.svg)

A new and improved Cologuard is coming soon.

Exact Sciences announced successful results from the BLUE-C study evaluating a next-generation Cologuard test for non-invasive colon cancer screening. The diagnostic candidate delivered improvements on all three key metrics used to quantify the value of the existing Cologuard product. Importantly, it reduced the number of false positives by 30%. The company intends to submit an application requesting regulatory approval before the end of 2023.

However…

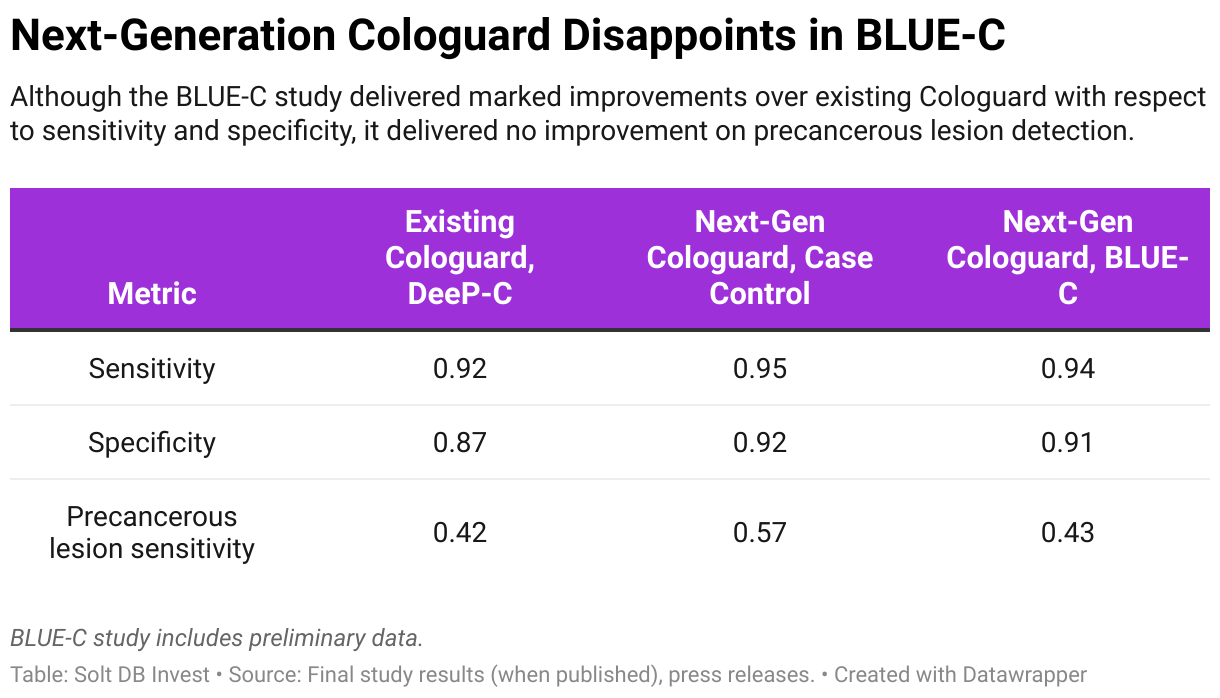

The next-generation Cologuard absolutely whiffed on precancerous lesion detection -- one of the three key metrics. The product candidate delivered an improvement compared to the existing product, but it needed to achieve at least 55% detection rates to mark a meaningful difference and position itself to dethrone colonoscopies as the standard of care. For reference, the existing Cologuard product has a detection rate of only 42%, a case control study of the next-generation Cologuard achieved 57%, and invasive and awkward colonoscopies can detect 60%.

The BLUE-C study delivered a precancerous lesion detection rate of only 43%. That all but guarantees the best-case scenario for the next-generation Cologuard is now firmly off the table.

BLUE-C Results, Explained

To be clear, the BLUE-C study was a success. The next-generation Cologuard shouldn't have a problem earning regulatory approval or payer coverage. A 30% reduction in false positives will continue the product's growth trajectory for several years.

