.svg)

Cash flow is king in 2024. So, naturally, Exact Sciences decided to kick off the year with its largest operating cash outflow in two years. And its largest operating loss in five quarters.

Nice.

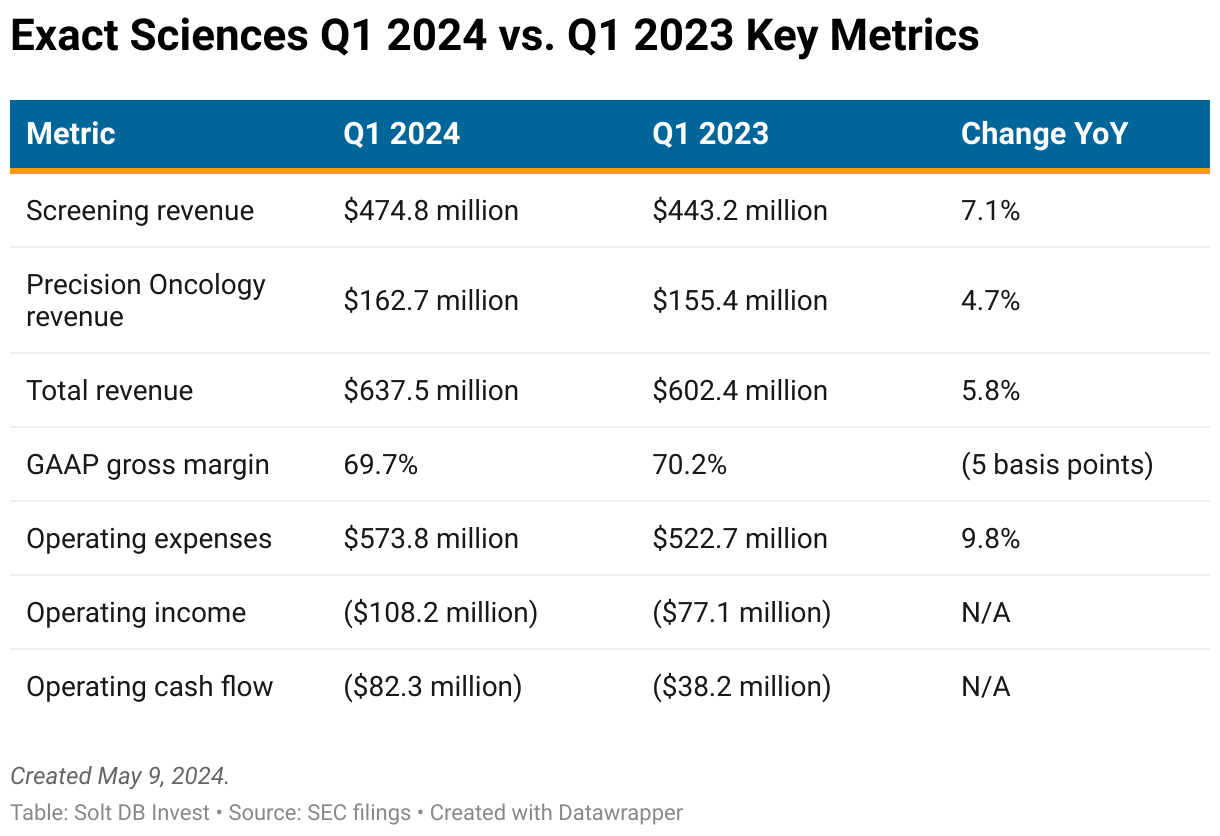

What happened? The cancer diagnostics company beat Wall Street estimates for total revenue (and came up short against my model), but the single-digit growth rate is uncommon for the business. Even if investors acknowledge the difficult year-over-year comparison due to a strong start to 2023 (when revenue surged a record 30% from the year-ago period), the larger-than-expected increase in operating expenses made for a one-two punch among key metrics.

