.svg)

There's good, there's bad, and there's ugly. The data readout for the blood-based colon cancer screening diagnostic candidate from Exact Sciences was pretty ugly.

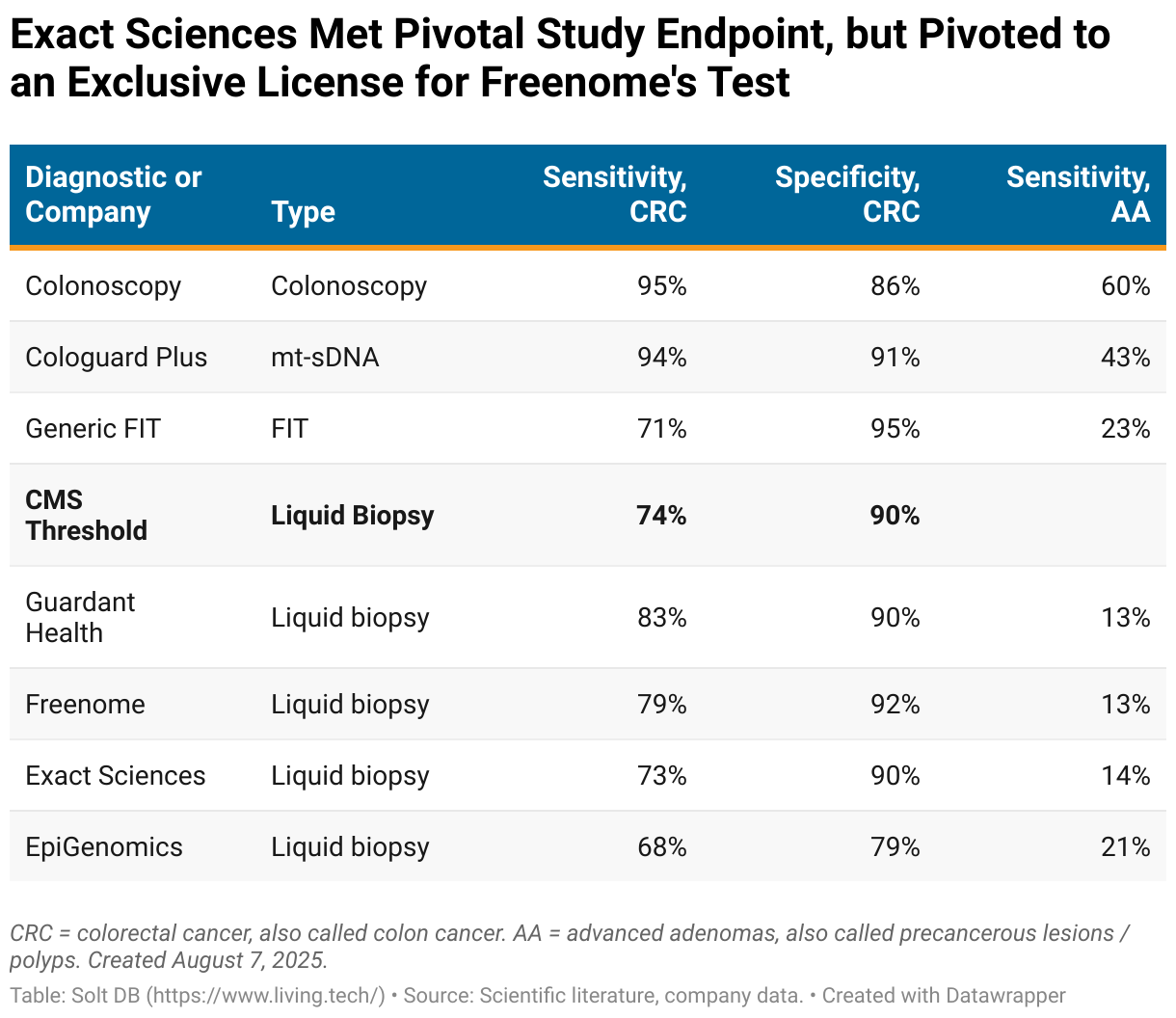

Performance in the messy real-world BLUE-C study was expected to drop off from the perfect conditions of the case control study. But sensitivity fell from 88% to 73% (below Medicare reimbursement threshold), specificity held steady somehow at 90% (meeting Medicare reimbursement threshold), and precancerous lesion sensitivity fell from 31% to 14% (investors were hoping for half that decline).

