.svg)

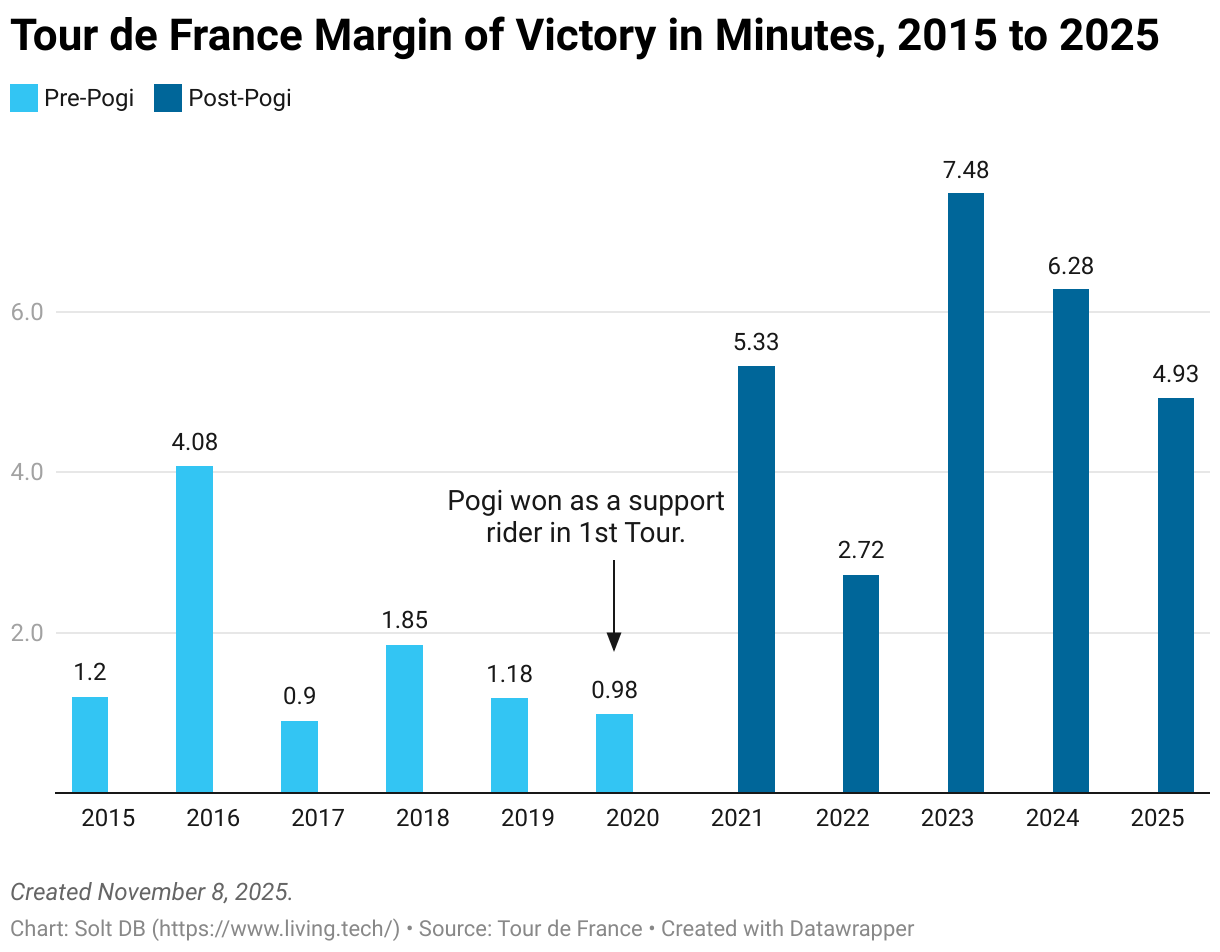

Tadej Pogačar is one of the most accomplished cyclists of all time. He entered his first Tour de France as a support rider in 2020, but when his team leader dropped out, he remained in the competition – and ended up winning the whole damn thing.

Pogi, as he's called, has won more cycling competitions than I can list here, including the Tour de France four times and World Championship Road Race twice. He's won multiple major tournaments in the same year to join a roster of greats you could count on one hand. He's sixth all-time in the number of Tour de France stages won.

Oh, and he's only 27 years old.

