.svg)

It was a quiet quarter for AVITA Medical. Then again, it's all relative.

The business outperformed Solt DB Invest expectations for second-quarter 2023 revenue and raised full-year 2023 revenue guidance. The new guidance is roughly in line with our modeled expectations, although the finch now expects AVITA Medical to outpace our 2023 model.

On the one hand, Solt DB Invest is now pegging the company's fair valuation to our 2024 model. We expect significantly higher revenue than the average Wall Street estimate ($69.05 million) or even the highest Wall Street estimate ($79.4 million). On the other hand, we value the business differently, as our expectations model more modest valuation premiums in the near future.

Our 2024 model excludes upside for international expansion and stable vitiligo partner opportunities, which are expected to be shared by the company beginning in November 2023.

By the Numbers

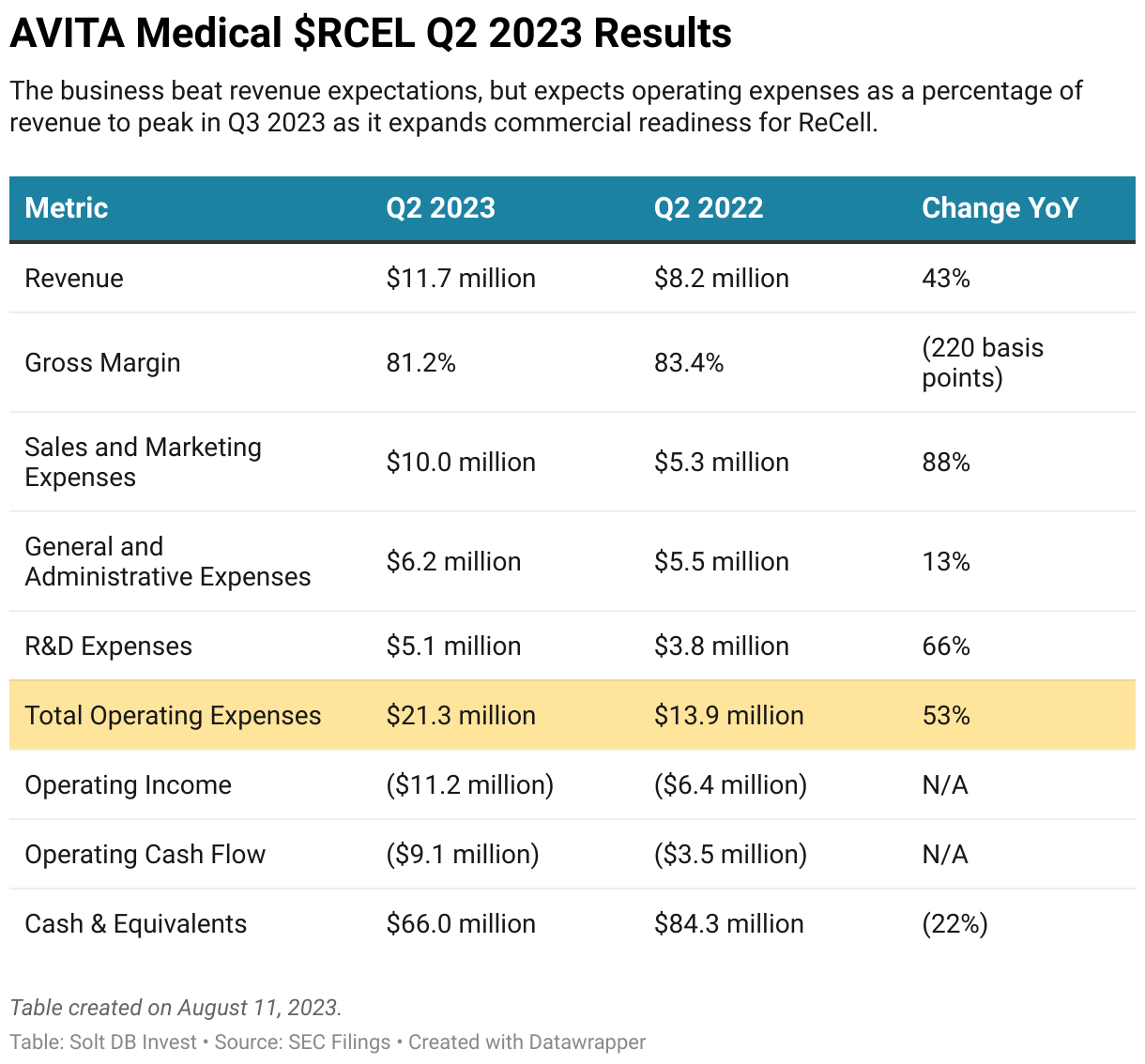

AVITA Medical launched the ReCell System in full-thickness skin defects, approved for an advantageously broad label, on June 8. It made almost no meaningful contribution to second-quarter 2023 revenue. That's a good thing.

Solt DB Invest expected second-quarter 2023 revenue of $11.2 million, which matched the company's expectations. It leapt ahead of expectations with $11.7 million instead. Although that's not an earth-shattering outperformance, the strength of the core business through the first half of 2023 bodes well for meeting or exceeding guidance.

The company lifted full-year 2023 revenue guidance from a midpoint of $50 million to a midpoint of $52 million. Solt DB Invest expects the company to have meaningful potential to blow past its latest guidance, although the finch is now focusing its fair valuation for the business on our 2024 model. Our full-year 2024 model expects at least $82.8 million in revenue, compared to the average Wall Street estimate of $69.05 million or highest Wall Street estimate of $79.4 million.

Our 2024 model expects year-over-year growth of at least 60%, an increase from the roughly 52% year-over-year revenue growth expected in 2023. The increase can be chalked up to improved penetration of trauma center accounts, increased adoption of the ReCell System broadly, and the add-on effects of the ReCell Go device expected to be approved in early 2024.

AVITA Medical noted its second-quarter 2023 gross margin of 81.2% is expected to be a temporary low point, as third-quarter 2023 gross margin is expected to higher than the 83.2% achieved in the year-ago period. Additionally, the business expects operating expenses as a percentage of revenue to peak in the third quarter of 2023 and then gradually recede as revenue growth outpaces operating expenses growth.

Forecast & Modeling Insights

(Changed to reflect 2024 model.)

Solt DB Invest is replacing its 2023 model with its 2024 model. As a result, the modeled fair valuation has increased from $11.40 per share to $18.37 per share on a fully-diluted basis. A fully-diluted basis means we expect the company to issue common stock resulting in 15% dilution from current levels.

On a non-diluted basis (the level shares can reach prior to a dilution event), our 2024 model results in a fair valuation of $21.12 per share.

The finch expects to introduce a preliminary 2025 model after the November 2023 conference call. AVITA Medical noted it won't introduce full-year 2024 revenue guidance until the February 2024 conference call, but that's where Solt DB Invest comes in.

Margin of Safety & Allocation

(Changed to reflect 2024 model.)

AVITA Medical is considered a Growth (Quality) position. The current modeled fair valuation for the company based on our 2024 model is below:

- Market close August 11: $18.45 per share

- Fair Valuation: $18.37 per share

- Allocation Range: Up to 15%

AVITA Medical reported 25.478 million shares outstanding as of August 2, 2023. The Margin of Safety range above assumes 29.300 million shares outstanding, which prices in 15% dilution.

Further Reading

- August 2023 press release announcing second-quarter 2023 operating results

- August 2023 quarterly filing (10-Q) detailing second-quarter 2023 operating results

- May 2023 research note analyzing first-quarter 2023 operating results

.svg)

.svg)

-cropped.svg)