.svg)

Profits are the single-biggest driver of investing returns, which presumably bodes well for a recovery in shares in Harmony Biosciences. It trades at less than 10x earnings in a market that's historically expensive.

But the ability to earn future profits is what matters most.

An unprofitable company can trade at a premium valuation if investors are confident it can become profitable, while a healthy business can lag behind if the durability of profit engines is in doubt. Unfortunately, Harmony Biosciences is struggling to convince Wall Street that it has strong future earnings potential.

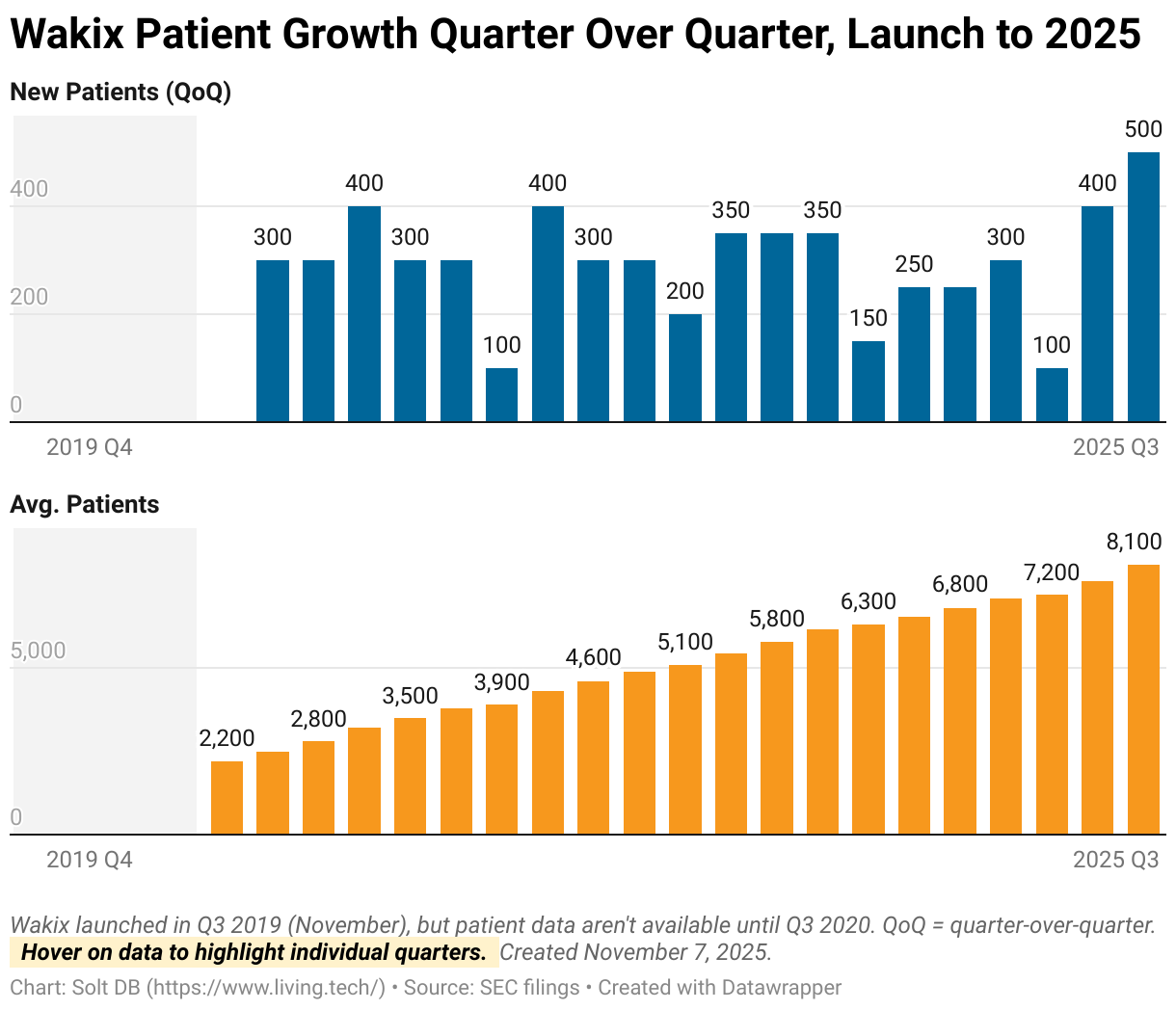

On the one hand, Wakix has surprising momentum in its sixth year on the market. The narcolepsy treatment has added roughly 900 net patients in the last two quarters – a record. The brand remains the only source of consistent growth in a competitive landscape that boasts three different mechanisms of action. Wakix ended September 2025 with 8,100 patients on treatment, which is less than 10% of the total diagnosed patients in the United States. Most patients aren't on any treatment.

On the other hand, Wall Street analysts are concerned about the upcoming arrival of orexin-2 receptor (OX2R) agonists in the back half of 2026. Takeda's oveporexton is expected to earn FDA approval and launch in adult patients with narcolepsy type 1 (NT1), which comprises roughly one-third of current Wakix prescriptions. There's also the threat of generic competition looming in 2030.

What should investors make of all this?

I think both things are true. Wakix won't become obsolete when oveporexton launches in NT1, but it won't add new prescriptions as easily. As a blunt reminder, Wakix isn't even the best-selling narcolepsy treatment in the competitive landscape right now, but that hasn't stopped its commercial rise. Competition is synonymous with drug development, especially in meaningful commercial opportunities. Investors tend to overestimate its impact in more dynamic landscapes, like narcolepsy.

Importantly, most patients diagnosed with narcolepsy aren't receiving any treatment at all. At the end of September 2025, Xywav/Xyrem counted 10,725 patients and Lumryz counted 3,400 patients. Throw in Wakix and the three leading treatments accounted for 22,225 of the estimated 100,000 diagnosed patients with NT1 or NT2. Treatment coverage is actually even lower considering patients on Xywav or Lumryz (or oveporexton) can take Wakix simultaneously, so the numbers are double-counting some patients.

Still, it sure would be nice for Harmony Biosciences to diversify its revenue base to alleviate concerns about shifting competitive dynamics. The high-profile failure of ZYN002 in fragile X syndrome leaves investors with few near-term options, although management is working on acquiring new assets. Will that be enough to unlock value?

