.svg)

Deciphering the financial statements of Coherus BioSciences in the last two years has been like looking into a snow globe. I never was a big fan of winter.

The asset sales of Cimerli, then Yusimry, and recently Udenyca have made it trickier to get a glimpse into the health and growth trajectory of the business. Analysts and investors have had to meticulously remove assets, liabilities, revenue, and expenses related to these now-discontinued products and their divestment transactions.

The bad news is that seems to have sunk the stock in the immediate aftermath of the first-quarter 2025 earnings report. Wall Street expected revenue of $62 million during the quarter, primarily related to the last gasp from the Udenyca franchise. That seemed reasonable considering the trio of pegfilgrastim presentations generated $66.1 million in revenue in Q3 2024, but the franchise coughed up just $31.5 million – lower than the supply-disrupted fourth quarter. The whiff was due to a combination of net revenue transactions and management taking a mulligan in the quarter to reset and refocus the remaining sales team on Loqtorzi with new territories, new accounts, and new relationships.

Nor did it help that Coherus burned $43.6 million in cash in the first quarter to exit March 2025 with just $82.4 million.

The good news is you already forgot you were looking into a snow globe. It's only been four paragraphs, man.

The business reported operating cash outflow of $25.8 million in Q1 2025, which was better than expected. The other $17.8 million in cash burn was attributed to one-time financing activities, including the final $12.5 million milestone to Junshi Biosciences that was delayed for 18 months and a $4.7 million payment related to prior asset sales.

Most important, early in the second quarter Coherus received $483.4 million in cash from selling Udenyca. Subtract another quarter of operating cash burn and the payments to cancel its debts – $47.7 million to remove the royalty on Udenyca sales and $230 million to repurchase convertible notes – and the business should end June 2025 with roughly $250 million in cash. That's about $30 million better than expected. It could be $15 million lower or higher depending on financial transactions related to the transaction.

You could also just take the simpler view: Coherus has enough cash to fund itself through all data readouts in 2026. Whether Loqtorzi ramps faster or slower is a secondary concern. The company's future – and maybe its survival – rests on casdozo and CHS-114.

By the Numbers

The first-quarter 2025 operating metrics provide an early glimpse of the expected steady state performance of the business for the next 12 to 18 months. Expenses will be relatively fixed, while Loqtorzi will slowly contribute more gross profit to reduce cash burn.

Management expects to spend roughly $25 million per quarter on each R&D expenses and selling, general, and administrative (SG&A) expenses for the rest of the year. I might expect slightly higher R&D expenses to support ramping clinical programs, but CFO Bryan McMichael provided SG&A guidance of $90 million to $100 million for the year.

For all the snow globe metrics thrown at investors in recent years, one trend has been reliable: Coherus has so far always underpromised and overdelivered when SG&A guidance was given. Investors might expect the business to reduce this line item to $20 million per quarter in the second half of the year (an annual run rate of $80 million).

Loqtorzi is likely to slightly outperform my model's expected 65% gross margin for the year, but the difference won't be meaningful at expected revenue levels. Longer term, the asset has peak gross margin potential in the low 70%s (this will be achieved well before it reaches peak revenue in 2027) including the 20% royalty paid to Junshi Biosciences. The PD-1 inhibitor will not nudge the business to positive cash flow even once it reaches its peak revenue potential in nasopharyngeal carcinoma (NPC), but it can gradually fund a higher share of operating expenses in the next 18 months.

Loqtorzi did have a weaker-than-expected start to the year. My model expected first-quarter 2025 revenue of $11.022 million, whereas the asset delivered $7.348 million. But my model was too optimistic and failed to account for the seasonality of drug development.

Product sales are usually lower to slightly better in Q1 than the most recent Q4 period. That's due to how drug products in many therapeutic areas are purchased, inventoried, and distributed in the United States. Wholesalers restock inventory at the end of each calendar year primarily to beat price increases that go into effect on January 1.

This isn't unique to Loqtorzi or a signal the ramp is off track. Simply consider every commercial-stage drug developer in the coverage ecosystem.

