.svg)

"Price discovery" is the bean-counter term for finding mispriced assets. It's why we make investments in businesses to begin with.

But these aren't the olden times when Buffett had to request physical copies of annual reports in the mail, and it took weeks to complete a trade. Today everyone has access to the same information – financial metrics, sector comparisons, conference call transcripts – in real time. Are any of us really going to have some magical insight when reading the financial reports of a business like Procter & Gamble or Apple?

No f*nching way.

However, biotech is one of the very few places in the public markets where the little guy can have an edge. Although every sector has unique attributes where domain competence provides more clarity, drug development might be the most challenging to understand because investors must convert molecules into dollars. You rarely have to do that for barrels of oil, data centers, or advertising. Those metrics are already neatly expressed in dollars.

That single extra step of converting molecules into dollars results in rampant mispricing of biotech stocks – in both directions. High-impact assets can be overlooked for long periods of time, while markets can get carried away with insignificant advances.

The sector's mispricing is exacerbated by another unique attribute: drug developers are typically built for an acquisition. Do investors value an asset for its commercial potential five years from now? What about competitive landscape dynamics? None of that matters if Pfizer or Roche sees an opportunity to acquire a promising molecule or platform.

A recent surge in acquisitions has triggered significant momentum for biotech stocks as 2025 draws to a close. That's partially due to lowly valuations following a four-year biotech winter, and partially due to high valuations for the broader market.

Is it sustainable? And just for fun, how would I rank the acquisition potential of companies in the coverage ecosystem?

A Record Year for Biotech Acquisitions

Despite a lingering recession for the American biotech sector, there was a record number of acquisitions in 2025. Can you feel it?

There have been 46 acquisitions this year through December 15, according to M&A data compiled by BioPharma Dive. That slightly outpaces the previous record of 43 set in 2022. The pace of acquisitions has also been relatively stable throughout the year, whereas recent years have had long stretches with no dealmaking.

Both years benefitted from relatively low valuations. Large price declines in 2022 looked favorable compared to record highs set in the prior two years. Little did we know that valuations would continue sliding for the next few years. But pessimism has limits. More data, dwindling cash runways, and falling interest rates – reversing the very thing that kicked off the biotech winter – have all aided dealmaking in 2025.

The value of acquisitions also rebounded this year. These data only include upfront value and exclude payouts contingent on hitting future milestones.

Evaluating trends in deal value is trickier. Since 2018, drug developers have been acquired for as little as $48 million and as much as $74,000 million. That has a funny way of throwing off averages and totals. Similarly, the number of acquisitions in a calendar year has ranged from 24 to 46. That results in muddy medians.

The trend becomes clearer when adjusting for mega deals. When acquisitions above $10 billion are excluded from the dataset, total deal value in 2025 is easily a record – roughly doubling activity from 2018 to 2022.

There are two weeks remaining in 2025 as of this writing, so the sector could continue adding to a record year. Will it continue in 2026?

A looming patent cliff for large pharma in the second half of the decade could drive healthy deal volume and value. Interest rate cuts across Western economies could also provide a tailwind, although cutting rates into a recession has historically crimped M&A activity.

If anything is evident in the biotech acquisition dataset from BioPharma Dive, then it's the simple reality that, in any given year, regardless of valuations or interest rates, there are always a few dozen high-quality drug developers getting scooped up. Investors shouldn't expect 2026 to be any different.

Ranking the Acquisition Potential of the Coverage Ecosystem

Well first, I think Exact Sciences has great acquisition potential…

Kidding aside, the $21 billion deal with Abbott Laboratories (excluded from the datasets above by the way, which only include drug developers) is a reminder that quality matters.

Exact Sciences is on pace to generate roughly $500 million in operating cash flow in 2025 and should generate GAAP net income in 2026. It doesn't have a better technology platform than Natera or Guardant Health, but Abbott can immediately reap financial benefits and doesn't have to divert its own cash flows to keep the business afloat.

