.svg)

If establishing a long-term growth trajectory is a marathon, then shoring up a balance sheet is a sprint. At least it is for Coherus BioSciences right now.

The drug developer is returning to growth – just like management said it would. National cancer centers are enthusiastically adding Loqtorzi to their formularies – just like management said they would. And the launch of Udenyca Onbody is revitalizing the competitive position of the entire Udenyca franchise – just like management said it would.

What management hasn't said much about is how it intends to bridge the gap between the current cash-burning operations and cash flow positive operations on the horizon. It's only a few quarters away. The milestone will be achieved by the first half of 2025 at the latest.

But the business had a pro forma cash balance of about $84.7 million at the start of April ("pro forma" means adjusted to account for the $175 million payment against the term loan). Depending on the near-term growth trajectories of Udenyca Onbody and Loqtorzi, that relatively low cash balance could be enough. Companies almost never cut it so close, however. It's usually a dumb thing to do – and the company's valuation certainly won't be reset higher until Wall Street is more confident in the cash position.

Which of the limited options will management choose?

By the Numbers

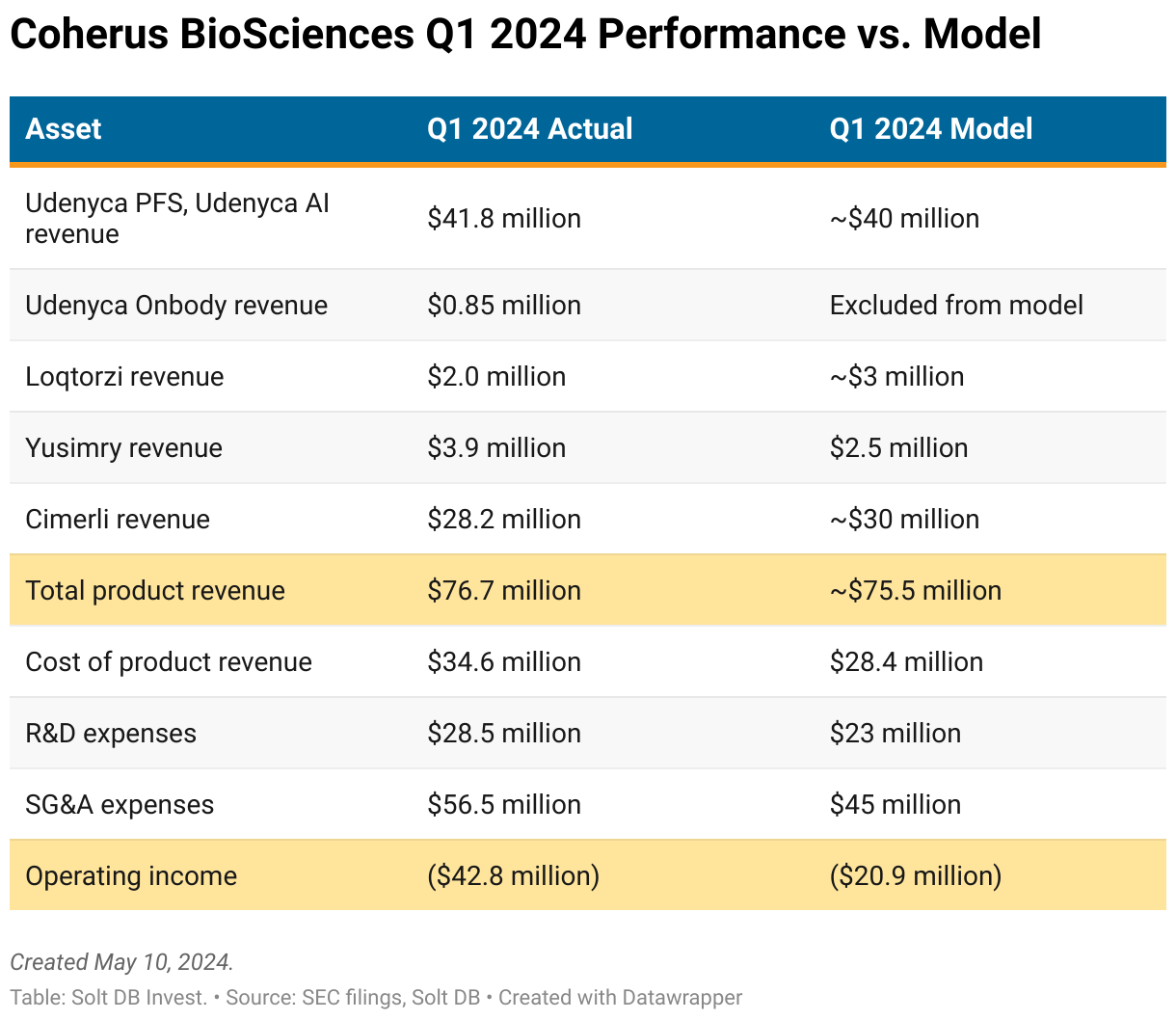

In 2023, my models for Coherus were getting wrecked by poor assumptions for Yusimry and the broader adalimumab market for biosimilars. I cleaned that up in time for the current 2024 model, which the business tracked very closely in the first quarter.

