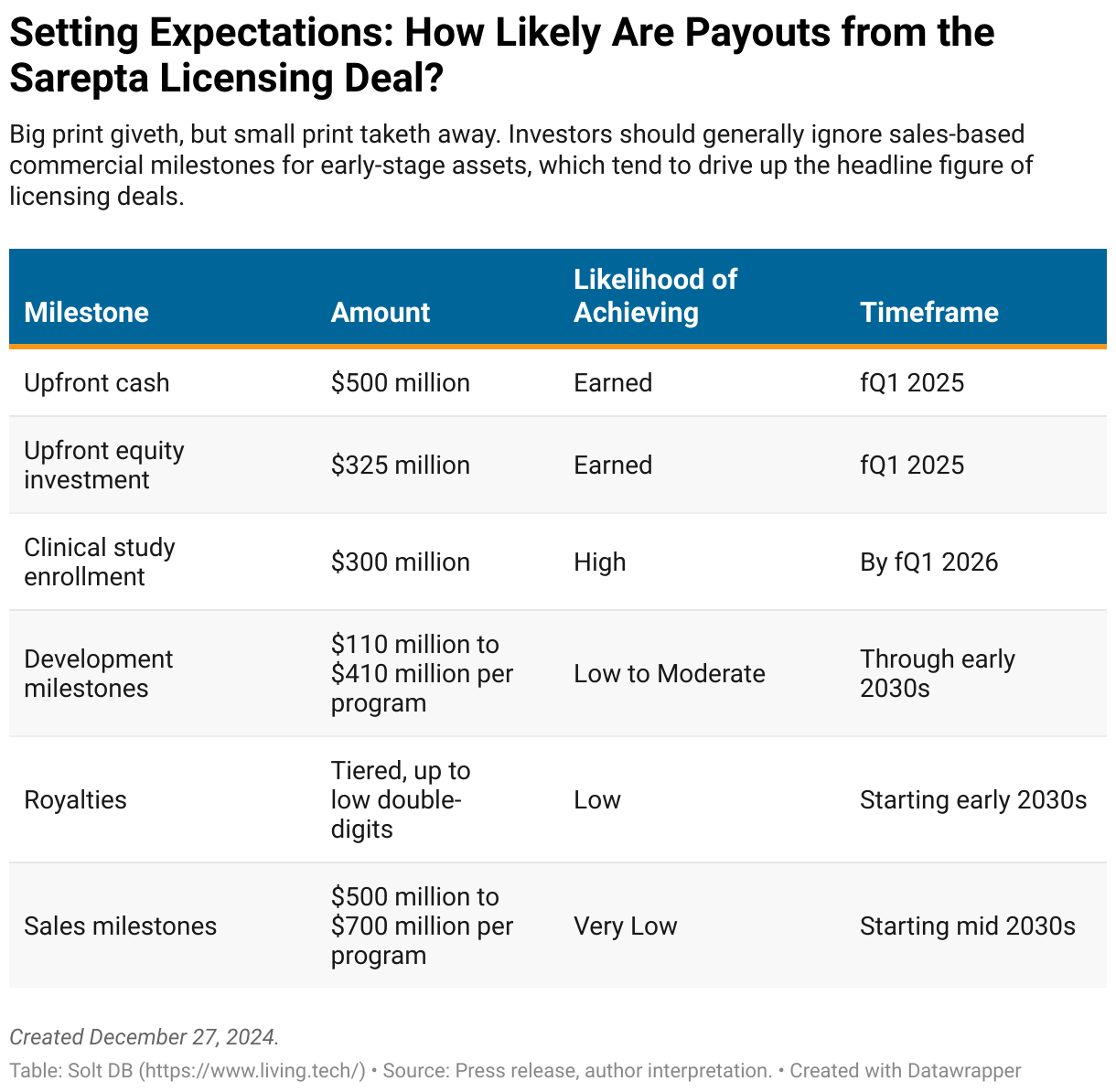

Arrowhead Pharma got swept up in the drama surrounding Sarepta Therapeutics, as investors jumped to conclusions about the partner's ability to pay. That never made much sense. For starters, Sarepta canned its gene therapy pipeline earlier this month, laid off 40% of its employees, and is now 100% focused on RNAi drug candidates licensed from Arrowhead.

