.svg)

What's in a name? My parents couldn't spell, so perhaps I'm not the best one to answer that.

But Harmony Biosciences has been thinking about this question.

It filed for two new trademarks for potential drug brands – Anbilsa and Solzy – on August 19, 2025. It's common for drug developers to file a handful of trademark claims for potential drug brands as part of commercial launch readiness, then whittle the list down to one.

If the pivotal RECONNECT study in Fragile X Syndrome (FXS) succeeds, then ZYN002 might launch in 2026 as one of those brands. The Finch is pulling for Solzy. If the pivotal RECONNECT study fails, then there's no need to follow through with the trademark filings.

Win or lose – what happens next?

The data readout will trigger additional up-risking and de-risking scenarios, some that are concrete and some that depend on the clarity of the data. Understanding the possibilities ahead of time can help reduce emotional decisions during what's expected to be a volatile day and potentially improve your returns. Let's conduct a little scenario analysis and review my game plan.

I don't expect to exit my position on the day of the data readout under any scenarios.

Will RECONNECT Succeed or Fail?

I think the risk/reward is lopsided in favor of reward. Remember:

- Harmony Biosciences isn't a precommercial drug developer. The company's fate doesn't rest on this data readout. It expects to generate full-year 2025 revenue of $840 million, while I model net income of $178.836 million and operating cash flow of over $250 million.

- The business has a valuation of $2.1 billion, which represents a price-to-earnings (PE) ratio of 12x based on my model. In other words, Harmony Biosciences is undervalued without any contribution from ZYN002.

- The business has $150 million remaining on its share repurchase program. It would likely deploy that to cushion any negative movement in the stock should the data readout disappoint.

An absence of valuation risk is nice, but the pivotal RECONNECT study could still fail or underwhelm.

The primary endpoint is improvement in social avoidance measured by a special scaling system. However, it's based on the responses of caregivers, meaning it's pretty subjective. A significant share of caregivers of individuals who received placebo will swear that treatment worked. This is why neuro studies often fail because "placebo performed better than expected."

Investors know ZYN002 works. We can be confident that ZYN002 works in enough patients to be commercially relevant. Consider that the open-label extension (OLE) study followed individuals for three years starting from the beginning of the CONNECT study.

- When patients were randomized to receive the drug candidate or placebo, the share of patients with complete methylation of the FMR1 gene rated as achieving a clinically meaningful improvement in social avoidance was 56% vs. 37%, respectively. This is the patient population and primary endpoint of the pivotal RECONNECT study.

- Patients who received placebo switched to ZYN002 after 14 weeks. By the three-year checkup, over 72% of all individuals responded to treatment – including individuals without complete methylation.

- The OLE had a discontinuation rate of just 3.3% over three years. By comparison, the quit rate for GLP-1 drugs exceeds 40% after just one year.

Harmony Biosciences thinks it can treat up to 25,000 individuals of the estimated 80,000 patients with FXS in the United States, and be the only treatment on the market. By comparison, Wakix generates $840 million in annual revenue by treating 7,600 patients. It has to share the narcolepsy market with four major competitors – and that's before orexin-2 receptor (OX2R) agonists arrive – which exerts downward pressure on selling prices.

My model is more conservative because it excludes the adult patient population. I only expect an FDA approval in patients up to 18 years old.

The pivotal RECONNECT study includes patients up to 30 years old. Will that be enough to snag a broader approval for adults of any age? Or maybe up to 55 years old, a common regulatory definition of "adults"? Harmony Biosciences is at least preparing for a broader approval. It has quietly begun enrolling a small safety study to evaluate drug-drug interactions (DDI) in adult patients, which cannot be ethically completed in children. The study could wrap up by November, which would support a full regulatory filing in late 2025 or early 2026.

If the data readout from the pivotal study suggests regulators will support a broader approval in adult patients, or management clearly states as much, then my model would be significantly undervaluing ZYN002. My model's fair value would climb to roughly $115 per share.

Of course, the question is not if ZYN002 works. The question is if ZYN002 works in the first 18 weeks of the pivotal RECONNECT study. That's defined as significantly outperforming placebo even if it "performed better than expected."

