.svg)

There's a simple rule in investing that falls under my "Don't Get Cute" mantra: If you name a price, then don't name a date. If you name a date, then don't name a price.

Right now, investors and analysts can't agree on either for Harmony Biosciences.

The company poured cold water on those hoping for the RECONNECT data readout in conjunction with second-quarter 2025 operating results. After toweling off and warming up again, analysts had to figure out if the slower revenue growth of Wakix was likely to be temporary or enough to knock the business off its guided trajectory for the year. Shares opened the day down 10%, but closed down just 1.7%.

Harmony Biosciences is a relatively low-volume stock, which can feed volatility in either direction on swing news or no news at all. And although the crown still belongs to Coherus Oncology, the narcolepsy leader has a surprisingly high short interest representing 17% of available shares. That represents a short ratio of 7.3x. A value over 5.0x generally means a stock has a lot of doubters. (Coherus has a stratospheric short ratio of 23.3x.)

I'm hoping that plays to my advantage for my position, as a positive data readout for the RECONNECT study could lead to a triple-digit surge in shares depending on achieving specific study endpoints. A failed study shouldn't have a lasting impact on shares, especially since management could immediately repurchase stock under an existing buyback program.

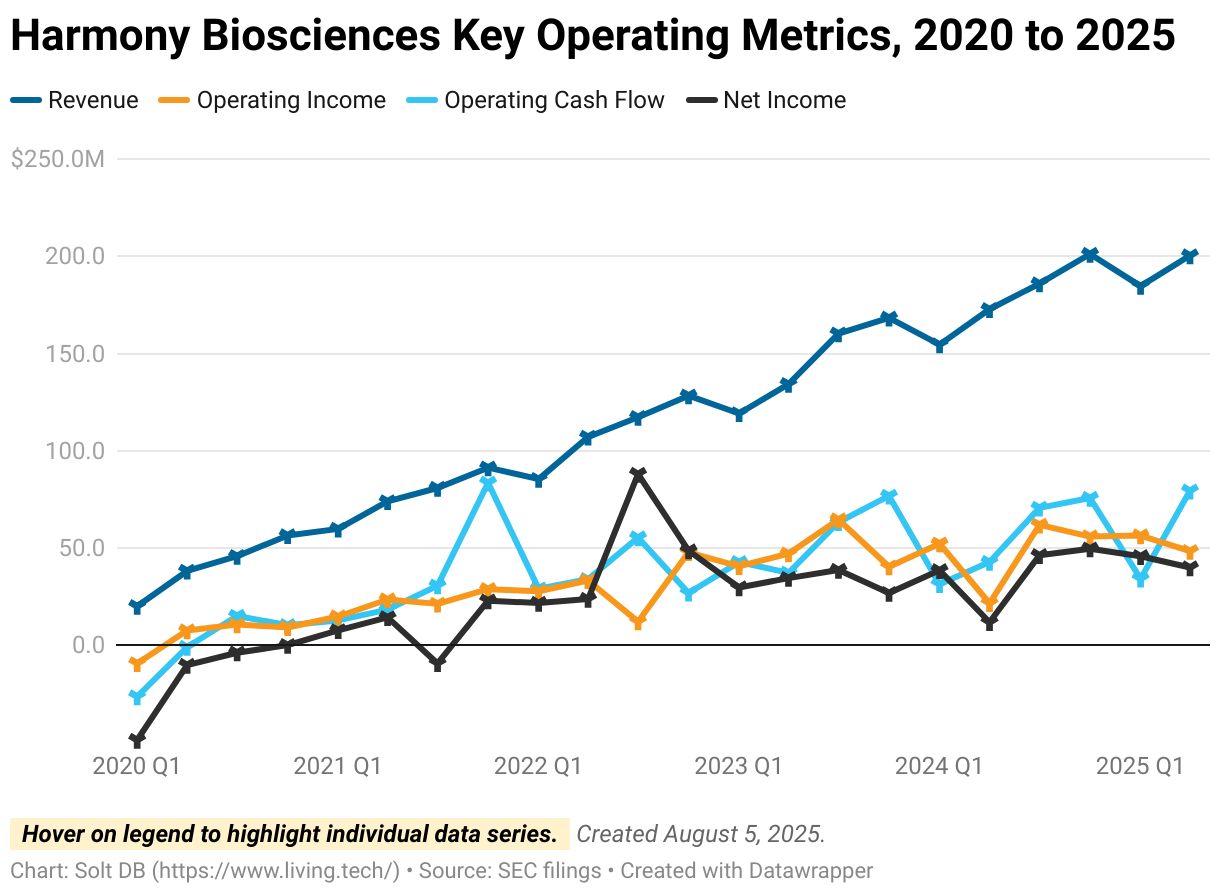

In the meantime, Harmony Biosciences is a rock-solid business. The metrics I track for modeling commercial momentum don't appear to be flashing red for Wakix, so I see no cause for concern for the flagship franchise. Similarly, cash flow and profitability are trending higher than expected.