Nor does the kneejerk reaction make sense when looking at the numbers. The RNAi pioneer received $825 million at closing, plus another $100 million in late July for hitting an enrollment target for ARO-DM1. It can clinch another $200 million enrollment milestone by the end of 2025. If Sarepta doesn't pay milestones for a program, then the asset's rights will be returned to Arrowhead. If it doesn't pay an annual R&D fee, then Arrowhead can terminate the entire agreement.

So far, nothing has deviated from my expectations laid out in the December 2024 research note analyzing the collaboration.

There are more important things than reacting to the market's kneejerk reaction.

The phase 1/2 study for ARO-RAGE, a high-impact asset with potential in asthma, wrapped up months ago. A data readout could coincide with the quarterly update on August 7. A relatively long period from study completion to data readout could be nothing, but it could also suggest the program will be terminated or partnered.

Management should give an update on the PDUFA date for plozasiran as a treatment for familial hypercholesterolemia (FCS), which is hopefully on track for November 18, 2025. Funding and headcount reductions at the FDA have resulted in multiple missed regulatory deadlines, although companies usually find out on the PDUFA date. Great.

Finally, Arrowhead has completed enrollment for three separate phase 3 programs for plozasiran – SHASTA-3, SHASTA-4, and MUIR-3 – aimed at expanding into severe hypertriglyceridemia (SHTG). Whereas less than 1,000 individuals have FCS in the United States, roughly 3.5 million have SHTG.

Coherus Oncology

- Modeled fair value: $3.12 per share / $380 million

- Last close (July 29, 2025): $1.07 per share / $124 million

- What to Watch: Beating the drum for data readouts in 2026

Coherus Oncology ended Q2 with a new name, a newly-clean balance sheet, and some new swag. Will it matter?

Loqtorzi should have over $9.5 million in quarterly revenue (>30% growth from Q1), but to be blunt, the current approval in nasopharyngeal carcinoma (NPC) makes it a low-impact asset. It's not the main driver for the stock.

That distinction belongs to the pipeline. The CCR8 inhibitor, CHS-114, is being positioned as the company's most important asset in recent investor presentations. That aligns with my analysis of the opportunity shared in an October 2024 research note. The more mature IL-27 inhibitor, casdozokitug, represents a multi-billion dollar opportunity itself.

No one wants to hear this, but investors simply have to wait for the three to four data readouts from the pipeline in 2026. The stock is likely to be very volatile between now and then – I wouldn't rule out another dip below $1 per share later this year.

In the near-term, two "catalysts" could lift the share price. First, as silly as it sounds, the company's cash balance and debt level will be updated in financial dashboards. That will make Coherus leap to the top of many stock screeners searching for value metrics. Second, meme stocks are back again. A good swath of them have been driven by short squeezes, which could potentially launch Coherus to unsustainable short-term gains. As of mid-July, 28% of all available shares are being shorted.