I'm confident enough to have invested almost 44% of all Finch Trades principal into the position. I'm also confident enough to test some new options strategies, although those aren't part of Finch Trades.

What Happens If RECONNECT Fails?

Shares would likely fall by double digits if the pivotal RECONNECT study disappoints. A drop of 30% or more from current levels near $37 per share wouldn't be surprising.

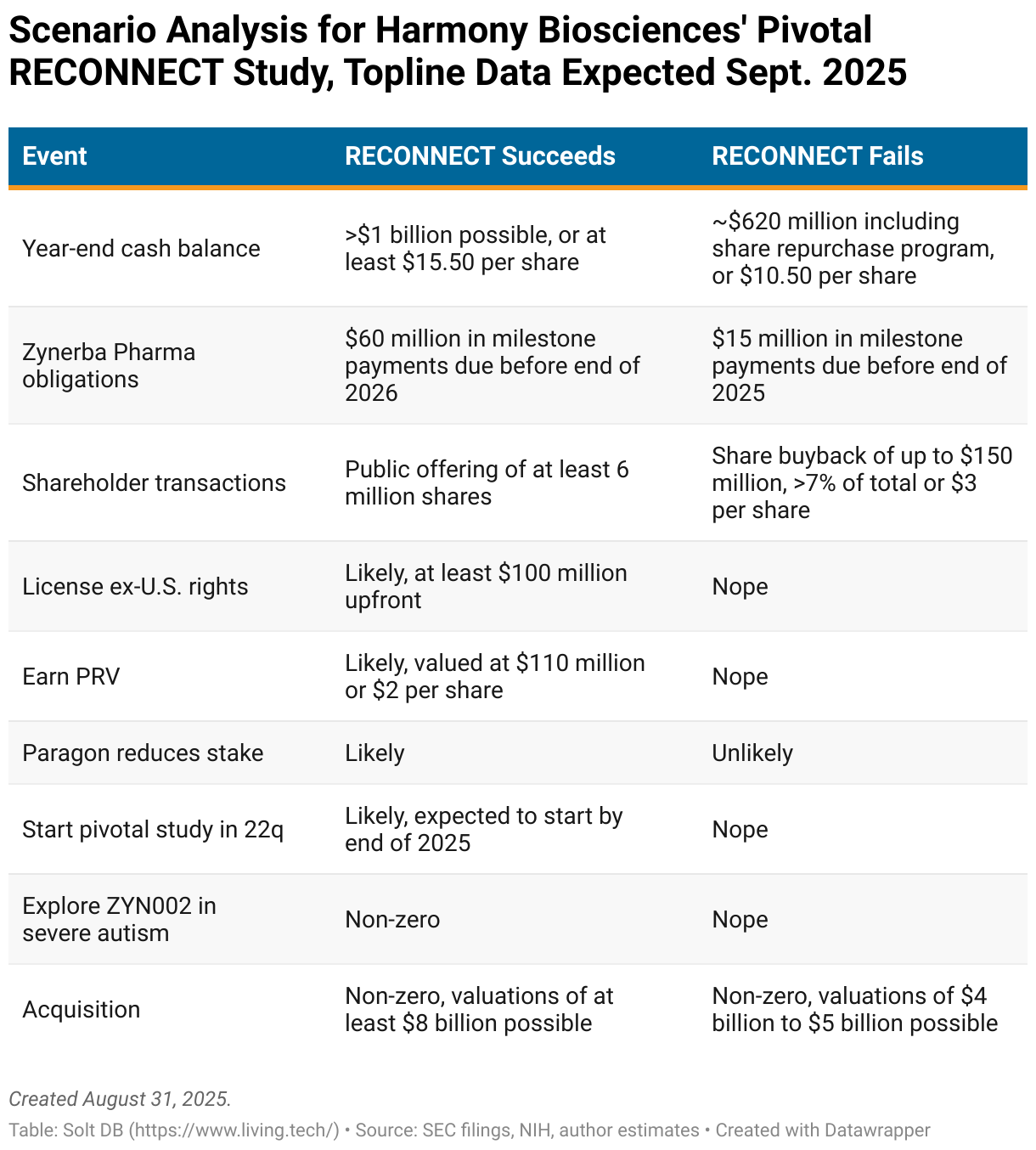

A few known and likely events would be triggered on a failed outcome. I've listed them below with the nearest events first.