The same is true for drug developers. Companies with high-impact assets on the cusp of commercial launches or early in their growth trajectory are more likely to trade at healthy premiums – and be acquired for the "right" reasons. Recent examples include SpringWorks Therapeutics (acquired for $3.9 billion) and Blueprint Medicines (acquired for $9.1 billion).

How would I rank the acquisition potential of the coverage ecosystem?

Let's consider the likelihood of a buyout in the next 12 months. I'd also make a key distinction: investors might be tacking on speculative premiums to high-quality companies, but that doesn't mean those companies are looking for an exit.

Arcus Biosciences (highest)

Arcus Biosciences is the most mature precommercial immuno-oncology company on the market. That deserves a premium. It also harbors the de facto PD-1 inhibitor of Gilead Sciences, which owns 29.3% of the drug developer. Although the partners just terminated development of their TIGIT inhibitor domvanalimab in gastric cancers, the value of immuno-oncology pipelines comes from combinations. The no-go decision merely removes an arrow from the quiver.

The lead drug candidate, HIF-2-alpha inhibitor casdatifan, holds promise in kidney cancer. The only other molecule in the class on the market, Merck's Welireg (belzutifan), is on pace to deliver full-year 2025 revenue of roughly $700 million. Data reported to date suggest casdatifan could outperform Welireg. Meanwhile, the recent unveiling of an immunology pipeline adds future value potential, albeit early.

Arrowhead Pharmaceuticals (above average)

Arrowhead Pharma is one of the high-quality companies being assigned a healthy speculative premium, but the company hasn't exactly positioned itself for an acquisition. It has expertly monetized R&D in recent years to keep the lights on, just earned its first FDA approval, has multiple pipelines and technology platforms hitting their stride, and has made significant investments in a wholly-owned manufacturing facility in Wisconsin. The best days are still ahead for the RNAi pioneer.

And hey, not for nothing, but big brother Alnylam Pharma has clawed its way to a $51 billion valuation. Why would Arrowhead's board of directors want to exit near a $10 billion valuation?

If Arrowhead's neuro pipeline shows promise crossing the blood-brain barrier and its bispecific RNAi shows promise in reducing heart disease risk, then it'll have differentiated assets with relatively little direct competition. Throw in emerging obesity assets and, even if companies are interested in acquiring the business, it's difficult to see that being in the best interest of shareholders. Therefore, I wouldn't group it with the highest potential peers (unless Eli Lilly busts out the checkbook).

AVITA Medical (average)

AVITA Medical went from the apple of my eye to a sharp pencil repeatedly jabbing my orbital sockets. The recent management change could be the first step in a turnaround – after all, the technology platform absolutely works – but there aren't any easy ways to fix the cash runway. Unfortunately, the window might be slammed shut if an economic slowdown or credit crisis makes investors nervous or incapable of lending to high-risk businesses.

If AVITA Medical can fix its commercial flaws and potentially dust off the stable vitiligo indication for licensing (it did earn FDA Breakthrough Device designation), then the company could still get acquired, but more likely out of desperation.

Bicycle Therapeutics (average)

Bicycle Therapeutics is one of three companies in the coverage ecosystem with a technology platform directly powered by a Nobel Prize-winning invention. The company's novel payload chemistries have the potential to anoint small molecule drugs with the tissue targeting attributes typically only reserved for antibody drugs. Such an approach has broad potential across therapeutic modalities and therapeutic areas. Indeed, the drug developer is currently focused on peptides that mimic ADCs, radiopharmaceuticals, and theranostics (radioimaging).

The lead drug candidate, zelenectide pevedotin, is a peptide that binds to a common cell receptor called Nectin-4. That's the same target of Padcev, a blockbuster ADC developed by SeaGen prior to its acquisition by Pfizer. Unfortunately, good ol' zele didn't deliver on the promise of the technology platform with initial results shared in late 2024. There didn't appear to be any meaningful efficacy advantages for Bicycle's approach vs. clinical data from Padcev in bladder cancer.

