.svg)

Cologuard celebrated its first decade of commercial availability in late 2023 by achieving positive operating cash flow for the full year. The next decade will see its impressive scale compound several-fold more and, importantly, lead the company to profitability.

That milestone could arrive by 2025 – and maybe even this year.

Exact Sciences expects full-year 2024 revenue of $2.83 billion, up from $2.5 billion in 2023, powered by the flagship product. It will be another trying year for the Precision Oncology segment, with year-over-year growth of just 6% at the midpoint of guidance. That compares to just 4.6% in 2023 and 7.1% in 2022.

Investors shouldn't be too downtrodden about once again needing to lean on Cologuard. Solt DB Invest expects the colon cancer screening test to grow at least 25% in 2024, which would grow annual revenue by an additional $456 million. That compares to annual growth of 32% in 2023 (which added $439.5 million in revenue), 30% in 2022 (which added $321.8 million in revenue), and 30% in 2021 (which added $247.2 million in revenue).

What's more, Wall Street and the market are overlooking a significant growth driver sitting in plain sight: Cologuard rescreens.

By the Numbers

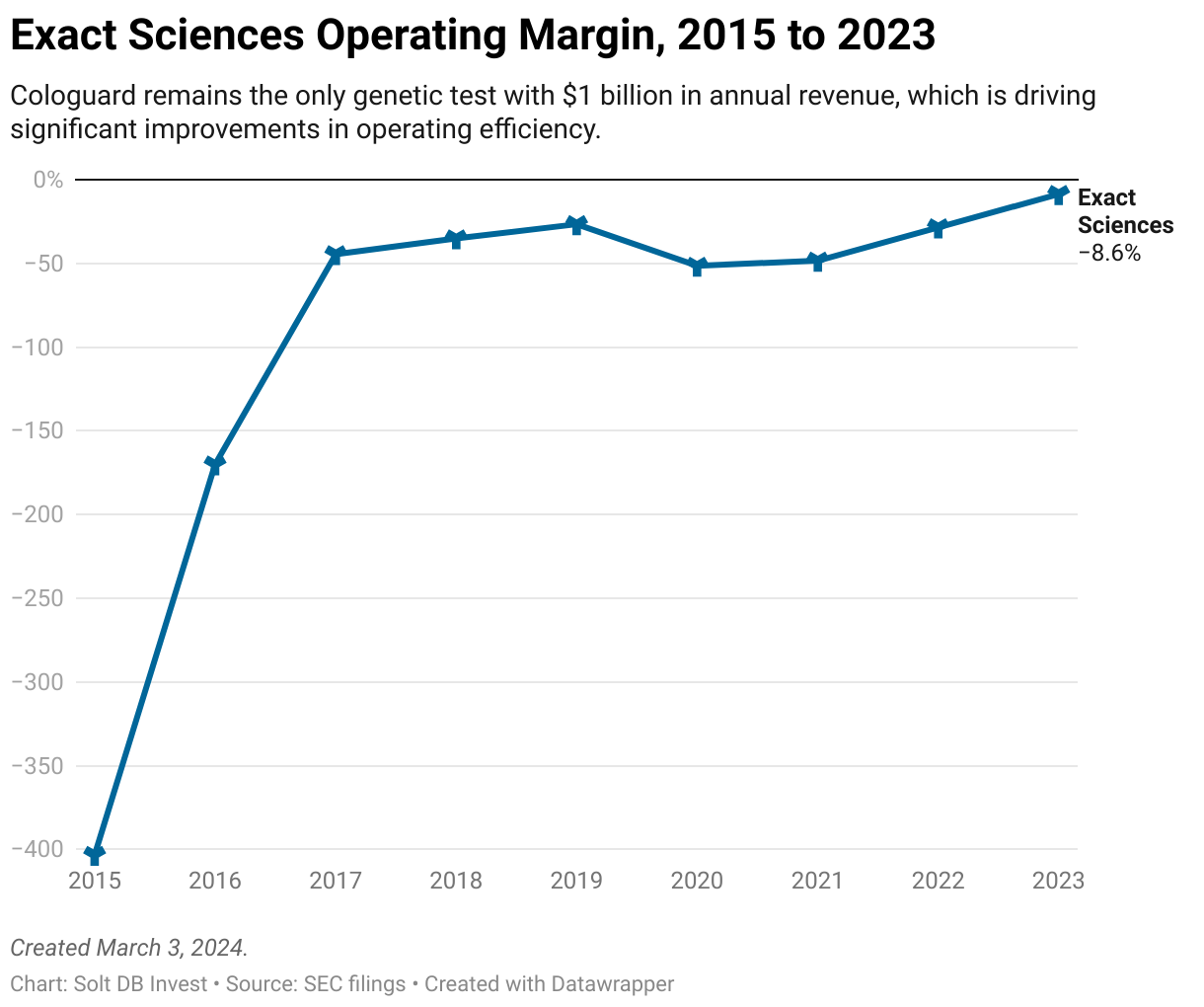

Exact Sciences has delivered solid execution in recent years, as evidenced by the company's increasing operating efficiency. Consider how operating margin has improved since Cologuard's first full year on the market in 2015.