By the Numbers

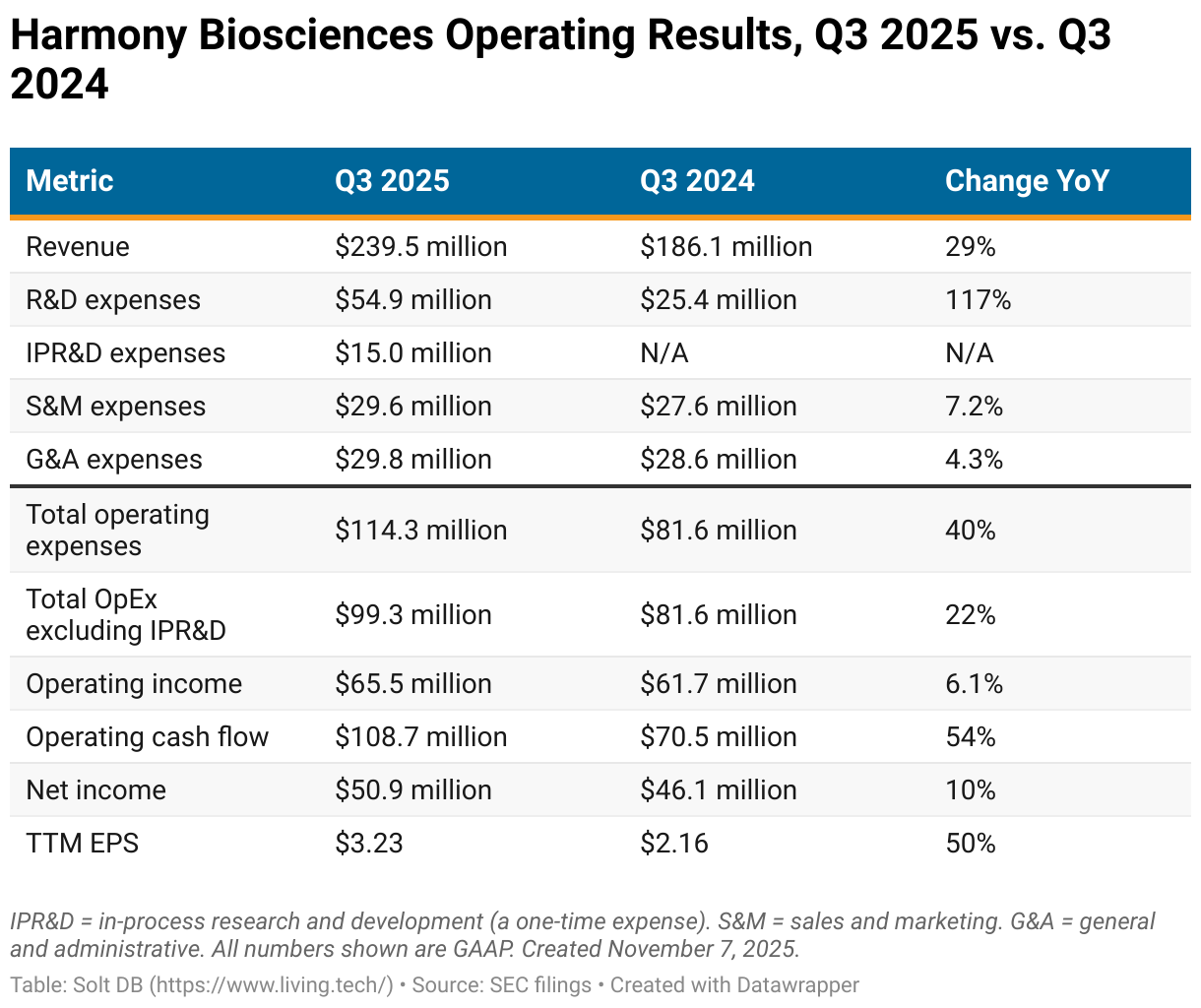

Harmony Biosciences reported an unusually strong quarterly performance for Wakix with both new patient additions and revenue growth. As the kids would say, that's hella convenient timing.

After adding 400 patients in the second quarter, Wakix added a record 500 patients in the third quarter. The prior high watermark for a six-month period was just 700 patients added. That drove a $39 million increase in revenue quarter over quarter, by far the highest ever. The business had only added more than $18.2 million in subsequent quarters one other time since the narcolepsy drug launched in 2019.