It wasn't much of a data readout either. Exact Sciences reported the results in a single sentence in a press release.

That's because the company immediately pivoted to an exclusive license for Freenome's diagnostic candidate, which had real-world sensitivity of 79%, specificity of 91.5%, and precancerous lesion sensitivity of 12.5%. Wall Street couldn't be more displeased.

The steep sell-off in shares is awkward. The blood-based screening opportunity has never been included in my model, which is based on underlying business performance – and the business has never been stronger.

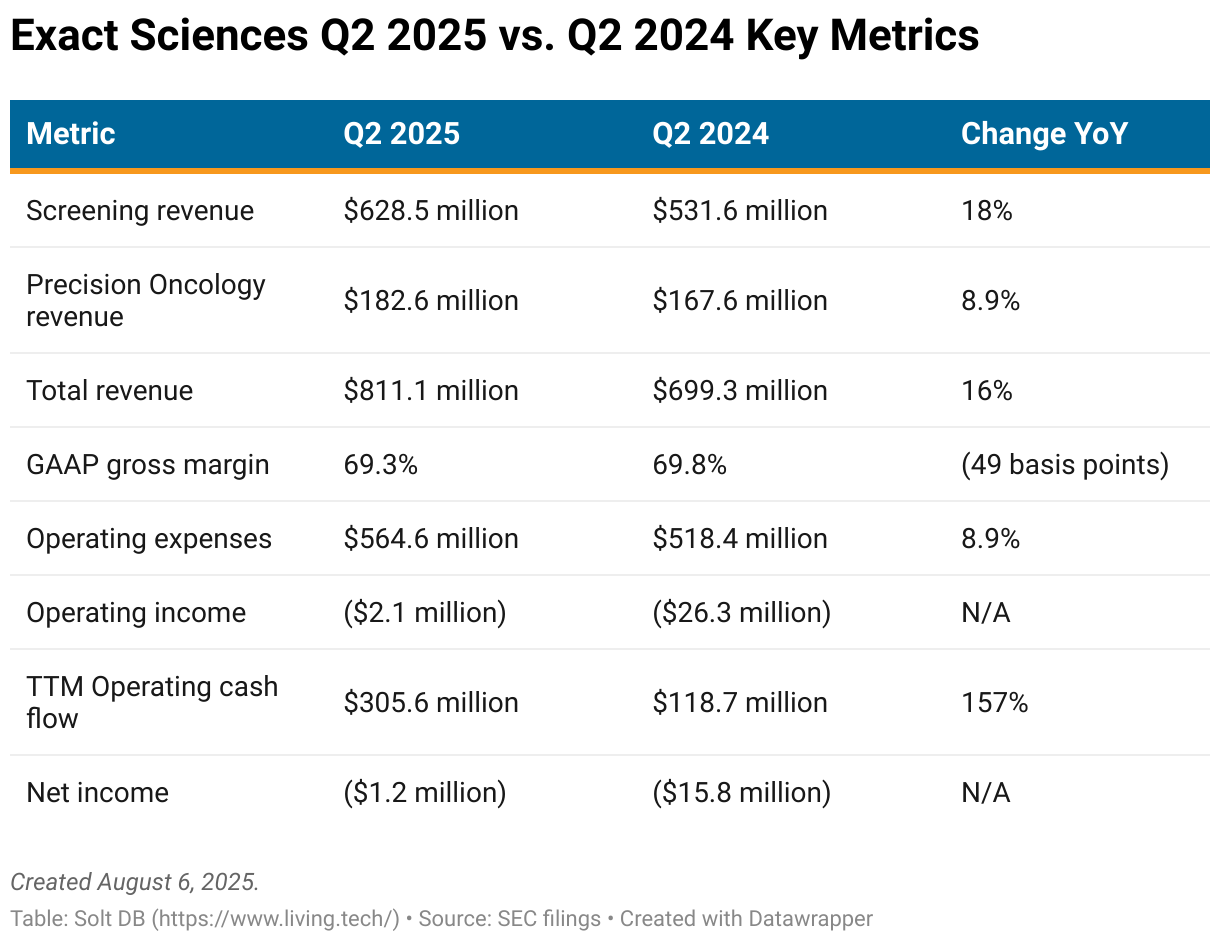

Exact Sciences reported second-quarter 2025 revenue of $811 million and raised full-year guidance. Wall Street didn't expect quarterly sales to reach that level until the fourth quarter at the earliest. That wasn't a crazy assumption. The business had never previously generated more than $713 million in quarterly sales.

