.svg)

Money talks. And right now, it can't say enough good things about Exact Sciences.

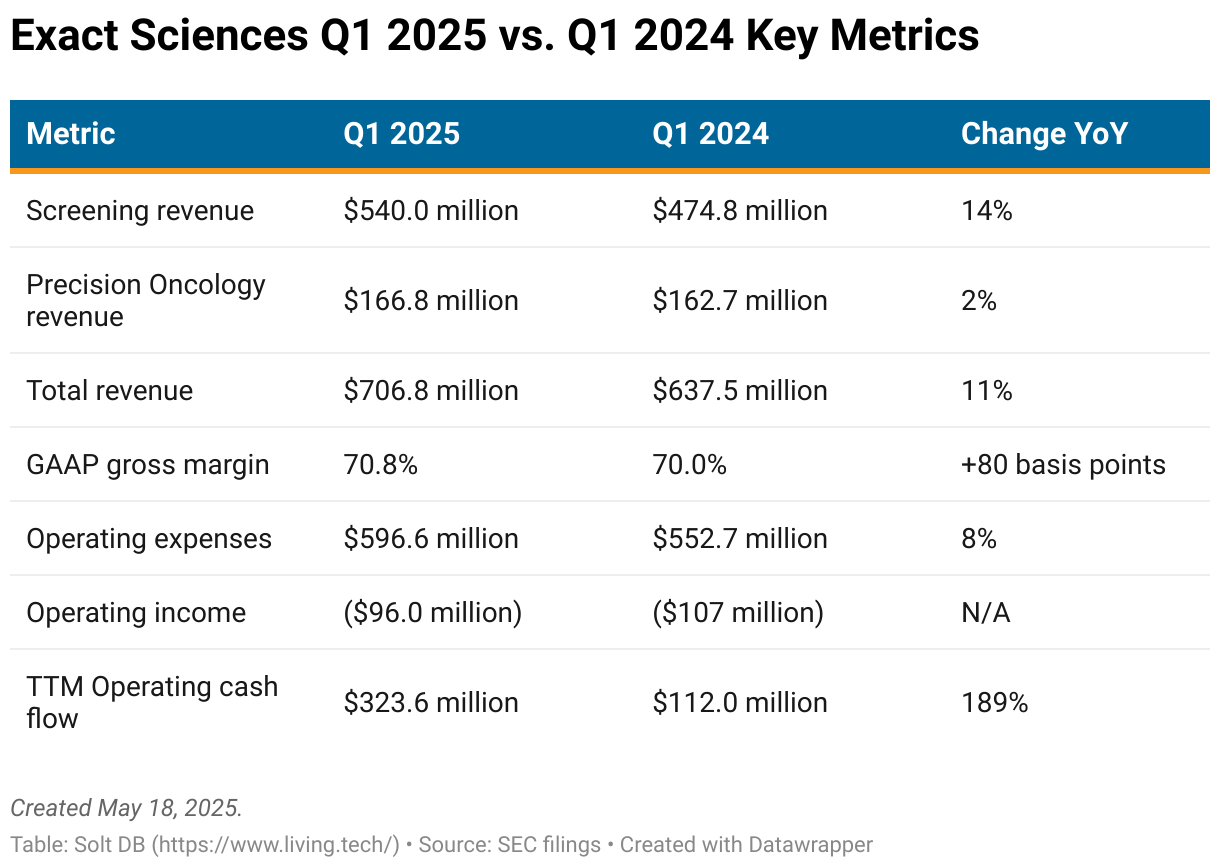

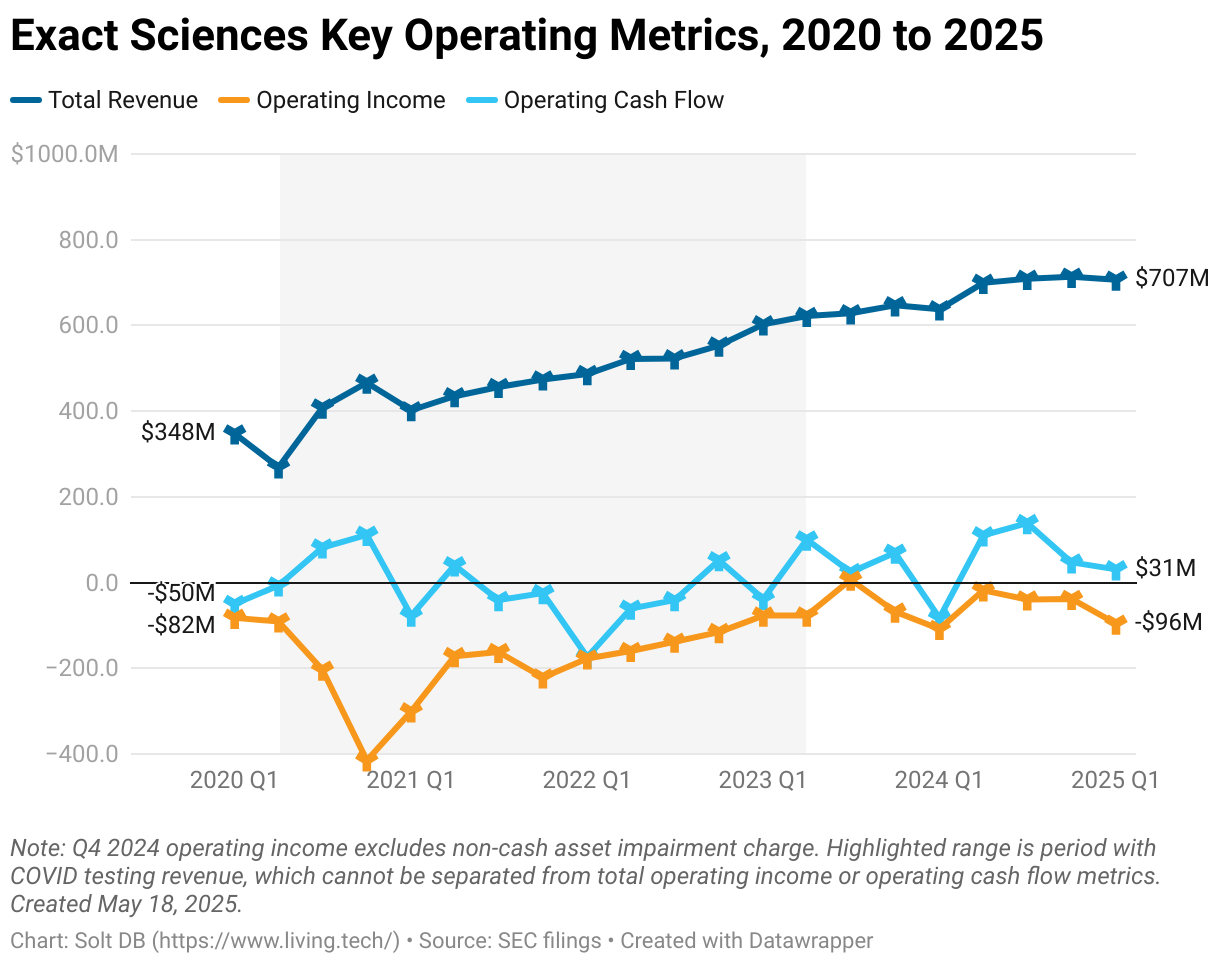

The business generated positive operating cash flow in the first quarter of a calendar year for the first time in its history. In the last 12 months, the owner of Cologuard generated $323 million in cash from operations, an increase of 189% from the prior-year period. That means it converted an incredible 11.4% of revenue in that span into cold hard cash.

Exact Sciences is so financially confident that it paid off $250 million in convertible debt that came due in January 2025 with cash on hand. It still exited March with $786 million in greenbacks.

The timing couldn't be better considering the lingering economic uncertainty, which could lead to another wave of bankruptcies and consolidation across the genetic diagnostics landscape. That's not the only reason.

For the last several years, Exact Sciences has been developing new product candidates across molecular residual disease (MRD), liquid biopsies, and sample preparation and processing. A significant portion of the pipeline graduates this year.

The second-generation multi-target stool DNA (mt-sDNA) test, Cologuard Plus, launched in March 2025. The first of several tissue-informed tests from the company's MRD platform, Oncodetect, launched in April 2025. Investors are eagerly awaiting the final pivotal data readout from BLUE-C this summer, which will immediately be compared to Guardant Health's Shield in blood-based screening for colon cancer.

