.svg)

Some companies can't shut the f*nch up about what they intend to do, but rarely deliver. The bill always comes due. Eventually.

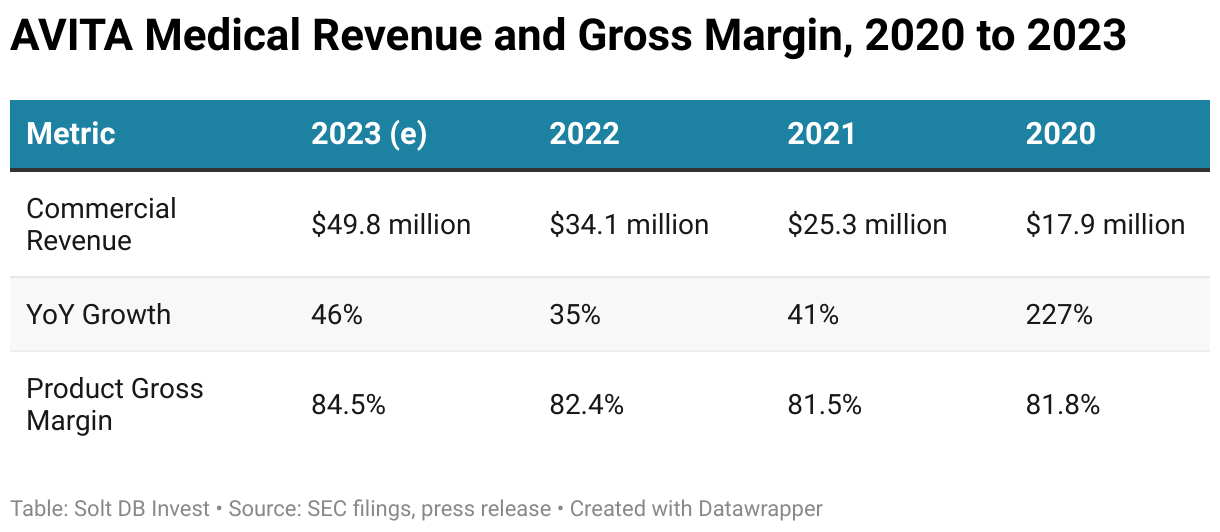

AVITA Medical has backed up recent promises for significant growth with real-world execution, which is the first-, second-, and third-most important thing for driving durable share price gains. Individual investors can thank CEO Jim Corbett for the change of pace. Corbett, the longtime chairman, replaced the longtime CEO after growing frustrated with management's sloth-like pace of communication and progress. He set a high bar in 2023, but the business delivered with year-over-year revenue growth of 46%.

Now he wants to top that by growing revenue 63% to $81.5 million in 2024.

It's not farfetched. There are efficiency gains the business has yet to unlock, while ramping sales of ReCell in wounds will add significant revenue. But the business will need to ramp revenue significantly in the second half of 2024, which leaves little room for error.

Preliminary 2023 Operating Results

AVITA Medical announced preliminary full-year 2023 operating results. It expects to have achieved gross margin of 84.5% and revenue of $49.8 million.

Gross margin was higher than my model. Revenue was a little lighter than I originally expected but in line with revised guidance. For reference, the business delivered annual revenue growth of 35% in 2022 and 41% in 2021 (from a much smaller base). An accelerating growth profile – when the revenue totals are much larger – is rare and encouraging.

I'll dive into last year's results when they're formally published in February.

