.svg)

AVITA Medical faced a no-win situation heading into second-quarter 2025 earnings.

After missing a series of internal guidance estimates in the last 18 months, even if the business performed well, how could investors possibly be confident it marked a permanent upswing? It needed multiple quarters of solid execution.

If the business performed poorly and failed to address its dwindling cash runway, then it might have been close to game over.

Unfortunately, it's looking like the latter – and the company is standing in front of the pinball machine and down to its last quarter.

Although that makes the analogy work, the business might literally only have $0.25 pretty soon.

AVITA Medical does appear to have been swept up in policy changes from the new federal administration. However, a deeper look at the numbers shows that it's a bit too convenient of an excuse. Revenue for the flagship ReCell brand has declined for three consecutive quarters now beginning in the fourth quarter of 2024. That predates the new administration.

The business exited June with just $15.7 million in cash. It's averaged a quarterly cash burn of $9.5 million since ReCell revenue began falling, which means AVITA Medical will run out of money before the end of the year. Curiously, management seemed ambivalent about the situation on the quarterly conference call.

The company sounds much less optimistic in SEC filings.

We are actively evaluating strategies to obtain the required additional funding for future operations. These strategies include, but are not limited to, obtaining additional equity financing, issuing debt or entering into other financing agreements. We intend to raise capital through the issuance of equity securities.

Management curtailed full-year 2025 revenue guidance from a previous midpoint of $103 million to a new midpoint of $78.5 million. In May, my model was lowered to full-year revenue of just $78.514 million. But there's no consolation in correctly modeling a business' implosion in real time.

Any remaining shareholders should understand the situation. AVITA Medical doesn't have great options to raise capital right now aside from ceding more control to OrbiMed. Getting acquired out of desperation, either by a fund or commercial peer, usually occurs at a valuation of 1x annual revenue or less. It could possibly sell the vitiligo asset rights, but that might only raise another quarter or two of cash at most.

Even if the business pulls through and survives, there's unlikely to be much benefit from stubbornly holding onto positions. If the business fails, then that would be a very disappointing outcome for a wound care product that objectively improves care.

By the Numbers

If you think the business has been in rough shape, then don't look ahead. It's about to get worse.