The business is also on track for a soft launch of its multi-cancer early detection (MCED) product, Cancerguard, in the second half of the year. The first product will be launched as a laboratory-developed test (LDT), meaning it won't have reimbursement in place, and go by the distinct brand name Cancerguard EX. Analysts will see how it stacks up against Galleri from GRAIL and Shield (distinct product, same name) from Guardant Health.

Launches don't always go smoothly, and the competitive landscapes are relatively crowded. Both are expected for new and significant market opportunities. Luckily, Exact Sciences is the only business in the landscape with positive cash flow and the only one within 12 months of profitability. It still needs to stick the landing. Er, landings.

By the Numbers

Exact Sciences delivered a strong start to 2025 powered by a familiar growth driver: the Screening segment. The business unit anchored by Cologuard grew 14% year over year, a sharp contrast to the Precision Oncology segment's 2% improvement.

The Precision Oncology segment is anchored by Oncotype Dx, which is the leading therapy selection diagnostic globally for breast cancer. Being disappointed in a globally dominant tool reaching peak revenue is a good problem to have, but it sure would be nice to diversify the sources of growth.

Investors ruminating on that can pull themselves out of the doldrums by remembering Cologuard has a peak annual sales opportunity of at least $7.2 billion. If it meets guidance this year, then it will have secured about one-third of that. There's plenty of room for future growth.

In the first quarter of 2025, revenue grew faster than operating expenses – and at an incrementally higher margin to boot. Still, operating loss is always steeper in the first quarter of each year as the business renews technology licenses, vendor relationships, and so on.

Despite the gusher of cash flow, investors need to keep an eye on several potential warning signs in the company's operating footprint.

Exact Sciences is no longer enjoying steady sequential revenue growth. It has reported between $699 million and $713 million in total quarterly sales in the last four quarters – relatively flat. That's been offset by strengthening cash flow and manageable operating losses primarily driven by non-cash charges.

Wall Street analysts don't appear to be too concerned. It helps that management increased full-year 2025 revenue guidance to a midpoint of $3.105 billion, meaning the business would need to average $799 million in quarterly revenue in the next three quarters. That would mark a step change in the growth profile and alleviate any concerns about slowing growth. But things could get ugly if the business doesn't deliver.

