.svg)

Not that long ago, a new management team at AVITA Medical reset its relationship with investors by re-establishing trust. That's one of the most difficult things to accomplish in business – and the feat was accomplished virtually overnight.

Management might have overlooked the fragility of Wall Street's newfound admiration.

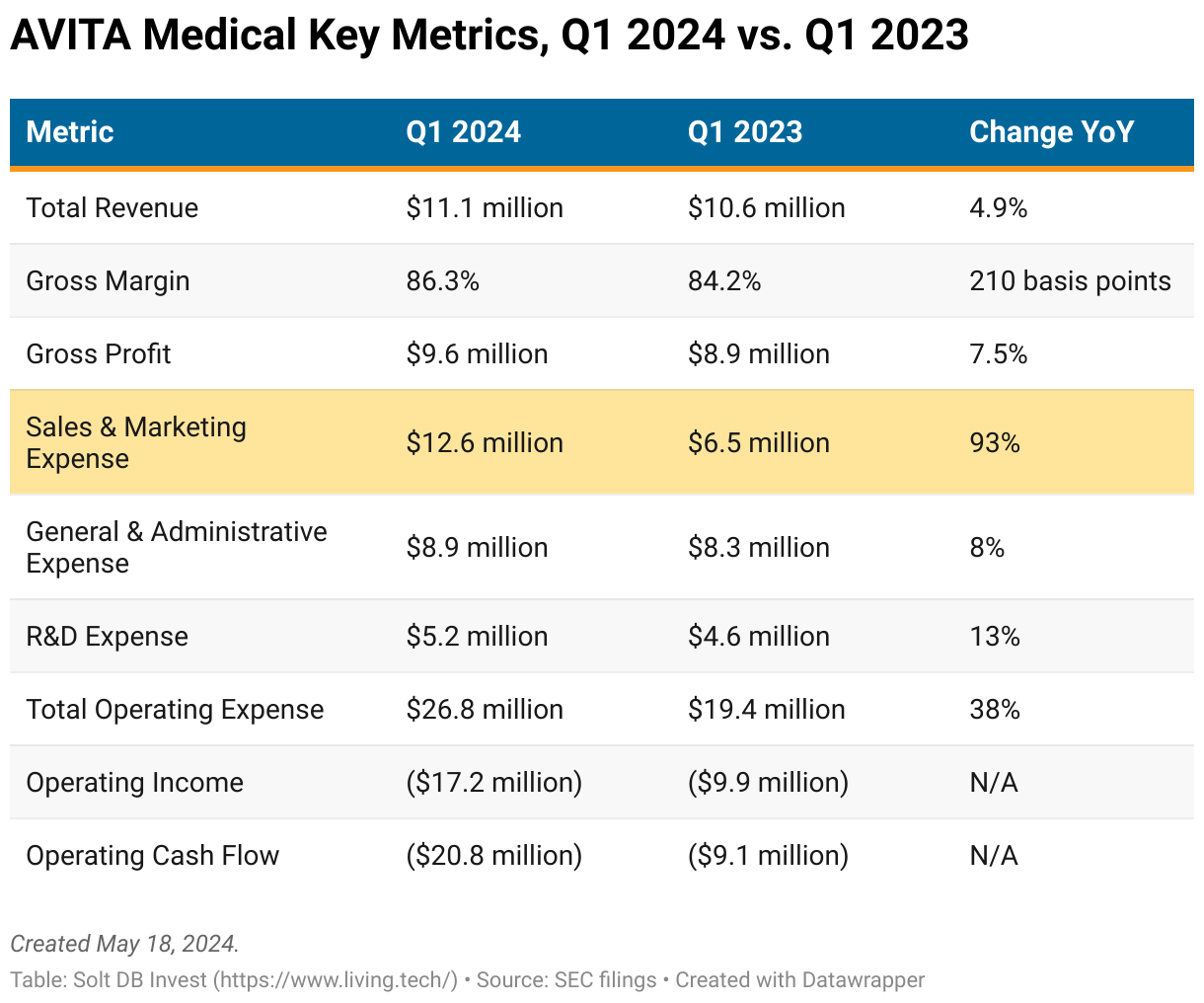

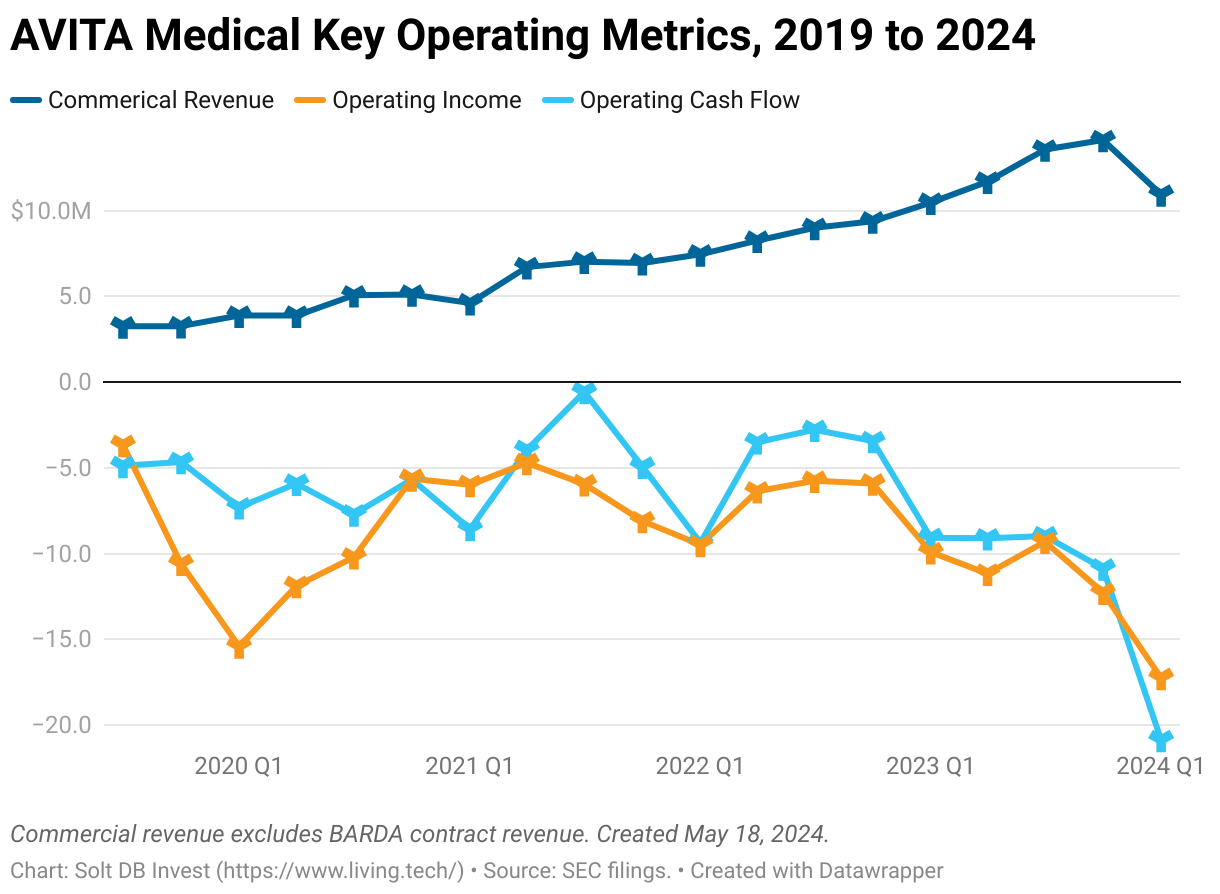

The business had a surprisingly weak first-quarter performance with revenue growth of just 5%. The optics aren't great, especially since two big surges in the sales team drove a 38% increase in operating expenses in the last year. That swelled the company's quarterly operating cash burn to the highest level in over five years, by a factor of two.

Management isn't backing down. Not only has AVITA Medical reiterated its belief in achieving near $78.5 million in full-year 2024 revenue, but it recently completed yet another increase in the sales team and announced new plans to expand the product portfolio into adjacent wound care areas. It's a bit perplexing.

On the one hand, the business does need to scale. Management is right about that. The company needs about 2x to 3x its quarterly revenue total (generously using fourth-quarter 2023 revenue as the base) to get within striking distance of breakeven operations. That's likely to be achieved by the first half of 2026 at the latest.

On the other hand, the timing of investments is easy to criticize, and the narrative doesn't match reality. It increasingly looks like management built the sales team too quickly, saddling the company with operational bloat with little immediate payoff. Not a great strategy with a limited cash runway. The irony is it could've still sold the strategy to prioritize building commercial infrastructure in 2024 and issued lower revenue guidance, but sticking to unrealistic growth targets somehow makes everything a little less believable.

To be clear, AVITA Medical is well positioned for near-term growth in the next few years. The sky is not falling. It's not time to panic. I just think management is making a mistake by trying to squeeze too much progress into calendar 2024.

By the Numbers

AVITA Medical had a rough start to the year. Revenue grew just 5% from the year-ago period, which reflects struggles within its core treatment indication of burns and the second treatment indication of full-thickness skin defects.