Working down the income statement, Coherus recorded much higher cost of product sold (and therefore had lower gross margin) and operating expenses than I had modeled. The entire difference in R&D expenses ($5.4 million) can be explained by process development and qualification costs for Loqtorzi, which the company is still establishing in the United States following tech transfer. That also helps to explain the higher cost of product sold, as Loqtorzi isn't at steady-state gross margin yet.

The entire difference in SG&A expenses can be explained by two items. First, Coherus wrote off $6.8 million in value for NZV930, an asset Surface Oncology licensed to Novartis prior to its acquisition. Novartis terminated development. It wasn't an important value driver, as almost all downstream value would go to former Surface Oncology shareholders. This was also a non-cash charge.

Second, the business recorded a $5.6 million increase in professional services compared to the year-ago period. There are many moving parts to Coherus, so these were likely related to layoffs, the Cimerli transaction, and product launches. It does seem unusually high, however. I don't think the business has great acquisition potential, but recent changes at Takeda (one of the few potential suitors) means a girl can dream.

It's important to point out management reiterated full-year 2024 expense guidance. What does that mean?

- Coherus had higher-than-expected Q1 2024 expenses for both R&D and SG&A. These amounted to 33% of the company's full-year 2024 expense guidance.

- A quarter is 25% of the year. That means expenses in the next three quarters will be lower than expected, which should lead to improvements in operating loss and cash flow, too.