Operating loss improved to just $2.1 million during the quarter, while operating cash flow in the first half of 2025 soared to $120 million. It was just $24 million last year. Management promised second-half cash flow would be even higher.

The cancer diagnostics leader also announced a new productivity push that aims to reduce annual operating expenses by $150 million by 2026. That, coupled with business performance that's two to three quarters ahead of projections, allows me to transition my current model to one based on 2026 earnings.

By the Numbers

If a management team is ever going to announce developments that could be interpreted poorly, then the best-case scenario would be to simultaneously announce good news. The gooder the better-er.

The ironic part is Exact Sciences couldn't have performed much better during the second quarter, but the market is currently fixated on blood-based screening tools.

Cologuard delivered record quarterly revenue. The Screening segment generated record revenue from Medicare, although it was a record low as a percentage of total segment sales. The Precision Oncology segment generated record revenue even when excluding one-time licensing revenue of $7.5 million. International revenue was a record. Operating margin and net margin were also records. First-half operating cash flow was a record.

The business added $111.8 million in total revenue from the year-ago period, which… was the third-highest since the end of 2020. Still pretty solid.

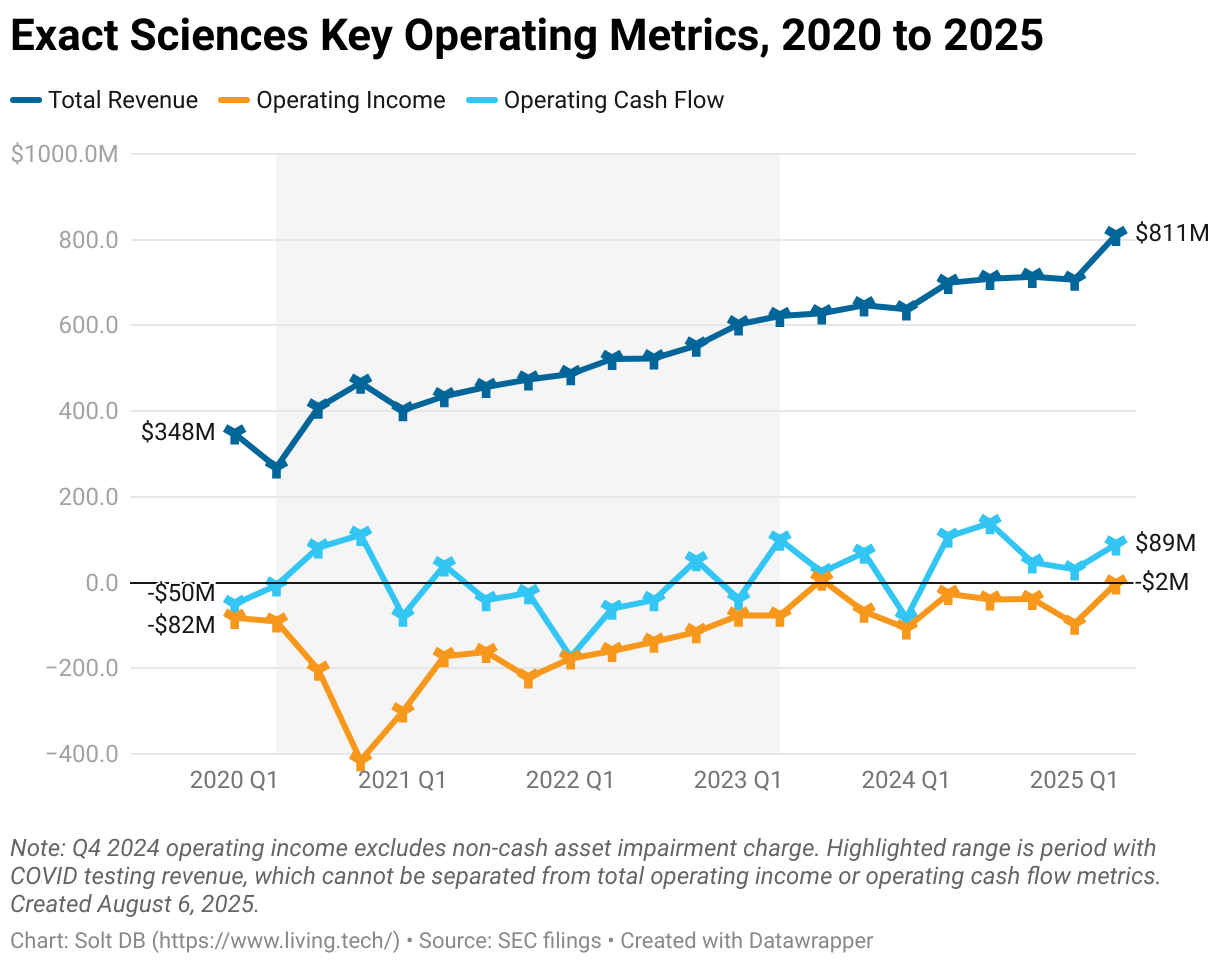

The sudden step up in revenue and other operating metrics is clearly visible in the long-term visualization of business performance. It shouldn't be a temporary blip. For the business to meet the midpoint of full-year 2025 revenue guidance, it needs to average quarterly revenue of $818 million in the second half of the year.

Exact Sciences is objectively crushing it right now.

The Screening segment generated record revenue from Medicare, but the U.S. healthcare program fell to a record low percentage of total segment revenue.