The sharp improvement in operating margin last year allowed the business to generate full-year 2023 operating cash flow of $156 million. Although the business reported a negative operating margin representing an operating loss of $215 million on paper, that included $371 million in non-cash charges. That means the business saw a real-world increase in cash from operations alone.

Things weren't quite as good as they seemed. The business realized a one-time gain in operating income of $78.4 million from a reworked deal with MDxHealth, which acquired the company's Oncotype DX Genomic Prostate Score test in 2022. The suitor requested different terms that may now lead to greater long-term value for Exact Sciences. The one-time paper gain improved operating margin (it would've been negative 11.7% otherwise) and was responsible for half of operating cash flow (it would've been $77.7 million otherwise).

But investors shouldn't be too concerned.

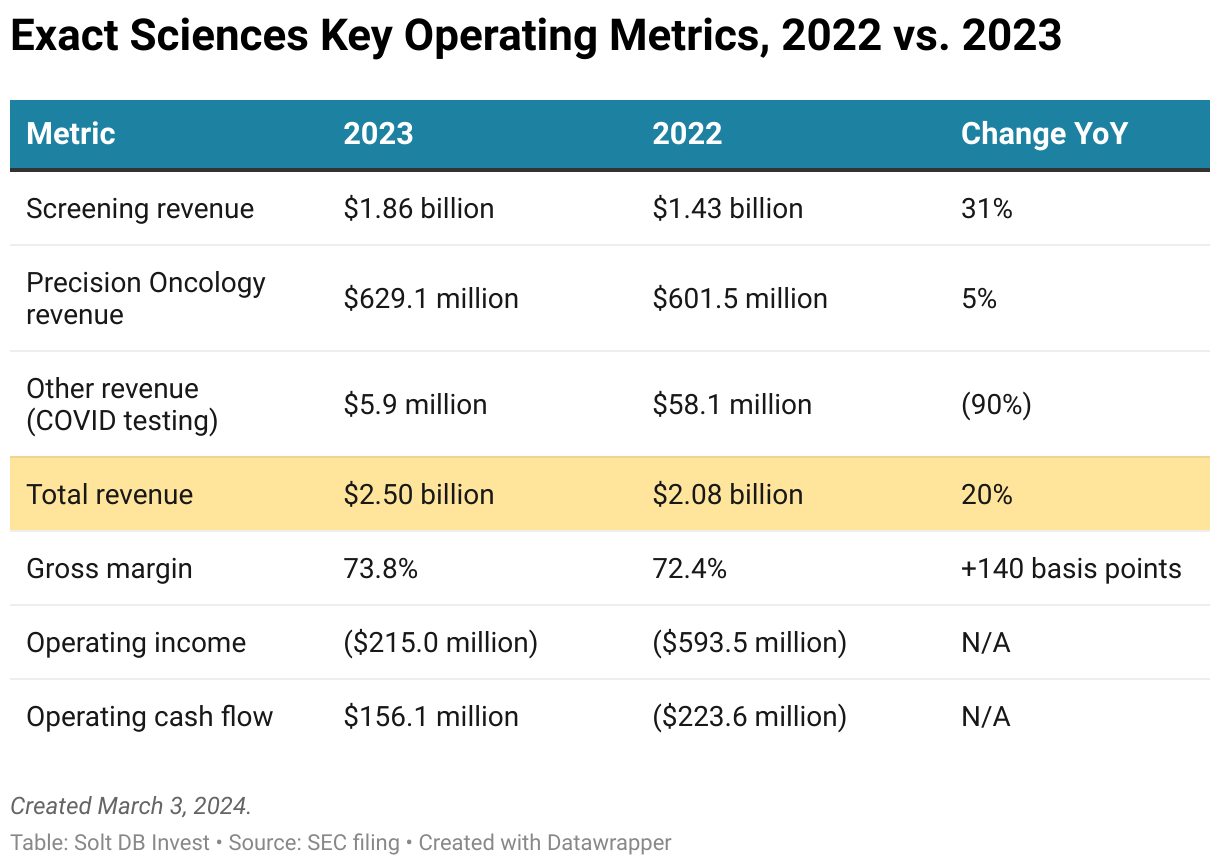

Revenue growth and improving gross margin have been a dirty combination in recent years. In 2023, Exact Sciences grew gross profit by $335.6 million and total operating expenses by only $48.8 million. That alone led to a $286.8 million improvement in operating loss – and it excludes the one-time gain from MDxHealth.