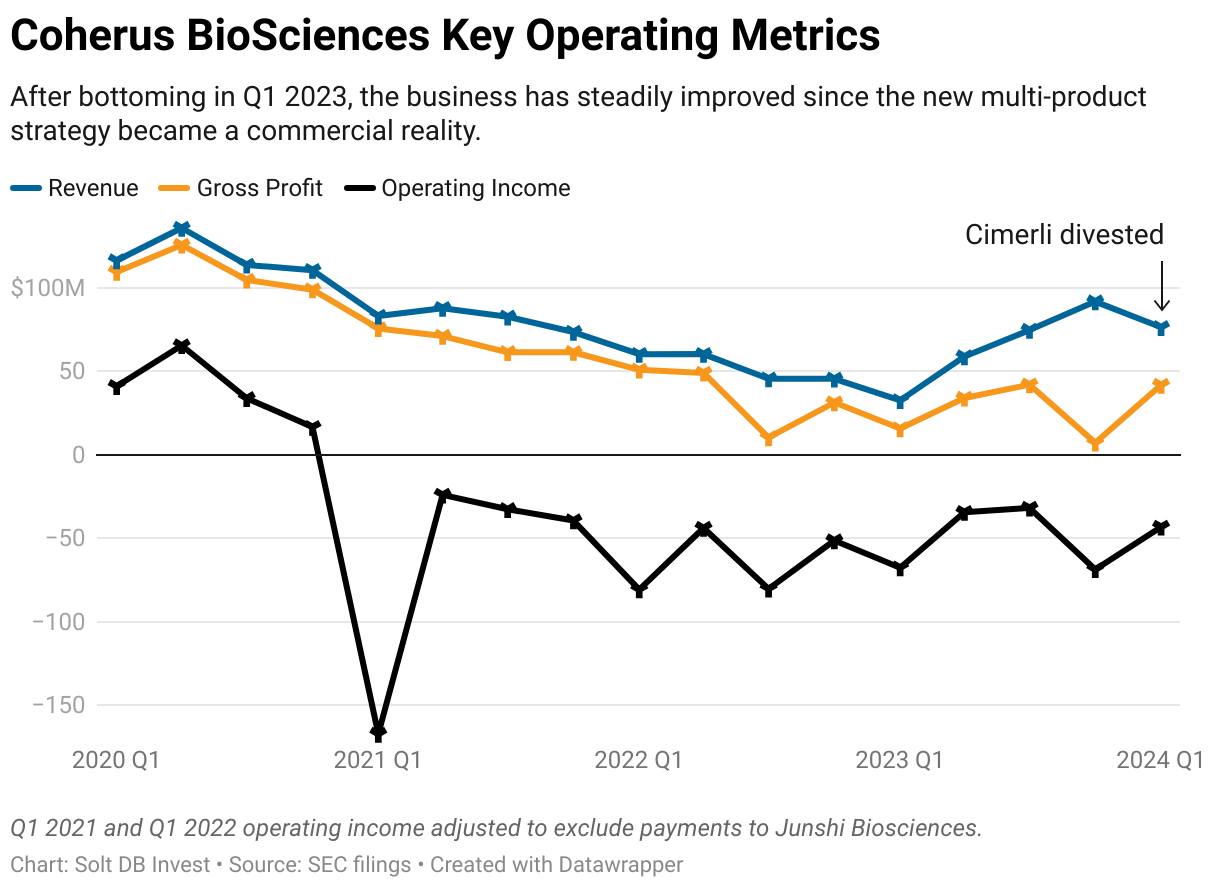

I normally lead off these sections with year-over-year comparison tables, but the performance in this case is deceptively favorable.

It's more important to zoom out and view the long-term performance. Coherus has been building toward the current multi-product strategy for a few years now. The moment has arrived, and the business is objectively improving. Unfortunately, it's impossible to exclude Cimerli's full impact across revenue, gross profit, and operating expenses. That will muddy up this chart as Cimerli contributed its last dollar in February 2024, but the business should begin a more stable growth trajectory beginning in Q2. That will make the improving trends clearer as the year progresses.

As for the most important outstanding question, how will Coherus bridge the gap between now and cash flow positive operations?

There aren't too many options. It doesn't seem that a public offering of common stock would be very favorable or advantageous. In fact, management highlighted the non-dilutive aspect of the recent transactions that paid off the former term loan.

The business has roughly $230 million in 2026 convertible notes outstanding, so a debt offering seems less likely. Coherus could possibly issue a slightly higher amount of new debt, swap out the old notes with the new, and pocket the difference. For example, issuing $300 million in 202X convertible debt would net roughly $70 million in cash before fees and other charges. The tricky thing is those 2026 convertible notes have a 1.5% interest rate – very favorable for the business.

The company could keep slapping royalty agreements on existing assets, but those provide upfront cash at the expense of future cash flow and profits.

The most favorable option would be to find a partner or royalty agreement for Yusimry that has a meaningful upfront cash component. The asset has relatively little value right now, which means such a transaction would require the partner to really buy-in to the future market opportunity. It also risks significantly undervaluing the asset. Then again, if it's a non-core asset, management might be willing to make a move.

