.svg)

Investors and Wall Street analysts might be a little bummed about the delayed launch for the ReCell System in stable vitiligo. Despite earning U.S. Food and Drug Administration (FDA) approval for the indication in June 2023, AVITA Medical doesn't expect to launch until the end of 2025 or early 2026.

Solt DB Invest has expected a vitiligo launch in 2025 since our 2022 model, so this isn't much of a surprise. The latest shuffling of the timeline makes me lean toward an early 2026 launch. That will need to be reflected in our 2025 model, which will be released in August or November 2024.

It's not much of a bummer when the full context is considered, both within the stable vitiligo indication and broader commercial strategy.

The updated timeline allows AVITA Medical to position ReCell for long-term strategic opportunities in the stable vitiligo market. That will be aided by quantifying quality of life metrics in the TONE study, quantifying long-term cost savings for vitiligo patients seeking more permanent repigmentation, and right-sizing investments required to build an entirely new commercial team.

Meanwhile, the ability to leverage significant growth opportunities in full-thickness skin defects ("skin wounds") will drive 50% revenue growth in 2024 and 2025. Following significant investments to expand the commercial footprint last year, management now expects to achieve cash flow breakeven and profitability next year – without any boost from stable vitiligo procedures.

The Vitiligo Delay, Explained

AVITA Medical has embarked on a three-step process to secure reimbursement for the stable vitiligo indication.

- The post-approval TONE study, which will quantify quality of life improvements for patients and physician satisfaction with treatment. A 12-month follow up means the study can be submitted for publication by the end of 2024.

- A health economics study to understand the long-term healthcare costs of a vitiligo patient, including how treatment with ReCell can help reduce healthcare costs. The results of this study are also expected to be submitted for publication by the end of 2024.

- Initiating conversations with commercial payors in the second quarter of 2025, which will benefit from the publication of the two studies above.

If all goes well, then the company expects initial insurance coverage to be in place during the fourth quarter of 2025. That would give AVITA Medical the option to launch in select regions or markets at the end of 2025. I would be more cautious and expect launch in early 2026.

That might seem like a bummer. The premarket approval (PMA) supplement for stable vitiligo was approved in June 2023. But there's virtually no competition to ReCell. That affords the opportunity to consider long-term strategic positioning in the roughly $5 billion market rather than launch just because approval is in hand.

Quality of life and economic impact

Vitiligo is characterized by patches of skin that lack pigment. Stable vitiligo means an individual's lesions haven't changed in size for a meaningful amount of time. Although there's no negative health impact, there's a significant negative impact on the quality of life.

A young woman might not feel comfortable in certain outfits, or an individual with lesions on their face or neck might feel less confident in social situations. That can lead to fewer strokes in life across social or career opportunities. Therefore, any vitiligo treatment will need to not just repigment skin lesions, but make patients feel more confident.

AVITA Medical decided to conduct the post-approval TONE study to understand physician and patient satisfaction after treatment with ReCell. These subjective measures are important for securing reimbursement.