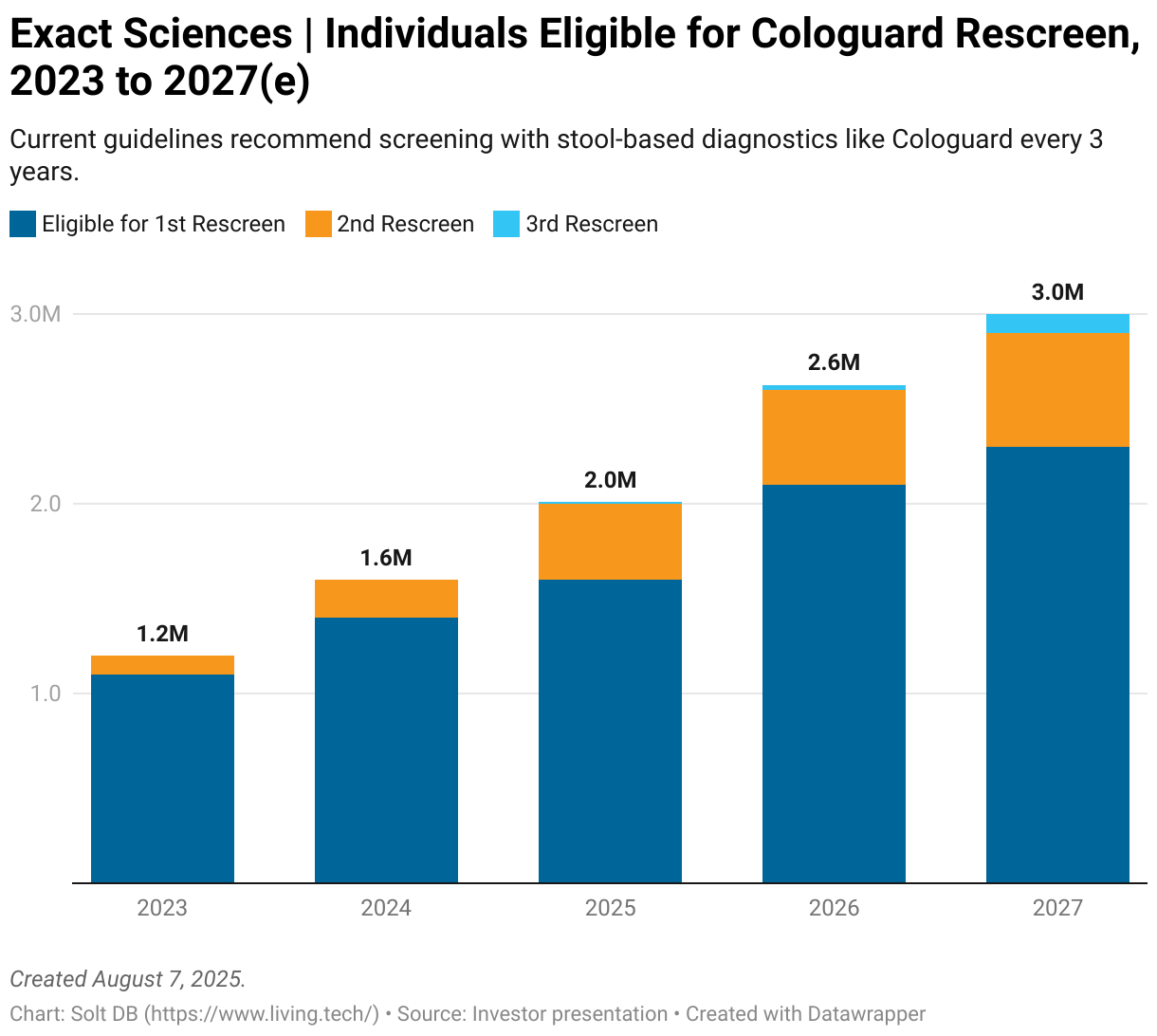

That's a sign Cologuard is gaining traction in the 45-49 year old age bracket, which is the most valuable from a long-term perspective. Data show these customers have a much higher compliance rate for future screenings than individuals who first used Cologuard at an older age. Younger individuals will also generate more lifetime revenue, as they'll be eligible for more screenings in their lifetime.

An estimated 2.6 million individuals are eligible for rescreens in 2026, up from just 1.2 million in 2023. The year-over-year increase in rescreen eligibility next year – 600,000 individuals – will be the largest ever. That coincides with the launch of Cologuard Plus and its favorable price increase.