(Certain) Zynerba Pharmaceuticals obligations

Harmony Biosciences must pay a $15 million milestone to Zynerba Pharmaceuticals for completing the RECONNECT study.

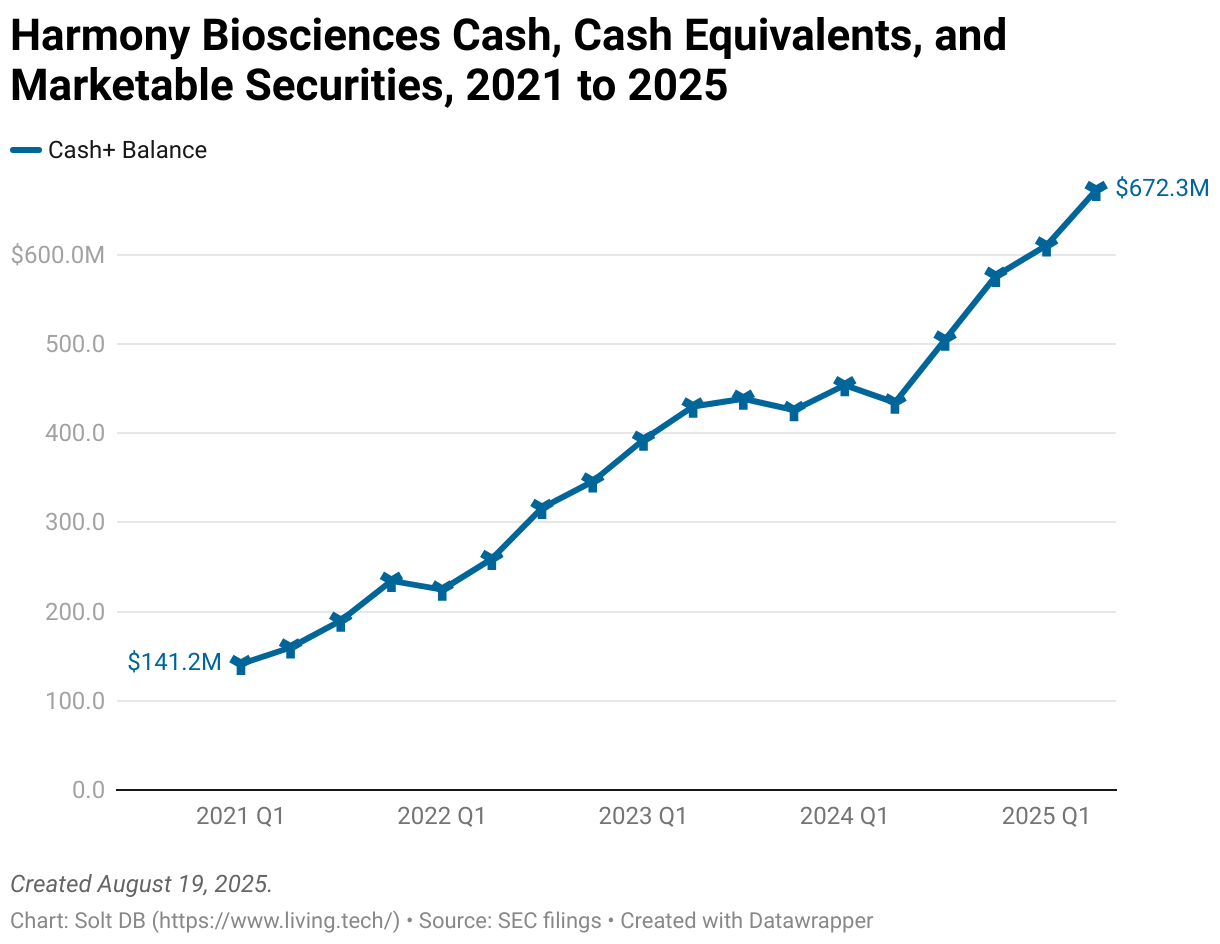

It ended June 2025 with $672 million in cash and should end the year with at least $770 million including this milestone payment, or at least $620 million including a potential share repurchase transaction.

