.svg)

Editorial note (June 26, 2025): The original version of this research note misstated the CONNECT and RECONNECT study designs, specifically the blinded period durations. The CONNECT study was blinded for 14 weeks, while the RECONNECT study will be blinded for 18 weeks. The RECONNECT study has also enrolled individuals aged 3 to 30 years old.

Retail investors are overwhelmingly more familiar with Axsome Therapeutics than Harmony Biosciences. I should know; I was the one who began coverage of Axsome Therapeutics at The Motley Fool against the will of the editorial team. The stock is up 945% from the publish date of the linked article to this research note.

It's certainly a great story.

The business was once valued at $53 million. Today it's valued at $5,200 million. The market's disrespect wasn't intentional. Axsome Therapeutics was developing a pipeline of neurological and central nervous system (CNS) drug candidates – notoriously difficult to translate to phase 3 success – based largely on repurposing existing treatments for new indications.

For example, its then-lead drug candidate for major depressive disorder was a combination of dextromethorphan and bupropion, which are commonly used as a cough suppressant and to help people stop smoking cigarettes, respectively. Why the finch should those work in treating depression?

But they did. It made sense from a clinical perspective even before clinical studies were wrapped up. It was easy to miss.

The combination, now branded as the FDA-approved drug Auvelity, generated $96 million in the first quarter of 2025. Axsome Therapeutics has since acquired a niche narcolepsy drug, Sunosi, and earned approval for its third commercial drug product, Symbravo, to treat migraines. There are some shady arrangements between the CEO and the corporate entity that aren't shareholder friendly, and the stock has consistently traded at a premium, but if you squint your eyes and tilt your head, then the potential to grow into its lofty valuation is there on paper.

For investors who have a crick in their neck or hints of FOMO, Harmony Biosciences is a more attractive analogue of Axsome Therapeutics sitting in plain sight.

- Axsome Therapeutics generated full-year 2024 revenue of $385 million, operating income of negative $281 million, and operating cash flow of negative $128 million.

- Harmony Biosciences reported full-year 2024 revenue of $714 million, operating income of $191 million, and operating cash flow of $220 million. It's the only company in the Solt DB coverage ecosystem with a share buyback program.

Axsome Therapeutics is valued at $5.2 billion. Harmony Biosciences is valued at $1.99 billion. I don't make the rules.

The difference – for now anyway – is that Harmony Biosciences is a single-product company staring down an onslaught of generic competition. Investors interested in a position need to dig deep into the context and nuance.

The threat of generic competition to the lead and currently only drug product, Wakix, is likely to be neutralized by settlements with challengers and new formulations that can extend patent protections to 2044. Wakix is on pace to generate $840 million in revenue this year, which among narcolepsy treatments is second only to the $1.7 billion haul expected for Xywav from Jazz Pharmaceuticals.

Unlike Axsome Therapeutics, Harmony Biosciences could have two drugs with blockbuster potential on the market in 2026, pending results from a separate asset in fragile X syndrome (FXS). That could alleviate concerns about threats to Wakix and unlock significant value.

Enter nuance. At the same time, investors cannot ignore long-term threats to the company's narcolepsy leadership. Whereas Wakix works on histamine H3 receptors to improve wakefulness, more recent scientific revelations have identified deficient orexin-1 receptors (OX1R) and orexin-2 receptors (OX2R) in the brain as the key regulators of wakefulness. Treatments that rebalance those signals are likely the future.

Adding to the nuance, Harmony Biosciences has licensed a next-generation drug candidate from the Japanese researcher who discovered the importance of OX2R (and could one day soon earn a Nobel Prize), but the molecule optimizes a different metric than everything else in the jampacked competitive landscape. If that's the wrong bet, then the company will miss out on the next-gen opportunity altogether. I don't make the rules.

What a rollercoaster. So, what's the investing thesis here? There's a short-term window where Harmony Biosciences could enjoy a significant increase in valuation. A successful phase 3 data readout in FXS expected in Q3 2025 could alleviate concerns about Wakix's competitive positioning, allowing investors to refocus on the underlying strong fundamentals of the business. It's trading at just 11.3x this year's earnings, so there's plenty of room to run.

To be blunt, neuro indications are notoriously difficult to translate into late-stage success, and regulators could still find reasons to reject an approval application in 2026 even with a successful data readout in the next few months. While a failed study would hardly be a surprise, I think the study design makes a positive outcome more likely than Wall Street is considering. The gap between consensus expectations (analysts expect the study will fail) and the modeled odds of a positive data readout could lead to an overnight revaluation for Harmony Biosciences.

The stock would fall if the study fails, but a low valuation supported by solid profitability offers some protection. So does an active share repurchase program, which could allow the company to buy back 10% of outstandings shares to backstop a negative reaction from Wall Street. How often do you get insurance in biotech investing for a failed phase 3 study?

Historical Context

Unlike tech-savvy startups that launch with bags of cash and dominate headlines by promising to cure all diseases by next Tuesday, Harmony Biosciences was quietly founded in 2017 by biopharma fund Paragon Biosciences. It didn't have a technology platform (it still doesn't) or rockstar scientists. Instead, it was founded around a license to a single asset being developed by Bioprojet, a French research institute largely off the radar of Wall Street.

The novel molecule, pitolisant, increases histamine production in the brain by binding to the histamine H3 receptor. Histamine plays many roles in the body, from regulating immune responses to impacting gut health. Its effect is determined by the specific receptor to which it binds. If you suffer from seasonal allergies and have ever hugged a bottle of an anti-histamine like Benadryl, Claritin, or Zyrtec; then histamine might be your sworn enemy.

Be careful about your call to arms though.

More recent discoveries show histamine also serves as a key molecular currency ("neurotransmitter") for cellular communication between neurons in the brain. As such, boosting histamine levels in the brain can help to treat excessive daytime sleepiness (EDS) and cataplexy (sudden muscle weakness). Both are the primary symptoms of the chronic sleep disorder narcolepsy, which is categorized as type 1 (NT1) or type 2 (NT2).

Whereas seasonal allergies are driven by the activity of the histamine H1 receptor, the H3 receptor governs its role as a neurotransmitter. The latter is exclusively expressed in the brain – and it's found densely packed in nearly every tissue. Although pitolisant was the first drug to act on H3, drug developers are exploring ways to modulate the receptor's activity for various indications unrelated to sleep/wake disorders.

The simple discovery of histamine's role in regulating sleep/wake states has launched pitolisant, branded as Wakix in the United States, as a leading treatment for narcolepsy. Whereas most prior treatments were regulated as controlled substances due to their potential for dependency and abuse, pitolisant's simple mechanism of action allows it to avoid stricter oversight. That's led to swift commercial adoption. Wakix is expected to generate full-year 2025 revenue of roughly $840 million – a solid ramp since launching in late 2019.