It sure would be nice to add some commercial diversity and become a multi-product company though – we'll have to wait a little longer for the highly-anticipated data readout, still expected by the end of September.

By the Numbers

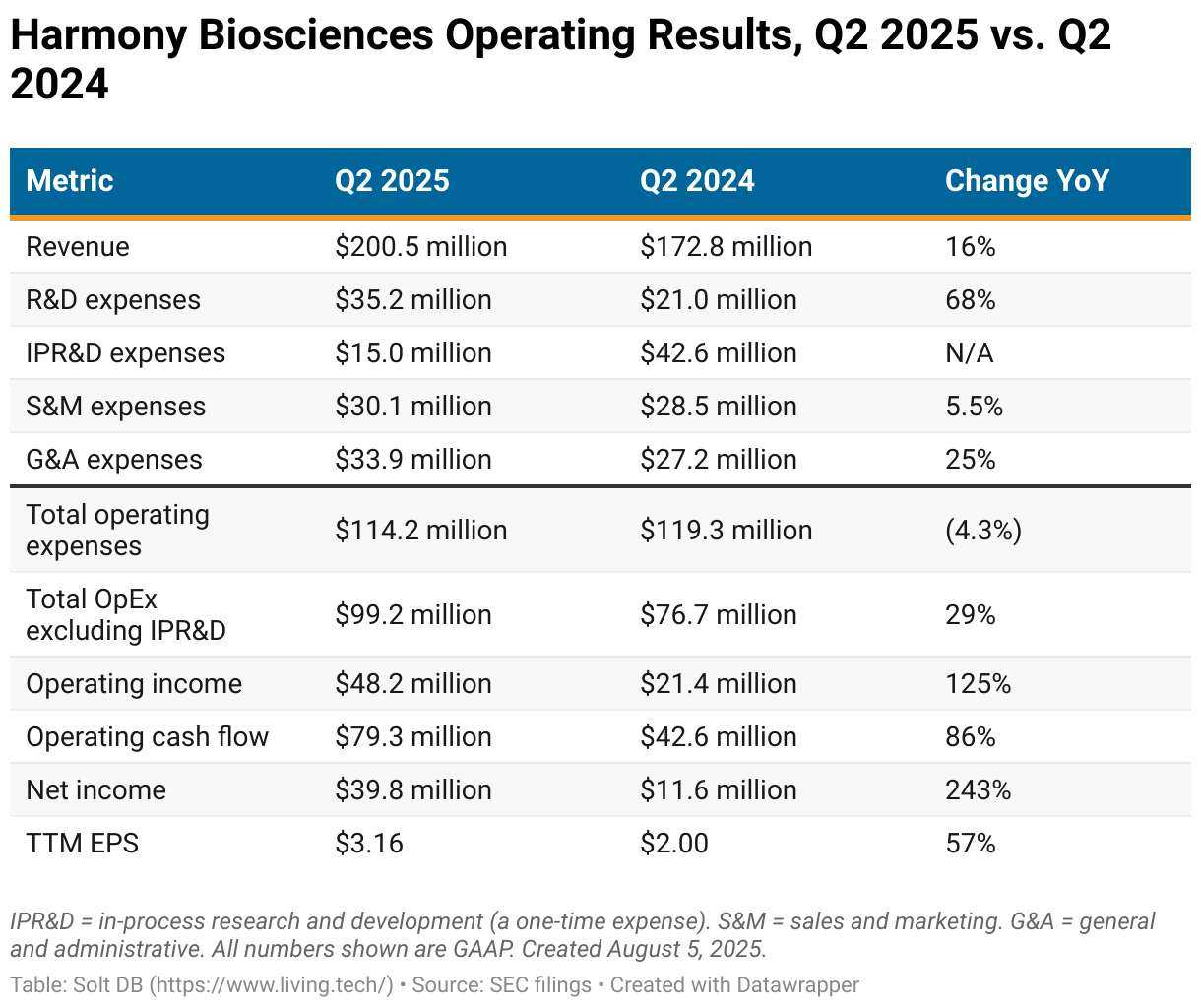

Harmony Biosciences delivered a solid quarter of operations. Quarterly revenue growth slipped below the expected annual growth rate based on the midpoint of guidance, but the business had healthy cash flow and remains comfortably profitable.

Investors can expect operating expenses to increase in the near future. The company's late-stage pipeline spans four active phase 3 programs, while two more could begin by the end of 2025. The impact is already showing up in the data.

Although total R&D expenses fell 21% year over year, one-time items drove up the tallies in both periods. Harmony Biosciences recorded a $15 million charge in the most recent period for its upfront payment to CiRC Biosciences. Last year, it recorded a $42.6 million charge to acquire the orexin-2 receptor (OX2R) agonist from Bioprojet.