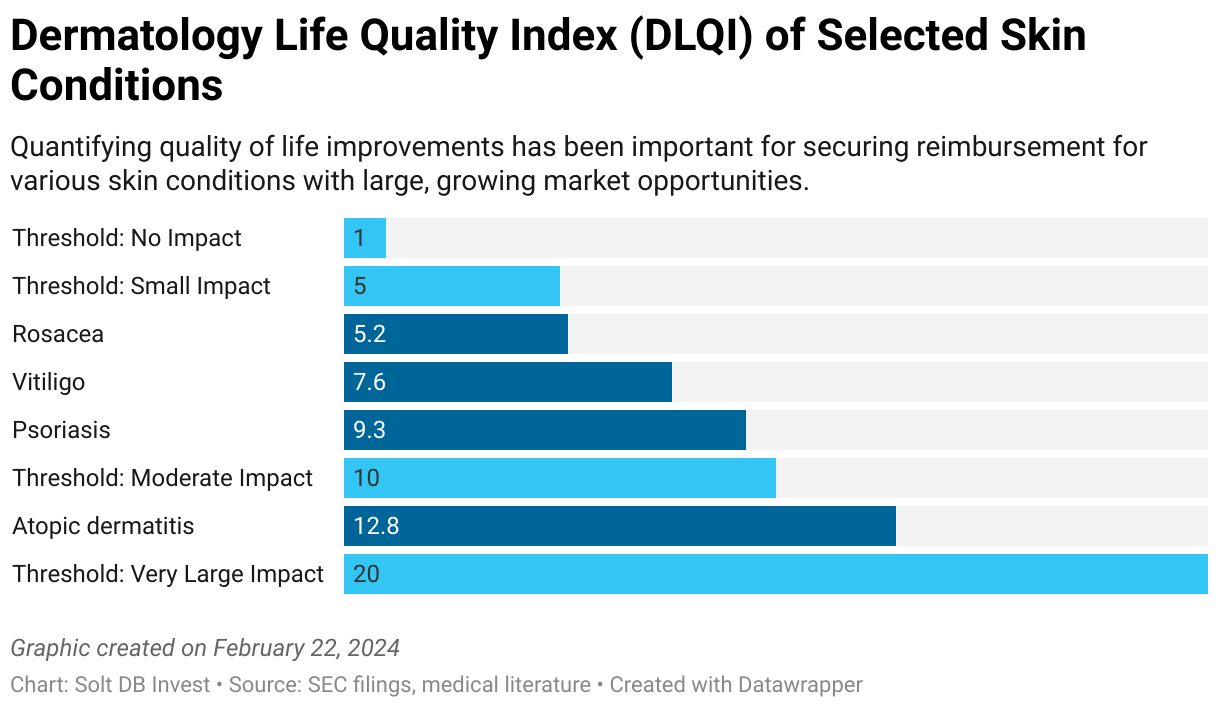

The Dermatology Life Quality Index (DLQI) is a simple questionnaire used to measure how individuals feel about a skin condition.

- Scores of 0 to 1 mean there's no impact on a patient's life

- Scores of 2 to 5 mean there's a small impact on a patient's life

- Scores of 6 to 10 mean there's a moderate impact on a patient's life

- Scores of 11 to 20 mean there's a very large impact on a patient's life

Vitiligo scores roughly 7.6 on the DLQI, while individuals with vitiligo on visible body parts such as the face and neck can score well above 10. Compare that to skin conditions with favorable reimbursement rates, considerable patient awareness, and many effective treatment options.

The only FDA-approved pharmaceutical intervention for vitiligo, Incyte's Opzelura, resulted in an average DLQI improvement of 7.2 points in a phase 3 clinical trial. Patients enrolled in the study had more severe DLQI scores at baseline than will be expected from patients enrolled in the TONE study.

Opzelura helps individuals with vitiligo achieve stable vitiligo, so it'll provide a nice tailwind for ReCell by expanding the number of vitiligo patients with stable vitiligo. They're complimentary, not competitive.

Whereas the TONE study measures quality of life improvements using the DLQI, the health economics study from AVITA Medical will quantify long-term reduction in healthcare costs for vitiligo patients. Opzelura is a topical cream that must be applied continuously to achieve stable vitiligo and quality of life improvements. ReCell is a more permanent one-time treatment, which can have lasting impact and result in significant savings for patients.

Insurance coverage

A favorable outcome for the TONE study and the health economics study could position ReCell as the go-to treatment for (stable) vitiligo.

Although immunosuppressants such as Opzelura help patients achieve stabilization, patients will likely seek repigmentation treatments as the last step of the treatment continuum. ReCell's pivotal clinical trial demonstrated marked improvement over other non-pharmaceutical interventions aimed at repigmentation, such as skin grafting, standalone laser ablation, and Melanocyte-Keratinocyte Transplantation Procedure (MKTP).

ReCell's potential positioning as the foundation of "combination" treatments is likely to remain in place for next-generation antibody treatments, too. The growth opportunity could span more than a decade once launched.

Commercial infrastructure

I've been careful to constantly remind investors that earning FDA approval for a drug or medical device is the end of development activities, but the beginning of commercial activities. A company still has to sell the damn thing.