Solt DB Invest previously published an outline for how to interpret the BLUE-C study results, which defined many nerdy terms. To recap briefly, the U.S. Food and Drug Administration (FDA) has clearly communicated the key metrics it looks for in an experimental tool:

- Sensitivity of colon cancer: The ability to correctly identify individuals with colon cancer. Overall sensitivity is most often communicated, which is the rate of detecting cancer at any stage. Tests are differentiated by their ability to detect early-stage cancers (Stage I and Stage II). It's easier to detect advanced cancers, which makes early-stage detection the biggest driver of overall sensitivity.

- Specificity of colon cancer: The ability to correctly identify healthy individuals. It's generally not great to scare the shit out of people by telling them they have cancer when they don't.

- Sensitivity of precancerous lesions: The ability to detect benign masses that can become cancer. Precancerous lesions are more important for some cancers (cervical or colon) than others (lung).

It's also important to reiterate the two different types of studies:

- A case control study uses a diagnostic candidate with tissue samples stored in a laboratory. Scientists and doctors already know the health outcome of these tissue samples ("Is this fecal sample from an individual who had Stage I colon cancer? A healthy individual? An individual with precancerous lesions?"), which allows them to gauge the performance of a diagnostic candidate and informs the design of a real-world study.

- A real-world study uses a diagnostic candidate in real humans with unknown colon health. Real humans also take grandkids to soccer practice, sleep past alarms, and fail to follow exacting directions for sample preparation, shipping, and so on. These real-world variables tend to introduce noise and error into clinical studies, which explains why real-world study results tend to underperform case control study results.

Let's compare the results from the existing Cologuard product's pivotal DeeP-C study, the next-generation Cologuard's case control study, and the next-generation Cologuard's pivotal BLUE-C study:

As expected, the results from the real-world study (BLUE-C) underperformed the results from the case control study. But as the table above reflects, there was a surprisingly steep drop in precancerous lesion detection.

It's also important note that the BLUE-C results announced via press release on June 20, 2023, are preliminary results. More detailed results, including sensitivity in early-stage colon cancer, will be an important metric to watch.

Next-generation Cologuard's low precancerous lesion detection rate will blunt growth in the second half of this decade.

A Missed Opportunity for 2026 and Beyond

Solt DB Invest's current Margin of Safety range is based on our 2025 model. Exact Sciences has a rare degree of certainty, which makes it "easier" to model than, say, a precommercial drug developer. As our coverage ecosystem expands, more Anchor and Growth (Quality) positions will have long-term modeling available.

That said, our model stops at 2025 for a specific reason.

In 2026, the U.S. Preventive Services Task Force (USPSTF) is scheduled to update screening recommendations for colon cancer diagnostics. The recommendations help to set minimum requirements on metrics for clinical trials as technology improves, inform payer coverage, and establish pricing benchmarks in the competitive landscape. The update in 2026 could significantly impact the growth trajectory, and therefore, our modeling.

This mid-decade de-risking event is why next-generation Cologuard needed to deliver significantly improved precancerous lesion detection rates, which it failed to do. If the diagnostic candidate notched at least 55% sensitivity in advanced adenomas (what nerds in lab coats call precancerous lesions), then the USPSTF could've recommended Cologuard as a first-line screening option for colon cancer.

That would've put the entire $18 billion market opportunity up for grabs. The only first-line screening option at the moment is a colonoscopy, which has a roughly 60% precancerous lesion sensitivity when used as a standalone diagnostic. The 43% sensitivity coughed up in BLUE-C won't be enough.

The best way to understand the disappointment of BLUE-C is through a metric Solt DB Invest developed in our modeling (please don't share this or the following charts). There's a correlation between the combined value of sensitivity, specificity, and precancerous lesion detection and Medicare reimbursement.

First, consider how the competitive landscape ranks on this combined metric, which is simply calculated by multiplying the three metrics together. The case control results for next-generation Cologuard suggested it could legitimately become a first-line screening option in the 2026 USPSTF update. The real-world BLUE-C results suggest it's only a little better than the existing Cologuard product, although a 30% reduction in false positive rates compared to the existing product is meaningful.