Management expects to provide an update on the asset's future after meeting with global regulators in Q1 2026. I think it's more likely than not to be terminated, which would force the business to pivot to its radiopharmaceutical and theranostics pipelines. Pivots usually hurt – and I'd expect shares to get whacked on a no-go decision – but I'm most interested in the emerging pipelines anyway. Nonetheless, there's not much to acquire yet unless the company panics and sells out of desperation.

Certara (below average)

As a self-funding business, Certara controls its own destiny. It finds itself favorably positioned as global regulatory agencies seek ways to accelerate and modernize drug development without sacrificing quality. A rare CEO change suggests the board of directors wants to triple down on high-margin software growth, especially considering John Resnick spent over 20 years at clinical data and software provider IQVIA.

However, hesitant customers could signal another painfully slow year for revenue growth in 2026. My read is that Certara simply has to wait for capital to flow more freely again to realize its true potential. Frustrating? Sure. A reason for the company to seek a sale? Nope.

Codexis (above average)

Similar to Certara, the board of directors made a rare change at the helm of Codexis. Unlike Certara, recent management changes make an acquisition more likely. Maybe not in the next 12 months as specified above, but eventually.

The industrial enzyme producer's fate rests on its ECO Synthesis platform for manufacturing the short-interfering RNA (siRNA) molecules that power RNAi therapeutics. Codexis still has a number of important technical milestones to deliver for the technology, but I think the primary question is how many delays are encountered (and how that pressures the cash runway) rather than whether they'll pull through.

Potential suitors include Agilent (one of the leaders in siRNA manufacturing) and Novonesis (the largest industrial enzyme company, created through the merger of two giants, Chr. Hansen and Novozymes).

Coherus Oncology (highest)

Coherus Oncology is doing everything it can to position itself for an acquisition, from cleaning house within its investor relations team to attending the JP Morgan Healthcare Conference in January. Heck, it's even sponsoring web content on the rise of CCR8. Shout out Findil for sharing on Discord.

A slew of data readouts expected in 2026 could create the buzz necessary to close a deal. It's also possible for the business to forge ahead with larger long-term aspirations in mind, but being handed big bags of cash is way more exhilarating.

Day One Bio (above average)

Despite recent rumors about Day One Bio being a takeover target, I think that's more contingent on data readouts for DAY301 than investors realize. The PTK7 inhibitor could put the elusive oncology target in play, owing to the antibody drug conjugate's (ADC) unique linker chemistry that may mitigate tolerability issues that derailed past attempts.

Oh, one important detail: there aren't any meaningful data yet. If Day One Bio delivers promising early data from the asset in 2026, then its valuation is likely to surge. It would then become a very likely acquisition target. Until and unless that happens, potential suitors are unlikely to open the checkbooks for Ojemda alone. It simply isn't a high-impact asset.

Harmony Biosciences (highest)

If quality matters, then Harmony Biosciences is sitting pretty. Wakix is the strongest brand in the dynamic narcolepsy landscape despite being in its sixth year on the market. That suggests it has strong commercial infrastructure, too. Throw in an early-stage orexin-2 receptor (OX2R) agonist drug candidate, consistent cash flow, an ever-growing cash pile, and a relatively low valuation, and it's not difficult to imagine potential suitors sizing up the business.

Management keeps telling investors it's working on business development activities. As in, Harmony Biosciences might be the one making acquisitions. But the high-profile failure in the RECONNECT study may have convinced the board of directors to look for an exit. An unusually strong Q3 performance and a likely repeat in Q4 provides a window to capitalize on surging momentum. Will management take advantage?

Incyte (above average)

A record year for biotech M&A is only evident when excluding acquisitions greater than $10 billion. We'd have to include those again should Incyte find a dance partner. The currently $19 billion drug developer has long been considered a top takeover target, but consistent clinical stumbles have crushed attempts to diversify revenue and hushed acquisition talk.

