.svg)

I think many questions investors have right now would be addressed if I had published the Base Research / Research Deep Dives, but I'm "a little" behind. This is meant to provide more insights into our 2024 model and what's over the horizon for Coherus BioSciences.

To start, Solt DB Invest is reiterating the Asymmetric Opportunity for Coherus BioSciences. This marks the fourth time the label has been given.

- AVITA Medical at $6.31 per share on December 6, 2022

- Relay Therapeutics at $12.47 per share on April 20, 2023

- Coherus BioSciences at $4.13 per share on June 16, 2023

- Coherus BioSciences at $1.60 per share on November 9, 2023

It's unusual for a stock to decline by at least 20% for three consecutive days. It's spooky. But investing is primarily about keeping emotions in check. Let's reorient ourselves on what matters -- with the good, the bad, and the ugly.

Execution Drives Business Fundamentals

Exuberance and fear can grip a stock in the short run, but share prices are driven by execution (or a lack thereof) in meaningful periods of time. That puts Coherus BioSciences in a favorable position.

Management has delivered against all goals throughout 2023 and heading into 2024. Regulatory delays, especially when caused by external third parties or international travel restrictions, are outside of management's control. Aside from that, the company has executed on its long-term multi-product strategy, which investors have been awaiting for over two years. It's now here.

For example, here's a summary of a pitch I made in November 2021 for Coherus BioSciences. I've been patiently waiting for today for over two years.

Tori has finally earned regulatory approval, the Lucentis biosimilar Cimerli launched as expected, Udenyca OBI is expected to earn approval before the end of 2023, and the Humira biosimilar Yusimry launched as expected. Management tossed the Avastin biosimilar by trading up for a more lucrative Eylea biosimilar (both are anti-VEGF products), which is expected to earn approval in mid-2024 and launch in 2025.

Let's focus on the business fundamentals.