AVITA Medical can quickly ramp sales in skin wounds because the market opportunity overlaps with burns. The same insurance coverage applies. The same trauma centers and surgeons who treat severe burns also treat severe skin wounds. Ditto for emergency departments treating smaller burns and wounds. That means the same sales team can visit the same physical locations, build relationships with the same surgeons and doctors, and sell ReCell for both indications. There's tremendous leverage.

The same cannot be said for stable vitiligo. Surgical dermatologists would be the point-of-care for ReCell procedures in this indication, which represent a completely different market. There's exactly no overlap to burns, skin wounds, trauma centers, or hospitals.

In other words, AVITA Medical needs to establish new insurance coverage, build new sales teams, and establish relationships with new physical locations and doctors. Although the company will rollout in specific regions and target larger facilities initially to launch as efficiently as possible, it's going to be very expensive.

Therefore, it makes sense to ensure ReCell has favorable quality of life data, health economics data, and insurance coverage before making investments in new commercial infrastructure.

By the Numbers

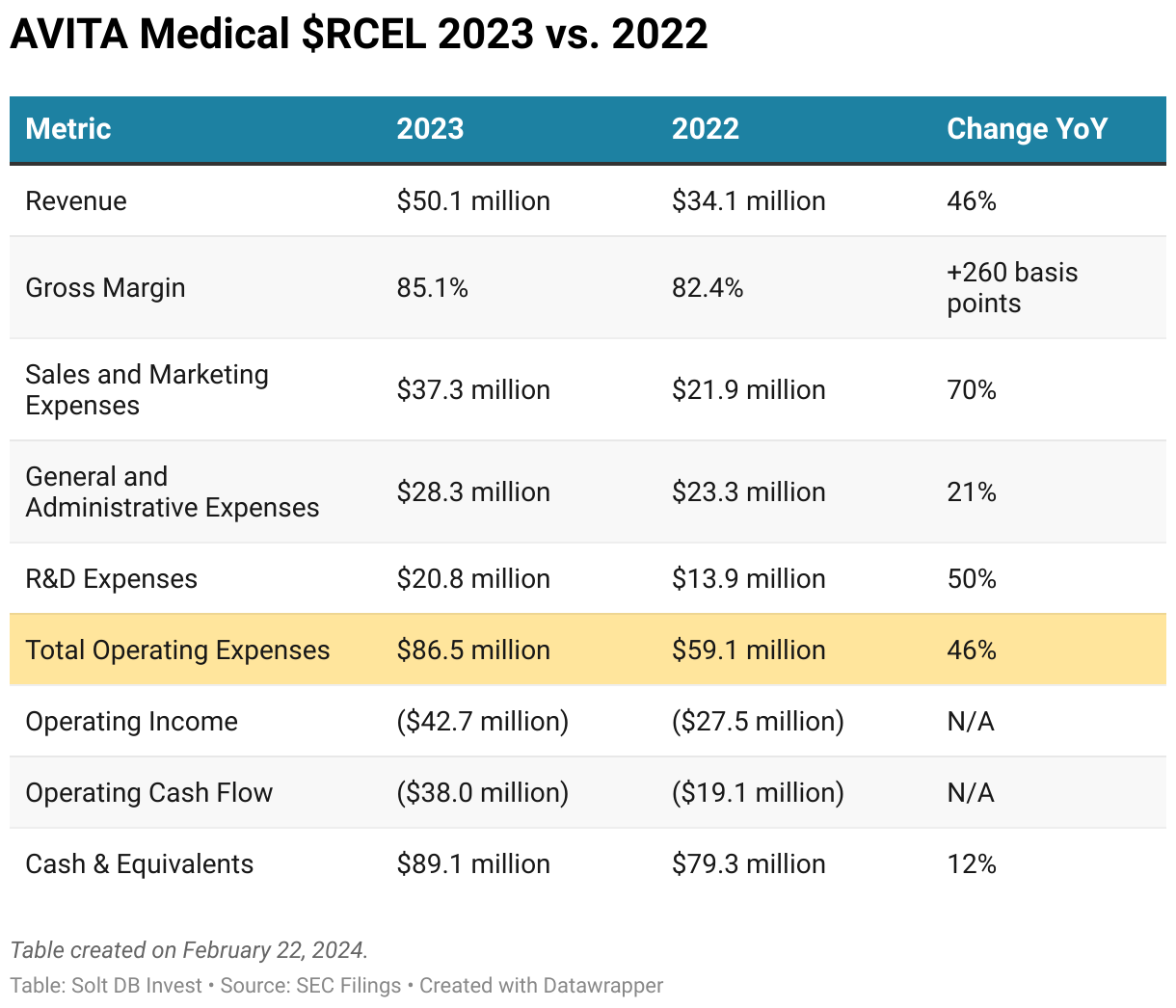

AVITA Medical delivered its most efficient year of operations yet. The business grew commercial revenue 46% year over year and notched a record gross margin of 85.1%. That came at the expense of much higher operating expenses, primarily the result of a greatly expanded commercial footprint. Full-year 2023 operating expenses soared to $86 million, compared to an average of $58 million in the previous three years.

Management believes it can drive significant growth from a larger commercial organization, and expects revenue growth to outpace operating expense growth beginning in 2024. That's how the business can begin reducing its operating losses and march toward profitability in 2025.

The primary reason for larger operating expenses was that AVITA Medical expanded its sales team from 30 reps to 70 reps in 2023. It's not done. In fact, it plans to pull forward a planned expansion from the second half of 2024 to the first quarter, which will result in a team of 104 reps.

The rationale is that initial efforts to expand in skin wounds since summer 2023 have gone better than expected – even if it doesn't appear that way from quarterly revenue yet. That's because there's a lag.

ReCell has the same reimbursement code in skin wounds as in burns, and is often being used in the same burn and trauma centers by the same surgeons. However, establishing ReCell as a treatment option for skin wounds requires vetting by a hospital's Value Analysis Committee (VAC). That takes time, but the first wave of impact will be seen in 2024.