In other words, the business is not relying on accounting tricks as it marches to profitability. When will that milestone occur?

Positive operating cash flow gives management options for how to navigate the next few years, which should see multiple new product launches. If the team chooses to increase investment in strategic growth opportunities, then the business could continue to generate operating losses and still maintain positive operating cash flow. That might emerge as the new "it" metric for growth companies in the new high interest rate environment.

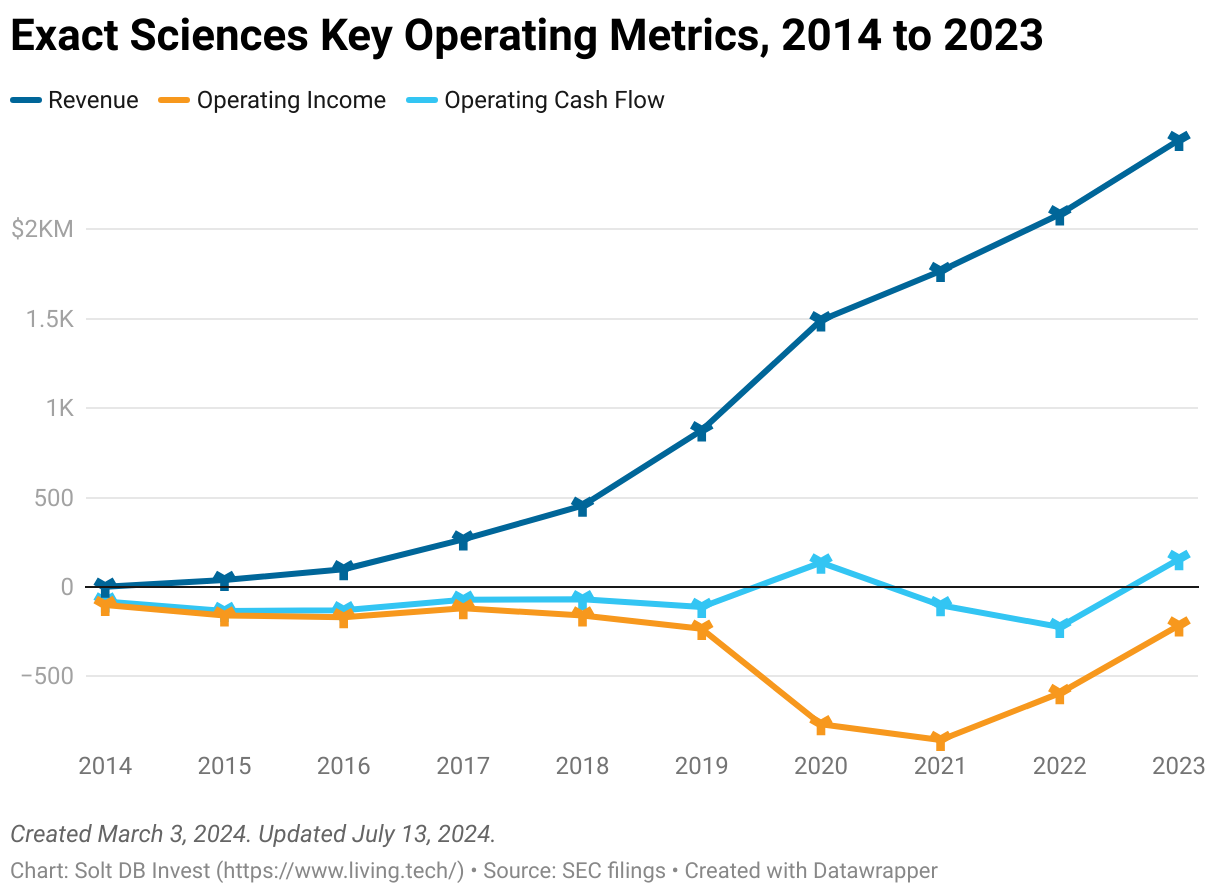

Nonetheless, my model expects the business to generate positive operating income by 2025 regardless of growth investments – at least with the information available right now. Consider a broader overview of key operating metrics from the last two years to fully appreciate how the company's scale is compounding.