The latter, which launched in July 2023 and is still ramping, has been bogged down by slower-than-expected approval processes from Value Analysis Committees (VAC). Management admitted it underestimated the length of these processes and that it lacked internal know-how for navigating them. After all, the company hasn't needed to go through VAC decisions for a few years, and not hundreds at a time, and not for a product approval as complex as full-thickness skin defects.

Longer-than-expected VAC decisions have collided with the significant investments made in the commercial sales team. The company grew the sales team from 30 reps at the beginning of 2023 to roughly 104 at the end of March 2024 – a noteworthy departure from the historically sleepy trend in headcount growth. For reference, the wound care specialist grew total headcount across the entire organization by just 28 individuals from 2019 to 2022.

It's probably too soon to say whether the expanded sales team was a poor investment, but it increasingly looks like an ill-timed one. AVITA Medical reported a 38% increase in operating expenses since the start of last year. And it's not yet realizing a meaningful increase in revenue growth.

The combination of slower-than-expected revenue growth and much higher expenses led to a rapid deterioration in operating income and operating cash flow – the two most important metrics for any growth stock. Temporary fluctuations aren't necessarily worrisome or unexpected, especially if there's a big growth push. But the context is important. Wall Street doubts the company's growth projections for 2024 and the cash balance is relatively light at $68.2 million.

Although the focus has primarily been on the slow start for the new full-thickness skin defects indication, the sudden slowdown in burns also deserves some attention.

AVITA Medical doesn't break out revenue by indication. But second-quarter 2023 revenue of $11.7 million only included burns since the new indication hadn't launched yet. The ReCell System had total first-quarter 2024 revenue of less than $11 million.

Management noted a slowdown in burn injuries nationally, but that doesn't quite align with the data.

First, larger peer Vericel reported $10.7 million in first-quarter 2024 sales from its flagship burn product, Epicel. That marked a year-over-year increase of 56%. Second, AVITA Medical saw total revenue decline in the United States, Japan, and Australia.

Those details suggest the business is suffering from some operational inefficiencies, which isn't too surprising given the swift increase in headcount and suddenly diverse growth priorities across the business. It could also suggest there was a bigger problem in the first quarter, such as a manufacturing challenge or unofficial recall. I'll interrogate financial statements more closely to see if something jumps out, but everything seems normal at first glance. It's difficult to tell given all the moving parts recently.