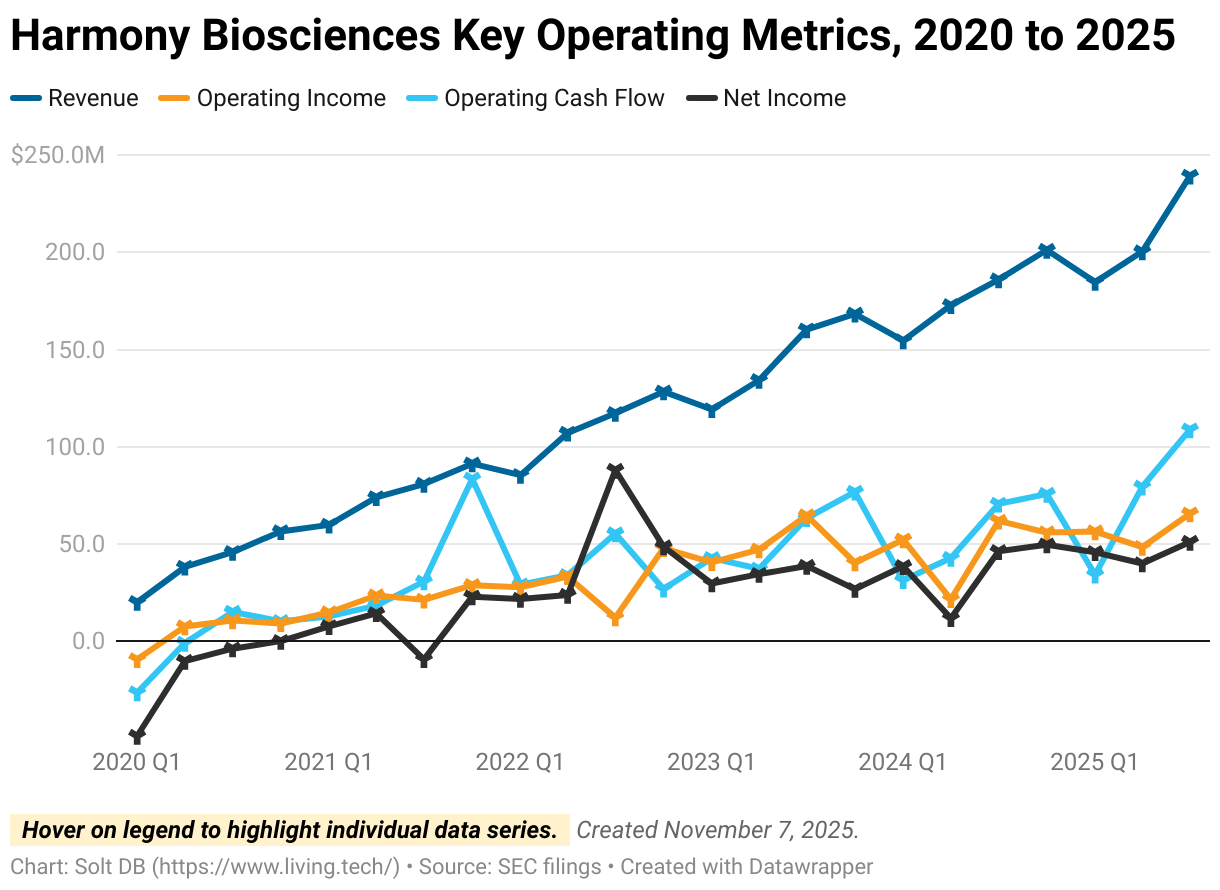

A surging topline lifted all other metrics further down the income statement and cash flow statements. Harmony Biosciences reported $65.5 million in operating income, a record $108.7 million in operating cash flow, and its first-ever $50 million quarter in net income.

Strong cash flow and profitability bode well for the business. These metrics will be the most likely reason shares steadily rise in value in the foreseeable future – even without additional commercial updates.

In the last 12 months, Harmony Biosciences has generated a staggering $297.6 million in operating cash flow and GAAP earnings per share (EPS) of $3.23. Profitability has steadily scaled with Wakix's commercial dominance and should continue to expand.