Harmony Biosciences kept things simple while guiding the U.S. ramp of pitolisant, but has more recently redeployed its Wakix windfall in a series of acquisitions. These transactions have added a cannabidiol (CBD) gel with potential in fragile X syndrome (FXS), two molecules being developed for rare epilepsy conditions such as Dravet syndrome and Lenox-Gastaut Sydrome, and a next-generation asset for narcolepsy.

When combined with additional clinical trials underway for pitolisant, Harmony Biosciences will boast six phase 3 studies by the end of 2025.

By the Numbers

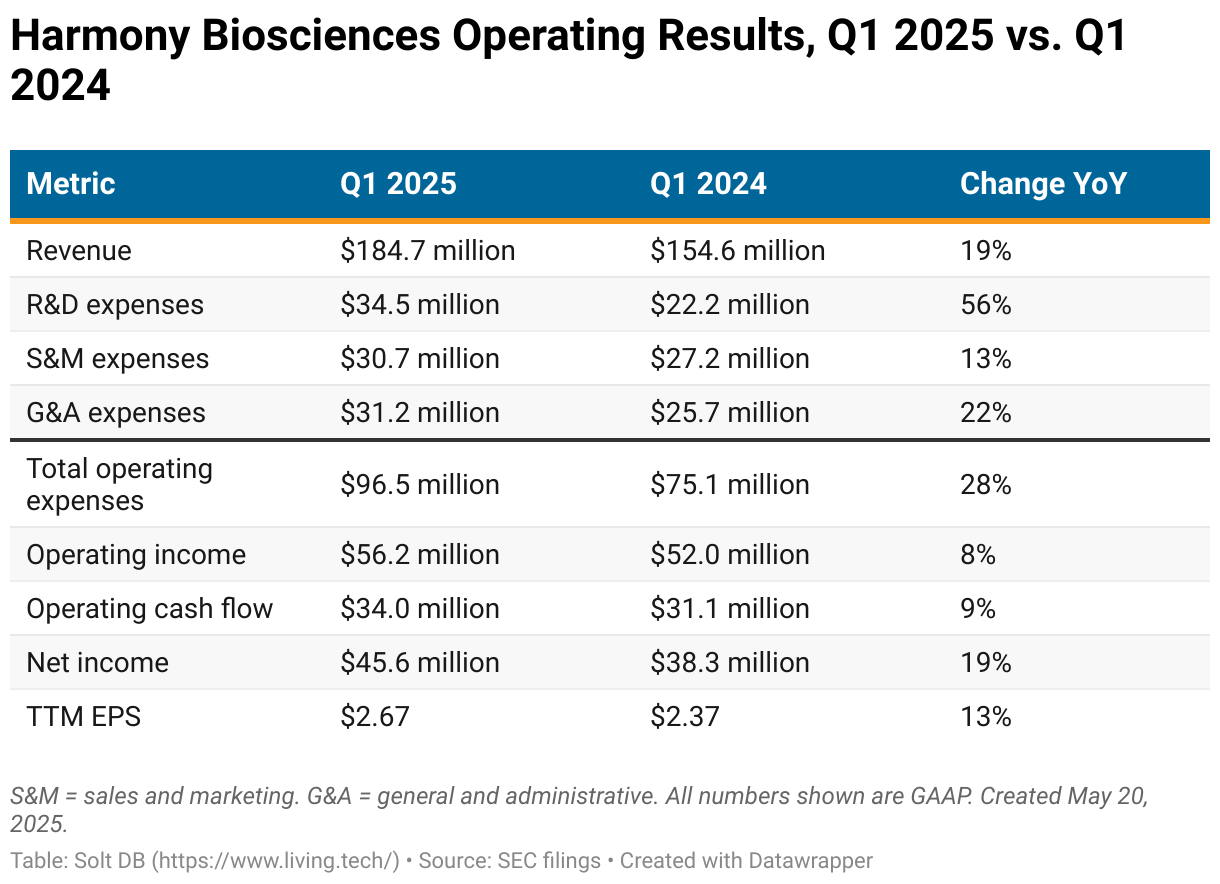

Harmony Biosciences is objectively a strong business, even if it is fully dependent on a single product. The company grew Wakix revenue to $184 million in the first quarter of 2025, up 19% from the year-ago period. Full-year 2025 revenue guidance expects $840 million at the midpoint, representing annual growth of 20%. I model slightly less.

Although the business is comfortably profitable, expenses are growing much more quickly than revenue. The investments required to support a large, late-stage pipeline explain the rise.

It's always important to consider the longer-term trajectory of a business, as point-in-time snapshots can be misleading. The commercial execution from Harmony Biosciences is clearly evident when visualizing key operating metrics since quarterly numbers first became public. A couple other trends stand out.

First, the seasonality of drug development is easy to spot. Drug products tend to generate less revenue in the first quarter than in the preceding fourth quarter. That shouldn't be confused with weakness or a struggling commercial ramp.

Second, the business has had weaker operating and net margins more recently compared to the initial periods of Wakix's ramp. That's due to rising operating expenses to support clinical programs, but also due to income tax treatment for newly-commercial companies.

In a trend we'll see with other emerging drug developers in the coverage ecosystem, Harmony Biosciences didn't have to pay income taxes when it first became profitable. That's because it could carry forward losses from prior periods before Wakix launched. But Benjamin Franklin was right in the end.

- In 2022, the business generated $104.7 million in earnings before income taxes (EBIT) and recorded a tax benefit of $76.8 million, resulting in a net income of $181.5 million.

- In 2024, the business generated $191.8 million in EBIT and paid $46.3 million in taxes, resulting in a net income of $145.5 million.

As a commercial drug developer with steady profits, shares of Harmony Biosciences will be more influenced by real-world earnings. The business should consistently convert about 20% to 25% of revenue into net income, or about 70% to 75% of operating income, impacted by one-time charges here and there. That means the business should be expected to generate full-year 2025 net income of at least $168 million, or earnings per share (EPS) of at least $2.89.

That also means the stock is currently trading at about 12.1x earnings – or just 9.7x if it reaches the upper bound of the range.

Why is Harmony Biosciences valued with such disrespect?

There seems to be little interest in several profitable, neuroscience-focused drug developers right now. Both Alkermes and Jazz Pharmaceuticals are trading at just 15x trailing earnings, although the duo is expected to grow revenue by negative 11% and positive 4% this year, respectively.