On the one hand, the oncology company's crown jewel Jakafi will face generic competition by the end of the decade. The brand is responsible for 69% of total product revenue, which makes the ticking clock louder with each passing quarter. Opzelura has provided much-welcomed diversity to the revenue base, weighing in at over 16% of product sales, but it alone cannot carry the business.

On the other hand, Incyte presented more than 50 abstracts at the American Society of Hematology (ASH) Meeting this month. That included promising data for INCA033989, a pan-CALR inhibitor with the potential to replace Jakafi soon after it loses market exclusivity. It earned FDA Breakthrough Therapy designation the same week.

The company also reset its C-suite roster in 2025, including the appointment of Bill Meury as CEO. He was the CEO of Karuna Therapeutics when it was acquired by Bristol Myers Squibb for $14 billion in March 2024, then hopped over to man the helm of Anthos Therapeutics – which was acquired by Novartis for $925 million in April 2025. Can he deliver a three-peat?

Kiniksa Pharma (highest)

Breaking up is never easy. For Kiniksa Pharmaceuticals, it means ditching the top 20 pharma partner that enabled its glow up and disrupting its only source of revenue. Definitely can't do that in a text.

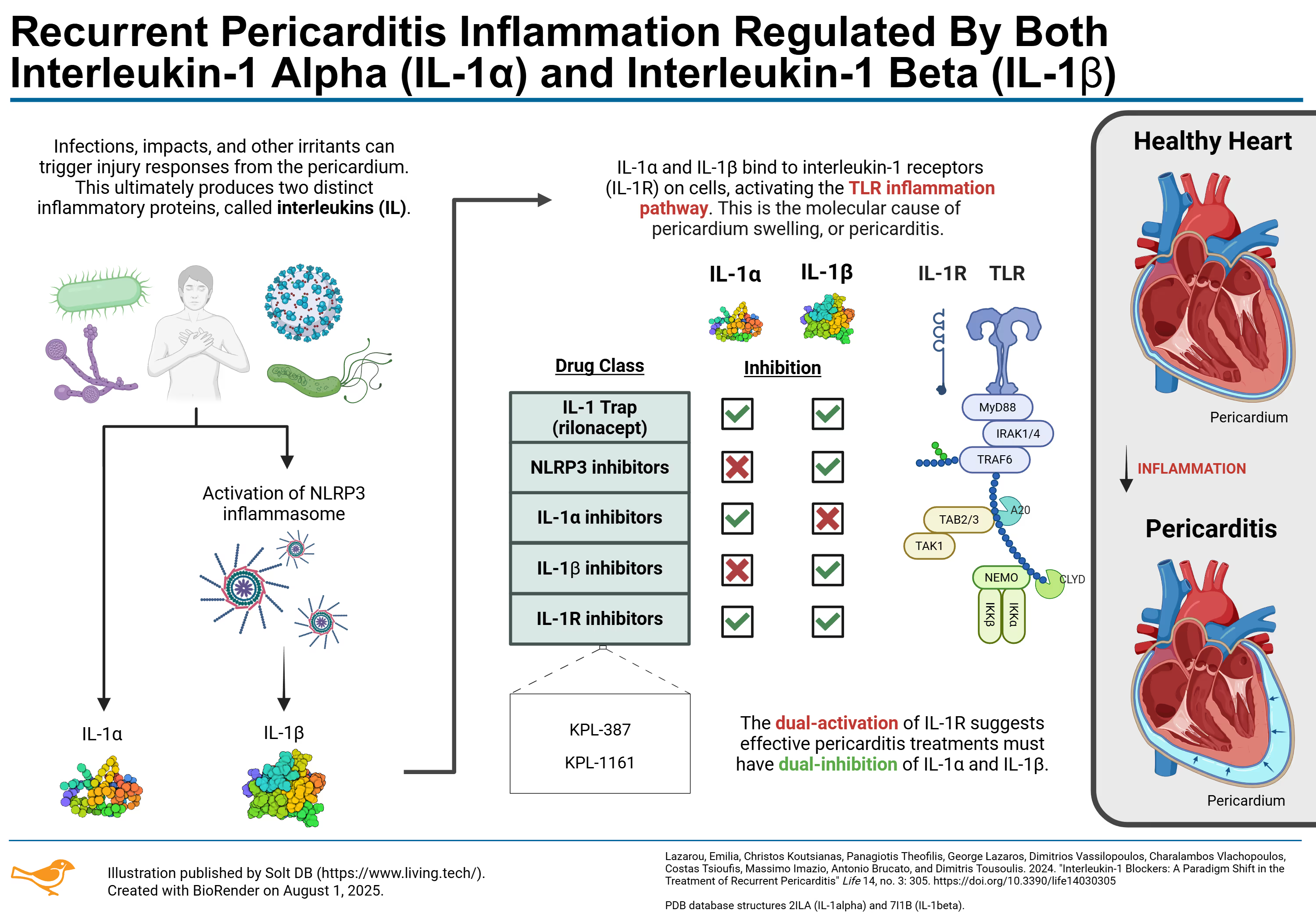

The drug developer owns the rights to Arcalyst in recurrent pericarditis, but Regeneron owns the asset. That means Kiniksa must pay hefty royalties on each sale. In the first nine months of 2025, the drug developer reported $475 million in revenue and $159 million in collaboration expenses. Although the business is profitable, the arrangement is a big drag on its financial flexibility.

The good news is that Arcalyst is uncontested in recurrent pericarditis and the mechanism of action will be difficult to beat. Case in point, Arcalyst was almost 100% effective in its pivotal study. The better news is Kiniksa Pharma is developing two wholly-owned antibody drug candidates that could match the performance of Arcalyst with more convenient dosing to boot.

Kiniksa expects to report phase 2 data for KPL-387 in 2H 2026. That will set expectations for the pivotal portion of the same study – and could force Regeneron to acquire its licensee to avoid changing its relationship status to "it's complicated."