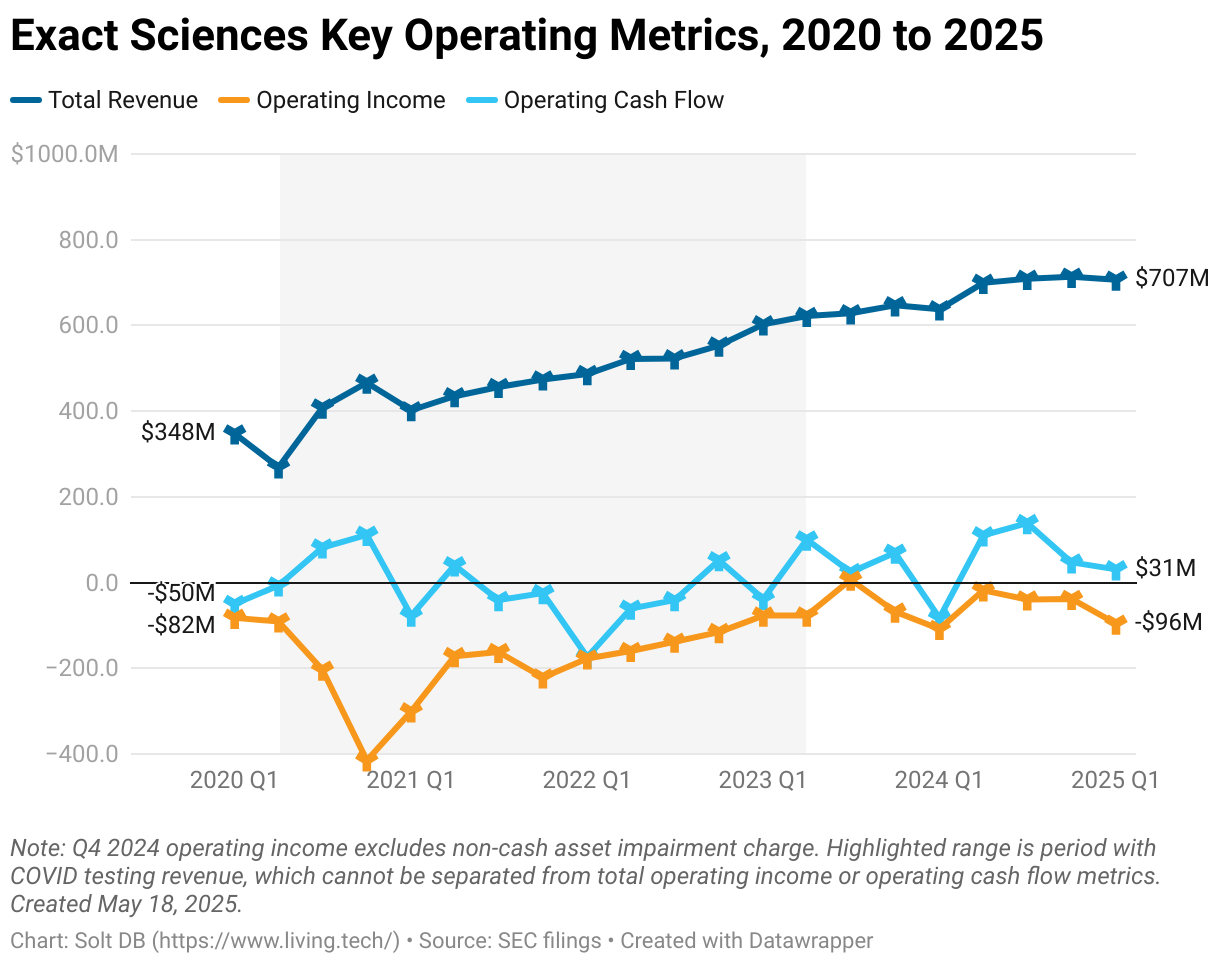

Exact Sciences

- Modeled fair value: $85.69 per share / $16.488 billion

- Last close (July 29, 2025): $48.04 per share / $9.062 billion

- What to Watch: BLUE-C results, commercial ramp

Exact Sciences expects a pivotal data readout from the BLUE-C study, evaluating a blood-based colon cancer screening tool, in "mid-summer." Similar to ARO-RAGE, that readout could coincide with the quarterly business update. The tool is likely to fall short of the specificity threshold required for Medicare coverage, but it might perform well enough on other metrics to earn regulatory wiggle room. Either way, announcing data with earnings could soften the blow.

The business is a cash flow machine and barreling toward profitability. It's also on the cusp of an expected growth surge. After reporting between $699 million and $713 million in quarterly revenue for the last four quarters, full-year 2025 guidance expects an average of $799 million in sales over the final three quarters of the year. Investors appear to have been lulled to sleep. Again.

Similar to the opportunity presented by the Q1 earnings update, Exact Sciences might be a good opportunistic investment – if the liquid screener's data don't ruin the party.