Shares of Harmony Biosciences would need to rise to $40 per share to go from its current level of "shameful disrespect" to merely "moderate disrespect" like its peers. That's before accounting for an expected 20% increase in revenue this year, well above Alkermes and Jazz.

In the near term, the stock price will be dictated by a single de-risking event: the phase 3 data readout of the CBD gel candidate, ZYN002, expected in Q3 2025. A successful outcome should unlock considerable value, especially since it has the potential to be the only approved treatment for any symptom of FXS. More importantly, it would allow Harmony Biosciences to shed its "one-trick pony" label, helping to offset the negative impact from competitive risks for Wakix on the valuation.

Around the Horn

Let's dive into the core assets and pipelines wielded by Harmony Biosciences, as well as the risks and potential de-risking events surrounding each.

Generic Threats to Wakix

Generic competition is often misunderstood by investors.

Small molecule drugs like Wakix are granted five years of market exclusivity upon earning regulatory approval. These become known as the reference product, since they represent the first approved use of the active ingredient(s) in a specific indication. In this case, pitolisant is the reference product and the active ingredient protected by patents.

Challengers can file an abbreviated new drug application (ANDA) seeking regulatory approval for a generic version of a reference product after the five-year period ends, or four years in some cases. Approval can be granted even if patents haven't expired yet – a common misconception.

Generic competitors can take two approaches when filing an ANDA:

- Claim their copycat doesn't infringe on the reference product's intellectual property

- Argue the reference product's intellectual property is invalid

Harmony Biosciences has received notice from seven companies – Lupin, Novugen, Novitium, Zenara Pharma, AET Pharma, Annora Pharma, MSN Pharma – seeking to file ANDAs with the U.S. Food and Drug Administration (FDA) for pitolisant. Each has made one or both of the arguments above, claiming they don't infringe on pitolisant's intellectual property and/or that it's invalid anyway.

This is common practice in the generics (and biosimilars) landscape. Typically, challengers file ANDAs with the understanding they'll be taken to court by the owner of the reference product, then reach a settlement spelling out a specific date they'll be able to launch. This reduces uncertainty by providing a firm launch date – usually closer to the expiration of intellectual property – and legally protects them from being required to pay royalties. That last part is key.

The three key patents for pitolisant expire in September 2026, September 2029, and March 2030. Therefore, investors can expect generic competition is most likely to be delayed until sometime in 2030 following settlements.

The volume of generics threatening to launch does add some uncertainty. If just one company resists a settlement and wins a court case in its favor, then that would jeopardize all other settlements. However, this is exceedingly rare in drug development with only a handful of examples in the last decade, almost all being biosimilars. An overwhelming body of legal precedent favors reference products over generics.

Harmony Biosciences has successfully consolidated all challengers into a single court case, which is scheduled to begin February 17, 2026. Novugen has already reached a settlement that will allow its generic pitolisant to launch in January 2030, which could get delayed to June 2030 if Wakix is soon granted pediatric exclusivity in narcolepsy.

Investors might expect a steady trickle of settlement announcements leading up to the court date.

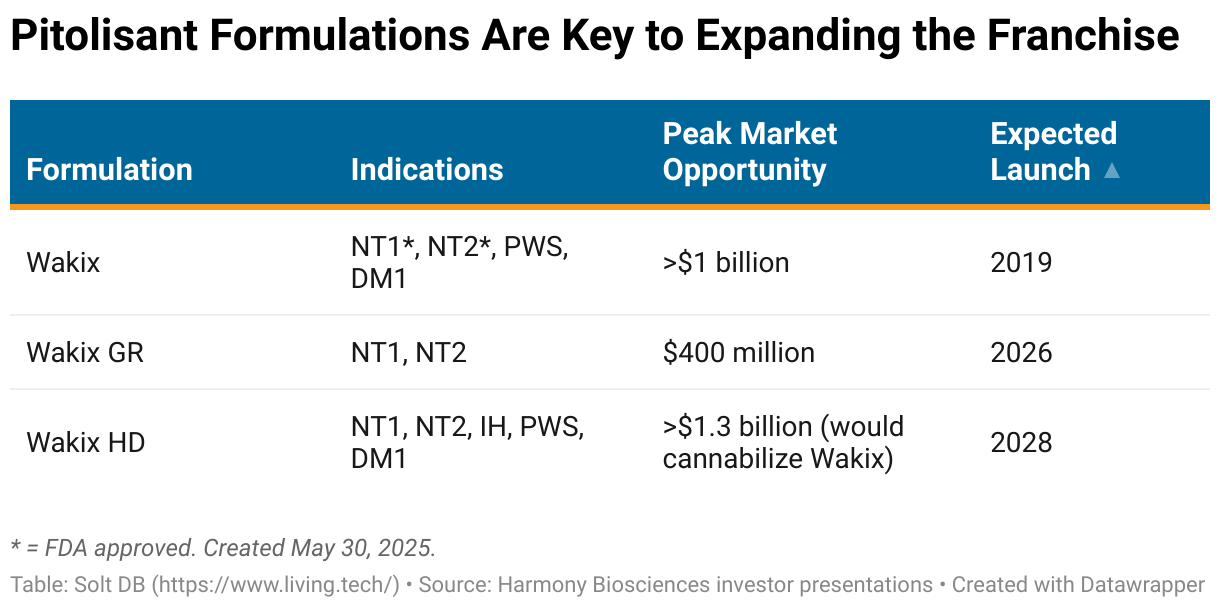

New Formulations of Wakix

Pushing generic launches into 2030 is important not only to give Wakix another four full years of market exclusivity, but also to buy time for two new formulations of pitolisant to launch. Each could launch before 2030 – mitigating the generic threat to Wakix – and extend patent protection to 2044.

Harmony Biosciences is developing Wakix GR ("gastro resistant"), which has a protective coating to reduce certain gastrointestinal side effects and the need for titration. For narcolepsy patients taking any treatment (including Wakix), up to 20% report nausea and 88% report gastrointestinal side effects. Additionally, all treatments require titration for new patients in an attempt to alleviate these symptoms. Titration means a gradual ramp to a recommended dose, which can delay the time to symptom relief.

The company is also developing Wakix HD ("high dose"), which is designed to have greater efficacy and position the franchise for new market opportunities. For example, a higher dose pitolisant could have an expanded label to include the treatment of fatigue in narcolepsy patients, while also earning approvals for sleep/wake disturbances beyond narcolepsy such as idiopathic hypersomnia (IH) and symptoms associated with myotonic dystrophy type 1 (DM1), as well as behavioral issues associated with Prader-Willi Syndrome.