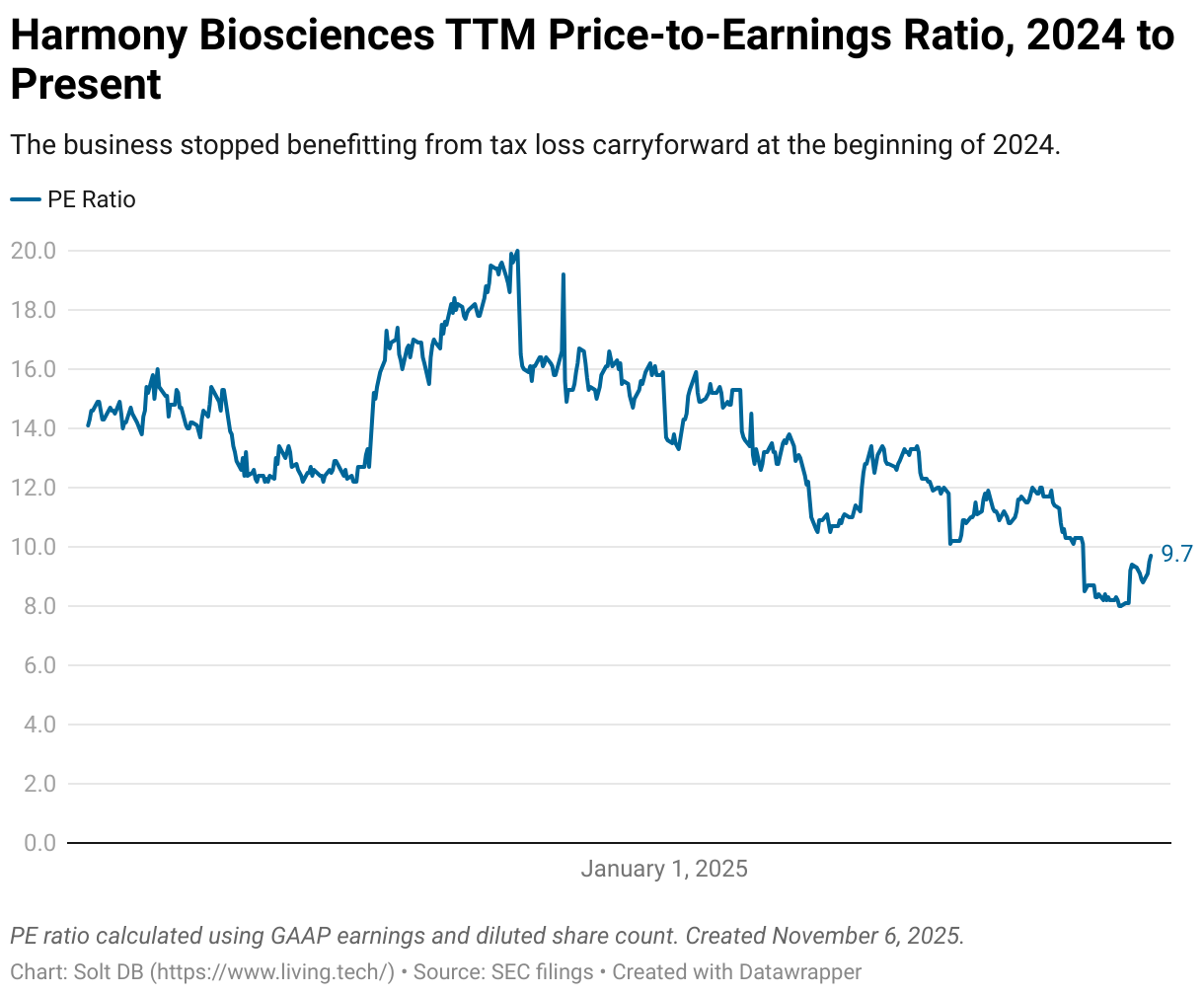

Consider the trajectory of GAAP EPS since summer 2023, which is the first period that excludes favorable tax benefits. The business was able to benefit from historical losses in the early years of Wakix's commercial ramp, but those benefits rolled off the calculation beginning in Q3 2023. Also consider that excluding one-time milestone payouts to CiRC Biosciences and Zynerba Pharmaceuticals, TTM EPS at the end of September 2025 would've been $3.74 -- 16% higher.

Similarly, although shares of Harmony Biosciences have trekked sideways in recent years, the market is failing to properly value the business' profitability. Consider how the share price looks when expressed as a daily price-to-earnings (PE) ratio, also based on GAAP EPS from the rolling 12-month period.

As described in last quarter's research note, the mismatch between patient growth and quarterly revenue predicted a rebound in Q3 2025 revenue. What commercial metrics cannot predict is back-to-back surges in patient additions.

I know what you're thinking.

Just weeks after the pivotal RECONNECT study failed so hard data weren't even shared, Wakix magically turns in one of its strongest quarters ever? In its sixth year on the market? Press "x" to doubt.

Investors might entertain the thought that management is fudging the numbers. I did too. However, the entire competitive landscape lurched upward in the third quarter. Every major drug brand delivered one of its strongest performances in recent memory. Apparently, a bunch of narcolepsy patients were swept into a cave, and doctors just found them.

- Wakix (histamine agonist): Harmony Biosciences reported 500 new patients during the quarter (highest ever barring first few quarters of launch), a 29% increase in year-over-year revenue (the highest in six quarters), and $39 million increase in quarter-over-quarter revenue (highest ever).

- Xywav (sodium oxybate): Jazz Pharmaceuticals reported 125 new patients during the quarter, 475 new patients since the beginning of the year, double-digit increase in year-over-year growth for the second consecutive quarter, and an $18 million increase in quarter-over-quarter revenue. Those are respectable numbers for a franchise that's been losing market share since peaking in 2022.