How does the Slovenian superstar crush the competition? Well, in cycling, individual riders stick with their teams for most of the race, while competing teams try to stay close to one another in a group called a peloton. This conserves energy by allowing drafting, which sets up a team's speed demon to make a final push closer to the finish line. Cycling is kinda boring until the end.

Pogi is unique. He breaks from his team for a final push, called an attack, up to 100 kilometers from the finish line for a stage. That's virtually unheard of in cycling. Most riders train to be much more conservative.

Even he admits the insanity of his approach, famously saying after a 2024 victory, "For sure it was a stupid move, but in the end stupid worked."

Consider how the margin of victory in the 3,323-kilometer Tour de France has changed since Pogi first saddled up in 2020. His first race in a non-support role wasn't until 2021.

Coherus Oncology is taking a similar approach to Pogi.

Whereas drug developers with a similar financial profile are usually pretty conservative with program selection, the immuno-oncology drug developer has adopted a rather aggressive clinical posture. It's exploring CHS-114 (CCR8 inhibitor) in four tumor types, evaluating casdozo (IL-27 inhibitor) in an ambitious phase 2 study seeking to outperform a blockbuster from Roche, has two additional studies for casdozo in lung cancer and kidney cancer queued up, and is quietly preparing the long-forgotten CHS-1000 (ILT4 inhibitor) for clinical entry or licensing.

It doesn't have much cash – and has burned $136 million in the first nine months of 2025.

Coherus has ample opportunity to outlicense rights, both domestically and internationally, for assets across existing and new indications (those not listed in the pipeline). On paper. The aggressive posture makes sense if management is positioning the business for an acquisition or confident in its asset stack. It wants to present the broadest opportunity set possible to attract partners, buyers, and investors.

In the end, will "stupid" work?

By the Numbers

I tried to set expectations in last quarter's research note. To reiterate, the only meaningful events on the horizon are data readouts and potential partnerships. It's going to be somewhat boring, but drug development has speed limits.

Coherus didn't have a noteworthy third quarter.