Wakix GR could have a regulatory decision date in 2026, while the company is targeting a PDUFA date in 2028 for Wakix HD. Both provide a comfortable margin relative to generic launches in 2030, which could cushion any potential regulatory delays. It's still beneficial to launch and ramp new formulations as soon as possible.

The Rise of Orexin-2 Receptor Agonists

Even with new formulations of pitolisant, Harmony Biosciences could see its narcolepsy leadership mowed down by next-generation competition. The rise of OX2R agonists represents a potentially more effective route to treat sleep/wake disorders such as narcolepsy and IH.

The threat shouldn't be dismissed. In fact, next-generation competition from OX2R agonists is hands down the biggest risk facing the business. But emerging clinical evidence suggests it's also not as clear cut as analysts might think.

The human brain produces neuropeptides, or small protein fragments, called orexin-A and orexin-B. These play a key role in regulating sleep, hunger, and the behavioral reward system by directly and indirectly influencing various hormones. They do so by binding to OX1R and OX2R, which act like on/off switches for wakefulness. These receptors guide the transitions between wakeful states, rapid eye movement (REM) sleep, and non-rapid eye movement (NREM) sleep. The goal for narcolepsy treatments is to stave off the onset of REM sleep during the day.

Sleep/wake disturbances are indicated in various neurological disorders, but excessive daytime sleepiness (EDS) is the primary symptom of narcolepsy. Whereas NT1 is known to be driven by orexin deficiency, the cause of narcolepsy NT2 isn't fully understood. There are an estimated 60,000 individuals living with NT1 in the United States, 140,000 with NT2, and 40,000 with IH.

Wakix is approved for both NT1 and NT2 in both children and adults. In February 2025, it was rejected as a treatment for IH due to a poor study design, but Harmony Biosciences expects to take another crack at the opportunity with Wakix HD.

Drug developers have previously attempted to inhibit (antagonist molecule) or activate (agonist molecule) orexin receptors to treat various neurological conditions, from panic disorders to addiction to narcolepsy. Ever heard of Valium? It's an OX1R inhibitor, although that wasn't understood when it was developed in 1959. Several clinical trials for molecules that muck with orexin receptors have been terminated due to devastating side effects including hallucinations, worsening panic episodes, and patient suicides.

Researchers believe these should be avoided for agonist molecules optimized for selectivity of OX2R over OX1R. But there's emerging evidence that activating OX2R might not be enough for long-term relief of narcolepsy symptoms, as OX1R still plays a key role in regulating sleep/wake states.

More important, we don't yet understand how long-term activation of OX2R impacts neurological health. What happens if patients stop treatment six months later? Two years later? The FDA could require long-term follow-up studies for this class of drugs – and the potentially severe consequences of messing with orexin receptors could nix the potential opportunity altogether even after approvals are handed out.

This could be similar to JAK inhibitors in immunology, which regulators required to carry dreaded black box warnings after the drug class had already generated billions of dollars in revenue.

Will Harmony Biosciences Be Competitive in OX2R Agonists?

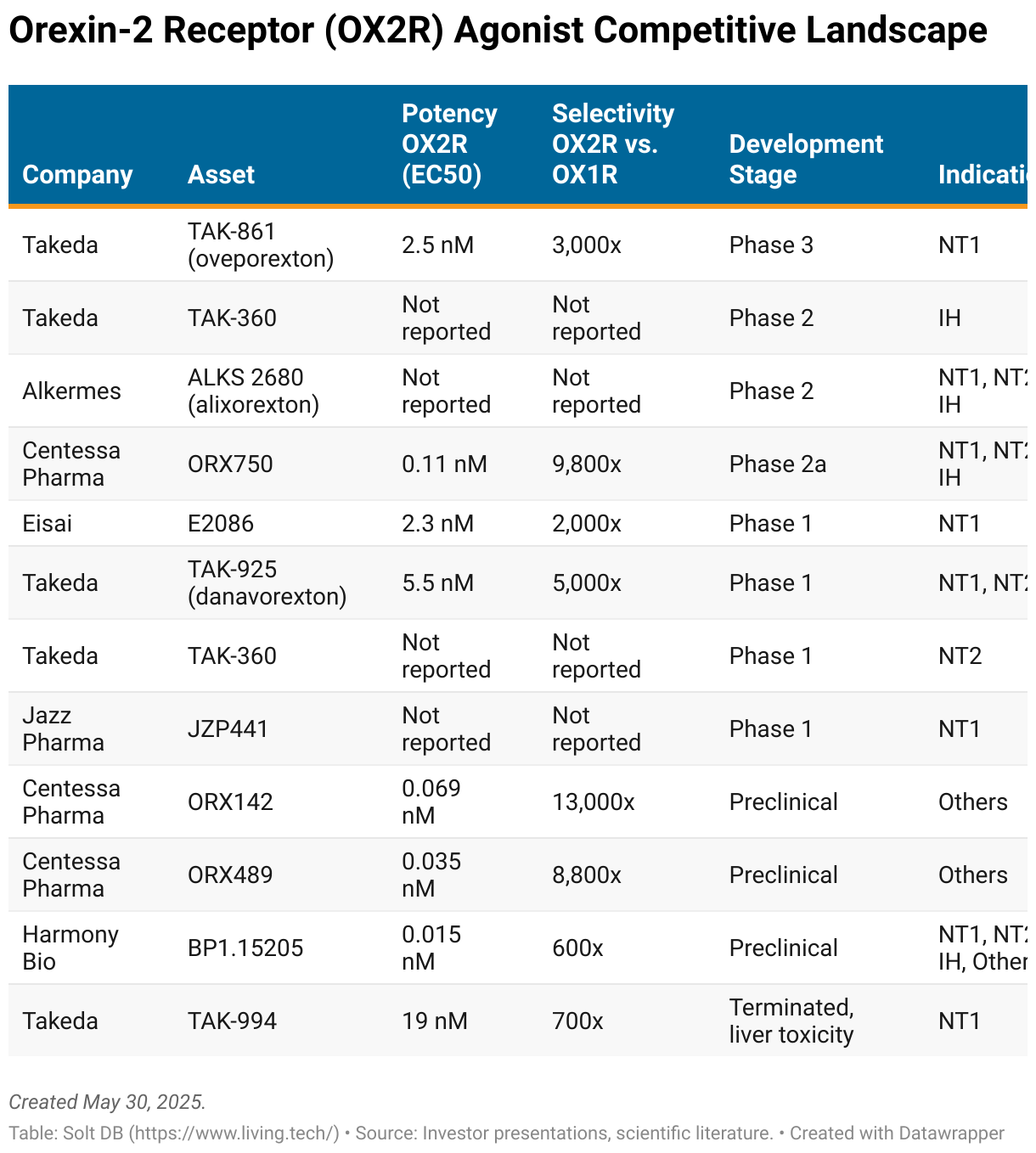

A handful of drug developers are racing to develop OX2R agonists as next-generation treatments for narcolepsy and other psychiatric conditions.