- Lumryz (sodium oxybate): Avadel Pharmaceuticals reported 300 new patients during the quarter and $77.5 million in quarterly revenue. The newest sodium oxybate on the market is still early in its ramp, but stealing patients from Xywav presents both opportunities and challenges. It's doing relatively well given the circumstances.

- Sunosi (DNRI): Axsome Therapeutics reports total quarterly prescriptions, not patient additions. Sunosi is a secondary treatment option in the narcolepsy treatment, but similar to Wakix, can be prescribed to patients already on another treatment. It saw a respectable 12% increase in prescriptions and 35% increase in revenue from the prior-year period (due to aggressive pricing).

As the quick survey of the competitive landscape shows, Harmony Biosciences remains the best positioned ahead of the expected launch of oveporexton in late 2026. It's delivering the most consistent revenue growth and patient additions.

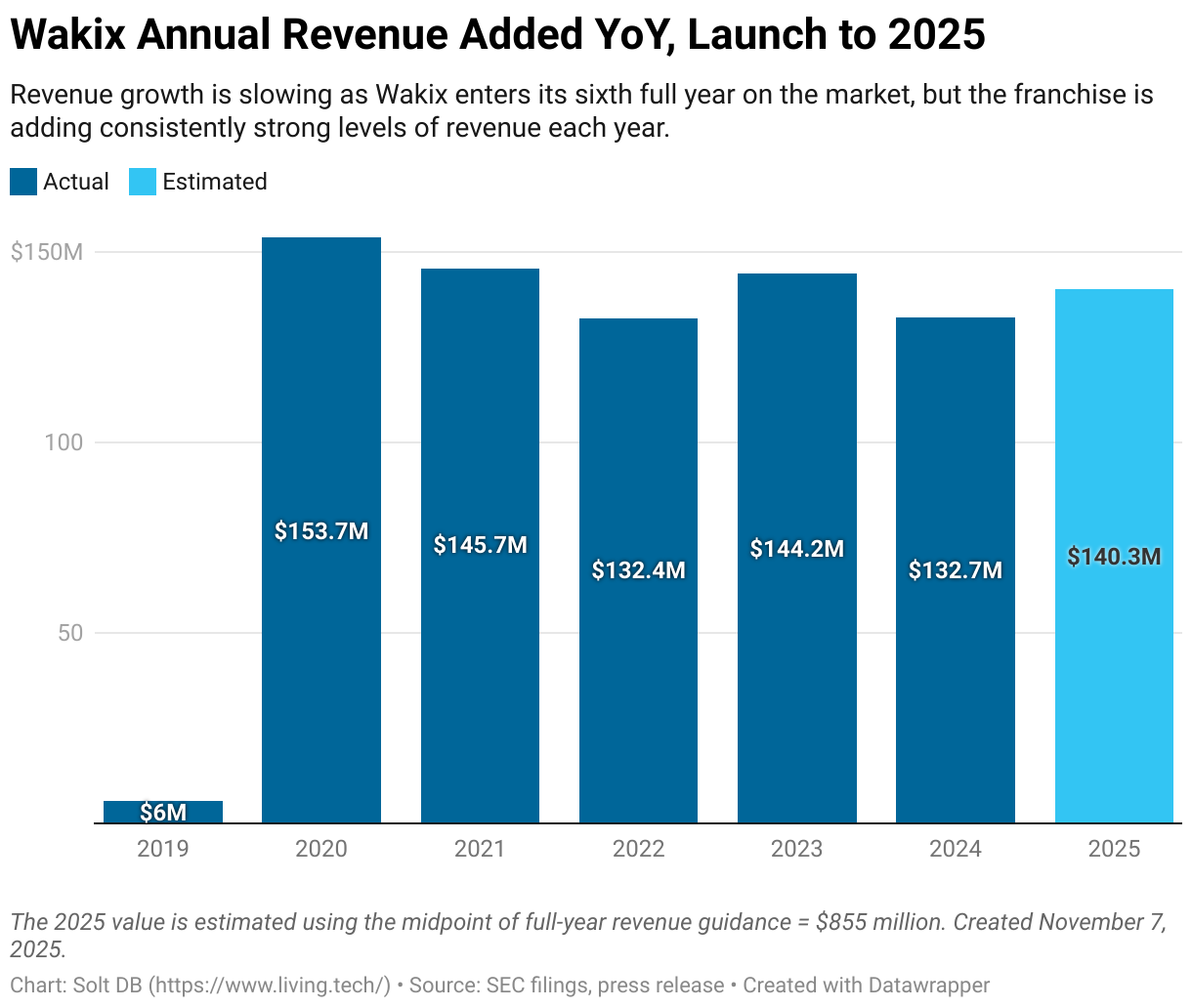

Management updated full-year 2025 revenue guidance to a midpoint of $855 million, up from a prior expectation of $840 million. That suggests Wakix could add $140 million in revenue compared to last year, continuing its impressively consistent commercial ramp. It might be difficult to get over the coveted $1 billion threshold next year, but it's slightly more possible than before.

Analysts peppered the company with questions about updated guidance on the quarterly earnings call – you should have questions, too.

- Harmony Biosciences reported revenue of $624.7 million in the first nine months of 2025. To meet the midpoint of guidance, the business would need to achieve Q4 2025 revenue of $231 million.

- The business just delivered Q3 2025 revenue of $239 million.

- The business has never delivered less revenue in Q4 than it did in Q3 of any calendar year, which makes sense given the seasonality of the sector.

It's difficult to say if management is simply being conservative or if other commercial factors are at play. Although patient additions are healthy, wholesalers made unusually large purchases of Wakix in the third quarter. That activity usually occurs during the fourth quarter as wholesalers rebuild inventory at the end of each calendar year before new price increases go into effect on January 1.

Are wholesalers simply responding to surging prescription growth, meaning they'll continue building inventory during Q4 as usual? It's impossible to know for sure.