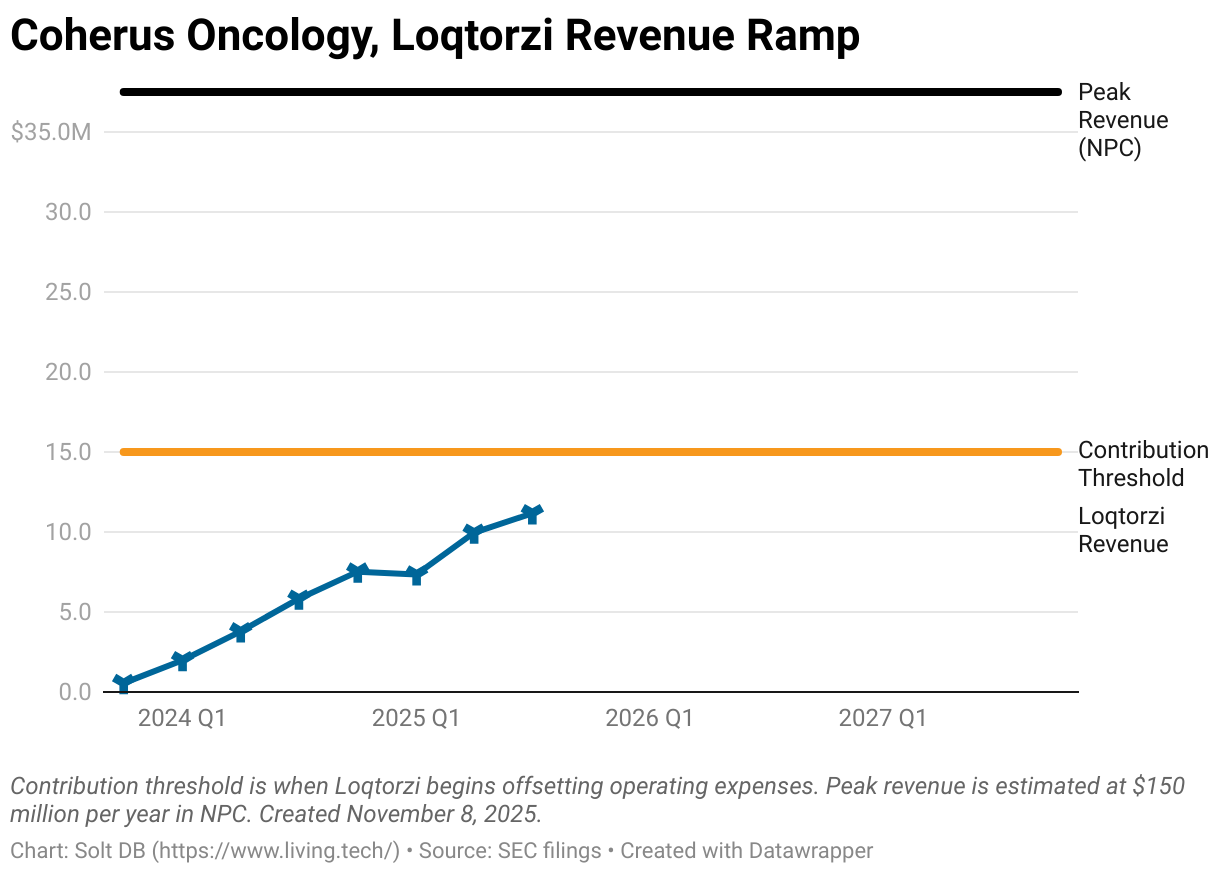

- Loqtorzi revenue was below my model ($11.169 million actual vs. $12.418 million modeled) and gross margin was above my model (67.8% actual vs. 65.0% modeled).

- That resulted in gross profit that was in line with my expectations ($7.85 million actual vs. $8.072 million modeled).

- Journey further down the income statement and operating expenses were also in line with my model ($52.183 million actual vs. $52.500 million modeled).

- All the slightly highers and slightly lowers add up to the most important metric, operating loss, being almost exactly in line with my model ($44.333 million actual vs. $44.428 million modeled).

Loqtorzi's current label includes sweeping approvals for nasopharyngeal carcinoma (NPC), but it's not a high-impact commercial opportunity. As such, the stock won't be driven by the asset – and certainly not in the next 24 months. It'll begin to pay for its commercial infrastructure once it reaches $15 million in quarterly revenue, which could happen in Q4 2025 or Q1 2026.

Denny "The Danger" Lanfear is being aggressive planting seeds in the pipeline. The business reported an operating cash outflow of $136 million in the first nine months of 2025. That's not unexpected, but it's important to understand that it's unsustainable without cash injections.

Coherus ended September 2025 with $191.6 million in cash. That's about 12 months of cash runway if management redlines the balance sheet, which companies tend to avoid outside rare circumstances. If the broader economy hits the skids in 2026, then investors might find themselves in rare circumstances.

It might not matter in the end. The totality of public information makes it likely management is positioning the business as an acquisition candidate. Investors just need to properly set their expectations, as frustration and turbulence seem more likely than a linear rise to the promised land.

Setting Expectations for 2026

Investors who improperly set their expectations are guaranteed to be disappointed. I can already foresee frustration when this or that press release, or data readout, or clinical supply deal, or licensing agreement doesn't trigger a movement in the stock.

Let's lay it out in simple terms. How can investors objectively judge execution at Coherus through the end of 2026? Coherus needs to execute across three facets of the business:

- Data readouts (offense)

- Cash runway management (defense)

- Corporate development (special teams)

These three parts of the business can work synergistically. Favorable data readouts can lower barriers for raising capital or attracting partners, while raising capital can give the company more leverage in corporate development, since it wouldn't be as desperate if negotiations fall through.

Although difficult, forging the right licensing deals – not giving up too much, but giving up just enough to raise meaningful capital – can protect and create value for shareholders while broadening the list of potential acquirers.

Coherus doesn't necessarily want to become too dependent on a single strategic partner. For example, Arcus Biosciences hitched its wagon to Gilead Sciences, which owns 35% of the business. While that funded the business and provided a lifeline, the arrangement made it much more difficult for another drug developer to acquire the company. (Gilead is also one of the worst at business development, so it has and might continue to drag its feet on an acquisition, but that's a separate issue.) That means Arcus has been "stuck" developing its pipeline for many years. Earn it? How boring!

Data readouts (internal)

The first band-aid to rip off is that any specific data readout from the CHS-114 basket study will lead to a surge in the stock price. That's unlikely.

Why should they?