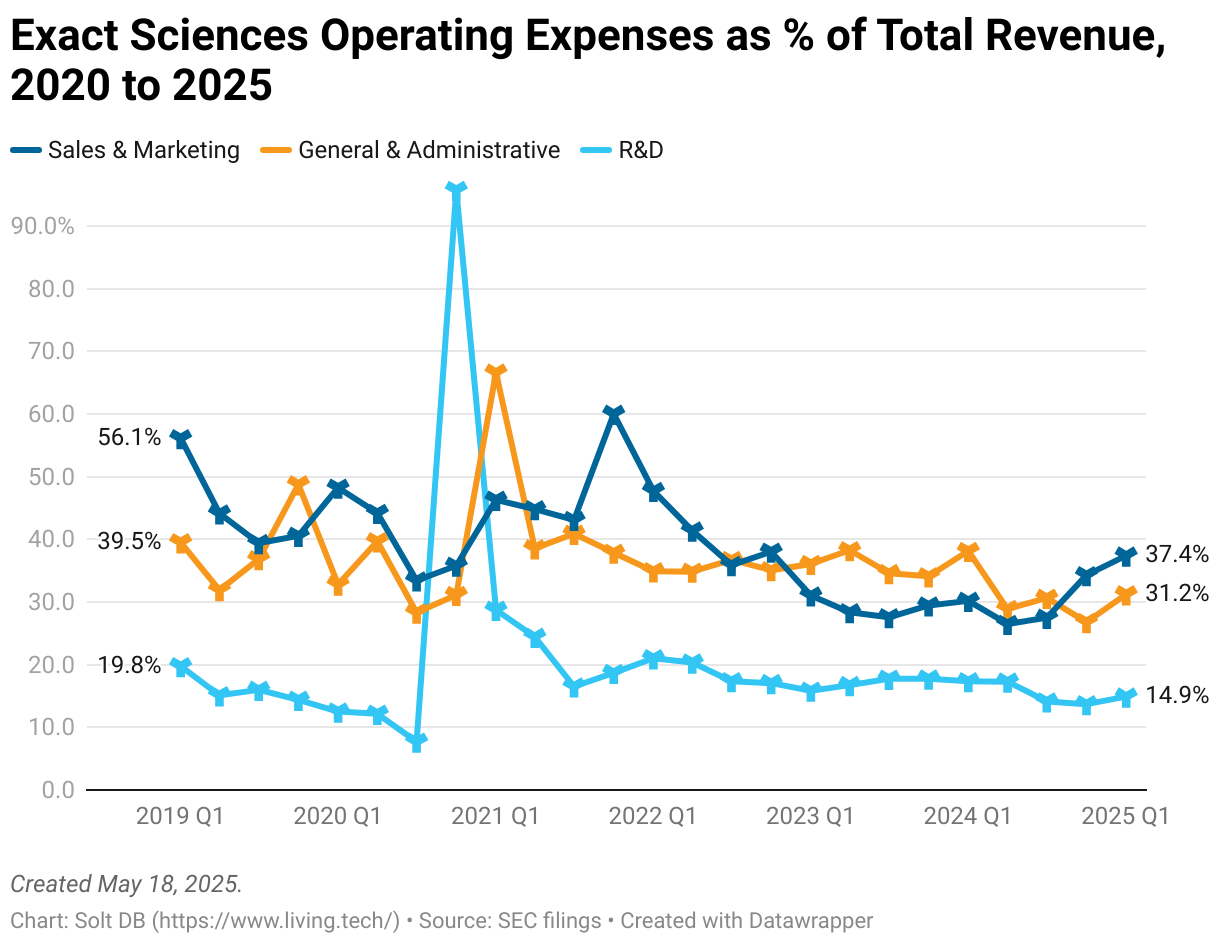

Another reason to man the watchtower: Exact Sciences is increasing investments in its commercial footprint at a noticeably sharper pace than recent years.

Let's be blunt: this isn't AVITA Medical. The Cologuard owner can easily fund an expanded sales team, higher marketing spend, and investments in commercial readiness for four recent and upcoming launches. I might be worried if expenses didn't increase.

Investors simply need to remember that the return on investment has to materialize. The surge in expenses must deliver growth and productivity gains in a meaningful period of time, which likely extends through the end of 2026 to nurture launches and ramps. If it doesn't, then the share price will be stuck in neutral.