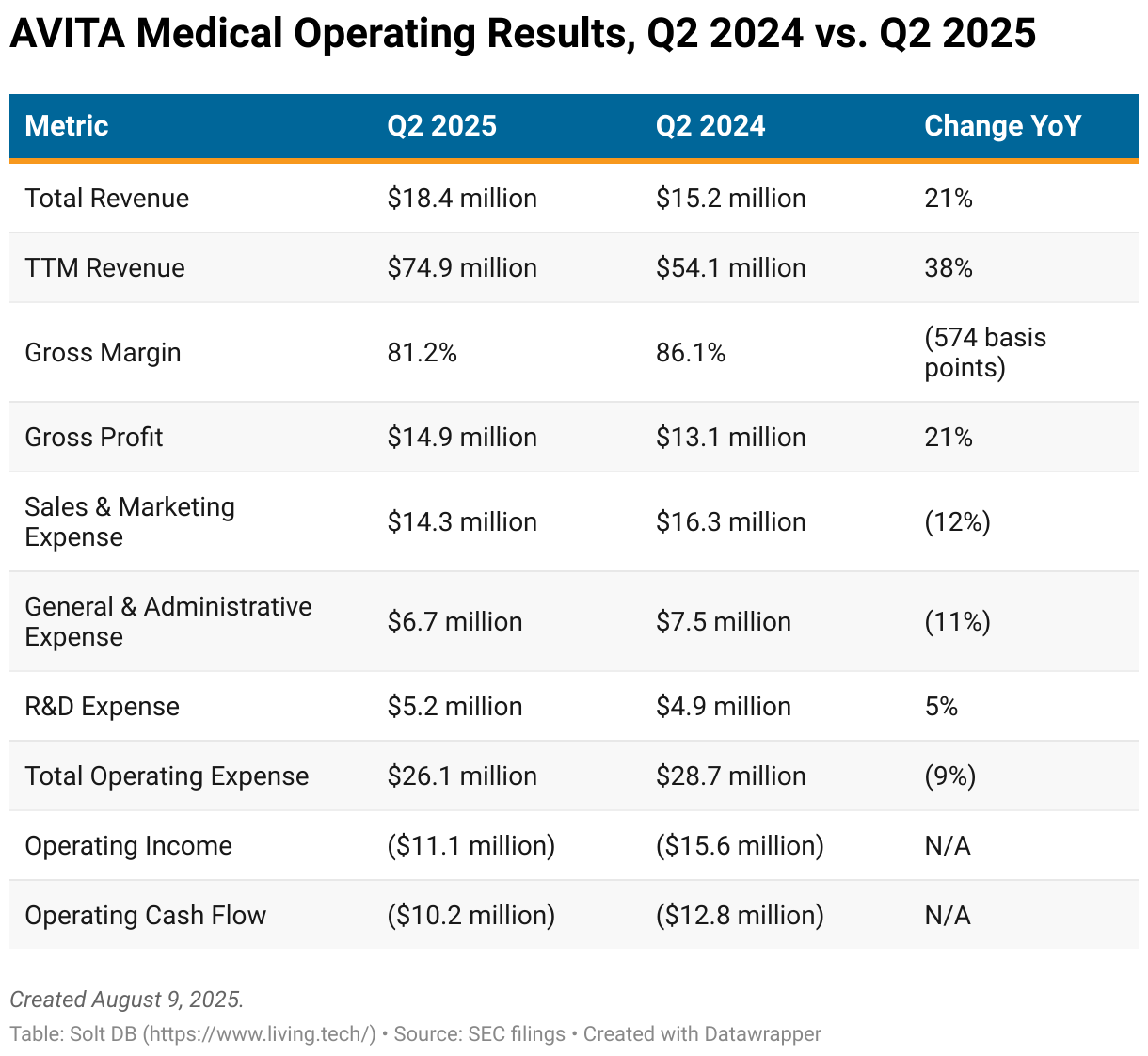

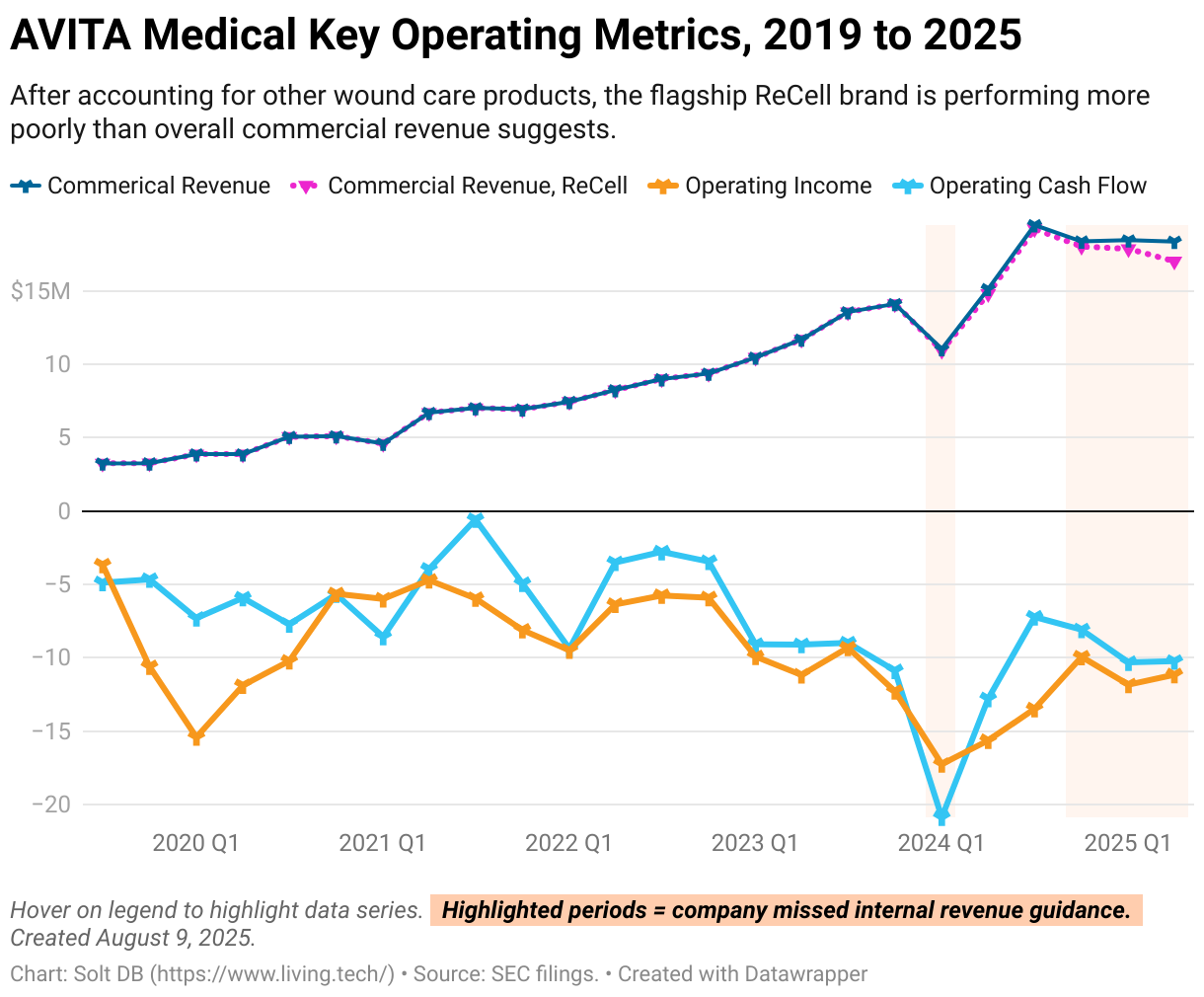

AVITA Medical has been able to report year-over-year revenue growth in recent periods, but quarter-over-quarter revenue has been flatlining for three consecutive quarters now. Four quarters make a year, which means the business is likely to report a year-over-year decline in revenue when it reports Q3 2025 results in November.

Consider that in last year's third quarter, the company reported $19.2 million in commercial revenue. It's been stuck at $18.4 million in each of the last three quarters though.

The performance is even worse if we only look at the flagship ReCell brand's commercial revenue, which is declining despite the launch of ReCell GO. This decline started in Q4 2024 – well before the any policy changes from the new administration could've left a mark. There seems to be something else going on with ReCell GO that management isn't acknowledging.

The business is also well behind expectations for PermeaDerm revenue. When AVITA Medical and Stedical Scientific amended the distribution agreement in March 2025, the wound care specialist increased its revenue share from 50% to 60%. But it was required to achieve full-year 2025 PermeaDerm sales of $6 million. Halfway through the year, revenue is less than 30% of that total.