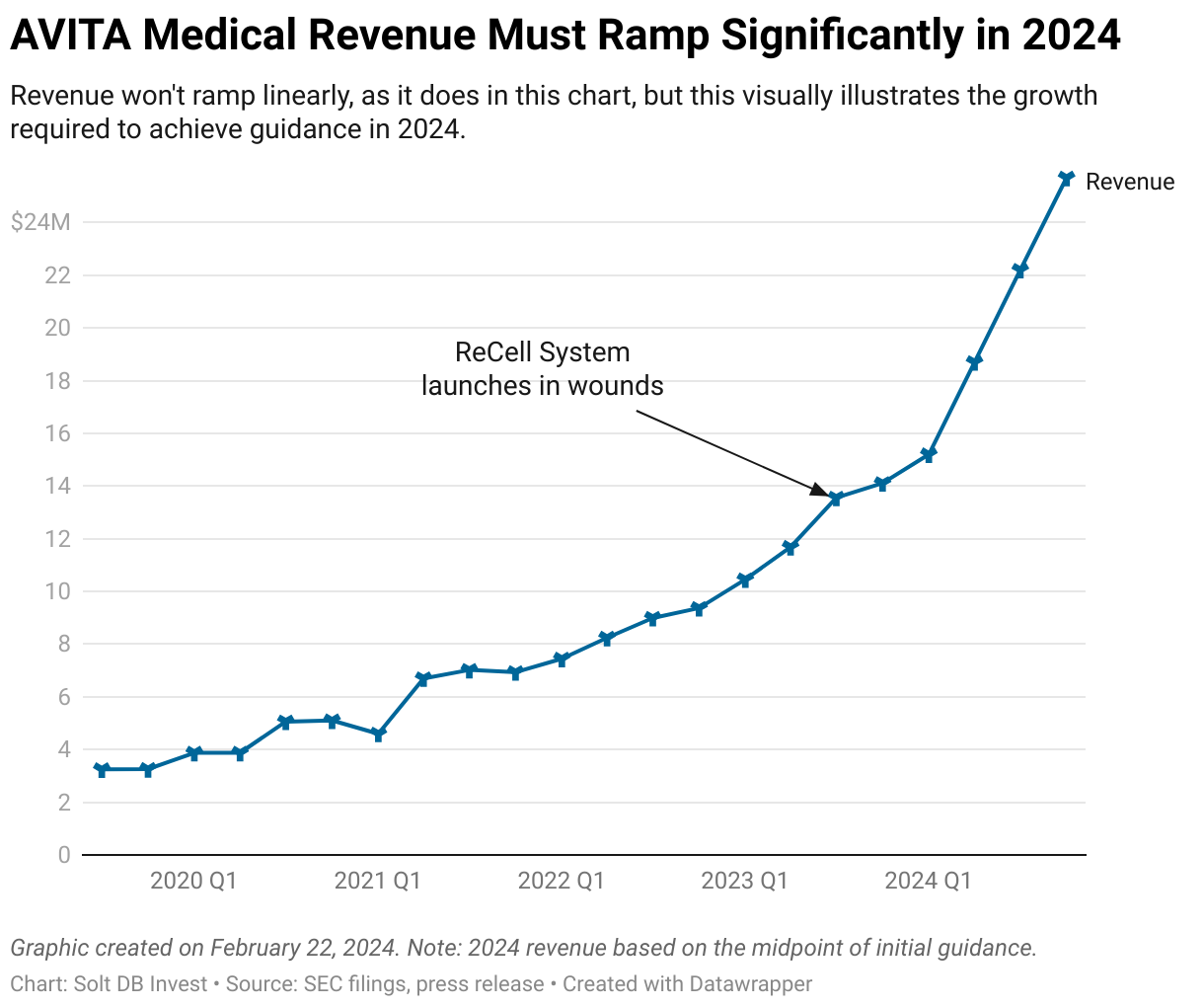

Management expects to add nearly 200 accounts in 2024, which would roughly double the account total from the end of 2023 and result in nearly 50% market penetration (measured by total accounts anyway). Revenue growth from these initial efforts will drive an inflection point in the second half of 2024.

The next wave will splash ashore next year, which could allow the business to grow revenue at least 50% in 2025. That would result in full-year 2025 revenue of at least $115 million – almost 10x from 2020.

Focusing on account growth will drive revenue growth, but will also have strategic importance by leveraging the operating efficiencies of ReCell Go, expected to launch in June 2024.