Around the Horn

A quick look around the product portfolio. I'll write a dedicated research note(s) on the pipeline after earnings season – I'm eager to jump into our BioRender tools more frequently to discuss the nerdy science.

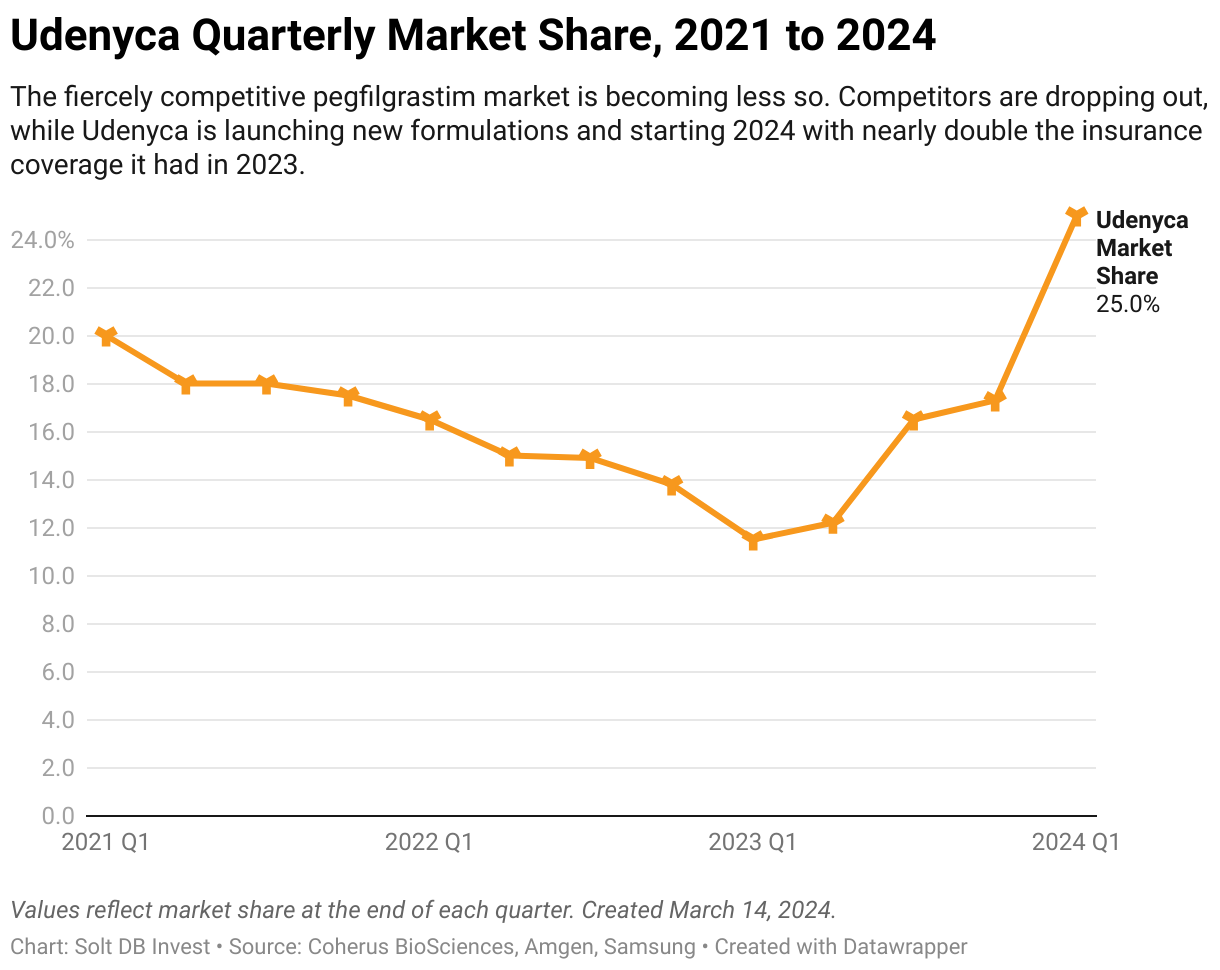

Udenyca franchise (pegfilgrastim biosimilars)