If management has continued its recent tradition of lobbing up underwhelming initial guidance to crush it later, then investors can expect a "surprise" leap toward profitability. Exact Sciences might even achieve that milestone in 2024 – if the growing pool of Cologuard rescreens delivers at its historic rate of conversions.

Cologuard's Increasing Rescreen Opportunity

The U.S. Preventive Services Task Force (USPSTF) sets health guideline recommendations for physicians to follow. In 2023, the task force recommended that colon cancer screening should begin once an individual turns 45 years old, which was five years younger than the previous guideline.

That's expected to change again when the USPSTF revisits guidelines in 2026. Considering colon cancer is becoming more common in younger individuals, including those in their 30s, the age threshold for screening could drop by a decade. But that's a topic for another research note.

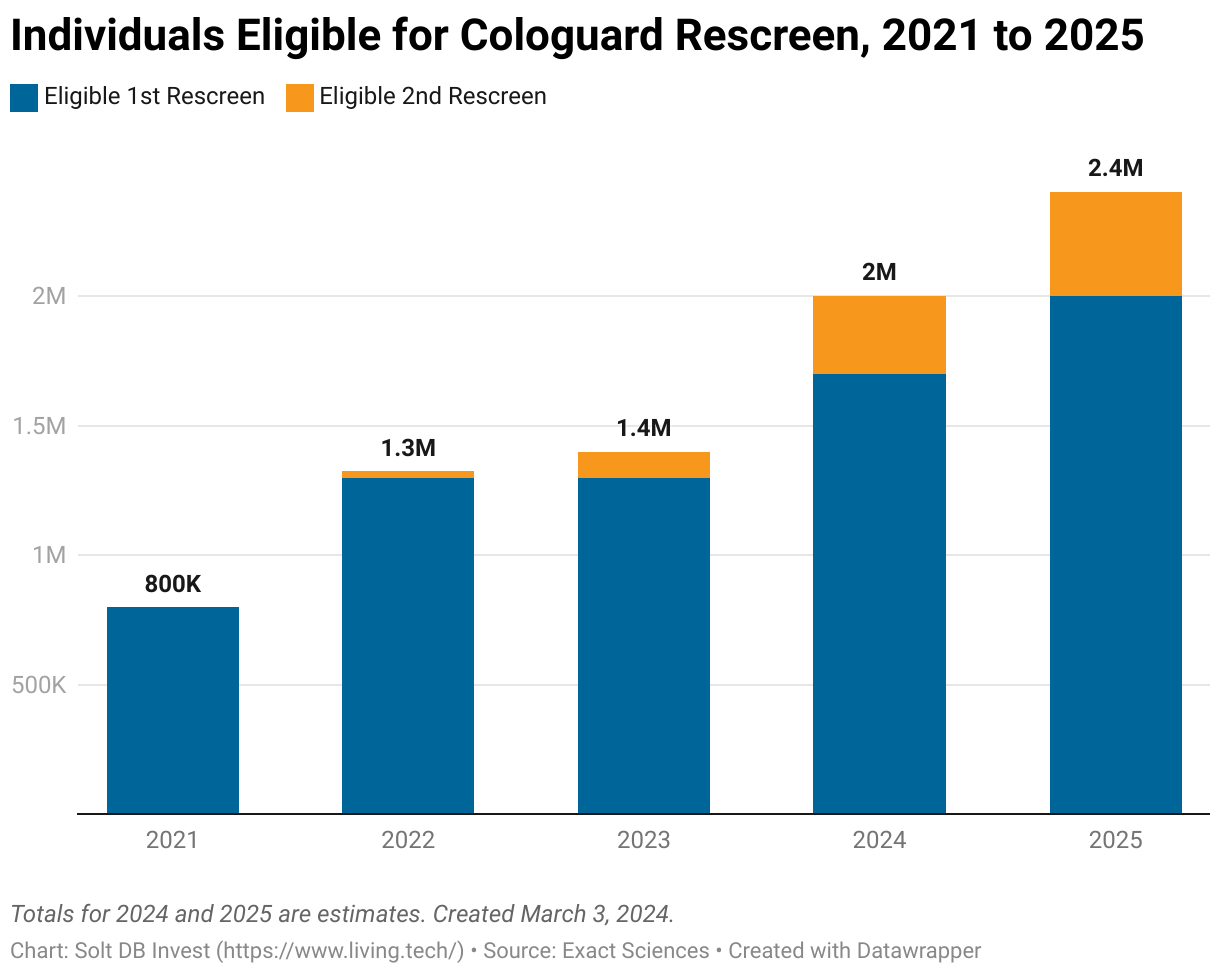

For now, if individuals receive a negative Cologuard result, then the American Cancer Society recommends getting rescreened every three years. The USPSTF and ACS recommendations work in tandem: The younger the recommended age for a first screen, the greater the number of potential rescreens over an individual's lifetime.