Takeda Pharmaceuticals, Alkermes, and Centessa Pharmaceuticals have each taken a spaghetti-at-the-wall approach. As in, they see the opportunity as so potentially lucrative they're developing multiple assets simultaneously and may whittle down their pipelines later. This might not be a bad strategy, and each has recently stumbled upon at least one promising drug candidate, but it also highlights the immaturity of the science behind and understanding of OX2R agonists.

Eisai, Jazz Pharmaceuticals, and others are all nipping at the opportunity, too. The leading drug candidates in the global industry pipeline have optimized for the highest possible selectivity of OX2R over OX1R, almost to comical levels. Investors might find prior-generation molecules further ahead in clinical studies, but they often have no selectivity, need to be administered intravenously, or need to be administered twice-daily. These will not be commercially competitive – and most probably won't be commercialized at all.

Harmony Biosciences has been comparatively slow to lace up its running shoes. It's years behind the leading competitors, but it's also adopted a starkly different development approach: pipeline-in-a-molecule.

In April 2024, Bioprojet (the inventor of pitolisant) acquired global rights to the OX2R agonist drug candidate BP1.15205 from Tokyo-based conglomerate Teijin. Harmony Biosciences acquired U.S. rights the next day. Let's refer to this asset as '15205 – the zip code of the Pittsburgh International Airport.

The asset originated from the lab of Japanese-American rockstar molecular biologist Dr. Masashi Yanagisawa, who discovered the roles of orexin receptors in narcolepsy. His lab also made discoveries suggesting drug developers shouldn't be so quick to ignore OX1R activation as a target for treating sleep/wake disorders.

As such, '15205 has favorable selectivity for OX2R over OX1R, but far lower than the competitive landscape. The molecule was instead optimized for potency – far higher than the competitive landscape – which means a small amount can go a long way. It's the only drug candidate with a higher potency than the naturally-occurring orexin-A neuropeptide, which could lead to both efficacy advantages and long-term safety concerns for patients who discontinue treatment.

Potency is generally not as important once a drug candidate enters clinical trials because efficacy, pharmacokinetics, and pharmacodynamics end up determining a molecule's clinical profile. But it does provide more dosing flexibility and potentially fewer on-treatment side effects.

That's important for Harmony Biosciences' "pipeline-in-a-molecule" approach. Whereas other drug developers are evaluating multiple molecules across NT1, NT2, and IH; high potency could allow '15205 to be used for all three indications, similar to Wakix. This is a key consideration since orexin receptor agonists will need higher doses to have a clinical impact on NT2 and IH (not directly influenced by orexin-2 receptors) than NT1. This strategy could end up saving hundreds of millions of dollars in development costs, too. Why buy new when you can recycle?

How does Harmony Biosciences stack up? Well, it's still about three years behind the leading drug candidates in the competitive landscape, but should enter the clinic before the end of 2025. That matches the clinical entry of fast followers from Centessa Pharma and Alkermes.

How do these assets really stack up?

The most commercially competitive asset will need to offer:

- once-daily, oral dosing

- high efficacy in restoring wakefulness

- acceptable tolerability and at least match that of Wakix

- avoidance of key treatment-emergent adverse events (TEAE) like liver toxicity and visual disturbances (hallucinations)

- selectivity for OX2R not just over OX1R, but over other off-target receptors

Given the range of potency, selectivity, and dosing convenience among assets in the global industry pipeline, investors can expect some molecules to differentiate themselves and others to fall flat. Case in point: spaghetti-at-the-wall approaches suggest companies don't even seem to know what they should be optimizing for.

It's possible the current industry hypothesis to hyper-optimize OX2R selectivity is wrong or at best flawed, but clinical evidence hints these molecules are hitting the marks on efficacy in short-term studies so far. The emerging tolerability profiles are what investors need to watch carefully. Even with regulatory approvals, undesirable side effects could create headwinds for adoption.

In May 2025, Takeda announced phase 2 results for oveporexton (TAK-861) in NT1. The clinical trial followed 112 patients for eight weeks across four dosing regimens, including three separate twice-daily cohorts and one once-daily cohort. All dose levels were effective in improving wakefulness compared to placebo, although the once-daily dose wasn't as effective.

- Efficacy: The goal of a narcolepsy treatment is to extend sleep latency, or the time it takes to fall asleep. Specifically, the goal is to extend sleep latency to at least 20 minutes, which is the value for healthy adults. Two twice-daily dose levels each led 81% of patients to reach this mark at Week 8 – a solid result.

- Tolerability: All dose levels led to high levels of insomnia, or difficulty falling asleep. It's the opposite problem of narcolepsy. The most effective twice-daily doses led to insomnia in 48% (lower dose) and 57% (higher dose) of patients, respectively. These dose levels of oveporexton also led to increased urinary urgency (48% and 57% of patients, respectively), increased urinary frequency (33% and 30%), and excessive saliva (10% and 26%). Patients were awake and liquids were spewing out.

Takeda says most of the side effects were moderate and temporary. For comparison, the most frequent TEAEs in the pivotal study of Wakix were insomnia (6%), nausea (6%), and anxiety (5%). Wakix is administered once-daily.

Oveporexton has received FDA Breakthrough Therapy designation for the treatment of EDS in NT1. It's the first and only OX2R agonist to reach a phase 3 study, which Takeda expects will read out before the end of 2025. While the asset is only being developed in NT1, the company is developing TAK-360 in NT2 and IH.

Alkermes considers its once-daily OX2R agonist, alixorexton, its prized pipeline asset. Case in point: It will make eight poster presentations at the SLEEP 2025 conference from June 8-11. Alixorexton has also triggered high levels of insomnia, urinary frequency, and excessive saliva, suggesting these are on-target side effects from activating orexin-2 receptors. Investors will see fuller data this month on rates of nausea, dizziness, and decreased appetite from the completed phase 1 study.

Centessa Pharmaceuticals isn't far behind. A phase 2a data readout for its lead drug candidate, ORX750, across NT1, NT2, and IH is expected before the end of 2025. The company is only developing once-daily drug candidates. It has a drug candidate that's even more potent and more selective than ORX750, which is expected to enter the clinic this year.

Harmony Biosciences expects to thrust '15205 into its first phase 1 clinical trial in the second half of 2025. The first data readout is expected in 2026. Preclinical data will be reported at SLEEP 2025 from June 8-11, but investors shouldn't care too much about data from mice and dogs, especially in neuro indications.