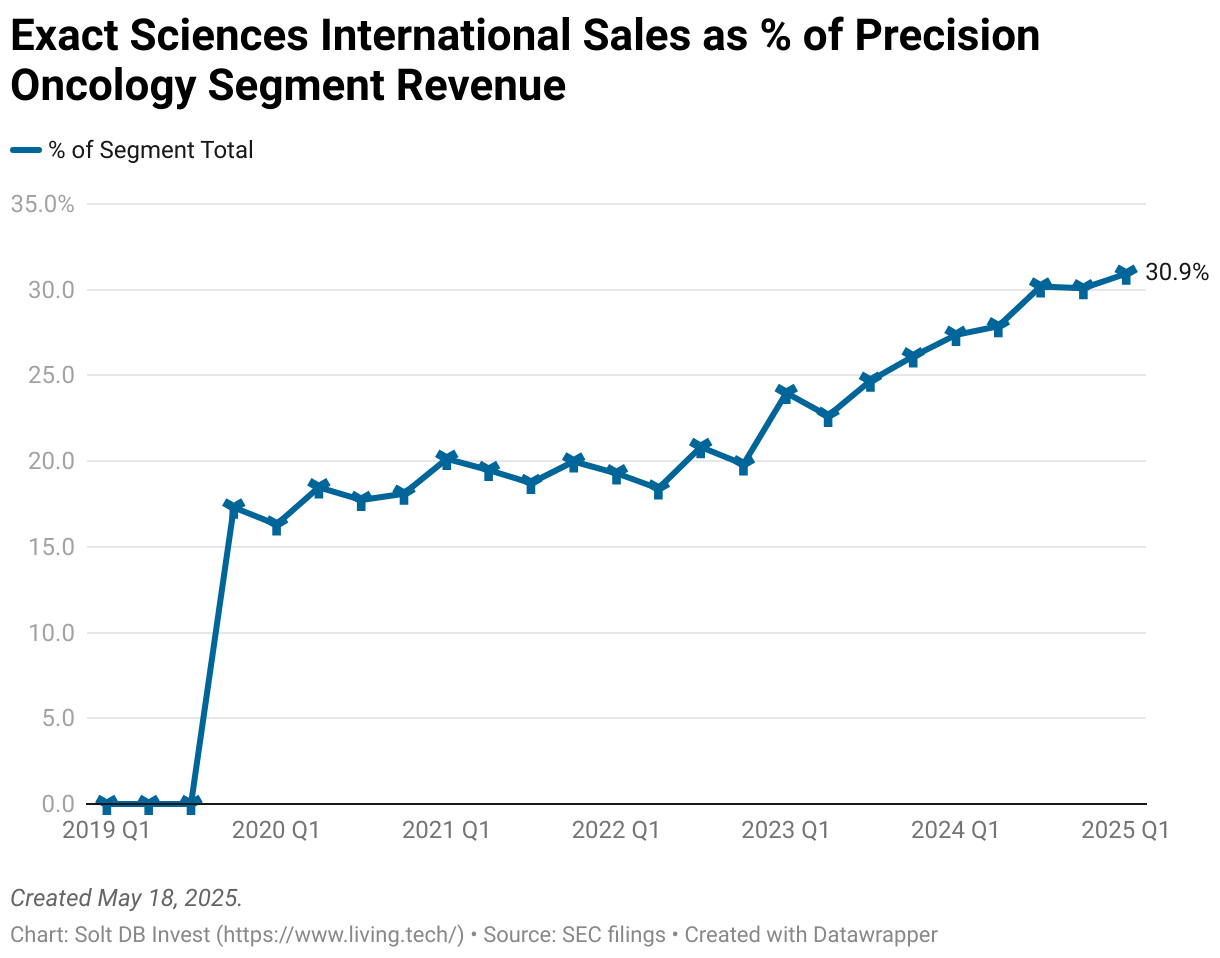

To end on a positive note, the Precision Oncology segment continues to expand internationally. Aside from annual price increases, most incremental growth for the unit's flagship Oncotype DX will come from ex-U.S. markets.

Around the Horn

This will be a busy year for Exact Sciences. Investors can expect one new product launch each quarter, while the competitive landscape is increasingly active too. Let's dig a little deeper into the expanding product portfolio and broader throwing of elbows.

Cologuard Plus launch and patent infringement

The next-generation mt-sDNA diagnostic launched in March 2025. Exact Sciences is prioritizing the highest-value accounts for the initial rollout and will gradually expand from there. It's expected to take until the end of 2026 to exhaust inventory of the prior-generation product.

Cologuard Plus improves the performance of the company's mt-sDNA offering, is accompanied by a lower cost of goods sold (COGS), and enjoys a 16% higher selling price than its predecessor. It's the most accurate non-invasive colon cancer screening tool available.

It's not alone though.

ColoSense, an mt-sRNA (not DNA) diagnostic product from Geneoscopy being commercialized with LabCorp, offers an equivalent performance to Cologuard Plus.

One way to rank screening tools is to multiply the sensitivity, specificity, and precancerous lesion sensitivity. A colonoscopy is unmatched at 0.4902. That will be difficult to beat without significant advances in sample preparation and processing, primarily owing to the difficulty of detecting genetic signals shed by precancerous lesions in stool or blood. Cologuard Plus offers a respectable 0.3678, while ColoSense offers 0.3683 – equivalent from a clinical perspective.

Exact Sciences has sued Geneoscopy for allegedly infringing on two patents. A court will issue a ruling on one claim by July 26, while the second will be ruled on by February 14, 2026.

There's not much at stake for Cologuard Plus.

- If a court rules in favor of Exact Sciences, then it will make it more difficult for Geneoscopy to sell its product or force it to pay royalties.

- If a court rules in favor of Geneoscopy, then the two companies get to compete with equivalent products for 106 million American patients.

Geneoscopy will not be the last company to bring a mt-sDNA or mt-sRNA product to market. Mainz Biomed and Prescient Metabiomics are attempting to get their slice of the pie, too. This is an absolutely massive market opportunity. There's going to be plenty of competition. That's a good thing for patients, you greedy little monopolist investor you.

And if you're still concerned, then remember Exact Sciences is already developing Cologuard 3.0 with an expanded slate of multi-omics signals.

Liquid biopsy colon cancer screening tool

Speaking of the colon cancer screening landscape, stool-based tests aren't the only option. The U.S. Food and Drug Administration (FDA) has approved multiple liquid biopsy screens, which look for genetic signals of tumors and precancerous lesions in a patient's blood. While Epi proColon was the first to launch, it was withdrawn from the market after failing to secure Medicare coverage.