Either way, Q1 revenue is always lower than the prior calendar year's Q4 revenue due to this wholesaler inventory dynamic. If inventory buildups are higher than usual due to Q3 and Q4 purchases, then investors might want to prepare for a "higher they rise, the further they fall" scenario for revenue in early 2026.

Business Development Activities

Avadel Pharmaceuticals acquired by Alkermes

On October 22, Alkermes announced its intention to acquire Avadel Pharmaceuticals for up to $2.1 billion. The upstart wields Lumryz, a sodium oxybate competing most directly with the Xywav from Jazz Pharmaceuticals, and is expected to generate full-year 2025 revenue just shy of $300 million. Through the first nine months of the year, the business delivered operating cash flow of $27 million.

The market hated the acquisition initially. Alkermes ended September 2025 with just $1.14 billion in cash. Through the first nine months of 2025, the business actually saw revenue decline from the prior-year period.

However, Alkermes doesn't give a shit about Lumryz. Although it'll add some revenue growth and cash flow, the real reason for acquiring Avadel Pharmaceuticals is for its commercial infrastructure in narcolepsy.

Alkermes is expected to be the second to market with an OX2R agonist behind Takeda. The company's drug candidate, alixorexton, is a couple years behind the first-mover. It had some additional side effects compared to oveporexton, but should be the first once-daily treatment to launch in the OX2R drug class. To maximize a potential launch down the road for its OX2R agonist candidate, Alkermes decided to acquire Avadel Pharmaceuticals now – when it was most affordable – and hope that pays dividends.

This serves as a reminder of the importance of commercial infrastructure in drug development and how difficult it is to properly establish. Alkermes would rather take on more long-term debt than it has in revenue than risk trying to build commercial infrastructure in a highly competitive market.

Everyone thinks the biotech stocks they own will be the ones to be acquired. I carefully select the companies in the coverage ecosystem, so there will be an above-average rate of acquisitions. Nonetheless, Harmony Biosciences could be a valuable takeover target both for the continued strength of Wakix and its potential OX2R agonist candidate '15205. It helps that the two largest CNS drug developers, Biogen and Bristol Myers Squibb, are a little more desperate to add growth and shore up patent cliff risks. Neither has an OX2R agonist candidate in development.