Remove those one-time charges, recorded as in-process research and development (IPR&D), and baseline R&D expenses jumped a whopping 68% since Q2 2024.

That also scrambles comparisons of total operating expenses. Removing IPR&D expenses reveals baseline operating expenses across sales, general, administrative, and R&D increased 29% from the year-ago period. The headline figure shows a slight decrease.

This isn't unusual or alarming. Harmony Biosciences has a mature, late-stage pipeline – the most expensive kind. It's also potentially the most rewarding kind. If any two of the four active programs succeed, then the company will diversify revenue and earnings growth away from Wakix. That's worth tens of millions of dollars of increased operating expenses. And considering all four active pivotal programs will have preliminary data readouts by the end of 2026, the recent surge in R&D expenses should be temporary.

A durable slowdown in Wakix could complicate the transition to a multi-product future. Despite Wall Street's initially negative reaction, a closer look at the data reveals no red flags yet.

Second-quarter 2025 revenue of $200.5 million was lower than $201.3 million notched in the final quarter of 2024. That's always uncomfortable. But net income in Q2 would've been the second-highest ever excluding the one-time payment to CiRC Biosciences. Operating cash flow was the second-highest ever behind only the tax-benefit-enriching final quarter of 2021, and that's including the collaboration payment.

Another perspective: Harmony Biosciences could see revenue drop to zero tomorrow and fund itself for six quarters with cash on hand. Many precommercial drug developers don't have that long of a runway.

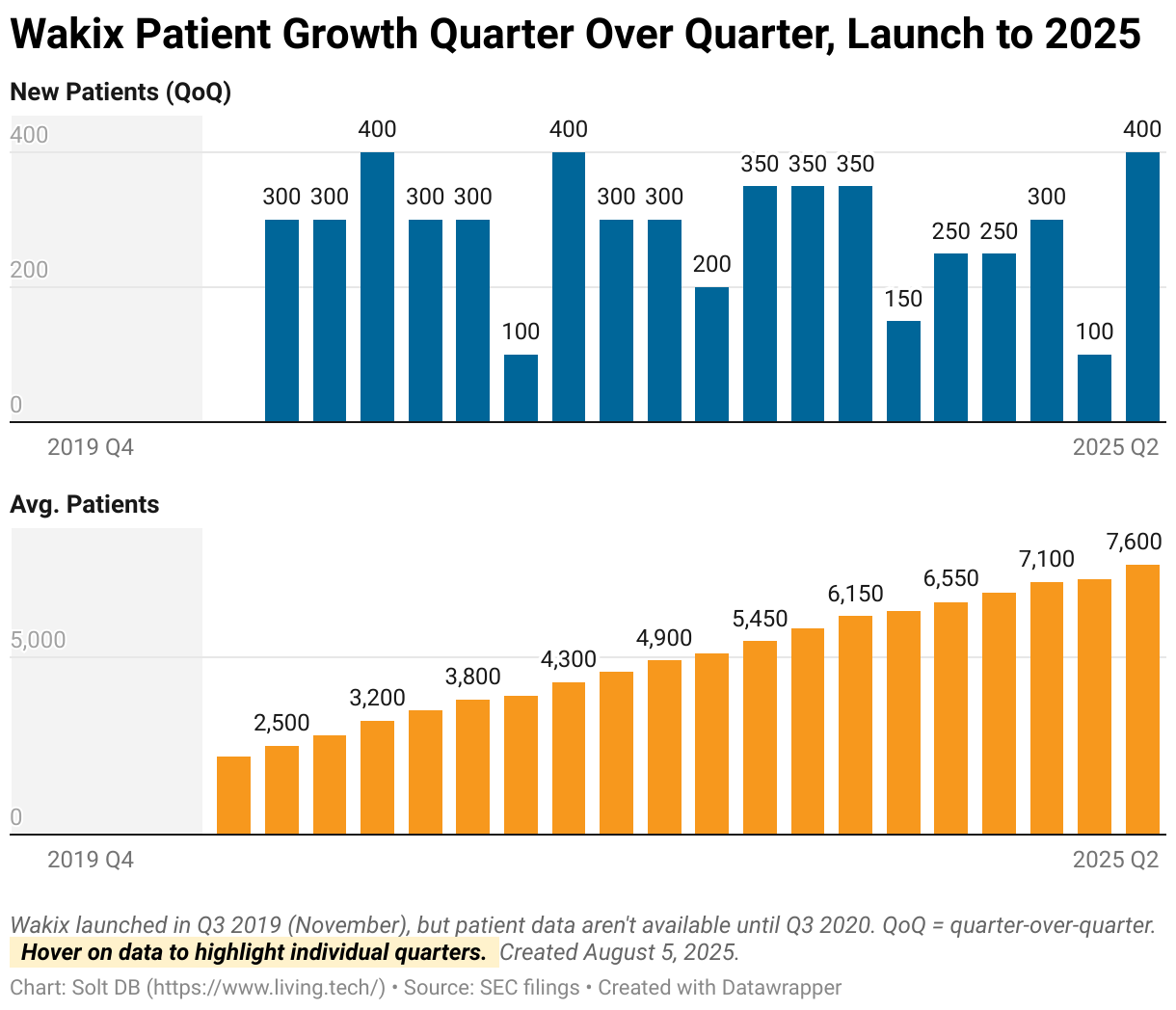

Importantly, revenue growth is a function of patient growth – eventually.