Rescreens are becoming an increasingly large source of revenue for Cologuard. Consider how the number of individuals eligible for a second or third rescreen is evolving.

Exact Sciences generated an estimated $220 million and $237 million in revenue from rescreens in 2022 and 2023, respectively. My model expects that to increase to at least $338.5 million in 2024 and $406.2 million in 2025. That would represent an increase of at least 85% from 2022 to 2025.

This is likely to be an underestimate for two reasons.

First, Exact Sciences reports that compliance rates increase with rescreen eligibility. Individuals see a 20% higher compliance rate for their first rescreen and a 30% higher compliance rate for their second rescreen.

Second, the improved accuracy and precision of next-generation Cologuard should lead to greater compliance for the first screen and subsequent rescreens. Both prescribing physicians and individuals should increase their trust in an improved test.

If the product earns U.S. Food and Drug Administration (FDA) approval as expected in 2024, then it should be fully rolled out in 2025. That would be just in time for a potential USPSTF guideline revision in 2026, which would go into effect in 2027.

Forecast & Modeling Insights

(Increased + Asymmetric Opportunity.)

Asymmetric Opportunity

Exact Sciences is being anointed an Asymmetric Opportunity. That might seem out of place for a $10.8 billion company, but our coveted label is intended for stocks with an unusually favorable risk-reward profile. Wall Street is ignoring just how rapidly the business could leap to profitability. The trajectory will no doubt be driven by Cologuard, although emerging products in minimal residual disease (MRD) will allow the Precision Oncology segment to return to double-digit revenue growth in 2025 and beyond. A combination of rapidly improving operating efficiency, the best damn commercial infrastructure in the landscape, multiple unrelated growth opportunities, a favorable regulatory landscape, and a relatively lowly valuation makes this a no-brainer investment near current prices for long-term investors.

Model Insights

The current Margin of Safety is based on the estimated fair value for our 2025 model. Solt DB Invest expects:

- A modeled fair valuation of $104.54 per share based on expected 2025 financials. This marks an increase from my prior fair valuation of $101.55 per share due to a lower expected share count.

- Full-year 2025 revenue of at least $3.640 billion (down from a prior estimate of $3.683 billion). This includes Cologuard revenue of at least $2.849 billion, PreventionGenetics revenue of at least $59.0 million, and Precision Oncology revenue of at least $731.5 million.

- Full-year 2025 gross margin of at least 75.5%. The increase is driven by a lower cost of goods sold from next-generation Cologuard.

- Full-year 2025 operating income of $464.6 million, although this depends on the commercialization of several new products.

Although our current model is based on 2025 financials, investors might find it useful to know the details of our 2024 model as well. This is not what the current modeled fair valuation is based on.

- A modeled fair valuation of $86.45 per share based on expected 2024 financials.

- Full-year 2024 revenue of at least $2.993 billion (vs. initial guidance of $2.830 billion).

- Full-year 2024 gross margin of at least 74.6% (vs. 73.8% in 2023).

- Full-year 2024 operating income of +/- $20 million.

I've reduced expectations for dilution, or how much the number of outstanding shares increases, due to the company's strong cash position and expectations for sustained cash flow. This assumes no additional acquisitions are made by the end of 2025.

Margin of Safety & Allocation

Exact Sciences is considered an Anchor position. The current modeled fair valuation for the company based on our 2025 model is below:

- Market close March 1: $59.44 per share

- Modeled Fair Valuation: $104.54 per share

- Allocation Range: Up to 15%

Exact Sciences reported 181.531 million shares outstanding as of February 20, 2024. The modeled fair valuation above assumes 183.500 million shares outstanding by the end of 2025, which is equivalent to 1.1% dilution.

Further Reading

- February 2024 press release announcing the latest financial results

- February 2024 regulatory filing (10-K) discussing the latest financial results

.svg)

.svg)

.png)

.svg)

.svg)

.svg)