Looking Ahead

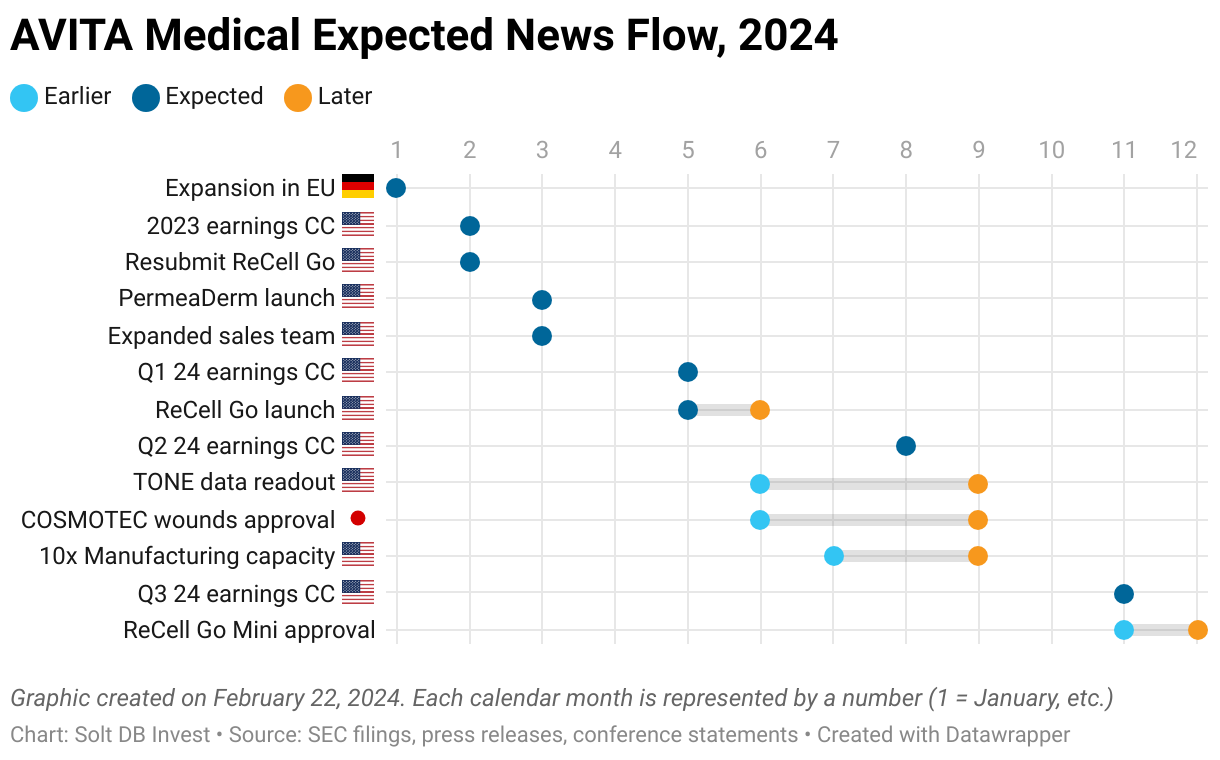

AVITA Medical announced several updates and multiple new initiatives that will help to support significant revenue growth and the march to profitability.

- (January 2024) The company's European distribution partner has commenced sales in Germany, Austria, and Switzerland. Additional distribution partners in Europe are being evaluated.

- (March 2024) The PermeaDerm matrix product, which can be used in combination with ReCell in burns and wounds, is expected to launch in March. It will have gross margins of 50%, a far cry from ReCell's nearly 85% gross margin, but it has nearly perfect overlap for burns and skin wounds procedures. It represents a low-hanging opportunity to accelerate profitable growth from the effort of each sales rep.

- (Q1 2024) The commercial sales team will expand from 70 to 108 reps to better leverage the growth opportunity in skin wound procedures.

- (May 2024) The third-generation automated device, ReCell Go, is expected to earn FDA approval in the first half and launch on May 31, 2024. This will transition all sales of the ReCell System across all indications to the new platform. Whereas the existing device is sold as a one-time kit, ReCell Go will be sold as a semi-permanent instrument with cartridges used for each procedure. It will increase uptake, utilization, and patent protections.

- (Q3 2024) An expansion of the company's Ventura, CA manufacturing and warehouse facility will be completed in the third quarter of 2024. It will increase capacity by 10x and support expected operations in 2029.

- (2024) A PMA supplement for a new ReCell Go cartridge, called ReCell Go Mini, is expected to earn FDA approval by the end of 2024. The new consumable will be more efficient for treating smaller wounds, specifically those covering less than 5% of a patient's total body surface area. This will address surgeon hesitancy to use larger cartridges for smaller wounds, increasing utilization and market penetration.