- Day One Bio reported Ojemda (oncology) revenue of $30.5 million in Q4 2024 and $29.0 million in Q1 2025.

- SpringWorks Therapeutics reported Ogsiveo (rare disease) revenue of $61.5 million in Q4 2024 and $44.1 million in Q1 2025.

- Krystal Biotech reported Vyjuvek (rare disease) revenue of $91.1 million in the final period of last year and $88.2 million to kick off 2025.

- Blueprint Medicines reported Ayvakit (rare disease) revenue of $144.1 million in Q4 2024 and $149.4 million in Q1 2025.

- Harmony Biosciences reported Wakix (neuro) revenue of $201 million in the final frame of 2024 and $185 million to start the new year.

What's more important is the overall trajectory and the clinching of specific milestones. Loqtorzi will pay for itself once it reaches $15 million in quarterly revenue, which is expected in Q4 2025 or the first half of 2026. Every dollar of sales after that begins to contribute to overall operating expenses.

My model expects peak annual sales in NPC of $150 million per year or $37.5 million per quarter. Management thinks the opportunity could be as high as $200 million per year or $50 million per quarter. In either case, peak revenue is expected to be achieved in 2027 – I model it as an exit rate, meaning Q4 2027 revenue of roughly $37.5 million.

It's important to keep in mind: Loqtorzi has an unusually high duration of treatment in NPC, meaning patients remain on treatment for 24 to 36 months.

A patient who began treatment in Q1 2024 could still be generating revenue in Q1 2027. This positively impacts the revenue ramp. Although it's challenging to discover patients for the rare cancer, most revenue comes from long-term patients, not new patient starts. The business still needs to grow the base, but it's very early. It appears to be on track so far.

Around the Horn

The fate of Coherus BioSciences previously rested on commercial execution for the Udenyca franchise. After the divestiture to clean up the balance sheet, the company's ability to earn a durably higher valuation (or get acquired) rests primarily on data readouts from the pipeline.

That's not to say commercial execution for Loqtorzi is unimportant, but a peak sales opportunity of just $150 million per year in NPC isn't enough to singlehandedly salvage respect from investors or analysts. Data readouts hold the key to significantly increasing the peak sales opportunity by expanding beyond the rare cancer.