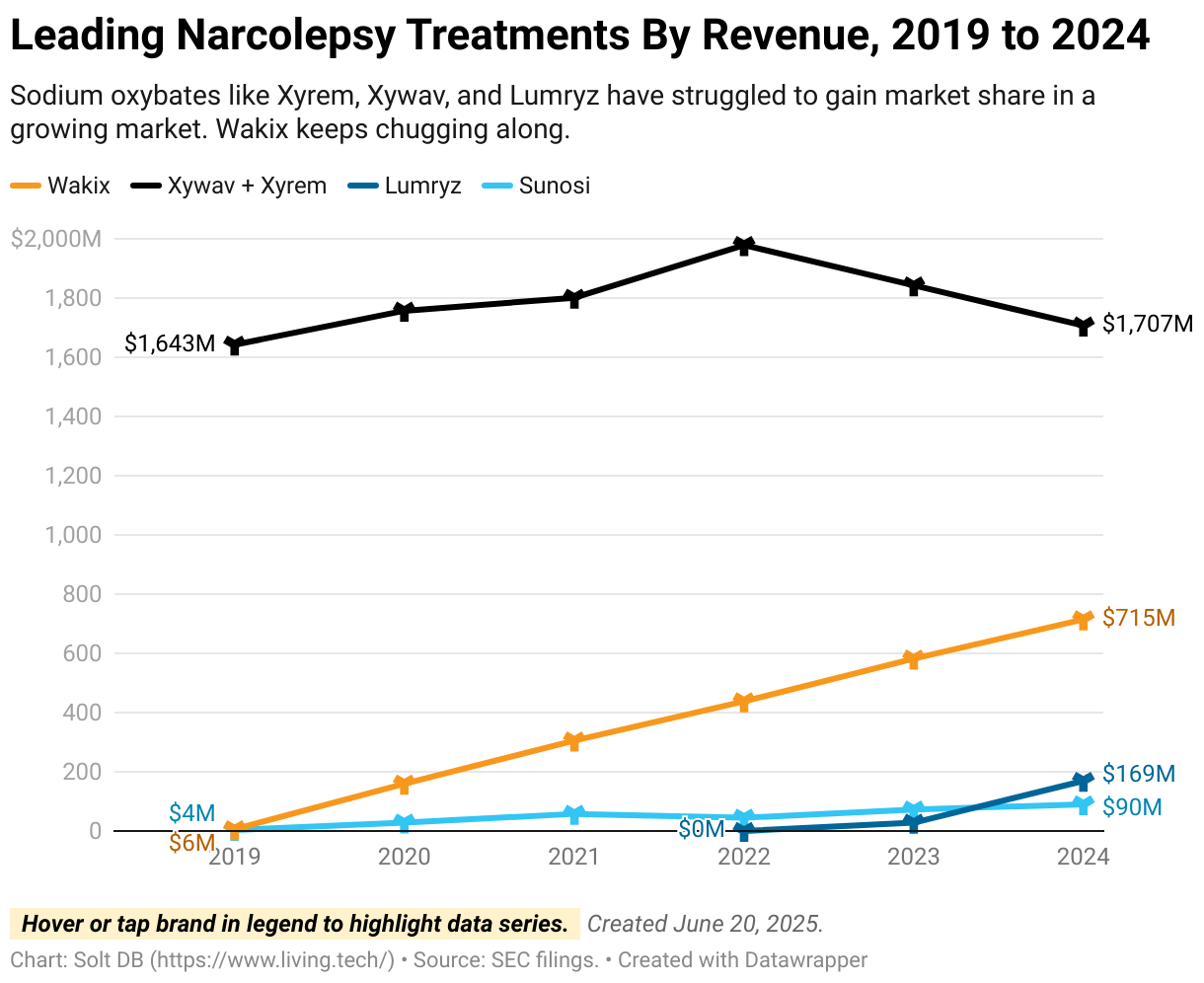

Harmony Biosciences

- Modeled fair value: $65.24 per share / $3.803 billion

- Last close (July 29, 2025): $35.76 per share / $2.053 billion

- What to Watch: RECONNECT data readout, ongoing commercial ramp, new collaboration with Circ Biosciences

All eyes are on the pivotal data readout for the RECONNECT study expected in by the end of September 2025. Similar to ARO-RAGE and BLUE-C, it wouldn't be surprising to see data announced with quarterly results.

If successful and ZYN002 goes on to earn regulatory approval, then Harmony Biosciences will have the first and only treatment for any symptom of fragile X syndrome (FXS). A negative data readout shouldn't impact shares for long, as the asset isn't currently factored into the valuation. The company can also quickly deploy $150 million in an existing share buyback program. I think it's an attractive risk/reward profile.