Additionally, don't rule out Takeda as a potential suitor. There's potential to study combinations of OX2R agonists and Wakix, as the mechanisms of action could be complimentary. Takeda might also like to add a highly potent OX2R agonist candidate with potential to treat NT1, NT2, and idiopathic hypersomnia. Oveporexton was only developed for NT1.

Harmony Biosciences wants to acquire pipeline assets

Although it'd be better for shareholders if management sold the company, Harmony Biosciences has been talking up the potential to acquire pipeline assets for several quarters now. On the Q3 2025 earnings conference call, management said it's exploring multiple potential deals.

That bodes poorly for a share repurchase – there's still $150 million in buybacks authorized by the board of directors – although that could occur if business development activities fall through. Analysts seemed to want the company to acquire later-stage assets, or even revenue-generating assets, although the business is limited by its cash balance. While respectable, there's only so much you can do with $778 million.

What could investors expect?

- Acquiring more tiny companies (Zynerba was acquired for $60 million upfront, Epigenix was acquired for $35 million upfront) is unlikely to move the needle much. Companies trading for less than $100 million are usually sitting there for good reason.

- Acquiring a slightly-larger drug developer – in the ballpark of $400 million to $500 million, or half the cash balance – could be more encouraging, but it depends on the assets acquired. A meatier acquisition also has a higher risk of backfiring if analysts question the use of cash.

- Acquiring rights to a "real" asset could be more rewarding, but wouldn't help diversify operations away from Wakix in the near term. This won't happen, but for an illustrative example only, a "real" asset might be the Alzheimer's disease candidate ARO-MAPT from Arrowhead Pharmaceuticals. Buying rights might cost $200 million upfront even though the asset hasn't entered clinical trials yet. (Harmony Biosciences is not interested in Alzheimer's disease.) Fellow CNS drug developer Biohaven recently imploded and signaled it's open to offloading some of its mid- and late-stage assets. Harmony Biosciences could potentially acquire several assets in one transaction.

- Buying into a revenue-generating asset could be one of the better uses of cash. Harmony Biosciences could pay $X million to acquire a 50% interest in a CNS drug that's already on the market, especially if its owner would rather have the cash than half of its revenue and earnings potential.

News Flow & Modeling Insights

(Refined, slightly higher.)

My current model is based on properly valuing the underlying business and assumes no threat from generic competition to Wakix until 2030.

The current model makes the following assumptions about key operating metrics:

- Full-year 2025 revenue of $859.677 million, up from a prior expectation of $835.222 million and above the $855 million midpoint of guidance.

- Full-year 2025 operating expenses of $435.468 million, up from a prior expectation of $431.150 million. This includes at least $35 million in in-process research and development (IPR&D) expense from milestone payouts, which are one-time expenses.

- Full-year 2025 net income of $182.371 million or GAAP earnings per share (EPS) of $3.16, up from prior expectations of $178.836 million and $3.10 respectively. The year-end outstanding share count is expected to be 58.460 million, assuming no purchases under the active share repurchase program. This does not account for one-time charges, adjustments, or acquisitions.

The current model continues to exclude all assets aside from Wakix.

Margin of Safety & Conviction

Harmony Biosciences is considered a Current Compounder position with the following Conviction rating.

- 1 = High

- 2 = Above Average (increased)

- 3 = Average

- 4 = Below Average

The estimated fair valuation based on my current model is below:

- Market close November 6: $30.94 per share

- Modeled Fair Valuation: $65.32 per share

- Allocation Range: Up to 5%

Harmony Biosciences reported 57.596 million shares outstanding as of October 31, 2025. The modeled fair valuation above assumes 58.460 million shares outstanding, which is equivalent to 1.5% dilution. An acquisition would have a fully-diluted basis of roughly 65 million shares.

Further Reading

- November 2025 press release announcing Q3 2025 operating results

- November 2025 regulatory filing (10-Q) detailing Q3 2025 operating results

- October 2025 quarterly earnings preview for the Solt DB coverage ecosystem

- September 2025 research note describing the pivotal RECONNECT study in fragile X syndrome

- August 2025 research note analyzing Q2 205 operating results

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)