The company has also suggested it may study combinations of Wakix and '15205, which could maximize its pipeline-in-a-molecule strategy for its OX2R agonist – or be a complete waste of time. It's too soon to say much.

Phase 3 Data Readout for ZYN002

The single-most important de-risking event of 2025 has nothing to do with Wakix, sleep disorders, or urinary frequency.

The phase 3 data readout for a synthetic cannabidiol gel, ZYN002, as a treatment for social avoidance in individuals with fragile X syndrome is expected in Q3 2025. Wall Street seems to be completely writing off this asset, but the context and nuance suggests a positive surprise might not be so surprising.

To be fair, it's easy to dismiss ZYN002.

For starters, this is actually the second phase 3 clinical trial for ZYN002 in this indication. The first attempt failed, but that's good news for the upcoming data readout.

FXS is a genetic neurodevelopmental disorder characterized by severe learning disabilities, anxiety, and mood disorders. It's caused by chemical modifications (methylation) to the FMR1 gene that reduce production of the FMRP protein. That causes a breakdown in the endocannabinoid system (ECS) in the brain and central nervous system, with cascading effects on cannabinoid receptor 1 (CB1) activity and serotonin, dopamine, and GABA signaling. In other words, a dysregulated ECS affects mood, pain, and sensory perception.

Individuals with FXS are typically categorized into three groups based on the methylation level of the FMR1 gene:

- 100% methylation, also referred to as full or complete methylation

- More than 90% methylation

- Less than 90% methylation

More methylation means more silencing of the FMR1 gene, which typically presents with more severe symptoms. That suggests restoring function of the ECS in the most severe patient population could be a promising treatment approach.

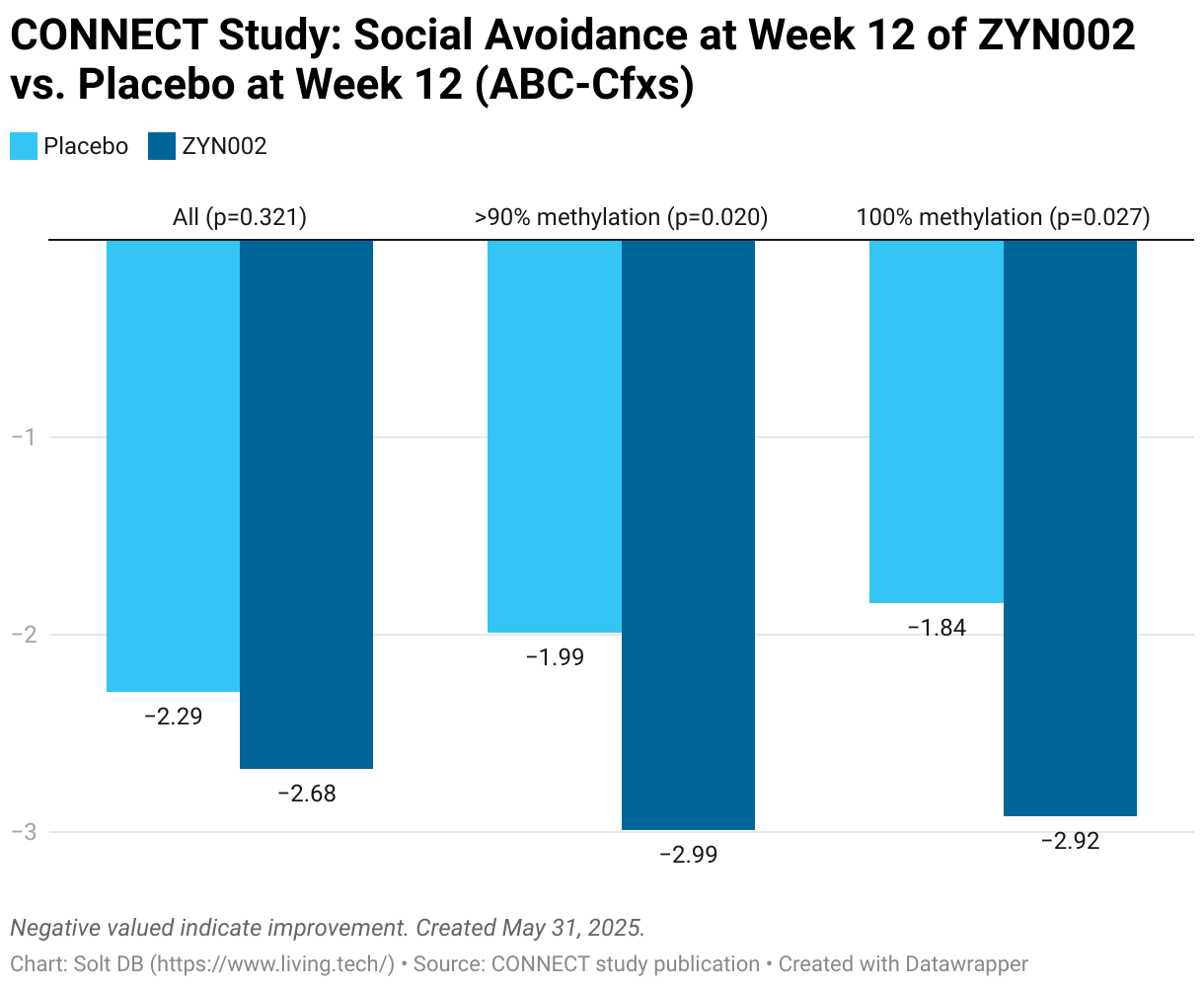

The first phase 3 study of ZYN002, called CONNECT, had a primary endpoint measuring improvements in social avoidance in the full patient population regardless of methylation status. Enrollment included individuals aged 3 to 17 years old. As measured by the Aberrant Behavior Checklist – Community Edition FXS (ABC-Cfxs), the study missed its primary endpoint compared to placebo. It also missed secondary endpoints of improvements in irritability and social interactions in the overall patient population. In fact, it wasn't really even close.

Zynerbra Pharmaceuticals designed the study to also evaluate these endpoints in patients with >90% methylation of the FMR1 gene. In this group, the primary endpoint was met, but the key secondary endpoints were both missed.

It wasn't part of the study design, but the company also evaluated these endpoints in patients with 100% methylation of the FMR1 gene. In this group, all endpoints would've been met.