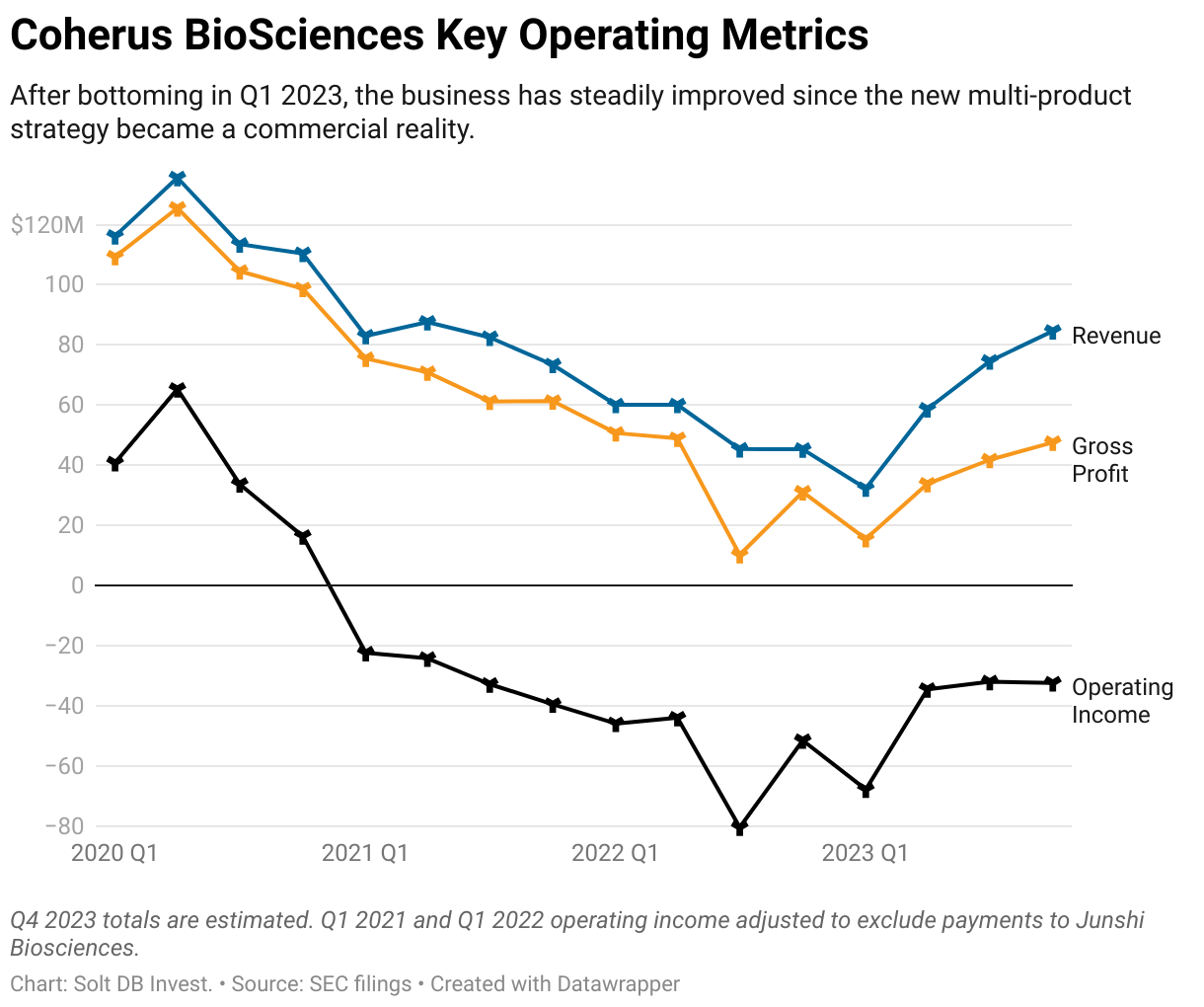

In the third quarter of 2023, Coherus BioSciences notched its highest revenue since the third quarter of 2021, highest gross profit since the second quarter of 2022, and lowest operating loss since the second quarter of 2021.

To achieve full-year 2023 guidance of at least $250 million in revenue, the business needs to generate fourth-quarter 2023 revenue of at least $84.4 million. That would be the highest since the second quarter of 2021 – continuing the steady trend of improvements since the multi-product strategy arrived with the ramp of Cimerli.

For the visual learners, here's how the trend might look after fourth-quarter 2023 operating results are announced.

Investors have been waiting for the multi-product portfolio to arrive for years. It's now reality. It's progressing as expected. Investors shouldn't lose sight of that, or the benefits that will be in hand from having a resilient revenue base driven by a half dozen products across three unrelated therapeutic areas (oncology, ophthalmology, and autoimmune).

Forecast & Modeling Insights

(No change.)

Udenyca

The third quarter of 2023 definitely raised some questions about the pegfilgrastim market.

For example, Amgen reported a 55% decline in Neulasta revenue from the year ago period. That's likely due to a combination of reduced selling prices (potentially in an attempt to squeeze competitors, or increase the pressure on the expected launch of Udenyca OBI) and fewer units sold (potentially stemming from a nationwide chemotherapy shortage). I'm unaware of pegfilgrastim alternatives, and neither Amgen nor Coherus BioSciences offered any explanation. The lack of communication or explanation from Coherus BioSciences management is either an example of poor leadership or, if there's nothing to explain aside from competitive dynamics, proof of an overreaction by markets.

But investors must resist the urge to extrapolate the slugfest of the pegfilgrastim market to all biosimilar markets.

- There are six pegfilgrastim biosimilars – more than any other market with a biosimilar, aside from adalimumab (Humira).

- Those six biosimilars aren't fighting for 100% of the market, but the 58% available for prefilled syringe (PFS) formulations. In other words, Udenyca's third-quarter 2023 market share of 16.5% isn't out of 100%, it's out of a possible 58%.

- To reiterate, there are six pegfilgrastim biosimilars fighting over slightly more than half of the total market opportunity. That amplifies competitive pressures and has led to disproportionate selling price decreases from competitors, which Coherus BioSciences has long resisted. Even after the 9% decline in average selling prices (ASP) from Q2 to Q3, Udenyca is the highest-priced pegfilgrastim on the market.

- If investors are worried about the Udenyca franchise, then imagine how poorly competitors with less market share and formulations are performing. Rapid drops in ASP can help grab market share, but aren't sustainable in the long run. There will be competitors that exit the pegfilgrastim market, which will help relieve some of the competitive dynamics just as the Udenyca franchise is ramping up again.

This is what makes expanded insurance coverage for Udenyca AI, the autoinjector formulation, so important. That will allow the Udenyca franchise to begin competing for the remaining 42% of the pegfilgrastim market that has been off limits for the last five years.