Harmony Biosciences reported a net gain of 400 patients on Wakix in the second quarter. The metric measures quarter-over-quarter performance. The narcolepsy treatment ended June 2025 with an average of 7,600 patients during the quarter, representing a 16% increase year over year.

By comparison, Jazz Pharmaceuticals reported a net gain of 225 patients for Xywav in the second quarter. There are now roughly 10,600 narcolepsy patients on Xywav.

So, why didn't revenue growth surge with patient growth? Sometimes there's just a lag.

Let's look at patient growth data a different way. While there was a net gain of 400 patients since Q1 2025, Wakix patient growth measured 16% in the year-over-year frame. That's what should be compared to revenue growth, which is also measured year over year.

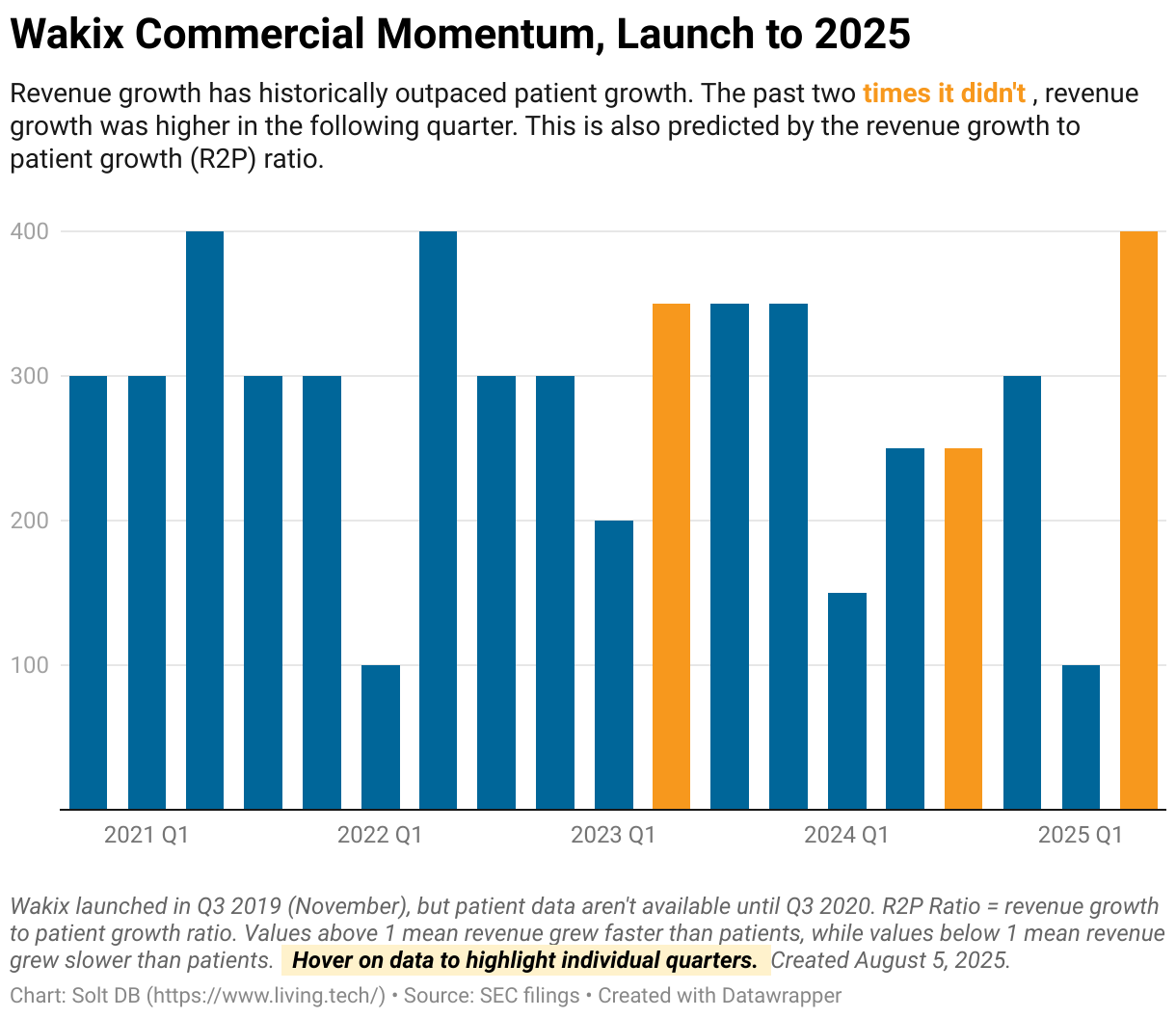

Growth rates for any metric tend to decline as numbers get larger. Still, patient growth shows a much smoother trend over time compared to revenue growth. The latter follows the same general shape, but can be more jagged. Deviations from trend can be driven by various factors, from inventory drawdowns (generally temporary) to pricing dynamics (can be more permanent).