Second, consider how these correlate to reimbursement rates, which are based on USPSTF recommendations. Next-generation Cologuard could've reset the standard for the entire competitive landscape and earned higher reimbursement than colonoscopies. That's because anything below the trend line is unlikely to earn Medicare reimbursement, or is likely to be removed from reimbursement as recommendations are updated, based on historical precedent.

This is what might have been possible based on the case control study results. Note that the data visualization keeps Cologuard pricing fixed, which better communicates the trend improvement.

Instead, BLUE-C coughed up a combined metric that barely raises the bar for the competitive landscape. Next-generation Cologuard still has the potential to earn higher reimbursement levels than the existing Cologuard, but the difference will be significantly less than the best-case scenario Solt DB Invest hoped for.

Maybe Cologuard 3.0 will hit the mark.

Forecast & Modeling Insights

(No change.)

There has been no change to our models since they were last shared in May 2023.

Full-year 2023 revenue of $2.550 billion

- Screening revenue of $1.917 billion, including Cologuard revenue of $1.868 billion. The company's updated guidance expects total Screening revenue of $1.782 billion at the midpoint.

- Precision Oncology revenue of $627.5 million. The company's updated guidance expects total Precision Oncology revenue of $612.5 million at the midpoint.

- Operating expenses of $2.118 billion

Full-year 2024 revenue of $3.131 billion, representing year-over-year growth of 22.8%

- Screening revenue of $2.382 billion, including Cologuard revenue of $2.441 billion.

- Precision Oncology revenue of $690 million

- Operating expenses of $2.201 billion, representing growth of about 3.9% from 2023. This could allow for positive operating income on a full-year basis, or at least during the second half of 2024. This milestone may be delayed into 2025 depending on investments made to support the launch of MCED tools.

Full-year 2025 revenue of $3.808 billion, representing year-over-year growth of 21.6%.

- Screening revenue of $3.048 billion, including Cologuard revenue of $2.978 billion. This expects an acceleration of market share capture from Cologuard 2.0, although the tool's growth rate declines from 2024. This acceleration remains intact despite lower-than-expected precancerous lesion detection, which would've impacted models in the second half of this decade.

- Precision Oncology revenue of $759 million. This expects continued momentum from portfolio expansion and evolution.

- Operating expenses of $2.265 billion, representing year-over-year growth of less than 3%. Importantly, the business delivers its first full year of profitability on an operating income basis.

Margin of Safety & Allocation

(No change.)

Exact Sciences is considered an Anchor position. The current Margin of Safety range for the company based on our 2025 model is below. This is the model reflected in our Margin of Safety dashboard:

- Current Price (market close June 20): $94.34 per share

- Likely Undervalued: <$81.24 per share

- Midpoint: $101.55 per share

- Likely Overvalued: >$121.86 per share

- Allocation Range: Up to 15%

The Margin of Safety range for the company based on our 2024 model is below:

- Current Price (market close June 20): $94.34 per share

- Likely Undervalued: <$67.71 per share

- Midpoint: $84.64 per share

- Likely Overvalued: >$101.57 per share

- Allocation Range: Up to 15%

The Margin of Safety range for the company based on our 2023 model is below:

- Current Price (market close June 20): $94.34 per share

- Likely Undervalued: <$55.90 per share

- Midpoint: $69.87 per share

- Likely Overvalued: >$83.85 per share

- Allocation Range: Up to 15%

Exact Sciences reported 180.388 million shares outstanding as of May 8, 2023. The Margin of Safety ranges above assume 187.500 million shares outstanding by 2025, 185.000 million shares outstanding by 2024, and 182.5 million shares outstanding by the end of 2023.

Further Reading

- June 2023 press release announcing preliminary data from the BLUE-C study for next-generation Cologuard

- May 2023 research note analyzing first-quarter 2023 operating results and our update models (these are the current models shared above)

- January 2023 research note describing how to interpret the BLUE-C study results

- December 2022 research note describing Guardant Health's disappointing results from its liquid-biopsy screening tool for colon cancer

.svg)

.svg)

.png)

.svg)

.svg)

.svg)