As of the third quarter of 2023, only about 9.5% (250 of 2,623) of Udenyca accounts had ordered Udenyca AI. The true demand for the product, the only autoinjector formulation on the market, is difficult to gauge. But investors won't be able to gauge market demand until full insurance coverage is in place.

Look at it this way: there will only be two products competing for that 42% market share – Neulasta Onpro and Udenyca AI. If Coherus BioSciences can launch and ramp Udenyca OBI, the on-body injector formulation, without legal challenges by Amgen, then it'll be in an even more favorable position in 2024.

There will be further declines in ASP in 2024. But the significant market share up for grabs will more than offset pricing declines. Remember, the Udenyca franchise has grown despite double-digit decreases in ASP in 2023.

- Third-quarter 2023 revenue for the franchise is equivalent to $132 million on an annualized basis. That's up from $104 million using an annualized rate for first-quarter 2023 revenue. The franchise is still growing.

- The Udenyca franchise could eventually have a market share near 40% -- double its all-time peak.

Although Udenyca revenue will grow in 2024 and 2025 as all three formulations ramp, the franchise will eventually transition from a source of growth to a source of consistent profits and cash flows. Growth will eventually be less important. That's okay. By then, other products will be driving the growth engine (Cimerli is already doing that in 2023). Udenyca served its purpose since launching in 2018 by enabling the multi-product strategy now taking hold.