The revenue growth to patient growth (R2P) ratio is the nerdy mathematical way to check in on the trend.

- An R2P ratio below 1.0 means revenue growth is lagging behind patient growth.

- An R2P ratio above 1.0 means revenue growth is outpacing patient growth.

- As growth slows, the R2P gradually converges around a value of 1.0.

- As a product loses market share, the R2P value falls sharply below a value of 1.0 (or becomes negative) for an extended period of time.

Wakix sports a quarterly average R2P value of 1.24 since the third quarter of 2021. That makes sense for a commercial ramp.

In the second quarter of 2025, revenue growth exactly matched patient growth in the year-over-year period. The important thing is it was below the average and below trend. That's happened twice before – Q2 2023 and Q3 2024 – and each instance was followed by higher revenue growth in the subsequent quarter.

Flipping between the third, fourth, and fifth tabs helps to visualize the relationship between revenue growth and patient growth.

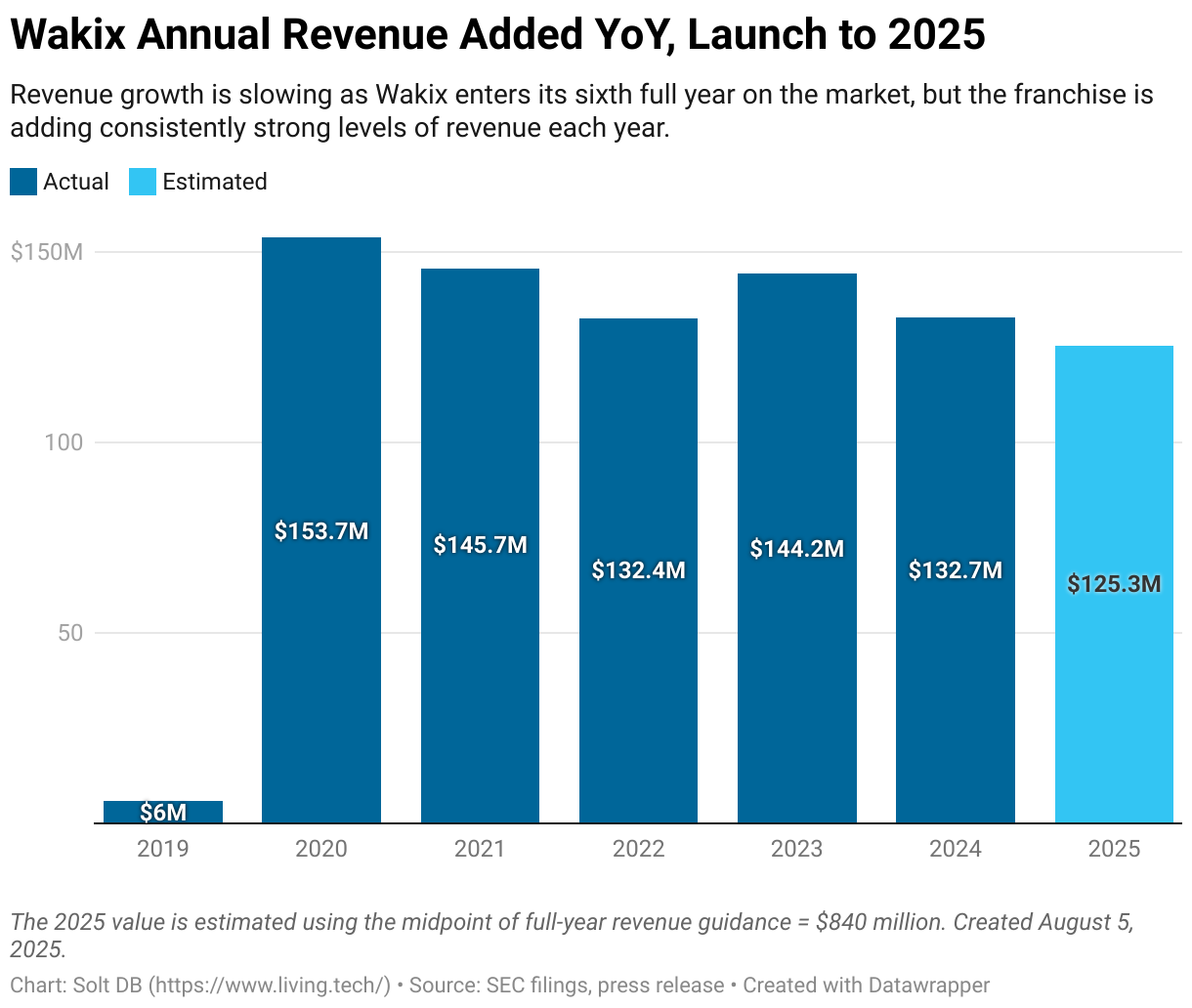

Investors can also use year-over-year revenue added as a barometer for commercial momentum. The steady rise of Wakix since launch has been powered by remarkably consistent growth each year. From 2022 to 2024, Harmony Biosciences grew total annual revenue by $132 million, $144 million, and $133 million, respectively.

This year management expects to add roughly $125 million using the midpoint of annual revenue guidance. Is that a slowdown? Sure. Is that catastrophic? Nope.

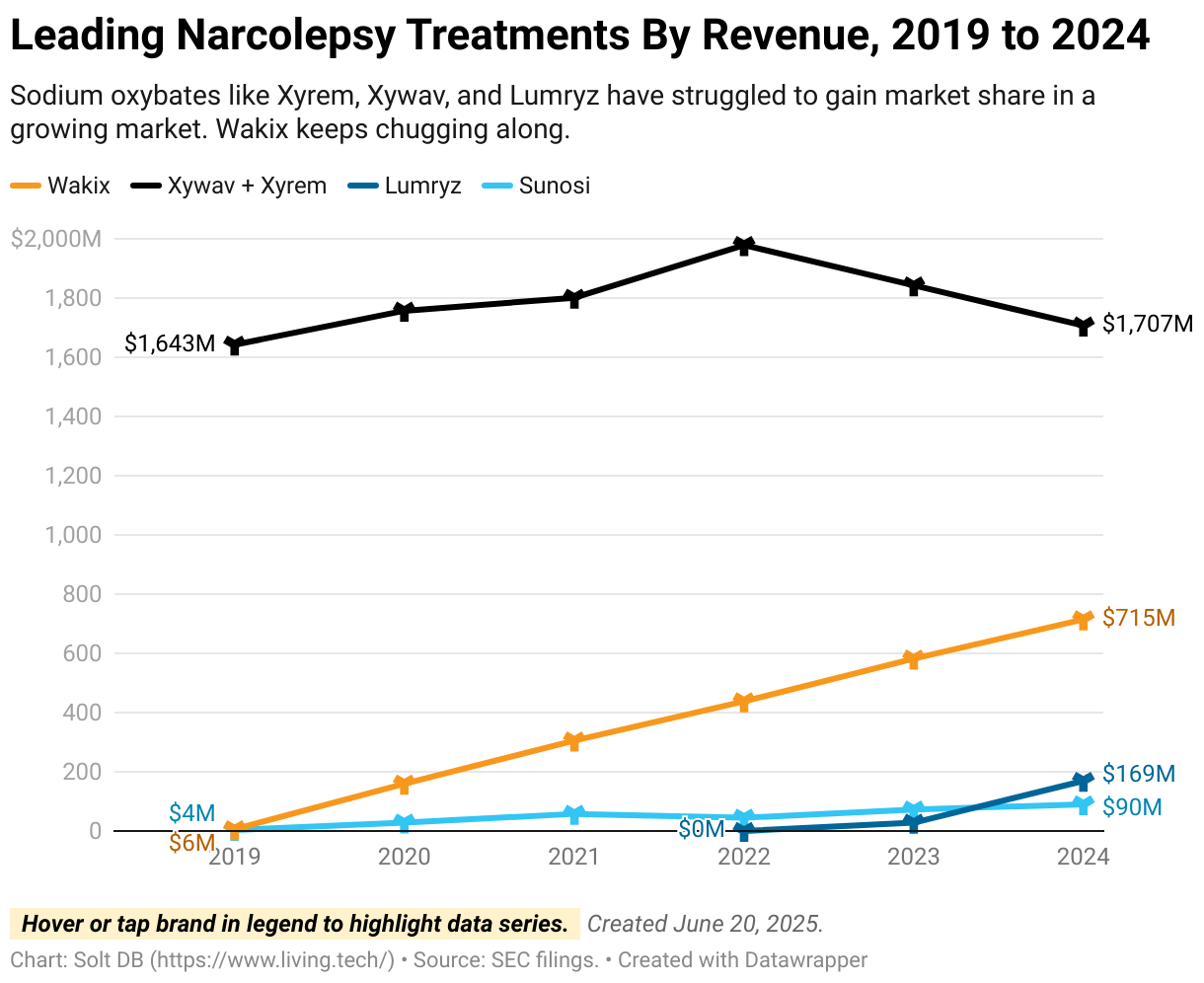

Similarly, investors can compare against the commercial momentum for Jazz Pharmaceuticals. The competitor grew combined Xywav and Xyrem revenue $22.5 million in the first half of 2025 compared to the year-ago period. By comparison, Wakix has added $57.8 million in the same span.