Wakix continues to shine in the narcolepsy market. There's not much that can ding its trajectory in the near term, so investors should expect a steady march toward the full-year 2025 guidance midpoint of $820 million. If the business can resume earnings growth this year, then shares could be significantly higher before Thanksgiving.

Harmony Biosciences will also announce a new collaboration with Circ Biosciences when it reports Q3 2025 earnings on August 5. The small company has a technology platform for reprogramming stem cells into specific types of brain cells. For a $15 million upfront payment, the narcolepsy stalwart will help develop two preclinical programs with the potential to treat rare epilepsies and at least narcolepsy type 1 (NT1).

Incyte (new)

- Modeled fair value: N/A

- Last close (July 29, 2025): $70.16 per share / $13.581 billion

- What to Watch: How will new CEO Bill Meury make his mark?

New CEO Bill Meury timed his arrival perfectly.

Incyte's trailing 12-month (TTM) earnings look atrocious, but that's only because of a one-time charge recorded in the second quarter of 2024. The $679 million expense resulted in full-year 2024 net income of just $32 million – and it rolls off the books soon. That should result in a new TTM price-to-earnings (PE) ratio of about 19.5x.

Although Incyte has grown into a $13.5 billion drug developer with 21 active clinical programs, regime change could herald pipeline prioritization decisions. Does Meury axe a few programs? Refocus the company on specific indications or assets? Make splashy acquisitions with the company's $2.4 billion in cash?

The company's crown jewel, Jakafi, loses patent exclusivity in 2028. It represents 75% of total revenue. While a new formulation is in late-stage testing, revenue concentration raises the stakes for pipeline prioritization decisions or acquisitions.