The overall Udenyca franchise had a market share of 25% averaged across the first quarter of 2024, up from 17.3% at the end of December 2023 and the all-time low of 11.5% during the first quarter of 2023. It generated revenue of $42.7 million during the period, an increase of 63% from the year-ago period. For reference, the Neulasta franchise from Amgen had revenue of just $87 million – a year-over-year decline of 59%.

Management noted Udencya PFS generated about 90% of the franchise's revenue, while Udenyca AI (8%) and Udenyca Onbody (2%) contributed less. The pre-filled syringe formulation had about $38.4 million in revenue, which was the highest since Q3 2022. That's encouraging.

The resurgence for Udenyca PFS was driven by the increasing competitiveness of the franchise. Coherus now offers a PFS presentation for in-office administration, an on-body injector presentation for at-home administration, and an autoinjector presentation for patients who want more control over treatment.

Udenyca AI is the only autoinjector formulation on the market, which helps to explain why it has only $3.4 million in quarterly revenue after its first full year on the market.

Udenyca Onbody won't have that challenge. Roughly 42% of all pegfilgrastim units sold in recent periods went to Neulasta Onpro – the only other on-body injector formulation – and hospital systems tend to prefer this presentation. It should generate most of the franchise's revenue by the first half of 2025.

Loqtorzi (anti-PD-1, not a biosimilar)

Roughly 80 individuals with nasopharyngeal carcinoma (NPC) received Loqtorzi since it launched in early January 2024. It's tempting to extrapolate that with the revenue generated to estimate market potential, but that's not quite how the math works.

Coherus is courting three separate patient populations:

- Loqtorzi plus chemotherapy is used as a first-line treatment once NPC has begun to spread in the body or returned after prior treatment

- Loqtorzi alone is used as a second-line and later treatment for advanced NPC for individuals who failed to respond or stopped responding to chemotherapy

- Individuals with NPC who are receiving another anti-PD-1 drug product off label. Loqtorzi is the only anti-PD-1 asset formally approved to treat NPC.

Individuals in the first patient population will presumably be on treatment the longest – and that can mean multiple years. Individuals in the second patient population will be on treatment for shorter durations. Meanwhile, it probably won't be possible to convert patients already receiving an anti-PD-1 treatment off label. Coherus will just need to ensure doctors use Loqtorzi for all future patients.

As usual, the company is crushing the commercial infrastructure buildout. Coherus expects Loqtorzi to have formulary position at all 33 National Comprehensive Cancer Network (NCCN) institutions by the end of June 2024 (this means the drug product will be used for all NPC patients at those facilities). Hitting that milestone just six months after launch is pretty insane.

Of course, patients are treated outside NCCN institutions, too. And NPC is a relatively rare cancer with a total patient population of between 1,200 and 2,000 individuals per year. But there's no competition, nothing in the industry pipeline, and Loqtorzi is the only treatment with preferred positioning in the NCCN guidelines. The revenue ramp will be steady and relatively linear (read: no major inflection points) every quarter for the foreseeable future.

Yusimry (adalimumab biosimilar)

Non-Core Asset ™ Yusimry is slowly ramping revenue, which aligns with management's expectations communicated in early 2023.

On the conference call, an analyst asked how management viewed the market opportunity in 2025 once regulations go into effect that will make biosimilars more competitive. Chief Commercial Officer Paul Reider gave great, detailed answers for every other question he fielded. But for this one, he stumbled through it with a response that didn't really instill much confidence in the asset's competitive positioning.

Either that or Coherus is determining how and when to divest the asset to maximize its value, which right now is pretty low.