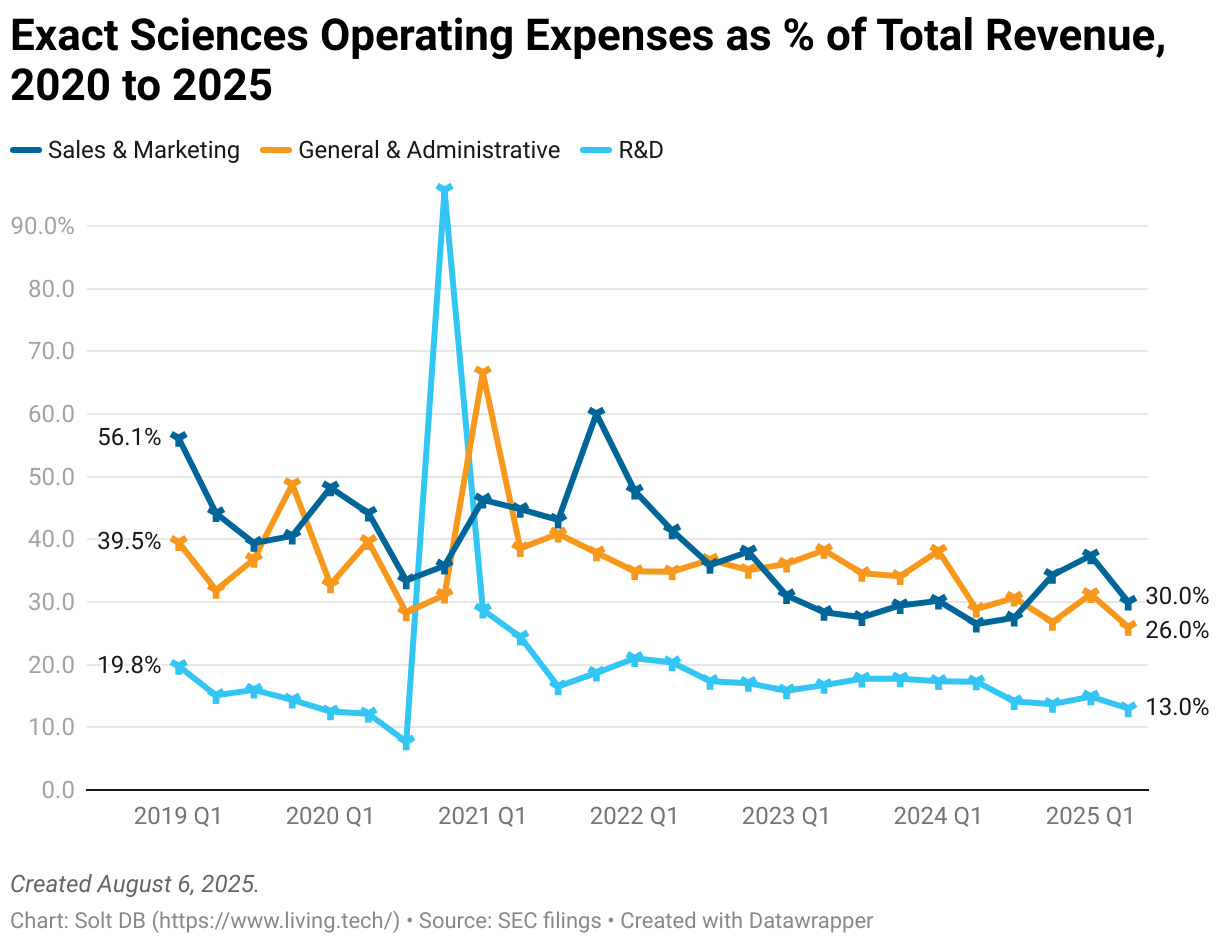

Recent increases in sales & marketing expenses and general and administrative expenses declined rapidly as a percentage of revenue. That means operating expenses are growing more slowly than revenue, which drives cash flow and profitability over time.

The Freenome License, Explained

Exact Sciences pivoted away from its internal blood-based colon cancer screening candidate and acquired exclusive rights to Freenome's competing diagnostic candidates, including a screening tool that's been submitted to the FDA and a next-generation candidate in development. The financial terms are flexible and well-matched to the regulatory trajectory.

In the beginning, Exact Sciences agreed to make an upfront payment, make a debt investment in Freenome, and provide an R&D allowance for three years. Regulatory milestones align with the regulatory environment. If it shifts more favorably than expected, then payments increase, but the market opportunity will be larger.

- $75 million upfront paid by Q4 2025

- $50 million debt investment that pays 5% until maturity in 2030

- $20 million per year for three years to offset R&D expenses for Freenome

- $100 million upon approval of the first-generation diagnostic candidate

- Up to $100 million upon approval of a next-generation diagnostic candidate, but it must achieve an overall sensitivity of at least 83% and a precancerous lesion sensitivity of at least 19%

- $500 million if a diagnostic candidate is included in the U.S. Preventive Services Taskforce (USPSTF) guidelines

- 0% to 10% royalty based on gross margin, triggered after gross margin reaches a specific threshold

The move is a win-win. The startup wants to pivot to focus on its multi-cancer early detection (MCED), as part of its own prioritization efforts in a tight capital environment. The licensing deal allows Freenome to refocus bandwidth, monetize its R&D investment in blood-based screening to date, earn some much-needed cash, and still share in downstream economic rewards. Exact Sciences gets a blood-based screening option after pivoting from its internal asset, shaves half a year off the regulatory timeline, and can immediately leverage its massive commercial footprint for the best launch possible in 2027.