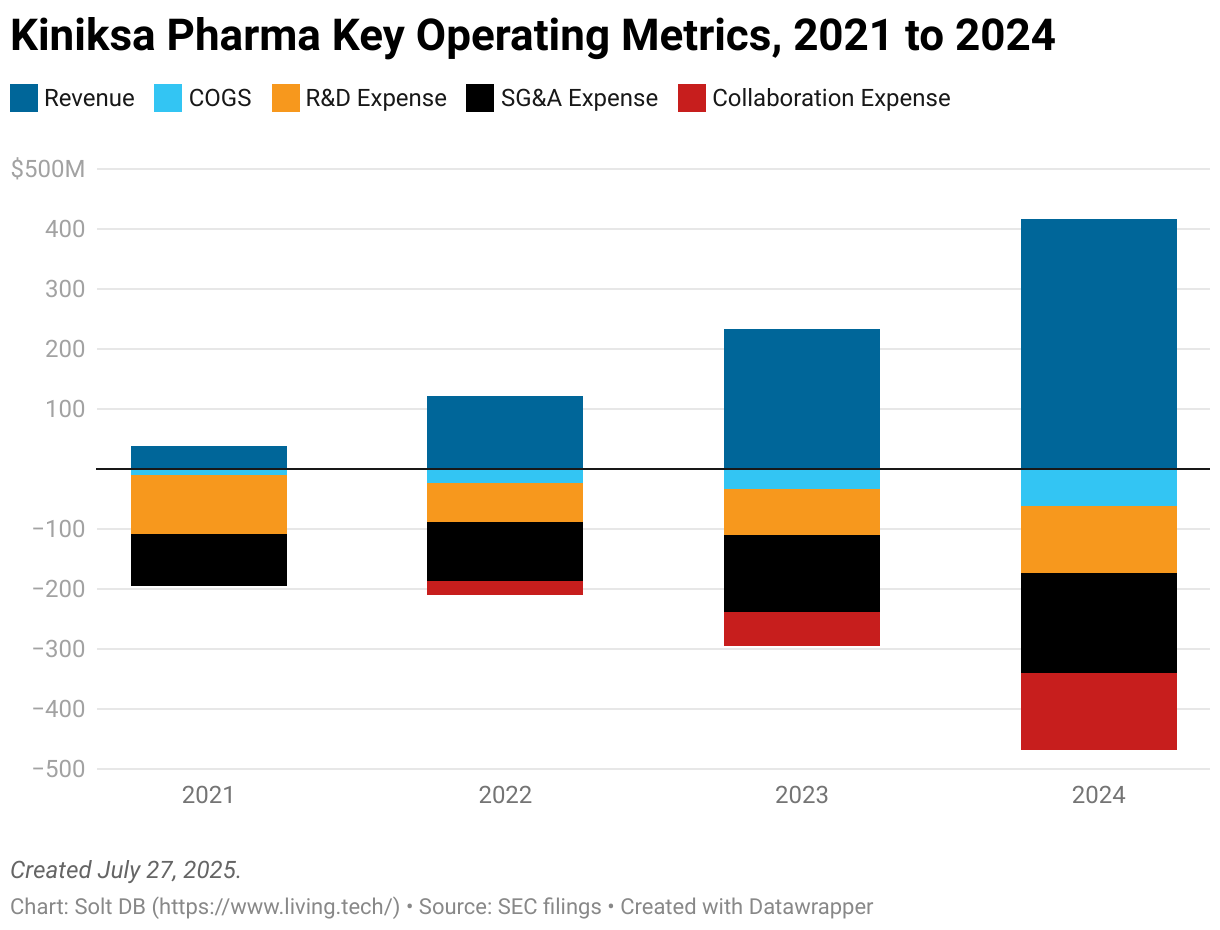

Kiniksa Pharma (new)

- Modeled fair value: $22.45 per share / $1.687 billion

- Last close (July 29, 2025): $27.04 per share / $1.973 billion

- What to Watch: Continued commercial ramp, expectations for KPL-387

In 2024, Arcalyst generated $417 million in revenue with just 13% market penetration in a barren competitive landscape. Full-year 2025 revenue is expected to be about $600 million. There's not much that can derail the product in the near term.

Kiniksa Pharma is trying though.

The company got a sweetheart deal from Regeneron, licensing Arcalyst for just $5 million upfront. But commercial success has brought new headaches. Kiniksa expects to report its fourth consecutive year of positive operating cash flow, but it generated only $45 million in total cash flow in the last three years combined. That's because it pays healthy royalties to Regeneron, recorded as collaboration expense, which could top $200 million this year. It's a drag.

Kiniksa is developing two wholly-owned, next-generation drug candidates that should work similarly to Arcalyst and offer more convenience. Whereas Arcalyst is dosed once-weekly, KPL-387 would only be dosed once-monthly, while KPL-1161 may enable once-quarterly dosing. A phase 2/3 program for KPL-387 should have initial data in 2026. If it's comparable to Arcalyst, then investors can dream of the day Kiniksa breaks free of Regeneron – or forces its hand at an acquisition.

We Have Questions

The future can never be predicted with perfect accuracy, but sometimes the world moves faster (or companies move slower) than investors like. Some investments require a little more babysitting and objective criticisms, especially when management provides infrequent updates or uncertainty creeps in on previously communicated timelines.

Arvinas

- Modeled fair value: N/A

- Last close (July 29, 2025): $7.61 per share / $572 million

- What to Watch: Vepdeg strategy, emerging pipeline

Arvinas and Pfizer reported lackluster pivotal data for their estrogen-receptor (ER) degrader, vepdegestrant, in HR+/HER2- breast cancer. It did show a benefit in a subset of tumors with an ESR1 mutation, and the duo are forging ahead with a new drug application (NDA). Competing assets from Eli Lilly and Roche encountered similar struggles, but performed better than vepdeg. In other words, the commercial opportunity isn't very clear. Investors might even wonder if the FDA will reject the submission altogether.

Pfizer greatly scaled back its development plans for vepdeg by axing combination studies with CDK4/6 and CDK4 inhibitors. If it doesn't earn approval in ESR1 mutated breast cancers, then the larger pharma might hand back rights to Arvinas.

The protein degradation pioneer will need to refocus on wholly-owned assets where protein degraders could have an advantage. That includes ARV-393 (BCL6 inhibitor), being evaluated for blood cancers, and ARV-102 (LRRK2 inhibitor), being evaluated for neurodegenerative conditions like Parkinson's disease. The neuro pipeline is especially important, as the ability to cross the blood-brain barrier with oral dosing while maintaining target selectivity is a key advantage for protein degraders.