Cimerli (ranibizumab biosimilar)

Remember how some investors were pissed about divesting Cimerli? Well, the asset was on pace to generate first-quarter 2024 revenue of roughly $42 million, compared to $52.4 million in Q4 2023 and $40 million in Q3 2023. This aligns with my analysis of the asset's waning market opportunity as competition encroached, as sales likely peaked in 2023. I had modeled full-year 2024 revenue of about $150 million, even though Q4 2023 sales worked out to $210 million at an annualized rate.

Management might have nailed the timing for the asset sale, which serves as one additional reason to remain confident and patient in the overall commercial strategy.

Forecast & Modeling

(No change.)

I've decided to continue excluding Udenyca Onbody in the 2024 model. There's still a sliver of doubt about Amgen legally challenging the product, especially with the Neulasta franchise getting absolutely trampled by competition in the first quarter. I've shared below what the model would look like if Udenyca Onbody is included.

A few minor refinements have been made, including factoring in the new 5% royalty on sales of Udenyca products and Loqtorzi. This impacts gross profit, gross margin, operating income, and operating cash flow in the model. It will have a greater impact on the 2025 model that will be based on operating income and cash flow.

For transparency, the second-quarter 2024 model assumes:

- Total product revenue of roughly $54.5 million. This includes $42.5 million from Udenyca PFS and Udenyca AI combined (vs. $41.8 million in Q1), no revenue from Udenyca Onbody, roughly $8.5 million from Loqtorzi (vs. $2.0 million in Q1), and $3.5 million from Yusimry (vs. $3.9 million in Q1).

- Gross margin of 73.5% with cost product sold of $14.45 million.

- Operating expenses of $75.5 million (vs. $85.002 million in Q1) inclusive of a one-time $12.5 million milestone payment to Junshi Biosciences.

- An operating loss of $35.45 million (vs. $43.378 million in Q1).

The current full-year 2024 model assumes Udenyca Onbody generates no revenue:

- Total product revenue of $260.390 million, compared to $256.580 million in 2023.

- Total oncology product revenue of $215.802 million, an increase of 69% from $127.618 million in 2023.

- Gross profit of $175.549 million, an increase of 21% from $145.335 million in 2023.

- Operating expenses (including a $12.5 million payment to Junshi Biosciences in Q2 2024) decrease by $31 million vs. 2023.

To be clear, my current 2024 model as of this writing excludes contributions from Udenyca Onbody. If projections for Udenyca Onbody are included, then the model would change as follows:

- Total product revenue of $323.563 million (including roughly $62 million from Udenyca Onbody), compared to $256.580 million in 2023. This represents year-over-year growth of 26%.

- Total oncology product revenue of $278.655 million, an increase of 118% from $127.618 million in 2023.

- Gross profit of $226.002 million, an increase of 55% from $145.335 million in 2023

- Operating expenses (including a $12.5 million payment to Junshi Biosciences in Q2 2024) will decrease by $31 million

In this scenario, Coherus BioSciences would generate operating income in the fourth quarter of 2024 and only burn about $50 million in cash to get there.

Margin of Safety & Allocation

Coherus BioSciences is considered a Growth (Quality) position. The current modeled fair valuation for the company based on my 2024 model is below:

- Market close May 9: $2.12 per share

- Modeled Fair Valuation: $10.39 per share

- Allocation Range: Up to 15%

Coherus BioSciences reported 114.726 million shares outstanding as of April 30, 2024. The modeled fair valuation above assumes 120.462 million shares outstanding, which is equivalent to 5% dilution.

Further Reading

- May 2024 press release announcing Q1 2024 operating results

- May 2024 regulatory filing (10-Q) detailing Q1 2024 operating results

- March 2024 research note analyzing full-year 2023 operating results

- January 2024 research note analyzing divestment of Cimerli

.svg)

.svg)

.svg)

.svg)

.png)

.svg)

.png)

.svg)

.svg)

.svg)