(Likely) Deploy remaining $150 million in buyback program

If the pivotal RECONNECT study fails or underwhelms, then management would likely buy back shares.

A company's board of directors must authorize a share repurchase program. Luckily, Harmony Biosciences has $150 million remaining on an active buyback scheme, so there wouldn't be a delay. It could repurchase a whopping 7% of all outstanding shares at the current valuation, so maybe closer to 10% should the valuation slide on a failed study. That's a "free" $3 per share of insurance.

Considering the business is undervalued, it would arguably be a great investment for the company. In addition, the business will generate almost exactly $150 million in cash from operations in the second half of 2025 alone.

The case against a share buyback is that it would reduce the float, or the number of readily-available shares, for an already low-float stock.

(Certain) Pressure ratchets up on next source of growth

Harmony Biosciences is undervalued without ZYN002, but you know… it still had better hurry the f*nch up and diversify revenue from Wakix.

The blow would be cushioned by having four other pivotal studies ongoing across the pipeline. Though pillows only cushion falls from a certain height. What if the next-gen formulation of Wakix is rejected by the FDA next year? Or the two studies for EPX-100 in rare epilepsy fail? Or Wakix stumbles in helping kids with Prader-Willi Syndrome reduce the most common untreated symptom?

Drug developers in this position need to score an immediate win in their quest for revenue diversification. String together too many misses at the start – and the most painful misses of all: late-stage studies – and things can get ugly for investors. For homework, check out the 10-year stock chart for Incyte Corporation.

Not before bed.

(Non-zero) Harmony Biosciences is acquired

Management could throw its hands in the air and decide to sell the company – even after a disappointing data readout. The economics would be worse than if the study succeeded, but could still be meaningful.

A valuation in the ballpark of $4 billion, or near $61.50 per share on a fully-diluted basis, wouldn't be unreasonable. That would represent less than 5x sales, while the business should end the year with at least $10.50 per share in cash.

Ol' Maxxie's game plan for a failed study

If the pivotal RECONNECT study has a disappointing data readout, then I would expect to hold my position through at least the third-quarter 2025 earnings conference call in November.

That would allow enough time for shares to recover and other events to be triggered (namely the share buyback). It would also provide an opportunity to remind investors of the strength of the underlying business without forcing it or sounding desperate.

What Happens If RECONNECT Succeeds?

Shares would likely increase by double digits if the pivotal RECONNECT study succeeds. Given the lowly valuation, relatively high short interest in the stock, and wide-open commercial opportunity in FXS; no-doubter results could drive shares to triple-digit percentage gains in the days following the announcement. If data are good enough, then don't be surprised if Harmony Biosciences is trading over $100 per share.

A few known and likely events would be triggered on a positive outcome. I've listed them below with the nearest events first.

(Certain) Zynerba Pharmaceuticals obligations

Harmony Biosciences must pay a $15 million milestone to Zynerba Pharmaceuticals for completing the RECONNECT study. It must pay another $10 million for a positive data readout. If the asset earns FDA approval in 2026, then the company must pay another $35 million. That's $60 million total in development and regulatory milestones by the end of 2026.

The business ended June 2025 with $672 million in cash and should end the year with roughly $782 million, including the first $25 million in milestone payments. That excludes both a potential share repurchase program (not expected to occur if the data readout is positive) and a public offering of common stock. Other expenses are tucked into the math in this scenario, including preparing the next pivotal study for ZYN002 and commercial readiness activities.

(Likely) A "Don't-Get-Cute" share offering

If the pivotal RECONNECT study is positive, then the company could easily raise at least $250 million from a public offering. Why not ring the cash register?

Don't forget, the management team has been executing a buy-and-build strategy since Harmony Biosciences was founded. Wakix, ZYN002, and every other asset was acquired – for relatively small sums of money. How dangerous could the management team be if it suddenly had a $1 billion war chest?