Krystal Biotech (highest)

The worst-kept secret in drug development is that Krystal Biotech was built for an acquisition since its founding. The husband and wife founders own 10% of the business – an unusually high percentage in biotech – and were mentored by RJ Kirk, a lawyer who became a billionaire when he sold New River Pharmaceuticals. All three are a bit shady, but hey, it's 2025, look around at who actually gets ahead in the world.

Krystal Biotech trades at a healthy premium thanks to the commercial strength of Vyjuvek, which has no meaningful competition now or on the horizon. International launches in Europe and Japan should power the asset through what appears to be a sales plateau in the United States, but the window for an exit won't be open indefinitely.

A lack of pipeline activity could hamper those ambitions, but future data readouts for KB707 in lung cancer and KB408 in alpha-1 antitrypsin (A1AT) deficiency could convince potential suitors that there's enough asset diversity to make a deal.

Recursion Pharma (average)

Recursion is yet another company that made management changes recently. Founder and CEO Chris Gibson stepped aside to let relative newcomer Najat Khan take the reins. She joined the company in 2024 after holding various positions at Johnson & Johnson, primarily leading R&D activities.

The primary roadblock for an acquisition is simple: What is there to acquire? Recursion has built impressive lab automation capabilities, but barcoding test tubes and properly labeling data doesn't automatically translate into commercially-viable R&D. The company has never advanced an asset past phase 2 study and has no coherent commercial strategy. The acquisition of Exscientia added a few molecules with more promise, but none have reported mid-stage data yet.

Relay Therapeutics (above average)

If Relay Therapeutics is trying to get acquired, then it would be difficult to tell. Management made difficult decisions to significantly reduce headcount, shelve preclinical assets, and whittle down the pipeline to a handful of shots on goal – all taken to protect the lead asset. The strategic shift makes sense considering zovegalisib is one of the most valuable assets in the global industry pipeline.

