.svg)

Coherus BioSciences first referred to both Cimerli (ophthalmology) and Yusimry (autoimmune) as "non-core assets" at the JP Morgan Health Care Conference in January 2024. Less than half a year later, both are gone.

What should investors make of the $40 million transaction value? It depends on how you look at it.

Biosimilars can be developed for about 10% of the R&D investment of a novel asset. In this case, Coherus BioSciences spent $294.7 million on R&D expenses directly related to Yusimry in the decade spanning 2014 to 2023, according to SEC filings. That included everything from conducting comparison clinical trials to securing relatively large domestic manufacturing capacity. The asset generated about $11 million in revenue for the company since launching last summer, which roughly offset operating expenses in that span.

On the one hand, quick math shows the company ate about $255.85 million in net expenses related to Yusimry spread over a decade. It's easy for investors to see the dwindling cash position at present, add the number above, and be disappointed. The business wouldn't have had an additional $250 million in cash right now if it never pursued the asset, but it probably would've had more cash.

On the other hand, those expenses were incurred over 10 years and represent a fraction of the expected market opportunity. Management once estimated Yusimry could generate $500 million in peak annual revenue at just a 10% market share. That would've driven a remarkable return on investment. It's also worth inserting that most times a drug developer terminates a program or asset there's nothing left to show for it.

On the third hand (?), the only thing that matters in 2024 is commercial execution. If Coherus convinces the market it's on a promising trajectory that will see it return to cash flow breakeven and profitable operations, then that's the only outcome investors care about. If the company fails to get on sustainable and stable footing, then the stock will remain in the basement. Or Cold War-era nuclear bunker, the depth keeps changing.

The $38.85 million in net cash provided by divesting Yusimry provides a meaningful level of breathing room.

It All Comes Down to Commercial Execution

There are no more excuses for Coherus in 2024.

The pandemic doesn't matter. The about-face of the U.S. Food and Drug Administration (FDA) on Chinese assets doesn't matter. Licensing a TIGIT asset for $35 million only to terminate development shortly thereafter doesn't matter. The messy American healthcare system holding back adalimumab biosimilars doesn't matter.

The drug developer has launched two important high-margin assets, Loqtorzi and Udenyca Onbody. It has shed two non-core assets to refocus on oncology. It has cleaned up its balance sheet, reducing term debt by nearly 85%. Management should have comparatively much more bandwidth to dedicate to many fewer activities now. Shareholders want to see that dedicated to the team's demonstrated core strength: commercial execution.

Let's consider scenarios.

First, it helps to lay out the assumptions:

- Coherus meets full-year 2024 R&D and selling, general, and administrative (SG&A) expense guidance of $250 million to $265 million. This includes approximately $40 million in non-cash stock-based compensation for employees.

- Coherus ended March 2024 with a pro forma cash balance of about $84.8 million, which accounts for the term debt repayment in early April.

- The Udenyca franchise has a gross margin of approximately 75%, while Loqtorzi has a gross margin that gradually increases from 35% in Q2 to 50% in Q4.

- Coherus paid a $12.5 million milestone to Junshi Biosciences in Q2.

Returning to cash flow breakeven and profitable operations has two components: increasing gross profits and decreasing operating expenses.

Let's start from the bottom and work our way up.