The current phase 3 study expected to read out in the next few months, called RECONNECT, was designed to replicate these findings from the CONNECT study. The primary endpoint measures improvement in social avoidance in patients with 100% methylation of the FMR1 gene. Secondary endpoints include irritability and social interactions in the same group. The study will also evaluate these three endpoints in individuals with less than full methylation, which aren't expected to be successful, but rather further prove the hypothesis of focusing on complete methylation for ECS rebalancing.

In the CONNECT study, improvements in placebo groups decreased in more severe methylation levels, while improvements in ZYN002 groups increased. That also supports the hypothesis for FMR1 severity being directly influenced by methylation level, as well as the rationale for evaluating treatment effect in individuals with 100% methylation.

The new RECONNECT study was designed with two other important changes.

First, it added a third dose level. That's an important consideration for a medication absorbed through the skin (transdermal gel).

Whereas the CONNECT study evaluated doses of 250 mg or 500 mg per day, the RECONNECT study will also evaluate 750 mg per day in individuals who weigh more than 50 kg (110 pounds).

FXS is much more common and more severe in males, who only inherit a single X chromosome (how the disease got its name). Females have two X chromosomes and are more likely to have at least one functional copy of the FMR1 gene.

The CONNECT study enrolled individuals age 3 to 17 years old. Roughly 74% of individuals enrolled in the CONNECT study were boys, and the average age of a patient was 9.6 years old. The median weight for boys reaches 50 kg by age 12, according to national statistics from the Centers for Disease Control. Finally, over 55% of patients enrolled in CONNECT weighed more than 35 kg (77 pounds).

Adding a higher dose cohort makes sense for the 3 to 17 year-old group, but the RECONNECT study also enrolls adult patients under the age of 30 years old. That makes a higher dose a necessity.

Second, the RECONNECT study was designed to measure differences between treatment and placebo groups for 18 weeks. This is called the blinded period, meaning patients and doctors don't know if they received or prescribed the CBD gel or a placebo. After 18 weeks all patients in the placebo group will be switched to receive ZYN002. This is called the cross-over period. Investors want to see a clear benefit from ZYN002 during the blinded period, and observe clear benefit in patients who cross over from placebo.

The CONNECT study was only blinded for 14 weeks, then switched all patients receiving placebo to ZYN002 for a long-term follow up. However, patients receiving ZYN002 the whole time appeared to show deepening responses beyond this timepoint. Therefore, extending the double-blind portion of the study could make it easier to observe statistically significant benefits during the blinded period.

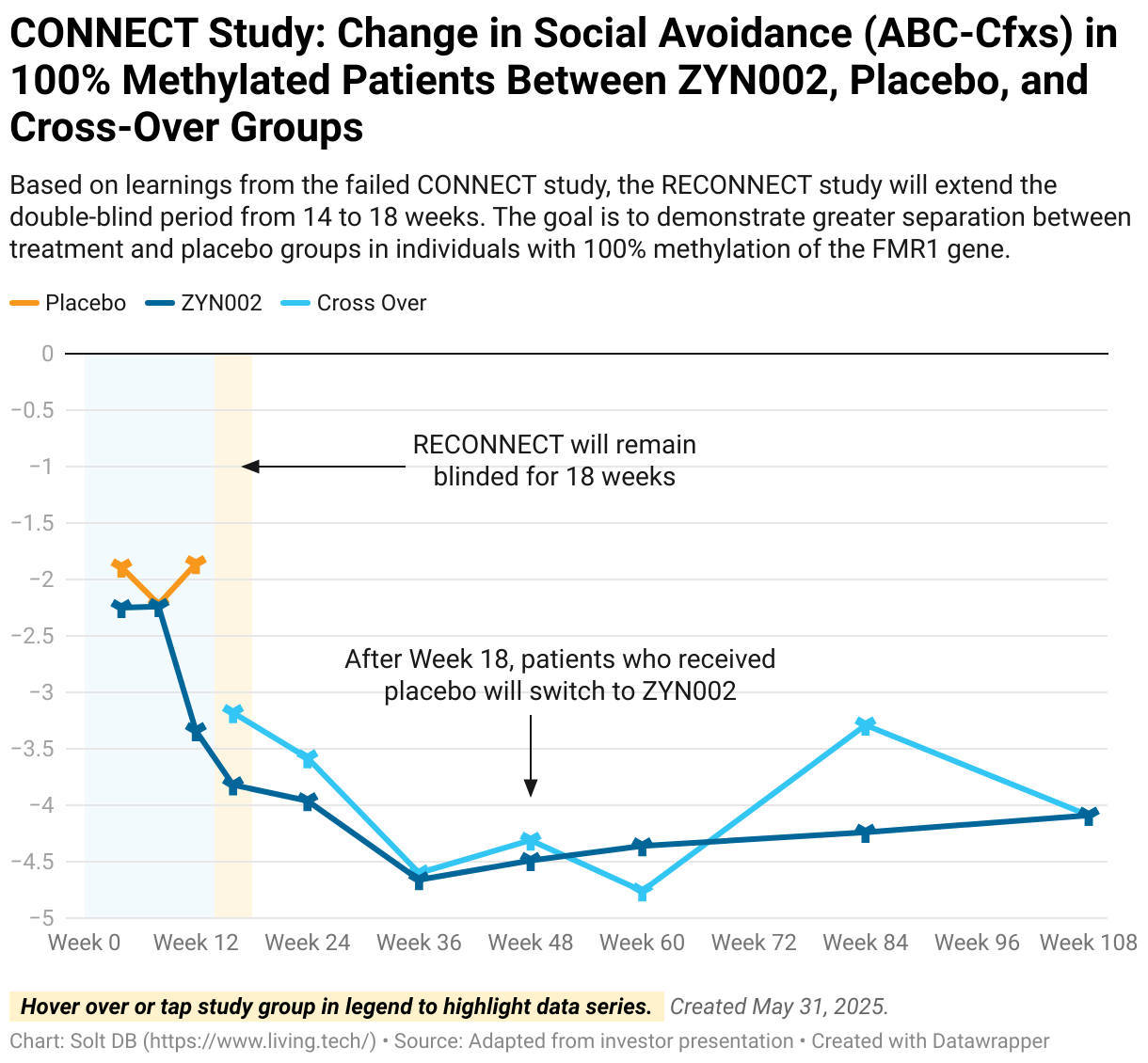

Why is extending the blinded period in the RECONNECT study important? Let's visualize it.

The chart below shows data from the CONNECT study in patients with 100% methylation. The primary endpoint would have been successfully achieved if the study was based on this patient population.

For the behavioral scale used in these studies, negative values mean improvements in social avoidance were observed. Placebo groups in neuro studies often show an improvement, the key is showing a statistically significant benefit beyond that in the treatment group. How would this chart look in a successful RECONNECT study?