The details matter, too. Relay wasn't forced to slow walk its near-term ambitions due to clinical failures or busted development hypotheses. It came down to economics. The remaining assets and indications each harbor high-impact potential.

I'm certainly biased. I don't want the business to be acquired any time soon. At the same time, the commercial value of zovegalisib in just CDKi-experienced breast cancer patients greatly exceeds the current valuation of the business. There's no incentive for the board of directors to entertain an exit, and it would be difficult to snag an acquisition premium from current levels that properly prices in future potential. Relay might be enjoying a slight speculative premium as investors realize it might be a takeover target, but I simply don't see a deal as likely.

Twist Bioscience (below average)

Similar to Certara, I don't think Twist Bioscience is an obvious acquisition candidate. The business is strong, improving, and on the path to positive cash flow later this decade. It's close to controlling its own destiny.

At the same time, the DNA synthesis pioneer is hitting some turbulence. The synthetic genes segment is struggling as synthetic biology customers navigate their own financial woes and academic customers contend with reduced federal grants. The timing isn't great. While the NGS segment continues to forge ahead with tailwinds from liquid biopsies and molecular residual disease (MRD) diagnostics, DNA synthesis is also a race to the bottom. There's never-ending competition from established peers like IDT, a ferocious lineup of Chinese players, and steady pressure from startups with new ideas.

Despite the uncertainty, it's important to remember that Twist Bioscience has among the strongest commercial infrastructure and customer relationships in the landscape. That can carry the business pretty far, although commodity products like synthetic DNA are always at risk of disappointing investors.