Management spoke at length about its decision to increase investments in commercial infrastructure, including adding new sales rep, on the first-quarter 2024 earnings conference call. Internal analytics clearly demonstrate that additional touch points between sales reps and care providers results in additional revenue per account. In fact, the leverage has increased in recent years as gastroenterologist wait times for a colonoscopy now sit at 6-12 months for high-risk individuals. That's leading more health centers to use Cologuard as a first-line diagnostic for average-risk individuals – and Exact Sciences is sharing analytics to care providers to help secure more of those decisions among new and existing customers.

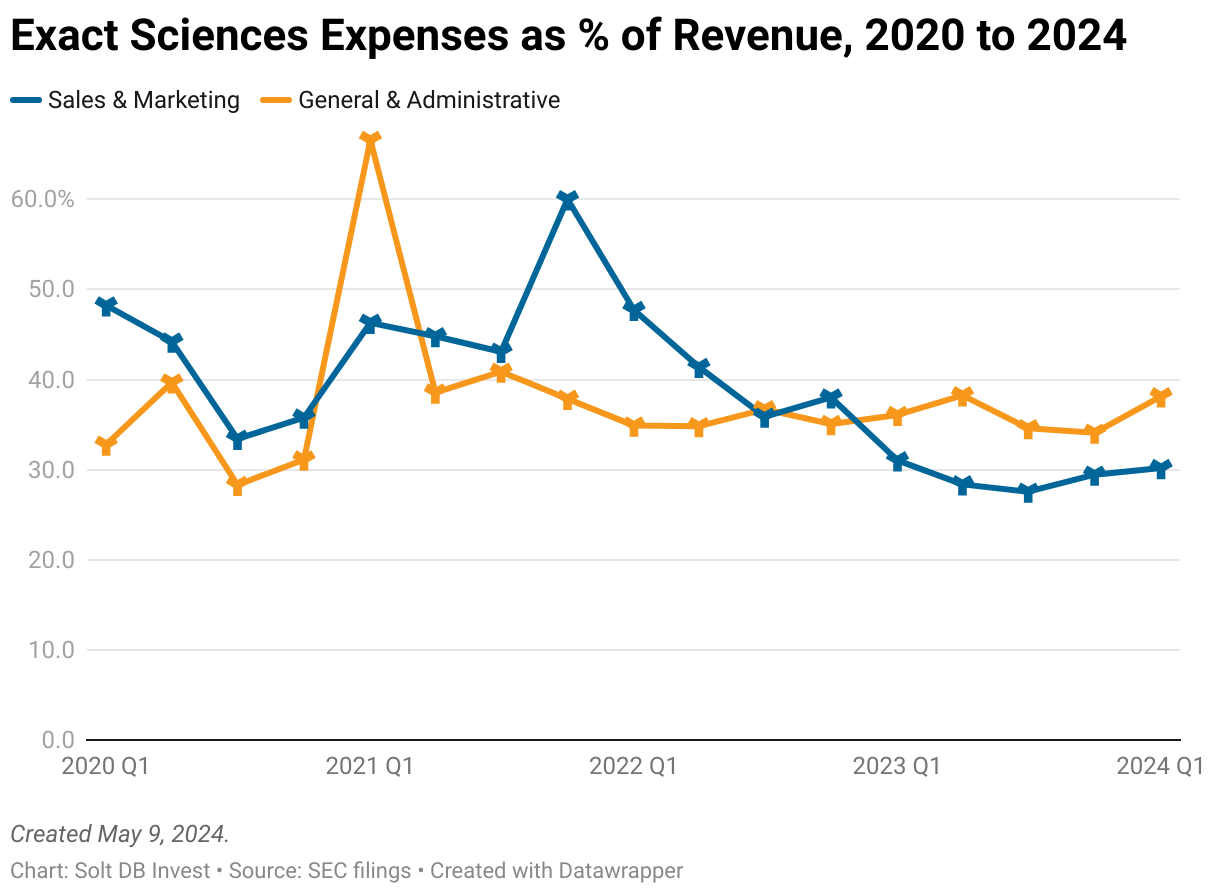

Wall Street was more focused on the "increased investments" part. But it's all relative. The new spending level marks an increase of 11% from the third quarter of 2023 – only six months ago – but is only 3% higher than spending in the first quarter of 2021.