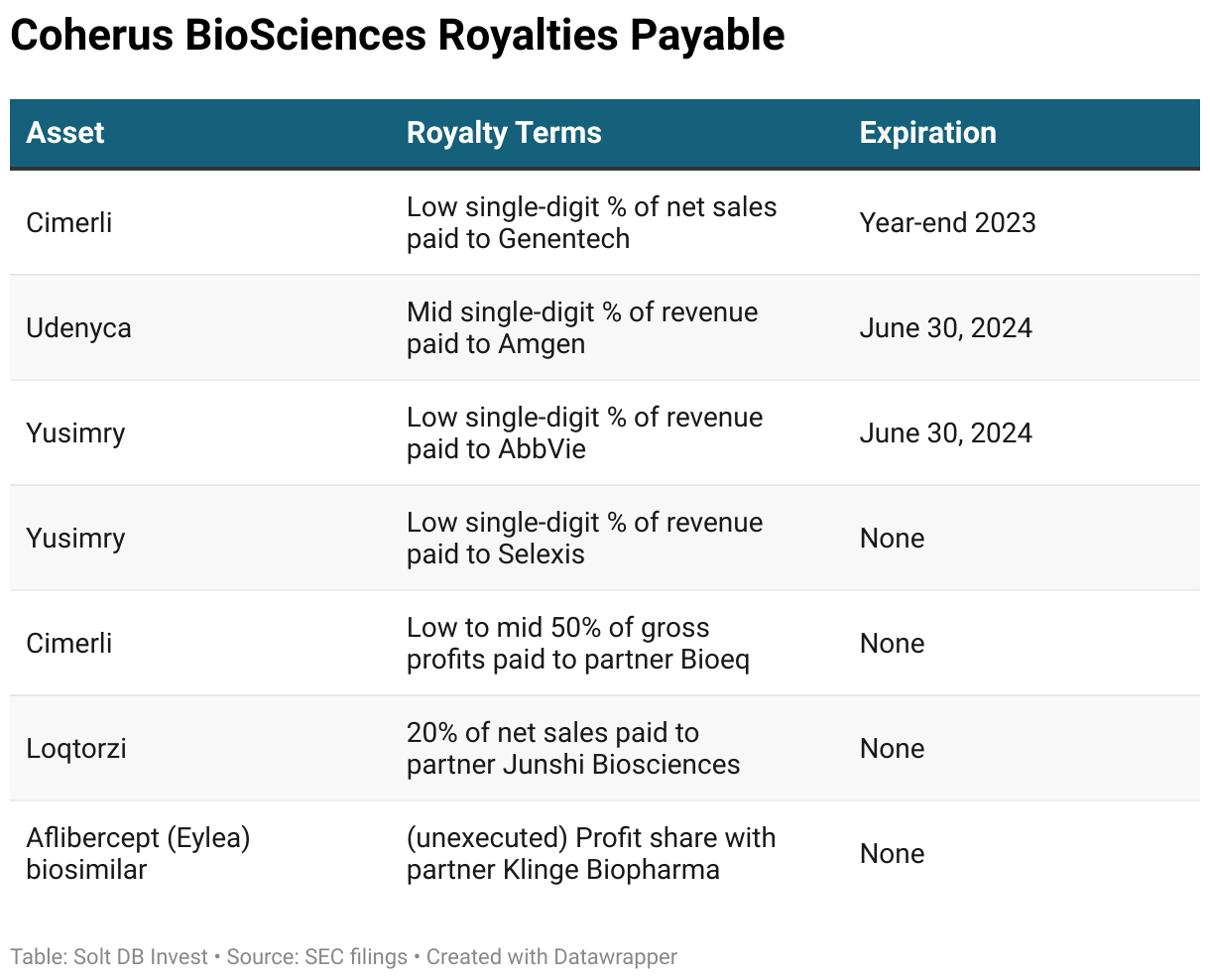

Royalty Expirations

It's also important to acknowledge the margin boost coming in 2024 as royalties begin to expire -- something everyone is overlooking.

Coherus BioSciences has been paying a mid single-digit percentage of Udenyca revenue as a royalty to Amgen for the last five years. This expires on June 30, 2024. Another low single-digit percentage of Cimerli net sales is being paid to Genentech. This expires at the end of 2023.

These two royalty expirations will lead to an at least $14 million increase in gross profit on an annualized basis based on our expected 2024 revenue totals. Another royalty paid to AbbVie for Yusimry revenue will expire in mid-2024, meaning it won't sully gross margin when the product begins the most important part of its ramp in 2025.

Cash Runway

It's important for Coherus BioSciences to achieve cash flow positive operations in 2024, which the business is on pace to achieve in the second half of 2024. That trajectory could be impacted by delays in earning insurance coverage, slower-than-expected ramps, or surges in accounts receivables (the company calls these "trade receivables").

There are three quarters between now and then. The business had $131 million in cash at the end of September 2023, which will decline significantly through the end of the first quarter of 2024. But as insurance coverage for Loqtorzi and Udenyca OBI (Solt DB Invest excludes this product from the 2024 model) kick in, cash flows should trend back to breakeven.

Additionally, Coherus BioSciences has a $100 million credit facility available, which would be subject to new terms from existing loans. Oh great, more debt! But… the point here is there's not a tangible risk of bankruptcy given the business fundamentals and portfolio ramp observable right now.

The business is positioned for a rapid improvement in cash flow. For example, Loqtorzi should have a net cash generation rate of roughly 70%. That means 70% of all revenue will become cash. Solt DB Invest expects $25 million to $45 million in full-year 2024 revenue, which would result in $24.5 million in cash generation at the midpoint. That's enough to offset one quarter of cash burn.

When Loqtorzi reaches peak annual sales potential in nasopharyngeal carcinoma (NPC) in 2026, then it'll be generating $70 million to $140 million in cash annually. For comparison, Coherus BioSciences generated full-year 2020 operating cash flow of $154 million when Udenyca reached its peak. That's aided by leveraging the same commercial infrastructure as Udenyca, which will accelerate ramp and only require minimal additional investment to expand the infrastructure, if needed. However, as a novel asset (not a biosimilar) with no competitors for the NPC niche, Loqtorzi can remain at peak annual revenue for the foreseeable future. It'll be a flat peak – a relief for investors.

Margin of Safety & Allocation

Coherus BioSciences is considered a Growth (Quality) position. The current modeled fair valuation for the company based on our 2024 model is below:

- Market close November 9: $1.60 per share

- Modeled Fair Valuation: $13.15 per share

- Allocation Range: Up to 15%

Coherus BioSciences reported 111.364 million shares outstanding as of October 31, 2023. The modeled fair valuation above assumes 116.932 million shares outstanding, which is equivalent to 5% dilution over the model period.

Further Reading

- November 2023 research note analyzing third-quarter 2023 operating results

- August 2023 research note analyzing second-quarter 2023 operating results

- June 2023 research note describing the low PD-L1 strategy for Loqtorzi in immuno-oncology

.svg)

.svg)

.svg)

.svg)

.png)

.svg)

.png)

.svg)

.svg)

.svg)