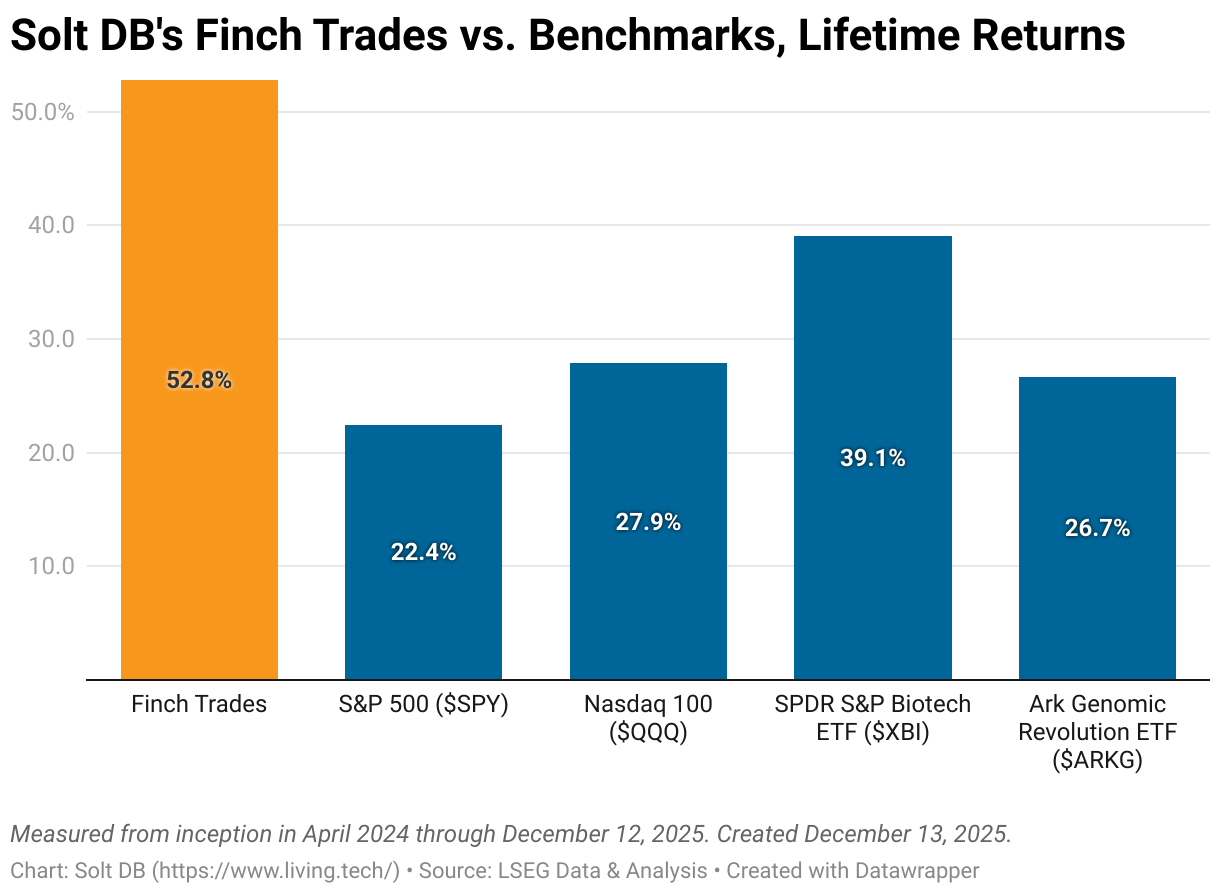

Finch Trades Review

As of market close on December 15, 2025, Finch Trades is outperforming all four benchmarks I measure against.

A rising tide lifts all boats. The recent market melt up, especially in small caps and biotech specifically, has boosted all Finch Trades positions. It's lifted many questionable and speculative stocks, too. Are we smart or lucky?

On the one hand, the recent market surge has favored quality businesses and drug developers with high-impact assets and/or strong commercial footprints.

At least some of that is a premium doled out by Mr. Market because these companies have better acquisition potential. At least some of that is because, somewhat counterintuitively, these quality companies have the most to gain from interest rate cuts. Sure, all the craptastic companies on the brink could grab a lifeline, but companies on the cusp of success could significantly de-risk themselves with just a little more capital.

With a little more money Relay Therapeutics could fully fund zovegalisib in the first triplets in breast cancer (pivotal studies) and the phase 2 ReInspire study in vascular malformations. Arrowhead Pharma could build commercial infrastructure faster to support the potential launch of Redemplo (plozasiran) in much larger markets. Less risk means higher premiums.

On the other hand, I think the recent market melt up is unsustainable. The perceived reduction in risk from interest rate cuts plus the surge in M&A activity have let investors dial up the speculative bets they're comfortable placing. Yes, many drug developers across the land have been and continue to be undervalued. I think some of the quality companies will hold onto at least some of their recent valuation gains.

Importantly, I think Finch Trades is well positioned to weather a market correction. I've taken intelligent risks and avoided making emotional decisions when managing positions.

- Locked In: After exiting Arrowhead Pharma (a position I'm eager to rebuild bigger in the future) I've locked in $8,900 in profits on $53,150 in principal – a nearly 17% gain. That provides a cushion should active positions in Relay, Coherus, and Harmony cough up some gains.

- Harmony: I expect to exit Harmony in Q1 2026 – hopefully locking in additional gains. The position is currently up $6,900 or nearly 30%.

- Coherus: I expect Coherus to rise closer to my modeled fair value through the end of 2026 and think it's likely to be acquired by 1H 2027. The position is currently down $1,800 or nearly 19%, which means it could offset potential reversals in Relay or Harmony.

- Relay: Finally, I'm not concerned with the share price of Relay for the next couple of years. If I can aggressively add to the position for $15 per share or less, then I consider that a best-case scenario. I wouldn't be surprised to see it crater in a large market downturn, which would reverse the position's current gain of $15,000 or roughly 75%.

.svg)

.svg)

.svg)

.png)

.svg)

.svg)

.svg)