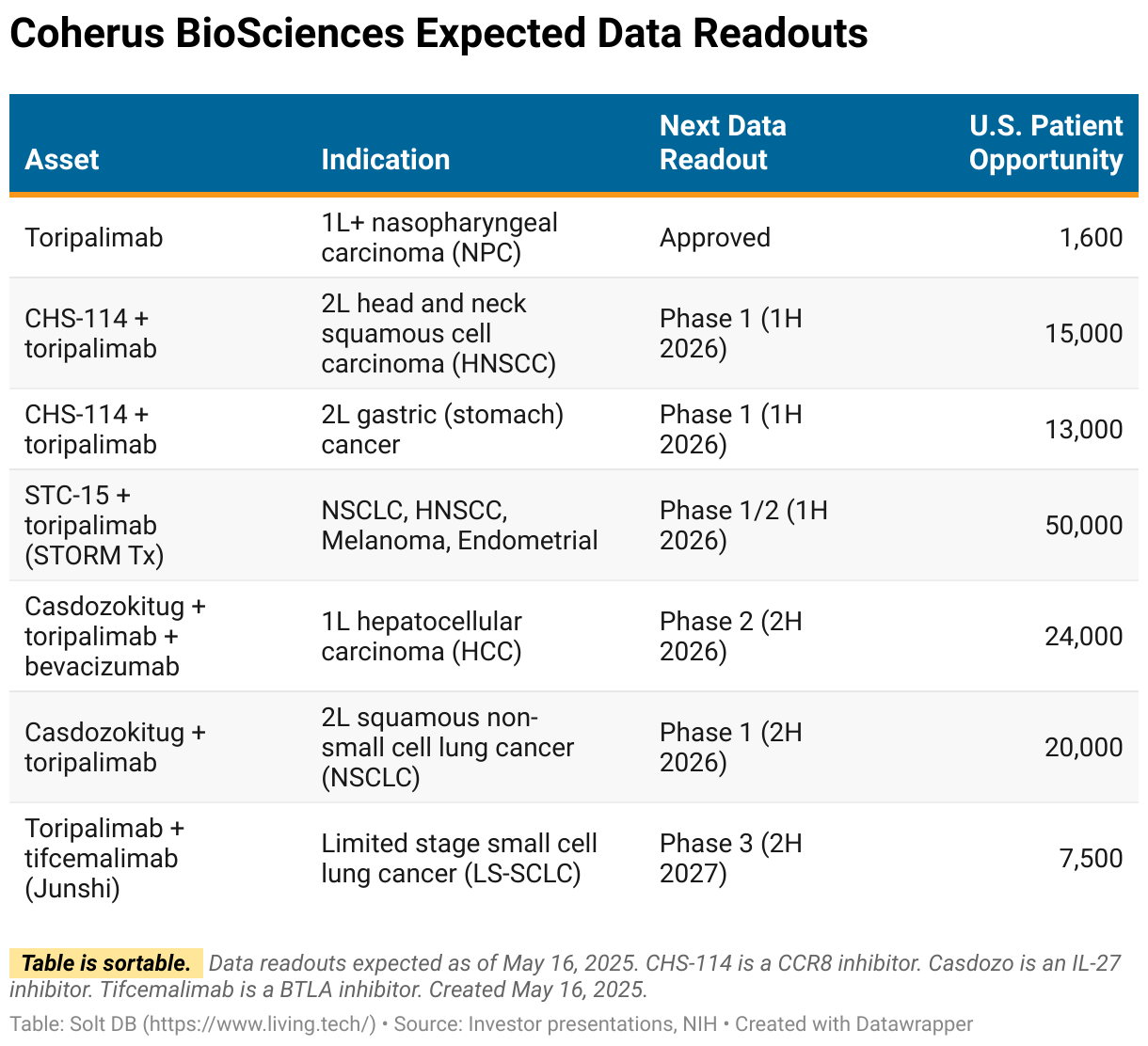

Let's walk through each expansion indication's current development status, expected data readout, and separate signal from noise. I've updated the table below with more realistic patient populations than communicated by Coherus.

Loqtorzi (toripalimab, PD-1 inhibitor)

In November 2024, the National Comprehensive Cancer Network (NCCN) updated guidelines to give Loqtorzi preferred status across NPC treatment lines. This means doctors can no longer prescribe off-label PD-1 inhibitors that do not have formal FDA approval in NPC. That could incrementally accelerate the ramp trajectory, as Loqtorzi will no longer compete with off-label treatments for new patients.

In April 2025, the FDA approved Akeso Bio's penpulimab in two NPC treatment settings. Regulators afforded the same regulatory flexibility pathway granted to Junshi Biosciences and Coherus, meaning it allowed data solely from Chinese clinical trials to support approval. In theory, every Chinese drug developer could do the same.

Although we refer to NPC as a rare cancer, that's only in the context of the United States. There are an estimated 140,000 new cases each year on a global basis, but only 1,600 diagnoses among Americans. That's because NPC predominantly impacts individuals of Asian descent. This is also why PD-1 assets that originated in the West – Keytruda, Opdivo, Tecentriq, Imfinzi, Libtayo, Jemperli, and so on – skipped over NPC development programs entirely.

Instead of getting into the weeds of this or that specific label, there's no evidence Akeso plans to launch or commercialize its asset in the United States. Case in point: approval announcements usually drop the generic name ("penpulimab") and replace it with the brand name for the first time. There is no U.S. brand name for penpulimab.

Even simpler, Akeso doesn't have a commercial footprint in the United States. It could license penpulimab, but its peak annual sales opportunity is about $135 million – and it would have to compete with Loqtorzi. That's a tough sell, especially given the headache of importing finished drug product from China in the current geopolitical environment.

My interpretation is Akeso used this approval to signal its global drug development chops. That's not quite true considering these studies never enrolled an American or European patient, but it boosts optics for the rest of its assets. Ever heard of Summit Therapeutics? The bispecific antibody (ivonescimab) it licensed originated from Akeso.