Management said it can terminate the entire agreement with Freenome if the next-generation tool fails to achieve a precancerous lesion sensitivity of at least 19%. It was intrigued by the platform after seeing preliminary data from a rudimentary next-generation test, which was evaluated in a small subset of the 48,995-patient PREEMPT study, the pivotal trial for the first-generation test.

Exact Sciences is continuing internal efforts to develop a blood-based screening tool with the goal of significantly improving precancerous lesion detection. It could pivot back to its own next-generation asset in the future.

As for the timing of payments, Exact Sciences will be on the hook for $135 million in total payments by the end of 2025. Freenome's first-generation diagnostic candidate could be approved in late 2026, which would trigger another $100 million payout, plus $20 million for next-year's R&D allowance. It's unlikely to launch until early 2027.

A next-generation tool is unlikely to be approved until the early 2030s. Although the USPSTF is expected to update colon cancer screening guidelines in 2026, it isn't expected to include blood-based screening options until 2031 when more real-world data are available. That could make it more difficult for this diagnostic modality to be covered by commercial insurance programs in the next five years.

Recent rumors suggest the entire panel of experts at USPSTF could be replaced by political appointees ahead of next year's expected guideline update, so there's increased uncertainty surrounding decisions or whether there will be an update at all. Guardant Health does seem to have an unusual hold on regulators in the current environment, as evidenced by its shockingly high Medicare reimbursement rate. Maybe it can influence USPSTF to include blood-based screening options, too.

What should investors make of the licensing deal?

Investors can think of the Freenome license like an insurance policy. Management couldn't really come out and say that on the earnings conference call, which would be disrespectful to Freenome, but an insurance policy is the most accurate characterization.

A drug product and a diagnostic product ramp very differently after launch.

As explained above, the market opportunity for blood-based screening tools will be dictated by post-approval regulatory decisions. These will take years to play out for each individual test and the diagnostic modality as a whole.

- First, a test must earn FDA approval to launch. But a launch isn't helpful if people cannot pay for a test.