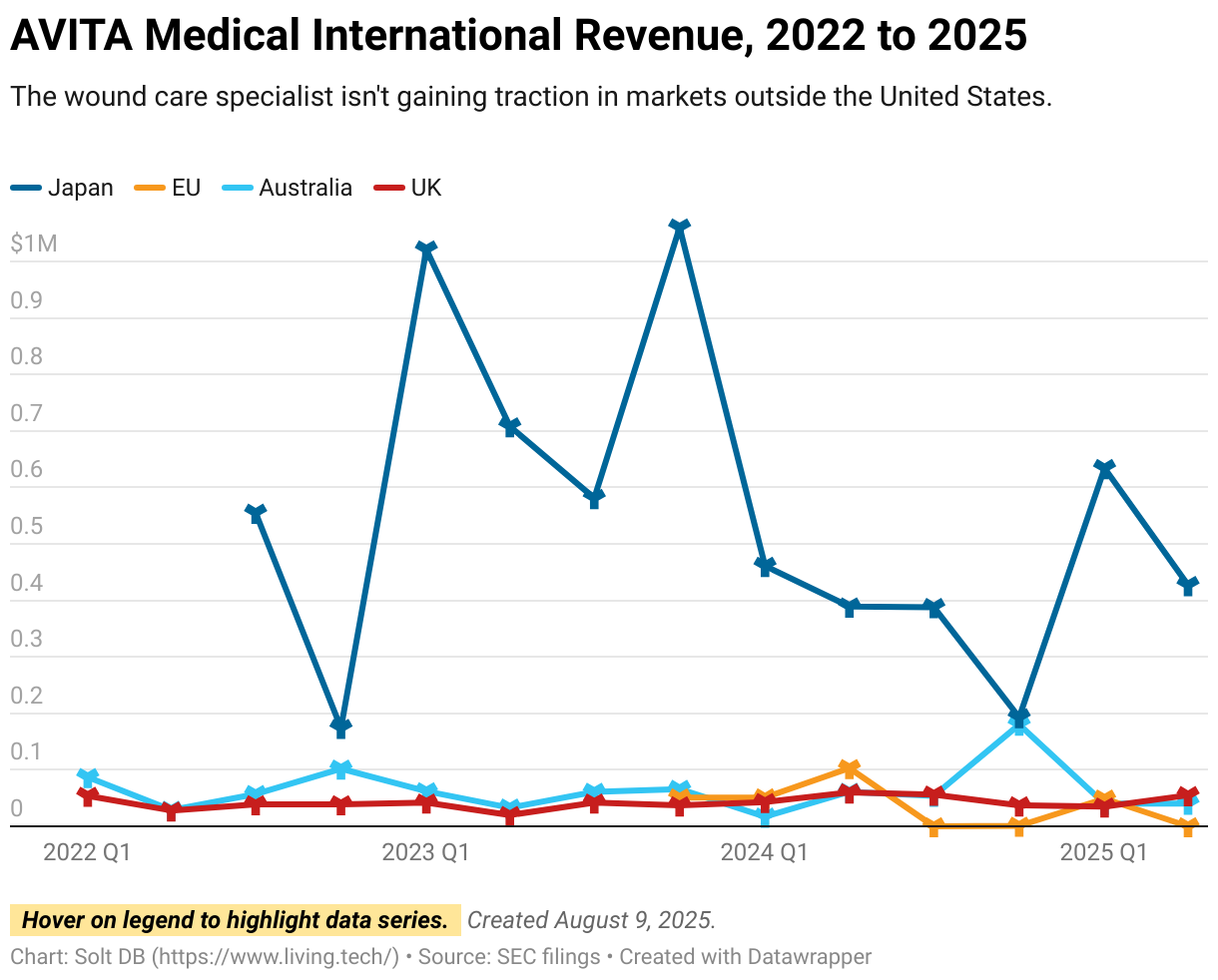

Despite management's prior enthusiasm for international expansion to create new growth shoots for the business, AVITA Medical has not gained traction outside the United States.

There's been no commercial ramp in the core international market of Japan since ReCell launched in Q3 2023. Allying with distributors in the European Union hasn't achieved any discernible real-world results, generating less revenue than non-core markets such as Australia and the United Kingdom.

You know what would've really helped offset policy uncertainty in the United States right now? Having executed in international markets in recent years.

OrbiMed is Likely to Gain Control of AVITA Medical (bad)

As a result of poor business performance, AVITA Medical has been forced to amend the October 2023 credit agreement with OrbiMed multiple times. The business raised $40 million in debt at closing and had access to an additional $50 million in future financing.

At the time, management patted itself on the back for avoiding dilution. All it had to do was maintain a minimum cash balance and achieve certain trailing 12-month (TTM) revenue totals. If it failed to meet either covenant, then the lender could force repayment of the loan.

OrbiMed has waived these covenants by amending the agreement five times. It didn't ask for anything in return the first two occurrences. When the lender amended it a third time by agreeing to cancel the TTM revenue convent for Q4 2024, it revoked the remaining $50 million in credit that could've been extended to the wound care specialist.

For the fourth amendment in February 2025, OrbiMed accepted 145,180 shares of common stock. The fifth amendment on August 7, 2025, up the demand for payment to 400,000 shares of common stock. For a small company with only 26.619 million shares outstanding a few days prior to that date, these transactions amount to 2% ownership in six months for free – and to the lender that would already end up owning the business in bankruptcy.

OrbiMed is one of the most active biotech investors in the current environment. A few days ago, it raised $1.86 billion to plow into growth companies in the healthcare space. It very well could end up taking control of AVITA Medical, get it back on track as a private business, and then offload it to another buyer years later.

This would not be a good outcome for investors in the current publicly-traded company, as OrbiMed would only gain control in bankruptcy or by acquiring the business for a fraction of its public valuation. Shares of AVITA Medical are likely to continue falling well below current levels, leading to exits at steep losses for shareholders who hang on.

If the business turns things around, then investors will be able to objectively identify progress and can decide to start new positions at that time. In the meantime, there's likely to be significantly more pain ahead.

News Flow & Modeling Insights

(Priced for bankruptcy.)

The business is now valued at $0 per share on a fully-diluted basis. The suggested allocation is now 0%.

The current model for 2025 operations now expects:

- Full-year 2025 revenue of $77.932 million, down from a prior model of $78.514 million, although even this may not be possible. This represents year-over-year growth of 22% – respectable, but the lowest since ReCell was commercialized. Company guidance expects $78.5 million at the midpoint.

- Full-year 2025 operating loss of $44.395 million, down from a prior model of $44.227 million.

- Full-year 2025 operating cash outflow of over $41 million, which is sharply higher than the available cash balance at the start of the year.

The current model uses an outstanding share count of 41.235 million:

- 26.619 million shares outstanding on August 4, 2025

- 0.400 million shares issued to OrbiMed on August 7, 2025

- 9.01 million shares of additional dilution for raising capital

- 5.3 million shares issuable as stock options

Margin of Safety & Conviction

AVITA Medical is considered a Future Compounder position with the following Conviction rating.

- 1 = High

- 2 = Above Average

- 3 = Average

- 4 = Below Average

The estimated fair valuation based on my current model is below:

- Market close August 8: $4.25 per share

- Modeled Fair Valuation: $0 per share

- Allocation Range: Up to 0%

The modeled fair valuation above assumes 41.235 million shares outstanding.

Further Reading

- August 2025 press release announcing Q2 2025 operating results

- August 2025 regulatory filing (10-Q) detailing Q2 2025 operating results

- July 2025 research note previewing Q2 2025 earnings across the coverage ecosystem

- May 2025 research note analyzing Q1 2025 operating results

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)