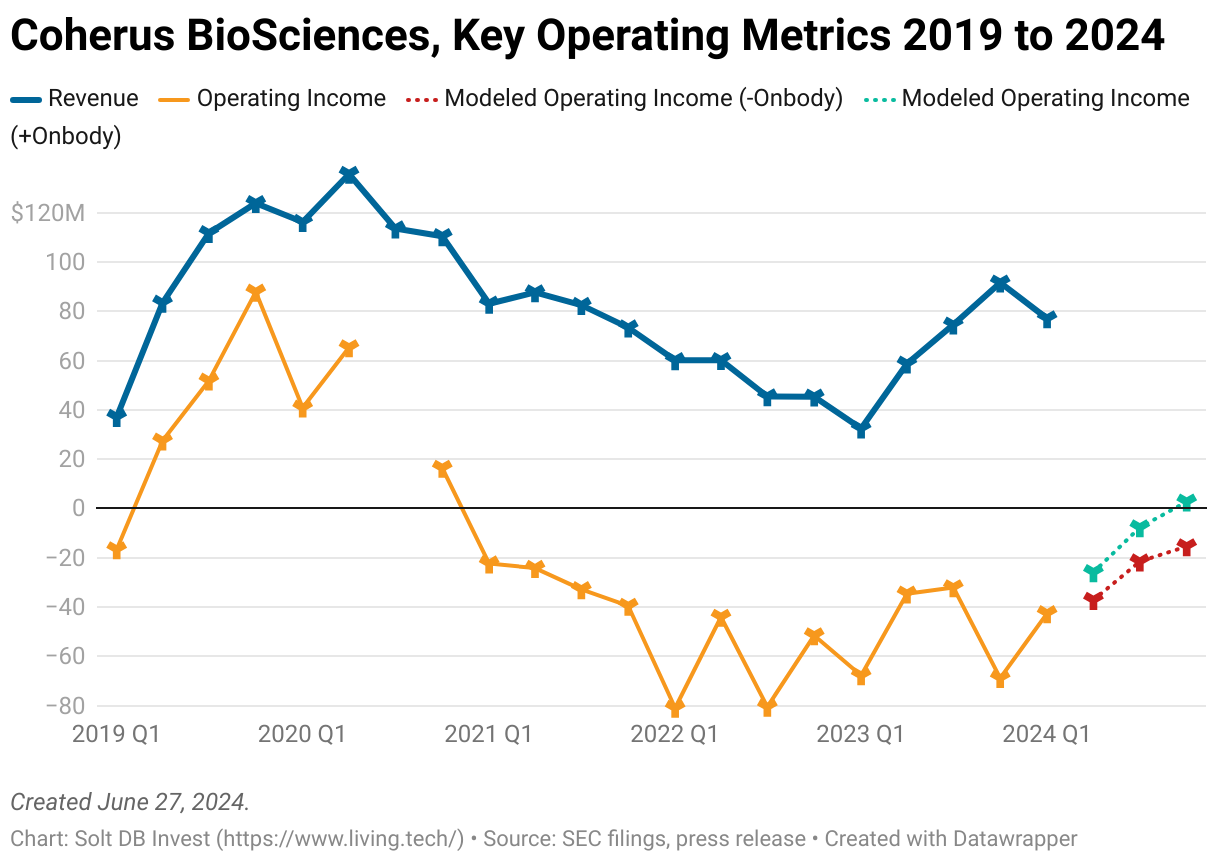

After recording first-quarter 2024 operating expenses of $85 million, the business should average just $64 million in the next three quarters. That falls to $53 million when non-cash expenses are excluded.

That means the company will need roughly $159 million in cash – on the balance sheet and generated from products – to make it to the end of the year. Coherus had $84.8 million in cash at the end of March 2024. It'll net $38.9 million from the Yusimry divestment. That brings the total cash position to $123.7 million before accounting for gross profit generated from products.

That means Loqtorzi and the Udenyca franchise only need to generate $35.3 million in total gross profit over the final nine months of 2024 for the business to fund itself. For reference, the company should generate at least that level of gross profit each quarter.

In other words, the business should now be able to survive 2024. But who the fuck is invested just for survival?

In my current model that excludes contributions from Udenyca Onbody, the business generates an operating loss of $74 million in the final three quarters of 2024. That includes a fourth-quarter operating loss of $15 million and operating cash outflow of roughly $5 million.

If my model includes Udenyca Onbody, then Coherus generates an operating loss of $30.8 million in the final three quarters of 2024, including a fourth-quarter operating profit. It would achieve positive operating cash flow in the third quarter.

My model that includes Udenyca Onbody assumes a relatively quick ramp for the asset. The product ends Q2 with 10% to 20% market share, then rises to 25% in Q3 and 33% in Q4. This is driven by existing insurance coverage, brand awareness, device innovation, and complete lack of competition aside from Neulasta Onpro.

Although that might sound ambitious, this trajectory roughly matches that of Cimerli, which ended its first full year on the market with a market share of 28.6% and needed more time to establish insurance coverage.

This model will be introduced in August 2024 in the absence of a legal challenge from Amgen.

Margin of Safety & Allocation

Coherus BioSciences is considered a Growth (Quality) position. The current modeled fair valuation for the company based on my 2024 model is below:

- Market close June 27: $1.70 per share

- Modeled Fair Valuation: $10.02 per share

- Allocation Range: Up to 15%

Coherus BioSciences reported 114.726 million shares outstanding as of April 30, 2024. The modeled fair valuation above assumes 120.462 million shares outstanding by the end of 2024, which is equivalent to 5% dilution.

Further Reading

- June 2024 press release announcing Yusimry's divestment

- June 2024 regulatory filing (8-K) detailing the transaction. There are links to the asset purchase agreement and pro forma financial information at the bottom.

- May 2024 research note analyzing Q1 2024 operating results

.svg)

.svg)

.svg)

.svg)

.png)

.svg)

.png)

.svg)

.svg)

.svg)