Finally, a phase 3 data readout from Loqtorzi and Lenvima in first-line, metastatic, hepatocellular carcinoma (HCC) is expected in mid-2025. It is not expected to support an approval.

Casdozokitug (IL-27 inhibitor)

- Modeled valuation contribution: $184 million

It's possible Wall Street is failing to appropriately value casdozo. Then again, I used to do the same. I was previously skeptical that an IL-27 inhibitor would have consistent results, as interleukins play dual roles in biology. There's evidence IL-27 inhibition both helps and hurts tumors. The statistical fog thickens when you consider casdozo is the only IL-27 inhibitor in the clinic globally.

But we're getting some objectively strong signals.

Final results are available from the prior phase 2 study in liver cancer designed by Surface Oncology.

- The development hypothesis was that adding casdozo to the standard of care (SOC) in first-line, metastatic, hepatocellular carcinoma (HCC) would improve outcomes.

- The SOC in 1L HCC is a combination of a PD-1 inhibitor and a VEGF inhibitor. Specifically, Tecentriq (atezolizumab) and Avastin (bevacizumab).

- To get their piece of the pie, many other drug developers with approved PD-1 inhibitors have studied their assets with VEGF inhibitors (usually Avastin or Lenvima) or other combinations (like the CTLA4 inhibitor Imjudo).

- Coherus is trying to improve the SOC, not match it.

In the prior phase 2 study, Surface Oncology simply added casdozo to the SOC resulting in patients receiving Tecentriq, Avastin, and casdozo.

Investors are always cautioned about making cross-study comparisons, especially when comparing mid-stage to late-stage studies. Nonetheless, it appears adding casdozo to the SOC could potentially improve outcomes in HCC based on Roche's phase 3 program called IMbrave150. The triple combination also appears ahead of other recent phase 3 studies, such as AstraZeneca's HIMALAYA program combining PD-1 with CTLA4.

Coherus is now conducting a new phase 2 study. This time, it's swapping in toripalimab as the PD-1 inhibitor, resulting in patients receiving Loqtorzi, Avastin, and casdozo. The results should be similar, especially since toripalimab has been evaluated in phase 3 studies in HCC in the past. Although I've increased the valuation contribution from casdozo in the current model, replicating prior results in the data readout due next year would make it a phase 3 ready asset, significantly increasing the value.

Separately, Coherus is evaluating a combination of toripalimab and casdozo in squamous non-small cell lung cancer (NSCLC). An earlier basket study suggested casdozo monotherapy could drive objective responses in this indication.

CHS-114 (CCR8 inhibitor)

- Modeled valuation contribution: $32 million

Coherus was developing its own CCR8 inhibitor before it acquired Surface Oncology. It decided to shave 18 months off the development timeline and save $25 million in R&D expenses by swapping in Surface's asset instead. Preliminary data suggest the acquired asset could be more selective than others being evaluated across the global pipeline from Bristol Myers Squibb, Roche, Amgen, and LaNova Medicines.

Given the proliferation of PD-1 assets, drug developers have been eager to identify blockbuster immuno-oncology combinations. CCR8 is one of the most promising targets due to its well-documented role in amplifying the benefits of PD-1 inhibitors.

Investors can expect a steady cadence of phase 1 and phase 2 data readouts from across the competitive landscape. Some could lift Coherus as investors scour pipelines for underappreciated CCR8 assets. The good ol' sympathy play.

Although that's possible and maybe likely given the company's lowly valuation, the most durable contributions to the market valuation will come from internal data readouts. Coherus' development strategy begins with head and neck squamous cell carcinoma (HNSCC) and gastric cancer ("stomach cancer"). That's smart for three reasons: toripalimab's global positioning in head and neck cancers, tumors most-reliant on CCR8, and the evidence to date.

First, toripalimab is the best-performing PD-1 inhibitor globally in head and neck cancers. NPC is often grouped there.