Xywav and Xyrem sported an R2P ratio of 0.66 in the second quarter. It's been well below a value of 1.0 for several years, which is exactly what you'd expect for a franchise with shrinking revenue since 2022.

The competitor's performance is telling. Xywav reported a net gain of 625 patients in Q2 2025, but only 225 patients were being treated for narcolepsy while the other 400 have idiopathic hypersomnia – an indication Wakix isn't approved for.

That suggests Jazz Pharmaceuticals is likely significantly slowing or even decreasing selling prices for its flagship brand. That could potentially represent a headwind for Wakix pricing, although it hasn't slowed patient gains yet.

Simply put, commercial momentum metrics suggest there's good reason to be observant of Wakix's growth trajectory, but no cause for concern.

Around the Horn

A bulging pipeline requires a status update.

ZYN002 in fragile X syndrome (FXS)

Investors are still waiting for a topline data readout from the phase 3 RECONNECT study. Management expects to announce results before the end of September. A successful outcome could force an immediate revaluation of the business, especially since the current market cap undervalues the profitability of Wakix and appears to exclude the entire pipeline.

A potential approval would also hand the company a priority review voucher (PRV), which can be sold for roughly $110 million.

Pitolisant (Wakix) in Prader-Willi Syndrome (PWS)

Harmony Biosciences didn't even mention the ongoing phase 3 TEMPO study evaluating pitolisant in pediatric PWS. The pivotal program began in Q1 2024, which suggests a topline data readout in 2H 2026.

This study is important because, under current regulations, an approval in pediatric PWS would grant Wakix pediatric exclusivity. That would extend by six months the market exclusivity of Wakix in all indications. That means competitors expecting to launch generic versions of pitolisant for narcolepsy in January 2030 would instead have to wait until July 2030.

Six months may not seem like much, but by 2030 it'll be equivalent to $500 million to $600 million in Wakix narcolepsy revenue. That increases the importance of an otherwise niche program in PWS. A potential approval would also hand the company a PRV, which can be sold for roughly $110 million.

Wakix GR

A phase 3 bioequivalence study for the delayed release, or gastro-resistant, formulation of pitolisant should have a data readout before the end of 2025. This will only include narcolepsy patients. A successful outcome could lead to an approval and launch in the second half of 2026. Management expects to transition all or most patients from Wakix to Wakix GR upon launch.

The key advantage of the delayed-release formulation is the ability to avoid titration. That means patients could immediately start treatment on the optimal dose level, instead of gradually ramping to a clinically-relevant dose as a way to mitigate gastrointestinal side effects. Up to 90% patients starting an existing narcolepsy treatment require titration, so this could be a unique label opportunity. Securing approval and executing a transition would greatly increase franchise longevity once OX2R agonists arrive and could make generic pitolisant competition in 2030 a moot point.

Wakix HD

A pair of phase 3 studies for the high-dose formulation of pitolisant are expected to start in the fourth quarter of 2025. Wakix HD also includes a gastro-resistant coating. Unlike Wakix GR, the high-dose formulation gives the company another shot at earning approval in idiopathic hypersomnia. Wakix was rejected in that indication earlier this year.

Harmony Biosciences thinks an approval decision for Wakix HD could happen in 2028. Both next-generation formulations of pitolisant have patent protection until 2044.

Clemizole (EPX-100) in rare epilepsies

A pair of phase 3 studies for clemizole in rare epilepsies are ongoing with expected topline data readouts in 2026.

Similar to the current narcolepsy market, many patients with Dravet syndrome (DS) and Lennox-Gastaut syndrome (LGS) take multiple treatments simultaneously in search of symptom relief. Similar to Wakix, the squeaky clean tolerability profile of clemizole could make it a valuable addition to treatment stacks. That could support a swift commercial ramp despite a crowded competitive landscape.

Epidiolex from Jazz Pharmaceuticals, approved in both DS and LGS, is on pace to become a blockbuster in 2025. That supports a healthy revenue opportunity for clemizole should it earn approval.

CiRC Biosciences collaboration

During the second quarter, Harmony Biosciences formed an early-stage research collaboration with CiRC Biosciences.

The narcolepsy leader essentially purchased the right-of-first-refusal to two cell therapy programs for $15 million total. If they achieve certain preclinical proof-of-concept milestones that support thrusting them into clinical trials, then Harmony Biosciences will fork over $10 million per program and agree to pay out future development, regulatory, and commercial milestones as well as royalties.