Guardant Health developed a more complete tool in Shield, which is expected to generate full-year 2025 revenue of at least $40 million. That's likely a sharp underestimate. The liquid biopsy screening tool has also significantly outperformed all expectations for reimbursement.

Whereas analysts thought it could secure nearly $300 per test, Shield is enjoying an astronomical $1,495 per test – almost 3x Cologuard Plus. The initial reimbursement rate is expected to fall precipitously after favorable pricing for new tests expires. Worse, Guardant Health might have to pay back the difference to the government.

Although investors have been worried about the competition between Cologuard Plus and Shield (or stool vs. liquid generally), these diagnostics aren't competing for the same customers. One is administered at the point of care in a doctor's office, the other is administered at home.

They also differ sharply in accuracy. Liquid biopsy tools struggle to detect genetic signals from precancerous lesions, which can mature into cancerous tumors. That limits the market opportunity and (in theory) reimbursement rates.

Exact Sciences will share data from the pivotal study of its own liquid biopsy tool this summer. In a case control study, meaning using the diagnostic against patient samples in a lab, the developmental tool outperformed Shield and delivered what would be the highest-ever precancerous lesion sensitivity for a liquid biopsy.

Here's the table again so you don't have to scroll back up.

An important nerdy detail: Case control studies always overestimate a tool's real-world performance. That's because sample stability decays in the time between removing biomaterials (tissue, blood, stool) from a patient to processing them in a clinical lab. But Exact Sciences has a favorable margin to work with.

- In its pivotal study, Shield delivered a sensitivity of 83%, specificity of 90%, and precancerous lesion sensitivity of 13%. The combined metric was 0.0971 – the lowest ever for an approved colon cancer screening tool.

- In its case control study, Exact Sciences' unbranded challenger delivered a sensitivity of 88%, specificity of 90%, and precancerous lesion sensitivity of 31%. The combined metric would've been 0.2455 -- that would be the highest ever for a blood-based colon cancer screening tool.

Investors can expect Exact Sciences to at least match the sensitivity of Shield, fall a few ticks below it on specificity, and likely outperform on precancerous lesion sensitivity. If it holds its own on the first two metrics and delivers a significant improvement on the final metric (24% or higher), then that could be disastrous for Guardant Health.

Another important nerdy detail: precancerous lesion sensitivity will see the sharpest drop off from the case control study. This is where a long-forgotten acquisition might give Exact Sciences a sneaky edge.

In October 2018, the company acquired Biomatrica, which developed special blood tubes capable of better preserving genetic material before processing. Compared to commercially available blood tubes, LBgard tubes can increase plasma yield (plasma is the component of blood that contains cell-free DNA) by 109% and decrease DNA contamination by 52% through 10 days.

Exact Sciences used to sell LBgard tubes to competitors, but "suddenly stopped" as it "expands their use for more applications." Wink wink.

Oncodetect (tumor-informed MRD)

In April 2025, Exact Sciences launched the first Oncodetect diagnostic. The molecular residual disease (MRD) tool is bespoke, designed using the genetic signatures of an individual cancer survivor's tumor. It can then be used for years of surveillance to detect the first molecular signals that a cancer is coming back – up to two years before imaging diagnostics detect recurrence. That allows doctors to restart treatment in the earliest stages of disease, when cancer is the easiest to treat.

A patient with a positive Oncodetect result is 50x more likely to relapse than one with a negative result.

The test has reimbursement in place. Although the first launch was in colon cancer, investors can expect a steady cadence of launches in other tumor types in the next few years.

The emerging market opportunity for MRD tools is meaningful, but smaller than for Cologuard and with significantly more competition.

- The company's flagship product has a market opportunity of $18 billion total. MRD tools have an estimated market opportunity of $15 billion across all tumor types.

- Cologuard has to compete against two commercial products. Oncodetect has to compete against Natera, Guardant Health, Tempus AI, NeoGenomics, Myriad Genetics, Quest Diagnostics, Personalis, and over one dozen emerging startups.

The current state-of-the-art for MRD technology is also limited by requiring a tissue sample from a patient's tumor. Not all cancer survivors have tumor samples available, or enough to be used across all follow-up diagnostics.

Natera and others are developing tissue-free MRD tools, but the approach won't work for all tumor types in the near term.