- Second, a test must earn Medicare coverage by earning FDA approval, meeting specific performance requirements, and being included in professional guidelines. Tests usually only launch once Medicare coverage is assured.

- Third, a test must earn commercial payer coverage. Insurance companies typically don't cover a screening tool or modality until it's recommended by USPSTF guidelines.

For reference, the Cologuard franchise generates 36% of total revenue from Medicare, 54% from commercial insurance programs, and 10% from out-of-pocket payments. Blood-based screening options are much less likely to be covered out-of-pocket due to higher costs, which makes commercial payer coverage even more important.

Liquid screens are still at the very beginning of the regulatory trajectory. I might argue Cologuard has paved the way for new diagnostic modalities, which should reduce the timelines involved. But even the reduced timelines are measured in half-decades.

One looming question for blood-based screens

The entire therapeutic modality hinges on a single question: Will low precancerous lesion detection rates exclude them from USPSTF guidelines altogether?

Although sensitivity and specificity get all the glory, regulators say a whopping two-thirds of the life-years gained from a colon cancer screening test come from detecting precancerous lesions. Blood-based screening tools struggle with this metric.

The uncertainty comes from a frustrating reality: Data from each diagnostic modality can be carved up and presented in favorable ways.

- Colonoscopy can't be beat on clinical metrics, but total healthcare costs and availability make matters more complicated. CT colonography offers an alternative option, but radiation concerns (increasingly important as guidelines recommend screening begin at younger ages) and an a lack of consensus on rescreen timing make it a less common option.

- Stool-based tests like Cologuard Plus are increasingly being used as the first-line option in average-risk individuals. This therapeutic modality offers at-home convenience, but pooping in a box is still a turn off for some individuals. This therapeutic modality alone probably cannot close the care gap of 45 million Americans.

- Blood-based tests offers in-office convenience, as it's straightforward to draw extra vials of blood during other routine checkups (for those who get routine checkups). But they perform poorly on precancerous lesion detection, which, given many other well-performing options, could make doctors hesitant to prescribe them as a first choice.

The management team at Exact Sciences has historically downplayed the market opportunity for blood-based screening tests, instead characterizing them as a likely niche option. It argues that a low precancerous lesion detection rate will reduce the commercial opportunity.

Because the market opportunity for screening tools is based on post-approval regulatory decisions, it's simply too soon to say if management is correct. The USPSTF could decide to include liquid screens by arguing even inferior screening options are better than no screening at all. I would agree.

But the USPSTF also considers the economics of screening guidelines. The much-higher costs and low precancerous lesion detection certainly complicate the decision for blood-based options.

If management is wrong that the emerging diagnostic modality will be a niche option, then it could benefit by having a blood-based tool (well, Freenome's) on the market by 2027 (assuming it earns approval).

Cologuard vs. ___

Wall Street's sharply negative reaction to the licensing deal is confusing. Analysts and investors get too hung up on the C-word: competition.

- There are 45 million Americans ages 45-75 who aren't up to date on colon cancer screening.

- The United States has the capacity to conduct about 6 million colonoscopies each year.

- Cologuard completed over 4 million tests in 2024 and expects to top 14 million annual tests in the future. That's a lot of growth for a franchise that delivered full-year 2024 revenue of $2.1 billion – but even that's not enough to close the care gap.

There's an enormous opportunity for many products of varying diagnostic modalities to achieve significant long-term growth. The launch of this or that tool isn't a threat to Cologuard Plus, as growth for external screening tools won't necessarily come at the expense of the market leader. All tools are trying to accomplish the same thing: closing the care gap.

The numbers clearly bear this out.

In Q2 2025, the Cologuard franchise grew revenue by $96.9 million from the year-ago period, an increase of 18.2%. That doesn't seem like a brand that's struggling to combat competitive pressures.

Investors should remain vigilant. Will competitive pressures build in the next 12 months or 24 months? ColoSense has yet to earn Medicare coverage or launch, while Shield will have less than $100 million in full-year 2025 revenue and still lacks commercial payer coverage.

Stock price volatility

A final word on stock price volatility, as investors punish Exact Sciences and bid up shares of Guardant Health.

As the saying goes, experience is what you get when you didn't get what you wanted. The biotech winter has made me realize my approach to investing is much more dependent on underlying business (or pipeline) fundamentals than narratives and headlines. There's nothing wrong with that. In fact, confidently understanding that is a good thing and protects against getting too emotional.