Barring a new collaboration, investors will need to patiently wait for initial clinical results expected in 2026.

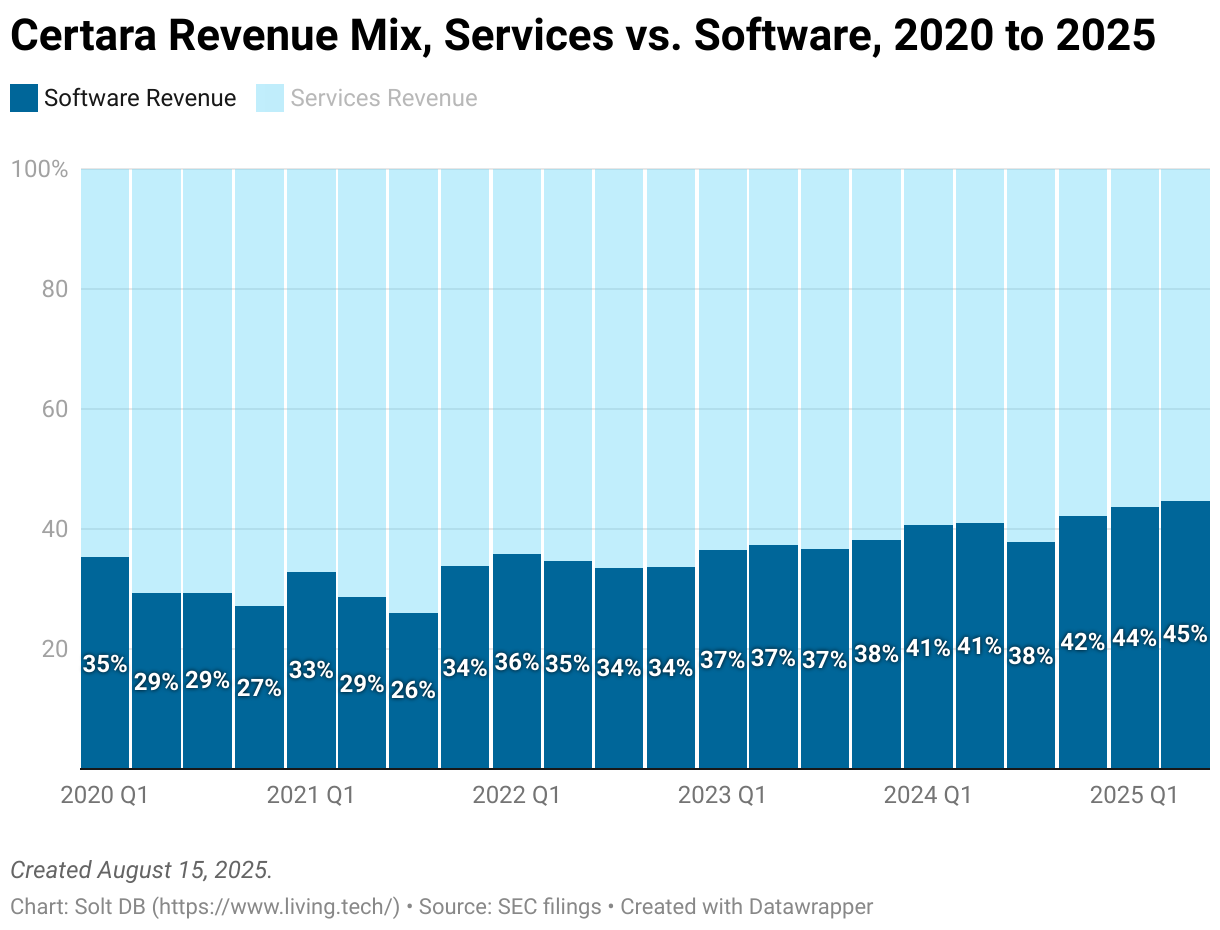

Certara

- Modeled fair value: $11.62 per share / $1.903 billion

- Last close (July 29, 2025): $11.07 per share / $1.796 billion

- What to Watch: Can Regulatory Services be divested?, commercial momentum

The irony of the market potentially being in an AI bubble is that Certara never joined in the fun. Maybe it needs to buy bitcoin to change its fortunes.