- In the chart below, imagine if the placebo group (orange) had a fourth data point at Week 18 that was similar to prior measurements, so in the ballpark of -2.0 to -2.5.

- If patients in the ZYN002 group (dark blue) show deepening responses through Week 18, then the fourth data point would be in the ballpark of -3.0 to -4.0. This would roughly match observations from the CONNECT study and look similar to the chart below.

- If both trends happen in the RECONNECT study, then it would comfortably meet its primary endpoint at Week 18.

- Additionally, investors want to see a clear improvement and convergence in the placebo group during the cross-over period (light blue), similar to the chart below.

Zynerba Pharmaceuticals did a solid job refining the study design for RECONNECT with learnings from the CONNECT study. Nonetheless, drug candidates for neuro indications are notoriously difficult to translate into phase 3 success. In the last decade, only 53% of late-stage neuro studies led to FDA approvals.

Why might the redesigned study still flop?

It's important to remember that all endpoints in the study are subjective. Harmony Biosciences isn't measuring objective tumor volumes from radiographic imaging like in an oncology study; it's asking caregivers to assess improvements through surveys.

Individuals also could be given a confidence boost just by having a gel applied every day for 16 weeks, whether ZYN002 or placebo, and see improvement in symptoms. The placebo effect is significantly more likely to derail neuro studies. Indeed, patients receiving placebo in the CONNECT study also reported improvements across all endpoints.

If the new study succeeds on at least the primary endpoint of improved social avoidance in individuals with 100% methylation, then Harmony Biosciences could be the first company to win regulatory approval for an FXS treatment. This patient population represents an estimated 80% of all individuals with FXS, so it's somewhat counterintuitively the most common genotype. This is likely an artifact in the data though, as more severe genotypes are more likely to be diagnosed.

With that nuance in mind, there are an estimated 64,000 individuals with 100% methylation of the FMR1 gene in the United States, although this estimate includes individuals of all ages. ZYN002 would only be approved in children and adolescents based on the RECONNECT study. It's still a meaningful opportunity.

If the study succeeds, then Harmony Biosciences is prepared to begin a separate phase 3 study in a related disorder called 22q deletion syndrome. It has a similar patient population as FXS. The company may also explore studies in an adult population, but transdermal dosing may not be favorable for individuals with larger body mass (adults).

Rare Epilepsy Franchise and 5HT2 (Serotonin) Agonist

Remember how Axsome Therapeutics repurposed active pharmaceutical ingredients for its leading drug product Auvelity? Harmony Biosciences is doing the same thing for its rare epilepsy pipeline.

Harmony Biosciences acquired Epygenix Therapeutics for two assets, EPX-100 and EPX-200, with potential in Dravet syndrome and Lennox-Gastaut syndrome. EPX-100 is clemizole, which was first marketed as an antihistamine in the 1960s. It was discovered to increase serotonin levels only within the last decade.

These two rare epilepsy indications represent a peak annual sales opportunity of over $1 billion. By the end of 2025, Harmony Biosciences will be actively enrolling patients in a phase 3 study evaluating EPX-100 in each indication. Clemizole has decades of safe use, which reduces development and regulatory risks.

Remember how ZYN002 is a cannabidiol gel? GW Pharmaceuticals earned FDA approval for its oral cannabidiol medication, Epidiolex, as a treatment for Dravet syndrome and Lennox-Gastaut syndrome. It will become a blockbuster drug in 2025.

Remember the table above listing Jazz Pharmaceuticals as one of the many companies developing OX2R agonists? It acquired GW Pharmaceuticals for $7.2 billion in February 2021 – within two weeks of the all-time peak for biotech stocks. Ouch.

That's all a funny way of saying neurological disorders and their competitive landscapes have a lot of overlap. The human brain is less explored than the bottom of the oceans. And until we unravel more of its mysteries, simple treatments can often have surprisingly profound effects.

Forecast & Modeling Insights

(Introduced.)

My current model is based on properly valuing the underlying business, assuming no threat from generic competition to Wakix, and a risk-adjusted contribution from ZYN002. This is a conservative model focused on near-term de-risking events.

The rest of the pipeline, from new formulations of pitolisant to the late-stage rare epilepsy franchise, make no contribution yet. Assets will make more or less contributions as data accumulates in the next 18 months, or by the end of 2026.

Harmony Biosciences has a modeled fair valuation of $3.803 billion or $65.24 per share.

The current model makes the following assumptions about key operating metrics:

- Full-year 2025 revenue of $837.233 million, compared to $840 million at the midpoint of guidance.

- Full-year 2025 operating expenses of $409.994 million, marking an increase of 12% from the year-ago period. The comparison from Q1 2025 vs. Q1 2024 is a bit misleading as the beginning of 2024 marked a temporary dip in between study starts.

- Full-year 2025 net income of $173.772 million or GAAP earnings per share (EPS) of $2.98. The year-end outstanding share count is expected to be 58.286 million, assuming no purchases under the active share repurchase program. This does not account for one-time charges, adjustments, or acquisitions.

The RECONNECT study is modeled with a roughly 62% probability of success, defined as a positive outcome in Q3 2025 and earning FDA approval in the second half of 2026. The asset ZYN002 contributes $210.8 million to the valuation.

If the RECONNECT study fails, then investors can expect the valuation to decrease significantly. For example, a valuation of $1.5 billion would be equivalent to $25.86 per share.

Harmony Biosciences would be expected to repurchase up to $150 million in shares – the full amount remaining under its active share buyback program – which would cancel 10% of the shares outstanding at this valuation level. That provides a rare backstop against a failed outcome.

In the example above, the company could repurchase roughly 5.8 million shares. If the business eventually regained its current valuation based on the profitability enabled by Wakix, then it would be valued at $2 billion or $38.74 per share. That provides an additional cushion to exit positions with roughly neutral returns.

Margin of Safety & Allocation

Harmony Biosciences is considered a Growth (Speculative) position. The current fair valuation for the business based on my 2025 model is below:

- Market close May 30: $34.50 per share

- Modeled Fair Valuation: $65.24 per share

- Allocation Range: Up to 5%

Harmony Biosciences reported 57.424 million shares outstanding as of May 2, 2025. The modeled fair valuation above assumes 58.286 million shares outstanding, which is equivalent to a 1.5% increase by the end of 2025.

Further Reading

- May 2025 press release announcing Q1 2025 operating results

- May 2025 regulatory filing (10-Q) detailing Q1 2024 operating results

- May 2025 Finch Trade of Harmony Biosciences ($30.00 per share)

- April 2025 research note (Members Digest) previewing Q1 2025 earnings across the coverage ecosystem

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)