Looking Ahead

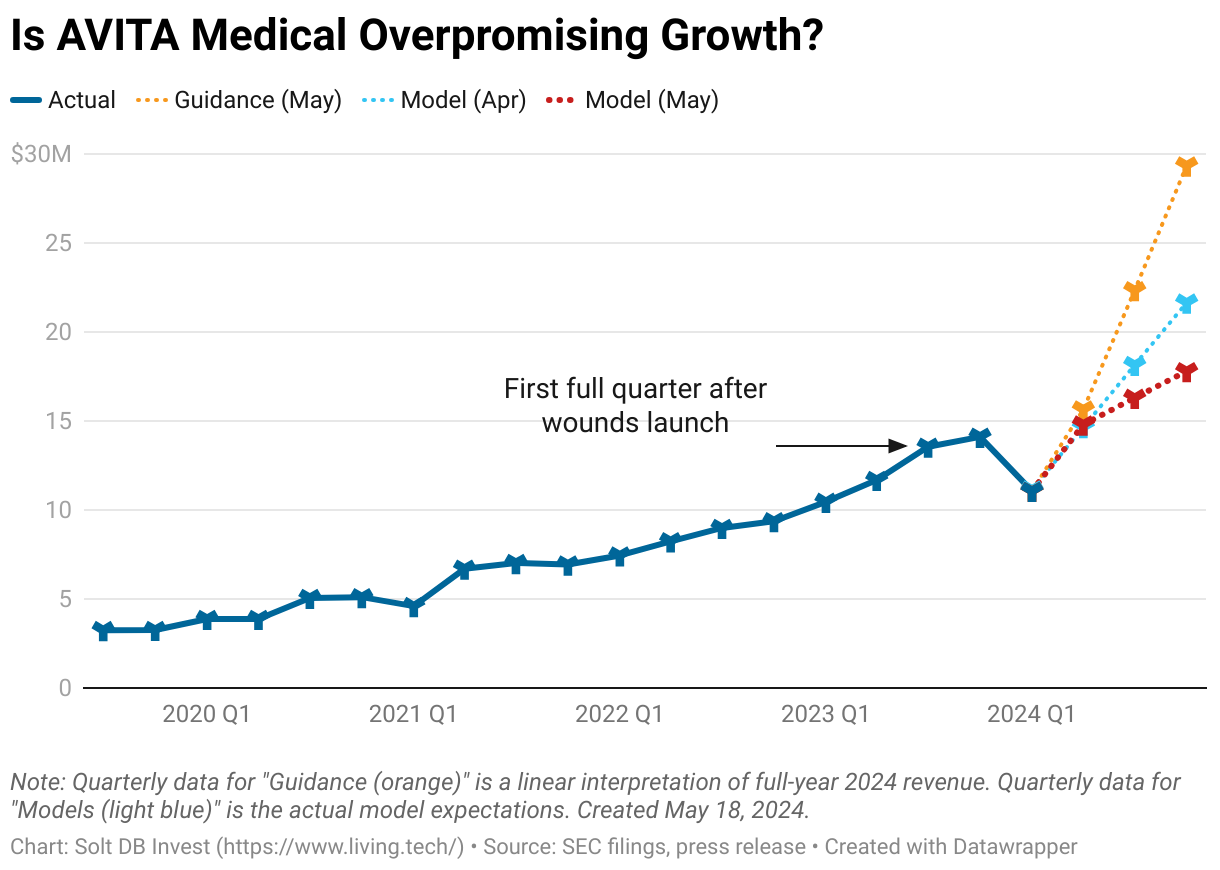

Almost every analyst questioned why management maintained full-year 2024 revenue guidance of $78.5 million. To put it as nicely as possible, it's almost delusional.

The company issued second-quarter 2024 revenue guidance of $14.8 million at the midpoint, which would result in first-half 2024 revenue of about $25 million. That would require second-half 2024 revenue of nearly $53.5 million to meet guidance. That's simply too steep of a ramp to be believable.

Yes, new growth channels will be pried open as the year progresses. AVITA Medical is growing more slowly than expected, but it's still growing.

The company expects the number of accounts added since the launch of full-thickness skin defects to increase from 73 at the end of March to about 119 by the end of June (excluding a rejection here or there). The PermeaDerm matrix product launched on March 23 and contributed $0.1 million in revenue in just one week. And the launch of ReCell Go is expected to be a significant growth driver for the business once it earns regulatory approval at the end of May 2024.

But these things won't magically double the size of the business once the calendar flips to July. If the deadline for achieving that milestone was instead changed to the second half of 2025, then I might say that's realistic. Unfortunately, management is sticking to an unreasonably aggressive timeline.

Forecast & Modeling Insights

(Reduced 2024 model.)

AVITA Medical reiterated full-year 2024 revenue guidance of about $78.5 million, which is the lower end of its initial guidance range. I don't see that being realistic.

My initial 2024 model expected annual revenue of $77.59 million. I revised that to $65.60 million in April 2024, which excluded any contribution from ReCell Go or PermeaDerm matrix products.

I'm revising my 2024 model lower once more, which now expects full-year 2024 revenue of $59.834 million. This also excludes ReCell Go and PermeaDerm matrix products. This represents year-over-year growth of 20%, which is disappointing relative to expectations but still a respectable growth clip.

The new 2024 model also accounts for the financial impact of higher expenses and cash burn, which reduces the valuation premium assigned to the company's operations.

Management provided an interesting detail on the recent conference call. For burns or wounds covering at least 10% of a patient's total body surface area (TBSA), surgeons must use two kits of the current ReCell devices. That means taking a skin biopsy, disaggregating it using the kit, spraying the skin cells onto a patient – and then doing that again with the next kit. The amount of labor required means the surgeon cannot do both kits simultaneously.

ReCell Go changes that. The automated benchtop device has consumable kits for each procedure. Surgeons have expressed interest in placing two devices in operating rooms, which means larger burns and wounds can be treated in half the time of the current devices with significantly less labor input. Given the shortage in nursing staff and willingness to train staff, the added convenience could be a significant growth driver.

I'm still waiting to introduce any efficiency gains from ReCell Go until my 2025 model is released in November 2024.

Margin of Safety & Allocation

AVITA Medical is considered a Growth (Quality) position. The current modeled fair valuation for the company based on my 2024 model is below:

- Market close May 13: $8.35 per share

- Modeled Fair Valuation: $11.66 per share (vs. $13.60 per share prior)

- Modeled Fair Valuation: $346 million (vs. $402 million prior)

- Allocation Range: Up to 15%

AVITA Medical reported 25.800 million shares outstanding as of May 6, 2024. The modeled fair valuation above assumes 29.670 million shares outstanding, which is equivalent to 15% dilution.

Further Reading

- May 2024 press release announcing Q1 2024 operating results

- May 2024 regulatory filing (10-Q) detailing Q1 2024 operating results

- April 2024 research note discussing preliminary expectations for slower growth and my reduced 2024 model

- February 2024 research note analyzing 2023 operating results

- January 2024 research note analyzing the little room for error based on management's then-rosy projections for 2024

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)