Shares spiked on the FDA's planned timeline for phasing out animal studies in preclinical data submissions for monoclonal antibody drug candidates, but the excitement was quickly drowned out by a tidal wave of broad regulatory uncertainty facing the sector.

Shares sank when the agency unveiled its own LLM chatbot, Elsa, purported to aid regulators in reviewing submissions. Most public reports suggest the tool was rushed out and may not be around much longer. Either way, to highlight the gap between the average perception of AI tools in the stock market and their real-world capabilities, Certara's built-for-purpose software cannot be replaced by a general purpose LLM.

The business could shake off the rust soon. Certara expects to return to growth in 2025, but operations should see steeper growth in the second half of the year. If that momentum can build through the end of 2026, then shares could secure a slow-and-steady ramp through the rest of the decade. Investors will simply need to remain patient with this position, although more software acquisitions can help accelerate the glow up.

Perhaps the most important thing for investors to watch is the divestiture of the Regulatory Services unit. It wouldn't result in a large payday – likely near $50 million – but it would allow Certara to follow through with a $100 million share buyback plan. Is a divestment still possible?

Codexis

- Modeled fair value: $4.43 per share / $422 million

- Last close (July 29, 2025): $3.04 per share / $252 million

- What to Watch: Updates on ECO Synthesis

Codexis won't be a very good investment if it cannot commercialize ECO Synthesis or use technical progress to get acquired. If enzymatic synthesis of short-interfering RNA (siRNA) for RNAi therapeutics doesn't pan out in time, then piecemeal manufacturing contracts for various other drug products are unlikely to drive the valuation much higher.

The enzyme engineering pioneer will likely have another quarter of choppy revenue – investors already know a payment was delayed from Q1 to Q2 – but all eyes will be on the technical and commercial timelines for the ECO Synthesis platform.

Day One Bio

- Modeled fair value: N/A

- Last close (July 29, 2025): $7.10 per share / $733 million

- What to Watch: Commercial ramp, DAY301 updates

Day One Bio earned a speedy approval for Ojemda, but it's not a high-impact asset. That means it alone won't be able to fund operations. More troubling, the investment needed to build commercial infrastructure for the first time can gradually sink an emerging drug developer, or at least force tough choices down the road.

Ojemda has value. As it ramps, it can at least offset a growing share of operating expenses. Early progress is encouraging. The business shrank its operating loss 38% from Q1 2024 to Q1 2025. The only hiccup is that companies like this don't tend to earn significant valuations or premiums.

That's what makes the lead drug candidate, DAY301, important for investors. The antibody-drug conjugate (ADC) targets PTK7, which is a highly sought-after target in various tumor types. The issue has been safely delivering the therapeutic payload. Day One Bio's asset has a unique structure that could address that very problem, but investors need to wait a few more quarters for initial clinical results to back up that potential.

Recursion Pharma

- Modeled fair value: $2.21 per share / $1.032 billion

- Last close (July 29, 2025): $6.31 per share / $2.736 billion

- What to Watch: More details on development strategy

Recursion Pharma touts itself as a leader in AI drug discovery, but someone should tell the company it also needs to develop drugs.

The company has never advanced a drug candidate past phase 2 development. It's never demonstrated superior efficacy for a drug candidate. It's never run a clinical study with more than 92 patients. Despite having 11 unique clinical assets in its lifetime, six programs were terminated and another remains paused. Three of the five active pipeline programs originated from Exscientia.

Those aren't the characteristics of a technology platform or company changing the paradigm of drug development.

Recursion boasts an R&D productivity factor of -1.6x, meaning its 1.6x worse than the expected average success rate across its programs. The only other company in the coverage ecosystem with negative R&D productivity is Kymera Tx (-4.0x), and at least it has a high-impact asset or two in the pipeline.

Investors should be looking for clarity on the development strategy following the recent reprioritization. Does management have more details on expected timelines? Will collaborations help offset some of the internal pipeline struggles?

.svg)

.svg)

.svg)

.png)

.svg)

.svg)

.svg)