Put more simply, Sales & Marketing represented 46.2% of revenue in Q1 2021, but only 30.2% of revenue in Q1 2024.

There are a couple trends to keep an eye on as the year progresses, but I don't see any alarming signals in the data. The business is objectively doing well.

By the Numbers

Exact Sciences faced a difficult year-over-year comparison. At the beginning of 2023, the business reduced operating expenses to prioritize operating efficiency and saw a surge in revenue from the final quarter of 2022. At the beginning of this year, the business increased operating expenses to drive operating leverage and saw a dip in Cologuard revenue from the final quarter of 2023.

The one-two punch drove the first operating loss over $100 million in five quarters and the worst operating cash flow in eight quarters. The business had delivered positive operating cash flow in five of the six prior quarters.

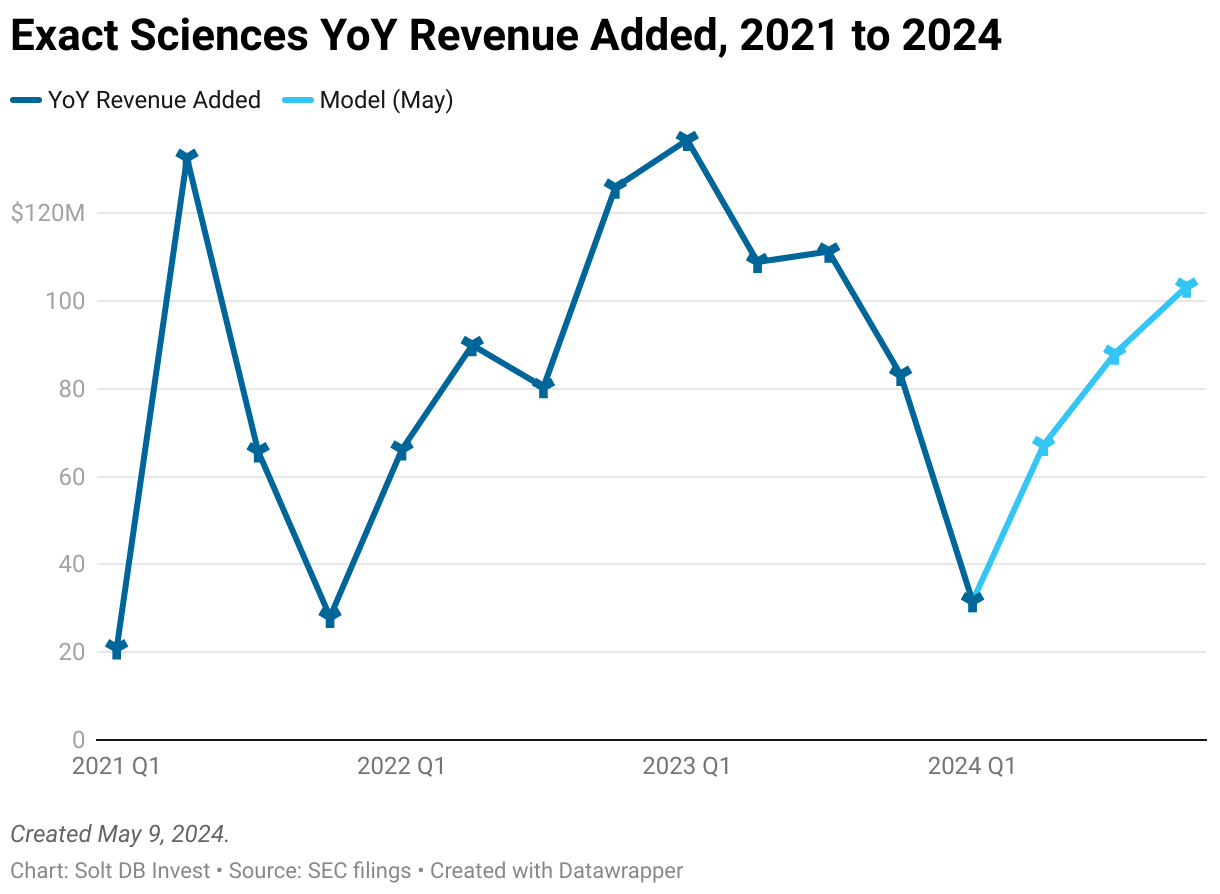

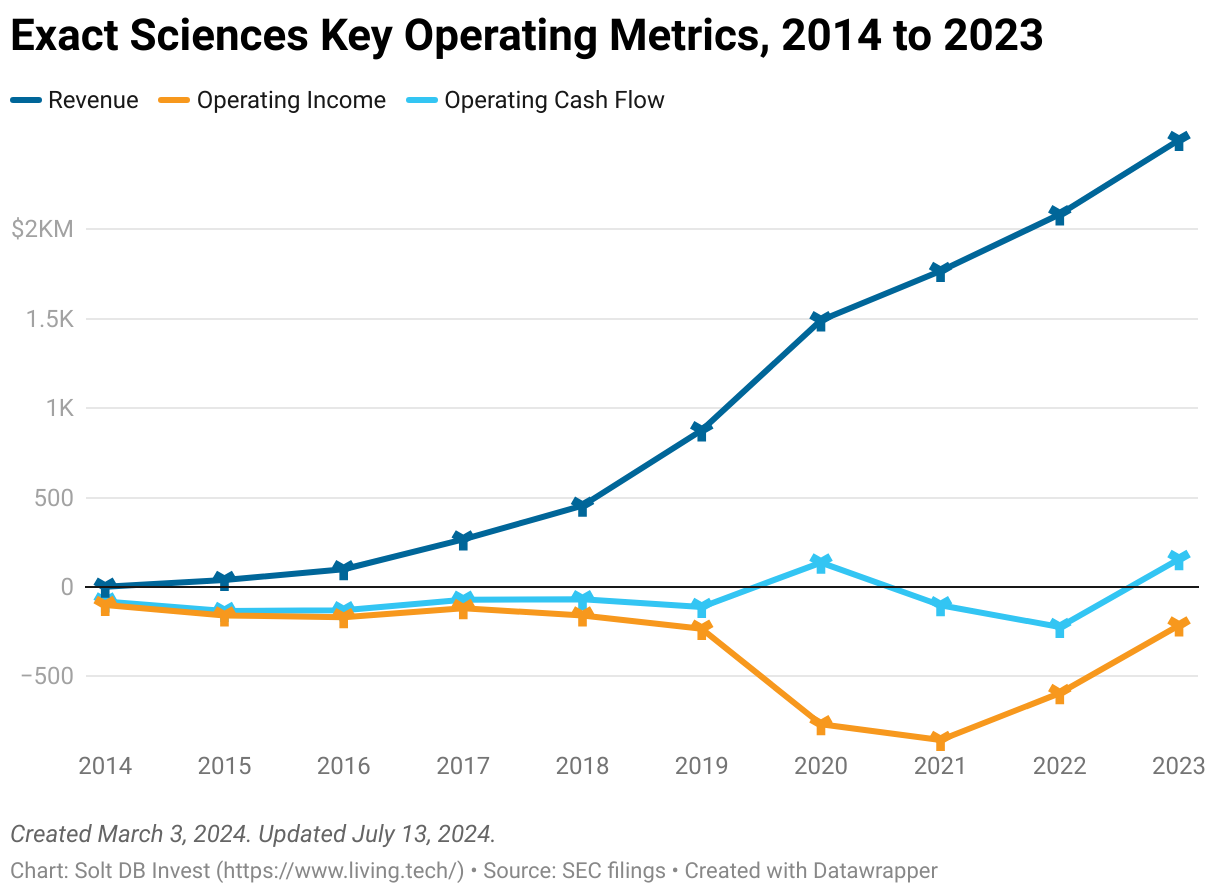

Okay, so the year-over-year comparison isn't favorable. What happens when investors zoom out for more context? The data visualizations below provide a more longitudinal view of trends in key operating metrics.