The programs, CBS-105 (narcolepsy) and CBS-104 (rare epilepsies), are in discovery-stage research right now. They aim to convert stem cells into specific types of brain cells. In this case, brain cells with functional orexin receptors and dopamine receptors, respectively. The initial clinical programs are likely to focus on treatment-resistant narcolepsy and epilepsies, but successful results could enable use in broader patient populations.

It's still very early, there are no data to scrutinize, and this is a totally new therapeutic modality. But Harmony Biosciences is on pace to generate over $250 million in operating cash flow this year and the biotech winter provides a target-rich landscape. Why not take some low-risk, low-cost swings?

One detail: Both companies were formed by biotech fund Paragon Biosciences. These incestuous relationships can sometimes be more about shuffling cash between entities than a serious research collaboration, but the programs align perfectly with Harmony Biosciences' focus on narcolepsy and rare epilepsies. We'll see.

Additional deal potential

Management hinted at the potential to make additional acquisitions, potentially including assets that are already generating revenue. I wouldn't get my hopes up.

The business might be in great shape financially, but the cash balance of $672 million cannot buy a meaningful commercial asset. I'd expect similar deals, if any, to those made in the past for promising late-stage assets, such as the acquisitions of Zynerba Pharmaceuticals (for ZYN002) and Epygenix Therapeutics (for EPX-100 and EPX-200).

News Flow & Modeling Insights

(Refined.)

My current model is based on properly valuing the underlying business, assuming no threat from generic competition to Wakix, and a risk-adjusted contribution from ZYN002. This is a conservative model focused on near-term de-risking events.

The rest of the pipeline, from new formulations of pitolisant to the late-stage rare epilepsy franchise, make no contribution yet. That means my current model excludes three ongoing phase 3 clinical programs. It also excludes the value of a PRV that could be penciled in upon a positive data readout from the RECONNECT study.

I expect to add contributions from the rare epilepsy franchise soon, although I need to dig into the surprisingly weak quarter for Jazz Pharmaceuticals' Epidiolex announced hours ago. Was that due to an asset-specific or a landscape-wide headwind? I also want to triple check the good-yet-maybe-bad data readout from Praxis Precision Medicines two days ago. Its drug candidate delivered solid efficacy, but investors weren't sure how to interpret the data since patients in the study were on an average of two other epilepsy treatments. The same dynamic could scramble the data readout for clemizole in 2026.

Harmony Biosciences has a modeled fair valuation of $3.953 billion or $67.69 per share.

The current model makes the following assumptions about key operating metrics:

- Full-year 2025 revenue of $835.222 million, down slightly from a prior expectation of $837.233 million and lower than $840 million at the midpoint of guidance.

- Full-year 2025 operating expenses of $431.150 million, up from a prior expectation of $409.994 million ($424.994 million accounting for the CiRC Biosciences collaboration payment), marking an increase of 17.5% from the year-ago period.

- Full-year 2025 net income of $178.836 million or GAAP earnings per share (EPS) of $3.10, up from $173.772 million and $2.98 respectively. The year-end outstanding share count is expected to be 58.396 million, assuming no purchases under the active share repurchase program. This does not account for one-time charges, adjustments, or acquisitions.

The RECONNECT study is modeled with a roughly 62% probability of success, defined as a positive outcome in Q3 2025 and earning FDA approval in the second half of 2026. The asset ZYN002 contributes $210.8 million to the valuation.

If the RECONNECT study fails, then investors can expect the valuation to decrease significantly. For example, a valuation of $1.5 billion would be equivalent to $25.86 per share.

Harmony Biosciences would be expected to repurchase up to $150 million in shares – the full amount remaining under its active share buyback program – which would cancel 10% of the shares outstanding at this valuation level. That provides a rare backstop against a failed outcome.

In the example above, the company could repurchase roughly 5.8 million shares. If the business eventually regained its current valuation based on the profitability enabled by Wakix, then it would be valued at $2 billion or $38.74 per share. That provides an additional cushion to exit positions with roughly neutral returns.

Margin of Safety & Conviction

Harmony Biosciences is considered a Current Compounder position with the following Conviction rating.

- 1 = High

- 2 = Above Average

- 3 = Average

- 4 = Below Average

The estimated fair valuation based on my current model is below:

- Market close August 5: $34.94 per share

- Modeled Fair Valuation: $67.69 per share

- Allocation Range: Up to 5%

Harmony Biosciences reported 57.533 million shares outstanding as of August 1, 2025. The modeled fair valuation above assumes 58.396 million shares outstanding, which is equivalent to 1.5% dilution.

Further Reading

- August 2025 press release announcing Q2 2025 operating results

- August 2025 regulatory filing (10-Q) detailing Q2 2025 operating results

- June 2025 research note analyzing the commercial strength of Wakix in the context of the narcolepsy competitive landscape

- June 2025 research note introducing coverage of Harmony Biosciences

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)