That's a lot of updates! Here's how the expected news flow looks now.

Forecast & Modeling Insights

(No change.)

AVITA Medical expects:

- Full-year 2024 commercial revenue of $78.5 million to $84.5 million, representing a midpoint of $81.5 million.

- Cashflow breakeven and GAAP profitability will be achieved by the third quarter of 2025 at the latest.

Solt DB Invest's current model for AVITA Medical values the business based on expected 2024 performance, which expects:

- Full-year 2024 commercial revenue of $77.59 million from ReCell units

- GAAP gross margin of 84.5% from ReCell units

Our model excludes contributions from the PermeaDerm matrix product, revenue from the European distribution agreement, and efficiencies from the ReCell Go device.

Margin of Safety & Allocation

AVITA Medical is considered a Growth (Quality) position. The current modeled fair valuation for the company based on our 2024 model is below:

- Market close February 22: $17.01 per share

- Modeled Fair Valuation: $16.80 per share

- Allocation Range: Up to 15%

AVITA Medical reported 25.706 million shares outstanding as of February 7, 2024. The modeled fair valuation above assumes 29.563 million shares outstanding, which is equivalent to 15% dilution. This accounts for expected dilution from the OrbiMed debt agreement, which will not be realized until 2028.

Further Reading

- February 2024 press release announcing full-year 2023 operating results

- February 2024 regulatory filing (10-K) detailing full-year 2023 operating results

- January 2024 research note analyzing preliminary full-year 2023 operating results and full-year 2024 revenue guidance

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)