Although the cancer diagnostics company has seen revenue decline in subsequent quarters in recent years, the prior occurrences coincided with the beginning of and first winter of the coronavirus pandemic. Vaccines weren't yet available, and since Cologuard customers skew older, fewer doctor visits resulted in less revenue. A prescription is still needed for the at-home test.

Given that context, Screening revenue has now been flat for three consecutive quarters. That's a trend to keep an eye on, but it's not (yet) alarming. Exact Sciences has guided for Q2 2024 revenue of $527 million from the segment, which would represent year-over-year growth of 14% -- in line with historical growth rates.

Penciling in expected growth rates for the second half of 2024 shows a return to historical growth expressed as total revenue added year over year. Note that full-year 2024 revenue guidance aligns with my model.

As for increasing operating expenses, management is responsibly managing both Sales & Marketing expense and General & Administrative expense as a percentage of revenue. I'll be more focused on the latter for the remainder of 2024, especially since managerial overhead can be a key source of operational bloat. Both categories are expected to decline as a percentage of revenue in subsequent periods this year.

R&D expenses have been essentially flat near $110 million per quarter since Q1 2021, so I've excluded the category from the chart below to reduce clutter.

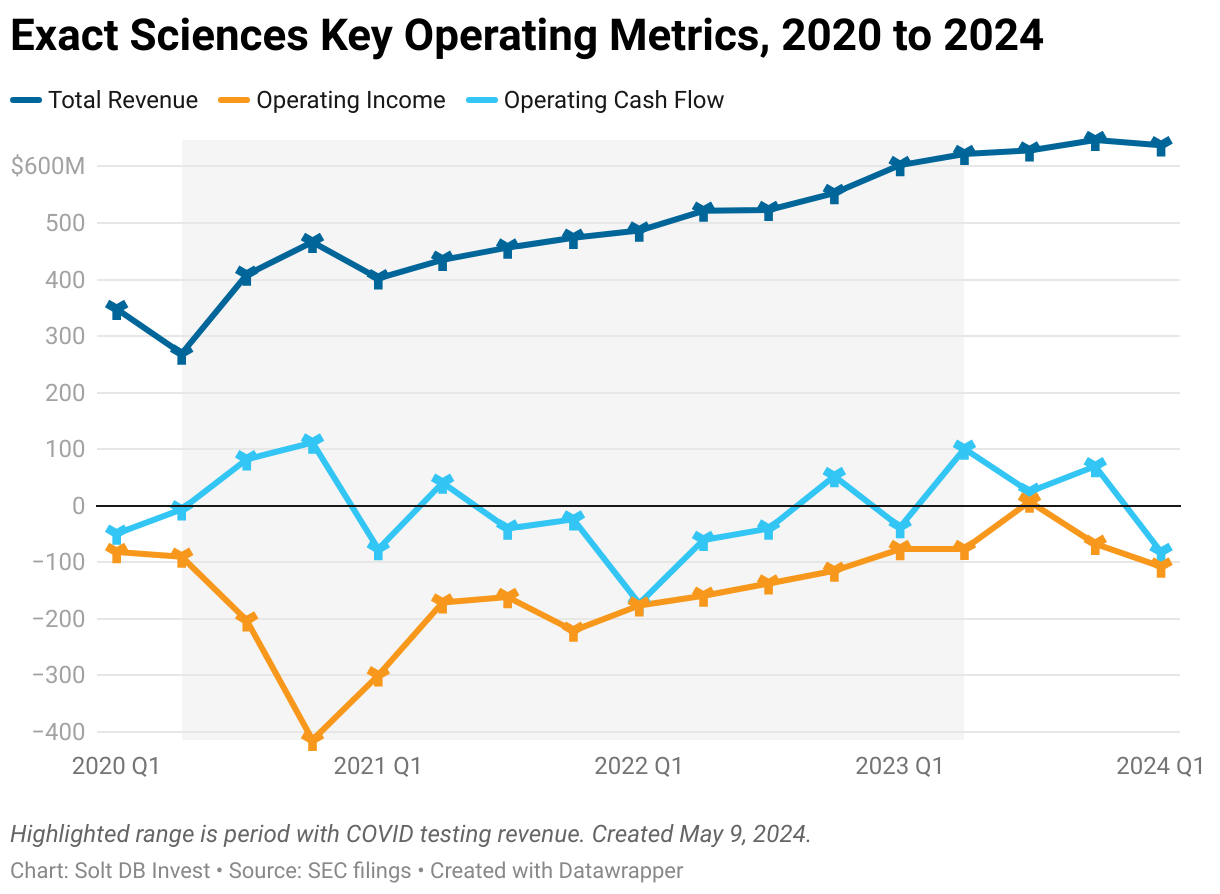

There are no alarming signals in key operating metrics over time, either. Looking at quarterly revenue, operating income, and operating cash flow shows an improving trend since the beginning of 2020. Note that investors cannot separate the impact of COVID testing revenue from operating income and cash flow in that span.

Whether any alarming signals appear depends on meeting full-year 2024 revenue guidance. If Exact Sciences delivers in Q2 2024, then it will return to an improving operating loss and positive cash flow. Management expects revenue growth to accelerate in each subsequent period of 2024 as it realizes increasing operating leverage from the sales team. Looking at the longer-term trend using annual performance provides additional confidence in the company's ability to deliver.

Forecast & Modeling Insights

(Reduced 2024 and 2025 models)