Second, some tumors are more reliant on CCR8 positive Tregs than others. The trio of HNSCC, cervical cancer, and gastric cancer top the list. Luckily, the prevalence of cervical cancer is falling precipitously thanks to rising HPV vaccination rates. Finland and Scotland recently made history by reporting no new cases among women who were vaccinated at 12 or 13 years old.

Many other tumor types – NSCLC, colon cancer, endometrial cancers, breast cancers, and more – are also worth evaluating with CCR8 inhibitor combinations, but the trio above are in their own tier. As is always the case in drug development, some indications will perform better than others.

Finally, the most robust clinical data for CCR8 inhibitors available today comes from a study in gastric cancer. LaNova Medicines evaluated its CCR8 asset LM-108 with the PD-1 inhibitor toripalimab (small world). It reported a preliminary objective response rate (ORR) of 36.1% across all treatment lines, 63.6% in second-line settings, and an incredible 87.5% in second-line settings with confirmed high CCR8 expression in the tumor microenvironment.

STC-15 (METTL3 inhibitor)

- Modeled valuation contribution: N/A

On May 16, STORM Therapeutics listed a new phase 1/2 clinical trial in a public government database that includes toripalimab. The rising U.K. drug developer seeks to combine Coherus' PD-1 asset with its own METTL3 inhibitor across various tumor types.

STC-15 is a small molecule that inhibits METTL3, an RNA modifying enzyme (RME). Tumor cells grow and spread through a combination of genetic sequence alterations (mutations, fusions, amplifications) and chemical modifications (methylation). METTL3 makes chemical modifications to microRNAs, which helps them grow faster and escape immune surveillance.

STORM Therapeutics has already completed a phase 1 study of STC-15 to evaluate initial safety and dose ranges. The new phase 1/2 study seeks to evaluate various doses in combination with toripalimab in 188 patients across NSCLC, melanoma, endometrial cancers, and HNSCC. The initial data readout is expected in early 2026 – adding to the data barrage for Coherus. Pending results, pivotal studies could begin in late 2026 or early 2027.

The role of METTL3 is relatively tumor agnostic, meaning many different types of cancers rely on its ability to modify microRNAs to copy themselves. If it proves to be a valuable target in immuno-oncology, then it has very broad potential across large patient populations -- and toripalimab gets to go along for the ride. That's pretty metal.

Modeling Insights

(Refined.)

The current model has been refined to adjust the expected ramp of Loqtorzi and more accurate contributions from pipeline assets.

- Full-year 2025 Loqtorzi revenue is now expected to be $45.462 million, compared to $65.088 million previously. The previous ramp is still possible, but new drug ramps are difficult to predict, doubly so for a low-volume product like Loqtorzi. I've decided to swap in a more conservative ramp in the model.

- The pipeline now contributes $206 million to the modeled valuation, compared to $52 million previously (last updated January 22, 2024).

- Following the phase 2 data readout in 1L HCC in early 2025, casdozo now contributes $184 million to the valuation, compared to $38 million previously.

- Following LaNova Medicine's ASCO 2024 data readout for LM-108, CHS-114 now contributes $32 million to the valuation, compared to $14 million previously.

Margin of Safety & Allocation

Coherus BioSciences is considered a Growth (Speculative) position. The estimated fair valuation based on my current model is below:

- Market close May 16: $0.76 per share

- Modeled Fair Valuation: $3.12 per share (vs. $2.78 previously)

- Allocation Range: Up to 10%

Coherus BioSciences reported 115.933 million shares outstanding as of April 30, 2025. The modeled fair valuation above assumes 121.730 million shares outstanding, which is equivalent to 5% dilution.

The fully-diluted basis for Coherus BioSciences (the share count used to determine the share price for an acquisition) is 147.291 million shares.

Further Reading

- May 2025 press release announcing Q1 2024 operating results

- Month 2025 regulatory filing (10-Q) detailing Q1 2024 operating results

- April 2025 research note (Member Digest) previewing earnings from across the coverage ecosystem

- March 2025 research note analyzing the outlook for 2025 and beyond

.svg)

.svg)

.svg)

.svg)

.png)

.svg)

.png)

.svg)

.svg)

.svg)