Cancerguard (MCED)

Exact Sciences plans to launch its multi-cancer early detection (MCED) liquid biopsy tool before the end of 2025. This will launch as a laboratory developed test (LDT), which is ineligible for reimbursement. Cancerguard EX will instead primarily be used to build brand awareness, gather real-world feedback from doctors and patients, and generate data to supplement a future potential approval. A massive, long-term pivotal study enrolling tens of thousands of patients is required first.

The company's MCED tool comes primarily from its largest-ever acquisition of Thrive Earlier Detection for $2.15 billion in October 2020. Although Thrive previously had the best MCED technology platform, more recent real-world data show it's a step behind Galleri from GRAIL.

Galleri is expected to generate full-year 2025 revenue of roughly $140 million, but at a negative gross margin. It's also sold as an LDT.

It makes sense for Exact Sciences to launch now – without reimbursement – and build brand awareness. Unlike competitors, it can eat breakeven or minor losses on Cancerguard EX and essentially consider it a long-term marketing expense. After all, the market opportunity for MCED tools could be as large as $25 billion. Why not start laying the foundation?

Just keep in mind: no one is quite sure if the current crop of products will ever earn premarket approval (PMA) from the FDA, which is needed to earn reimbursement. I'm certainly not confident in the market's prospects as I write this in May 2025. Let's be patient as data accrue and payers weigh in.

Cologuard Mini (not the actual name)

A smaller version of Cologuard, internally dubbed "Cologuard 2.5," is in development. Exact Sciences heard from customers that a smaller kit would be appreciated. If individuals are on the go or at work, then the current kit is relatively bulky. It's difficult to hide or simply bring with you when you leave the house.

Cologuard Mini is designed to address those concerns. It's small enough to fit into a small purse or even your pocket, which the company thinks could help incrementally increase screening rates for mt-sDNA tools. Additionally, a smaller footprint means lower COGS, which should translate into higher margins.

The developmental product is not expected to become the dominant kit form factor, but it could add incremental growth and make it easier to get screened.

Modeling Insights

(No change.)

My current model for Exact Sciences remains unchanged from February 2025. Management increased guidance in May 2025, which brings expectations closer to my model.

My current 2025 model for Exact Sciences assumes:

- Full-year 2025 revenue of $3.128 billion, representing year-over-year growth of 13.4%. The company's guidance expects $3.105 billion at the midpoint (increased from $3.065 billion previously).

- Screening revenue of $2.444 billion, representing year-over-year growth of 15.9%. The company's guidance expects $2.407 billion at the midpoint (increased from $2.370 billion previously).

- Precision Oncology revenue of $684 million, representing year-over-year growth of 4.5%. The company's guidance expects $687.5 million at the midpoint (increased from $685 million previously).

- Gross margin of 70.5%, marking an improvement from 69.5% in 2024.

The business could flip to positive operating income during quarterly periods in 2025, but it's difficult to confidently model expenses given the avalanche of product launches. The timing isn't that important for this long-term position, which is considered an Anchor position (or a Current Compounder in the June 2025 update for Solt DB Invest).

I'd rather have the launches go smoothly and the company lose money. If the company succeeds in providing Cologuard some help as the lone growth driver (unlike the Pittsburgh Pirates and Paul Skenes), then investors can expect a healthy earnings yield within the next few years.

One minor change: I now expect dilution to increase 2% from the prior year, up from 1% in the prior model. This better reflects the historical average. That reduces the modeled fair value to $85.69 per share, a slight decrease from $87.88 per share previously.

Margin of Safety & Allocation

Exact Sciences is considered an Anchor position. The estimated fair valuation based on my current model is below:

- Market close May 19: $56.94 per share

- Modeled Fair Valuation: $85.69 per share

- Allocation Range: Up to 15%

Exact Sciences reported 188.638 million shares outstanding as of April 30, 2025. The modeled fair valuation above assumes 192.410 million shares outstanding, which is equivalent to 2% dilution.

Further Reading

- May 2025 press release announcing Q1 2024 operating results

- May 2025 regulatory filing (10-Q) detailing Q1 2024 operating results

- April 2025 research note (Members Digest) previewing Q1 2025 earnings across the coverage ecosystem

- February 2025 research note evaluating full-year 2024 operating results and the year ahead

.svg)

.svg)

.png)

.svg)

.svg)

.svg)