Solt DB Invest is reducing its 2024 and 2025 models for Exact Sciences to account for a slightly lower growth trajectory.

Highlighted metrics from the updated 2024 model:

- Full-year 2024 revenue is now expected to be $2.902 billion vs. a prior model of $2.993 billion (-3%). The company's guidance has a midpoint of $2.832 billion.

- Full-year 2024 operating expenses are now expected to be $2.333 billion vs. a prior model of $2.216 billion (+5%). This results in an operating loss of $100 million vs. a prior model for operating income of $16.3 million.

Highlighted metrics from the updated 2025 model (the Margin of Safety is based on this model):

- Full-year 2025 revenue is now expected to be $3.420 billion vs. a prior model of $3.640 billion (-6%).

- Full-year 2025 operating expenses are now expected to be $2.401 billion vs. a prior model for $2.282 billion (+5%). This results in operating income of $345 million vs. a prior model of $464 million.

Negative impact: The number of shares outstanding jumped in Q1 2024 due to an exchange of senior debt notes. Exact Sciences reported 184.529 million shares outstanding as of May 7, 2024, up from 181.530 million shares outstanding on February 20, 2024.

Positive impact: The net impact of the debt exchange transactions was a $266.8 million increase in the company's cash position. This settled after the end of Q1. As a result, the business started April 2024 with approximately $918 million in cash vs. the $652.1 million reported for the end of March 2024.

The surge in cash (albeit partially offset with dilution) helps to neutralize most of the negative impact of increased spending and operating losses in my updated model.

Margin of Safety & Allocation

Exact Sciences is considered an Anchor position. The current modeled fair valuation for the company based on my 2025 model is below:

- Market close May 8: $59.48 per share

- Modeled Fair Valuation: $96.61 per share (vs. $104.54 per share previously)

- Allocation Range: Up to 15%

Exact Sciences reported 184.530 million shares outstanding as of May 7, 2024. The modeled fair valuation above assumes 186.4 million shares outstanding, which is equivalent to 1% dilution.

Further Reading

- May 2024 press release announcing Q1 2024 operating results

- May 2024 regulatory filing (10-Q) detailing Q1 2024 operating results

- March 2024 research note analyzing full-year 2023 operating results and the impact from Cologuard rescreens

.svg)

.svg)

.png)

.svg)

.svg)

.svg)