Initial updates throughout 2026 will include a few dozen patients spread across four tumor types. Three cohorts are evaluating two dosing levels each and the fourth is giving patients multiple chemotherapy regimens. They'll provide signals, but not interpretable data.

That's also not the point. While the individual (and preliminary) datasets for CHS-114 won't have much value in isolation, they'll have value in aggregate.

If CCR8 inhibition lives up to the hype as a must-have mechanism of action in immuno-oncology and PD-1 combinations specifically, then it'll be better to go broad than deep. That's something the business can do with its limited cash position. The team is reading the commercial opportunity clearly and aligning the strategy to match – a strength the business has always had, which is one of the reasons I didn't boot it from the coverage ecosystem.

It'll take time to build the aggregate data package.

Data readouts (external)

Barring an epic licensing agreement or strategic partnership, external data readouts are likely to be the most important trigger for the stock.

Institutional investors are weird. They'd rather cry about risk and uncertainty than do any real analysis… but if, you know, Bristol Myers Squibb and Amgen and Roche tell them that CCR8 inhibition is working, then they don't have to actually to their job. They can just suddenly see Coherus as a valuable, standalone drug developer that also happens to be working on CCR8 programs.

Cash runway management

Coherus ended September 2025 with $191.6 million in cash, which provides a roughly 12-month cash runway. That's an awkward length of time.

If management is positioning the business for an acquisition, then it doesn't need to raise capital for advancing CHS-114 or casdozo. (But that's our little secret.) However, a higher cash pile would ease investor concerns in the short term and provide some leverage in negotiations. If partners or acquirers see a low cash balance, then they'll take advantage to wrestle more favorable terms – not great for shareholders. A longer cash runway also provides more breathing room, as working out partnerships or acquisitions can take longer than expected.

There are several identifiable cash infusions on the way or likely:

- (Actual, $7.5 million in Q4 2025): Shout out Raj for finding the details and sharing on Discord. On October 21, Coherus sold 4.635 million shares at an average price of $1.73 per share in a private placement. The gross proceeds were $8 million, so investors can expect roughly $7.5 million net to be added to the cash balance in Q4 2025. The investor was Bering Capital, one of the original venture capital firms in Coherus, which seems a little unusual for them to more than double their stake now.

- (Actual, $2.5 million to $5 million in Q4 2025): Toripalimab earned regulatory approval in Canada in late October 2025, which will trigger a milestone payment from licensee Apotex in Q4 2025. The exact amount isn't known, but Coherus stands to receive $51.5 million (Canadian dollars) in total regulatory and sales milestones. Although Apotex will also pay royalties on sales each quarter, Coherus is required to give all Canadian royalties to Junshi – they won't be much anyway.

- (Possible, $37.5 million Udenyca milestone in Q4 2026): If Udenyca generates $300 million in revenue in any consecutive four quarters from Q3 2025 through Q3 2026 (five quarter window), then it will earn a $37.5 million cash milestone from Intas Pharma. The timing of the payment could be uncomfortable, but Coherus could also sell the royalty for an immediate $25 million to $30 million.

- (Possible, $64.9 million ATM): Like most companies, Coherus has an At The Market (ATM) Offering arrangement that allows it to sell shares directly into the market at the current stock price to raise capital. It's unlikely to tap this vehicle under normal circumstances, but in the event of a short squeeze the company could immediately add four months of runway.

If the company taps its ATM Offering during a short squeeze, then it'll need to do its best Johnny Cash impression and walk the line of dilution. A very high short interest suggests the stock could rise by triple digits in the event of a short squeeze, so there could be an opportunity to make dilution relatively manageable. It'll still sting though.

- Coherus had 120.871 million shares outstanding on October 31, 2025.

- At $4 per share, the full ATM Offering would result in 16.225 million shares of dilution.

- At $6 per share, the full ATM Offering would result in 10.817 million shares of dilution.

- At $8 per share, the full ATM Offering would result in 8.113 million shares of dilution.

The other way to raise capital is through strategic partnerships and licensing agreements.

Corporate development

To rip off another band-aid, licensing deals are unlikely to have meaningful upfront cash components outside specific scenarios.

- Maturity of assets: CHS-114 is an early-stage asset. It's unlikely to yield large upfront cash payments unless full rights are included, which would significantly reduce the asset's value to shareholders.