Ending the year with over $1 billion in cash could allow management to adopt an aggressive stance. The company might acquire a commercially-ready or revenue-generating product from a down-on-its-luck peer, which is something management has recently hinted at in public remarks. Harmony Biosciences could swing from one commercial drug product today to three by the end of 2026, including Wakix, Anbilsa/Solzy, and a potentially acquired asset.

In fact, Anbilsa might be a trademark for an unknown, commercially-ready asset that isn't ZYN002.

(Likely) Paragon Biosciences reduces its stake

Harmony Biosciences might not be the only one ringing the cash register. Paragon Biosciences, the fund that founded the drug developer, would likely want to cash in, too.

Paragon is facing the same struggles as every other investment fund in biotech: a lack of liquidity. Investments made in prior years, usually at higher valuations, are now locked up in struggling biotechs with generally lower valuations. This dynamic has frozen funds across the landscape, which exist to recycle capital for more productive uses at a regular cadence. That's been nearly impossible outside a handful of exceptions (usually much larger funds) during the biotech winter.

Investors and trusts associated with Paragon own a whopping 12.7 million shares, or 22%, of Harmony Biosciences. And that's after selling 1.2 million shares in October 2024.

Drug developers with large, single investors can sometimes struggle with a low float. Harmony Biosciences only has 58 million shares outstanding, so Paragon locking up 12.7 million shares is the biggest reason for the stock's relatively low liquidity. If Paragon reduced its stake, then it would sell existing shares to other investors. That would increase the float without dilution, improving liquidity and pricing for shareholders.

(Likely) License ex-U.S. rights

The pivotal RECONNECT study was designed to support approvals in all 28 European Union member countries. However, from a historical perspective, it probably doesn't make sense for Harmony Biosciences to retain international rights to ZYN002. The company would need to build commercial infrastructure in Europe for the first time, which would be relatively expensive.

The term "historical perspective" is doing some heavy lifting there.

If the United States federal government pressures drug developers to raise prices in international markets and/or lower them at home, then the laughably easy decision of owning U.S. rights and selling ex-U.S. rights might not be so simple.

It might make sense for drug developers to own global rights to certain assets in the near future. That could force investors to accept higher capital expenditures in the immediate aftermath of launch required to build out international commercial infrastructure. For Harmony Biosciences and ZYN002, a big, fat capital raise could make the price tag a bit easier to stomach, should it pursue global ambitions.

Although I think investors need to be open-minded as to how drug development economics will or could change in the next decade, the most likely scenario involves selling international rights to ZYN002. The upfront payment and all development, regulatory, and commercial milestones would be data dependent. An upfront payment could be at least $100 million and potentially a few multiples of that.

(Likely) Start a pivotal study in 22q deletion syndrome

If the pivotal RECONNECT study delivers a positive outcome in FXS, then Harmony Biosciences expects to initiate a separate pivotal study in 22q deletion syndrome (22q). The mechanism of action and clinical hypothesis are exactly the same.

The size of the patient population is nearly identical, too. That could double the size of the treatable U.S. patient population from 25,000 patients in FXS alone to 50,000 patients in both. There are no approved treatments for either condition.

This is also why no-doubter data in the pivotal RECONNECT study are much more valuable than merely good-enough data. Analysts would be forced to price in the value of ZYN002 in FXS, which isn't priced in at all heading into the data readout, and also account for the potentially buttery-smooth regulatory path and commercial opportunity in 22q.

A pivotal study in 22q wouldn't take very long to complete, especially if regulators are on board with a streamlined study design. ZYN002 wouldn't need to gather additional long-term safety or efficacy data, while a crossover period (switching patients on placebo to active treatment after Week 18) could be shorter.

Harmony Biosciences could have topline data available in 22q in summer 2027 and earn approval in early 2028. Whether or not you plan on maintaining a position that long, the commercial opportunity (assuming no-doubter data from RECONNECT) could make an acquisition more likely in the near term.