However, stock prices have been much more driven by narratives since 2020, with a brief reprieve during 2022. I don't think the current narrative-driven approach is sustainable.

The last few times I capitulated on my fundamentals-based approach have been disastrous. From 2016 to 2020, I wrote about a gazillion articles at The Motley Fool arguing how Invitae's growth-at-all-costs business model was doomed to fail. Five years is a long time to look like an idiot. I made it six, eventually succumbing to peer and market pressure in June 2021 -- exactly two months before the wheels started to come off.

Similarly, I think I kept AVITA Medical on a relatively tight leash tied to fundamentals, but in retrospect I might have given it one quarter too much leeway. There were signs the business was struggling with new product launches and international revenue, while management had missed a worrying amount of guidance expectations by that time.

For Exact Sciences, I have absolutely no idea why Wall Street is so obsessed with blood-based screening options. They can and will add growth for the companies that own them, but they're not commercially relevant right now. I have yet to include them in my model for a reason!

Exact Sciences was unlikely to launch a test, whether its own or Freenome's, until 2027 anyway. If liquid screens aren't included in USPSTF guidelines in the expected 2026 update, then they may not earn commercial insurance coverage until 2031. Favorable Medicare pricing would expire before then, which could rapidly change Wall Street's stance on growth prospects. There's no reason for Exact Sciences to lose $1.2 billion of market cap in a single day based on any developments to date.

I can always be wrong, but I'm confidently sticking with my assessment of the commercial, regulatory, and competitive landscapes on this one.

News Flow & Modeling Insights

(New earnings-based model for 2026.)

The business is tracking a few quarters ahead of the previously-expected trajectory, while a new productivity push aims to reduce annual operating expenses by $150 million by 2026. That allows me to introduce a new earnings-based model for Exact Sciences.

The modeled fair valuation is lower than the previous 2025 model ($12.435 billion vs. $16.488 billion), which was the most forward-looking in the coverage ecosystem, having been anchored to 2025 operations since 2022. But the new earnings-based model for 2026 is also more accurate as it incorporates business and commercial metrics that have better predictive value.

My current 2026 model for Exact Sciences assumes:

- Excludes blood-based screening tools.

- Fair valuation of $12.435 billion, or $64.40 per share.

- Full-year 2026 revenue of $3.598 billion, representing year-over-year growth of 13.9%.

- Screening segment revenue of $2.851 billion, representing year-over-year growth of 15.7%.

- Precision Oncology segment revenue of $746 million, representing year-over-year growth of 7.5%.

- Operating income of $349 million.

- Net income of $329 million to $369 million, or earnings per share (EPS) of $1.70 to $1.91.

Although the fair valuation is no longer based on business performance in the current year, the model expects the following for 2025:

- Full-year 2025 revenue of $3.159 billion, representing year-over-year growth of 14.5%. Revenue guidance expects $3.150 billion at the midpoint.

- Screening segment revenue of $2.464 billion, representing year-over-year growth of 17.5%. Segment revenue guidance expects $2.455 billion at the midpoint.

- Precision Oncology segment revenue of $694.382 million, representing year-over-year growth of 7.5%. Segment revenue guidance expects $695 million at the midpoint.

- Operating loss of $65.868 million, an improvement from an adjusted operating loss of $210.359 million in 2024. The adjustment excludes a one-time impairment charge of $869 million.

Margin of Safety & Conviction

Exact Sciences is considered a Current Compounder position with the following Conviction rating.

- 1 = High

- 2 = Above Average

- 3 = Average

- 4 = Below Average

The estimated fair valuation based on my current model is below:

- Price August 7, 12pm ET: $41.70 per share

- Modeled Fair Valuation: $64.40 per share

- Allocation Range: Up to 15%

Exact Sciences reported 189.319 million shares outstanding as of August 5, 2025. The modeled fair valuation above assumes 193.105 million shares outstanding, which is equivalent to 2% dilution.

Further Reading

- August 2025 press release from Exact Sciences about the licensing deal

- August 2025 press release from Freenome about the licensing deal

- August 2025 press release announcing Q2 2025 operating results

- August 2025 regulatory filing (10-Q) detailing Q2 2025 operating results

- July 2025 research note previewing Q2 2025 earnings across the coverage ecosystem

- July 2025 research note analyzing blood-based screening regulatory dynamics

- May 2025 research note analyzing Q2 2025 operating results

.svg)

.svg)

.png)

.svg)

.svg)

.svg)