- Ex-U.S. rights: Coherus has always been focused on commercial opportunities in the United States, which is the most lucrative market for drug sales. Across all blockbuster drug brands, over 60% of revenue is generated in the United States. The remaining 96% of humanity generates the other 40% of revenue. Licensing international (meaning ex-U.S.) rights can provide value, but financial terms match the reality of smaller commercial opportunities.

- Combination drives value: Although CCR8 inhibition is a potentially must-have mechanism of action in immuno-oncology, it only has value when paired with a PD-1 inhibitor. That makes it awkward and unrewarding to sell rights to individual indications.

There are scenarios where Coherus could realize greater value from licensing deals.

- Specific indications for CHS-114: Coherus keeps adding tumor types to the basket study of its CCR8 asset, but there are some indications it cannot realistically explore on its own. Management has drawn attention to the addition of a colon cancer cohort, but it's starting in fourth-line colon cancer – a very small subset. Large print giveth, small print taketh away. To move into earlier lines of treatment would be prohibitively expensive without a partner, as would much larger opportunities like lung cancer, breast cancer, and ovarian cancer – all worth exploring with CCR8 assets, and all better suited for larger drug developers.

- Casdozo ex-U.S. rights: Liver cancer is the sixth leading cause of cancer deaths in the United States, according to the National Institutes of Health SEER database, but the third leading cause of cancer death globally. This makes the indication a rare outlier in terms of commercial opportunity, as it has more value internationally than usual. Casdozo's ex-U.S. rights could therefore be licensed for a meaningful amount of cash upfront, although it would be better to wait for phase 2 data in mid-2026. There's no reason Coherus can't queue up potential partners now and make terms contingent on data, which could result in a data readout and licensing agreement on the same day.

How the business chooses to partner or license its assets will be important for determining the likelihood of an eventual acquisition. If Coherus gives up too much too soon, or carelessly carves up rights, then an acquisition might be much less likely.

For example, Coherus could sell 100% of the rights to using CHS-114 in a major tumor type (ex: lung, breast, ovarian). That would be more valuable upfront, but make an acquisition less likely. If Large Pharma A already carved up asset rights, then why would Large Pharma B want to acquire the business?

Partnering 50/50 rights on larger indications would preserve acquisition potential at the expense of lowering upfront economics. If Large Pharma A owns 50% of the rights, then Large Pharma B could acquire Coherus to bag the other 50%. For reference, six of the top 20 bestselling drugs on the planet and three of the top 10 have split rights – it's a common arrangement.

Finally, licensing agreements or partnerships could also come with equity investments into Coherus. That could provide additional upfront cash and buy-in from strategic partners.

Coherus hired Denny's old buddy from Amgen, Arvind Sood, as the Chief Strategy and Corporate Affairs Officer. He'll take the lead on corporate development (partners), tighten up investor relations, and handle government affairs. Maybe when he's done he can hop over to Relay Therapeutics and add a second paragraph to their press releases…

News Flow & Modeling Insights

(Refined.)

The current model makes the following assumptions:

- Full-year 2025 Loqtorzi revenue of $42.102 million (previous: $44.280 million).

- The pipeline contributes $263 million to the modeled valuation, including $184 million from casdozo and $79 million from CHS-114 (previous: $32 million). The value of the latter has increased due to expansion of the basket study and slightly higher confidence in combinations from real-world biomarker data. It can increase in the near future from data readouts in the competitive landscape.

Margin of Safety & Conviction

Coherus Oncology is considered a Future Compounder position with the following Conviction rating.

- 1 = High (no change)

- 2 = Above Average

- 3 = Average

- 4 = Below Average

The estimated fair valuation based on my current model is below:

- Market close November 7: $1.34 per share

- Modeled Fair Valuation: $3.44 per share

- Allocation Range: Up to 10%

Coherus Oncology reported 120.871 million shares outstanding as of October 31, 2025. The modeled fair valuation above assumes 123.893 million shares outstanding, which is equivalent to 2.5% dilution.

Further Reading

- October 2025 press release announcing Q3 2025 operating results

- October 2025 regulatory filing (10-Q) detailing Q3 2025 operating results

- October 2025 quarterly earnings preview for the Solt DB coverage ecosystem

- August 2025 research note analyzing Q2 2025 operating results

.svg)

.svg)

.svg)

.svg)

.png)

.svg)

.png)

.svg)

.svg)

.svg)