(Non-zero) Explore potential in broader autism populations

For patients with FXS who have complete methylation of the FMR1 gene, ZYN002 works by restoring balance in the endocannabinoid system (ECS). Individuals with severe autism don't necessarily have a mutated FMR1 gene, but cannabidiol isn't a genetic medicine, so the specific genes aren't important. What matters is that behavioral symptoms in certain autism populations are also caused by an imbalanced ECS.

Depending on the strength of the data from the pivotal RECONNECT study, Harmony Biosciences may ponder whether there's an additional opportunity to use ZYN002 in certain autism populations.

I think autism is over-diagnosed at a rate of 3% of children, but over 1 million individuals in the United States have severe autism. The company could probably design a study with several cohorts categorized by specific groups of mutations. ZYN002 wouldn't work in all patients with severe autism, but it could work in enough to greatly expand the 50,000-patient opportunity in FXS and 22q.

This could proceed in several different ways, from announcing exploratory research, the possibility of a clinical trial, or partnering U.S. rights in severe autism to de-risk development.

To be clear, this is a very unlikely scenario, but not impossible. If it does occur though, then Harmony Biosciences could become a meme stock – defined as briefly absurd valuations far detached from reality.

(Certain*) Harmony Biosciences earns a priority review voucher

If ZYN002 earns FDA approval* in pediatric patients, then Harmony Biosciences would earn a priority review voucher (PRV).

A PRV can be slapped down on top of a regulatory submission to reduce the review period from 10 months to 6 months. It can also be sold to another drug developer; the going rate recently has exceeded $110 million. Although this cash wouldn't be realized until the PRV is sold in 2026, investors can pencil in the $2 per share value it represents.

Harmony Biosciences doesn't need the cash, but drug developers outside the top 20 rarely keep PRVs. It might make sense to hang onto one to accelerate another internal asset, like the company's own OX2R agonist, but that's years away from being submitted – if it's submitted at all. Besides, the company can earn a second PRV if Wakix is approved in children with Prader-Willi Syndrome in 2027.

Additionally, the FDA is making smart changes to accelerate review periods. That could sharply reduce the value of PRVs in the near future, so selling it next year would be prudent.

(Non-zero) Harmony Biosciences is acquired

A positive data readout could immediately catapult the business to the front of the line for high-value acquisition candidates. Harmony Biosciences could end September 2025 with:

- Two potential blockbuster franchises. That includes Wakix, which is almost ready to shed the "potential" qualifier with $840 million in revenue this year.

- Reduced pressure on and concern about the competitive positioning of Wakix. ZYN002 could more than offset potential weakness for the flagship franchise.

- Over $1 billion in cash.

- Four phase 3 clinical trials underway, which could grow to six by the end of the year once the pivotal studies for ZYN002 in 22q and Wakix HD in sleep disorders kick off.

What could Harmony Biosciences be worth in an acquisition following a positive data readout?

It depends on the strength of the data for ZYN002, the performance in adult patients (for which there are no historical data), whether there's a public offering of common stock, and how much value is unlocked by reducing pressure on Wakix.

For ballpark thresholds:

- Precommercial drug developers with a single submission-ready asset with blockbuster potential can be acquired for $4 billion or more.

- Commercial drug developers with $400 million to $600 million in annual revenue, a path to profitability or cash flow generation, and visibility into a moderately long growth runway can be acquired for $8 billion or more.

Harmony Biosciences is a commercial drug developer expecting $840 million in annual revenue, while I model next income of over $178 million and cash flow of over $250 million. Perhaps the value of Wakix would get dinged in an acquisition due to the looming loss of exclusivity in 2030 or the new competitive threats from OX2R agonists. Takeda's oveporexton is expected to earn approval and launch in 2026.

But a potential acquisition following a positive data readout from the pivotal RECONNECT study would likely be over $8 billion.

The company has roughly 58 million shares outstanding today, plus another 7 million shares in restricted stock units or employee stock options that would need to be issued in an acquisition. To be the most conservative, assume the company conducts a public offering of common stock that adds 10 million shares to the outstanding count. That results in 75 million shares outstanding (58 million + 7 million + 10 million).

An acquisition for $8 billion would be equivalent to $106 per share.

As for timing, an acquisition could occur as soon as the end of 2025.

Ol' Maxxie's game plan for a successful study

If the pivotal RECONNECT study has a positive data readout, then I have some options. I don't expect to exit my position on the day of the data readout under any scenarios.

How long will I maintain a position? It depends.

As explained in a members-only Discord thread from early April 2025, my plan is to hop, skip, and jump from Harmony Biosciences to Coherus Oncology to Relay Therapeutics in the next couple of years. I don't think it matters much if I move the capital from this position into Coherus in September or October, or heck even December.

It might make sense to hold my position through at least the third-quarter 2025 earnings conference call in November, especially since Harmony Biosciences will report before Coherus. There aren't any known de-risking events for Coherus expected before data readouts start rolling in next year, although management has strongly hinted at additional toripalimab clinical licensing deals and possibly licensing deals for other assets before the end of 2025.

News Flow & Modeling Insights

(No change, but below I've shared more details than in the past.)

My current model is based on properly valuing the underlying business, assuming no threat from generic competition to Wakix, and a risk-adjusted contribution from ZYN002. This is a conservative model focused on near-term de-risking events.

The rest of the pipeline, from new formulations of pitolisant to the late-stage rare epilepsy franchise, make no contribution yet. Assets will make more or less contributions as data accumulates in the next 18 months, or by the end of 2026.

Harmony Biosciences has a modeled fair valuation of $3.953 billion or $67.69 per share.

The current model makes the following assumptions about key operating metrics:

- Full-year 2025 revenue of $835.222 million, compared to $840 million at the midpoint of guidance.

- Full-year 2025 operating expenses of $431.150 million, marking an increase of 17.5% from the year-ago period.

- Full-year 2025 net income of $178.836 million or GAAP earnings per share (EPS) of $3.10. The year-end outstanding share count is expected to be 58.396 million, which excludes transactions under the share repurchase program or a potential public offering of common stock. This does not account for one-time charges, adjustments, or acquisitions.

The pivotal RECONNECT study is modeled with a roughly 62% probability of success, defined as a positive outcome in Q3 2025 and earning FDA approval in the second half of 2026. The asset ZYN002 contributes $210.8 million to the valuation.

My current model only accounts for a pediatric label. That's defined as earning an approval in FXS patients up to 18 years old.

The pivotal RECONNECT study enrolled adult patients up to 30 years old. If that patient population responds to treatment and ZYN002 can earn approval in a broader patient population age range, then my model would change significantly.

- The current model values Harmony Biosciences at $3.953 billion or $67.69 per share.

- If the current model included adult patients up to age 55 years old, then Harmony Biosciences would have a pre-data readout fair value of $4.796 billion or $82.13 per share.

- If the data readout is positive and a broad label in adult patients is possible, then the modeled fair value – including a public offering of 6 million shares – would be $7.456 billion or $115.79 per share.

- If the data readout disappoints, then the modeled fair value – excluding ZYN002 – would be $3.742 billion or $64.08 per share.

Acquisitions often occur well above the intrinsic value for commercial drug developers and/or commercially-ready high-impact assets.

Margin of Safety & Conviction

Harmony Biosciences is considered a Current Compounder position with the following Conviction rating.

- 1 = High

- 2 = Above Average

- 3 = Average

- 4 = Below Average

The estimated fair valuation based on my current model is below:

- Market close August 29: $36.89 per share

- Modeled Fair Valuation: $67.69 per share

- Allocation Range: Up to 5%

Harmony Biosciences reported 57.533 million shares outstanding as of August 1, 2025. The modeled fair valuation above assumes 58.396 million shares outstanding, which is equivalent to 1.5% dilution.

Further Reading

- August 2025 research note analyzing Q2 2025 operating results

- August 2025 press release announcing Q2 2025 operating results

- August 2025 regulatory filing (10-Q) detailing Q2 2025 operating results

- June 2025 research note analyzing the commercial strength of Wakix in the context of the narcolepsy competitive landscape

- June 2025 research note introducing coverage of Harmony Biosciences

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)