Initial Guidance for 2024

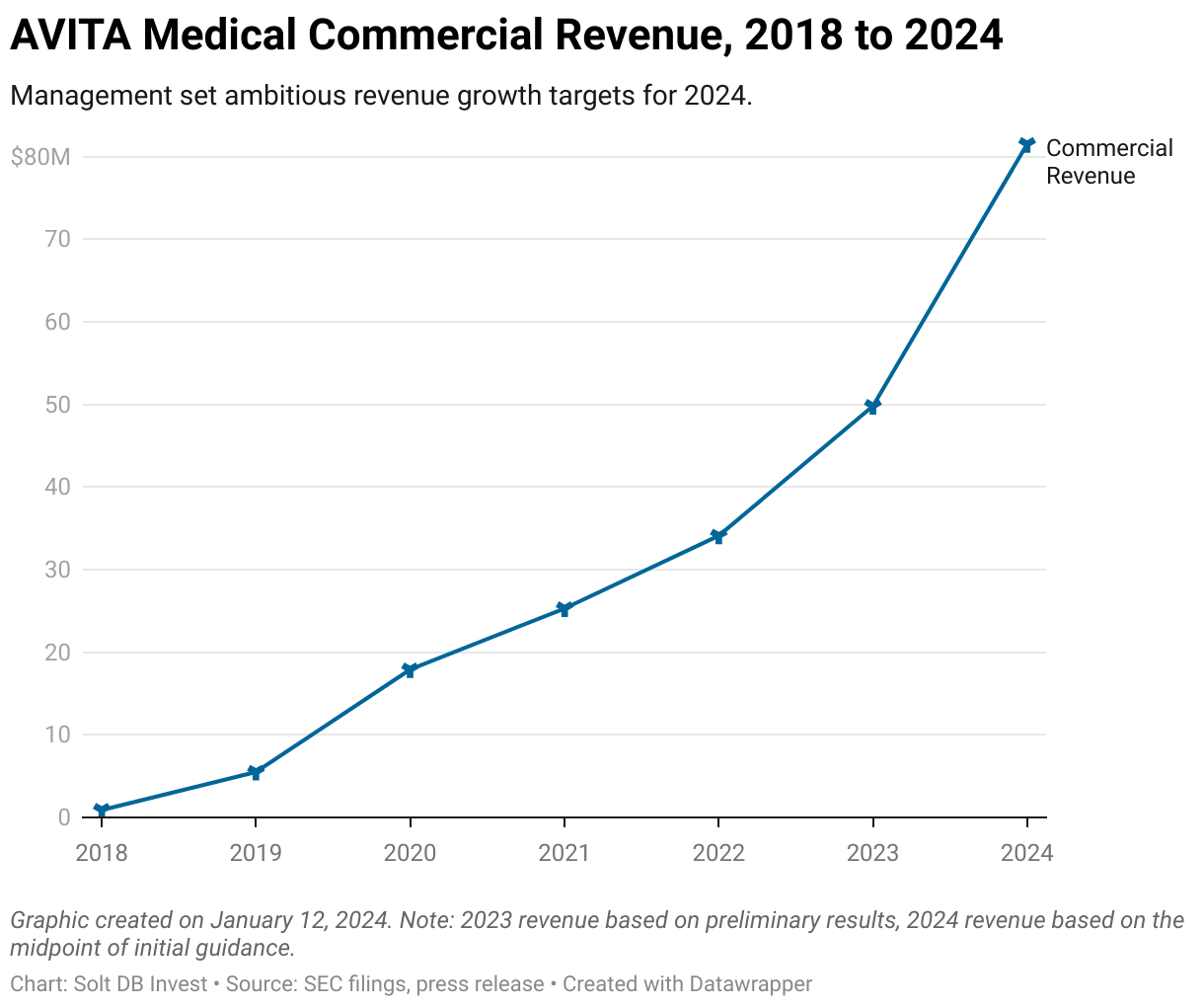

Looking ahead, AVITA Medical expects full-year 2024 revenue of $78.5 million to $84.5 million, representing year-over-year growth of 63% at the midpoint ($81.5 million). Achieving that level would accelerate an already impressive growth ramp from the time ReCell launched commercially in 2018.

That matches our 2024 revenue model, which expects between $77.59 million (our base case without ReCell Go) and $82.81 million. Initial guidance is also well above the Wall Street consensus of just $68.8 million.

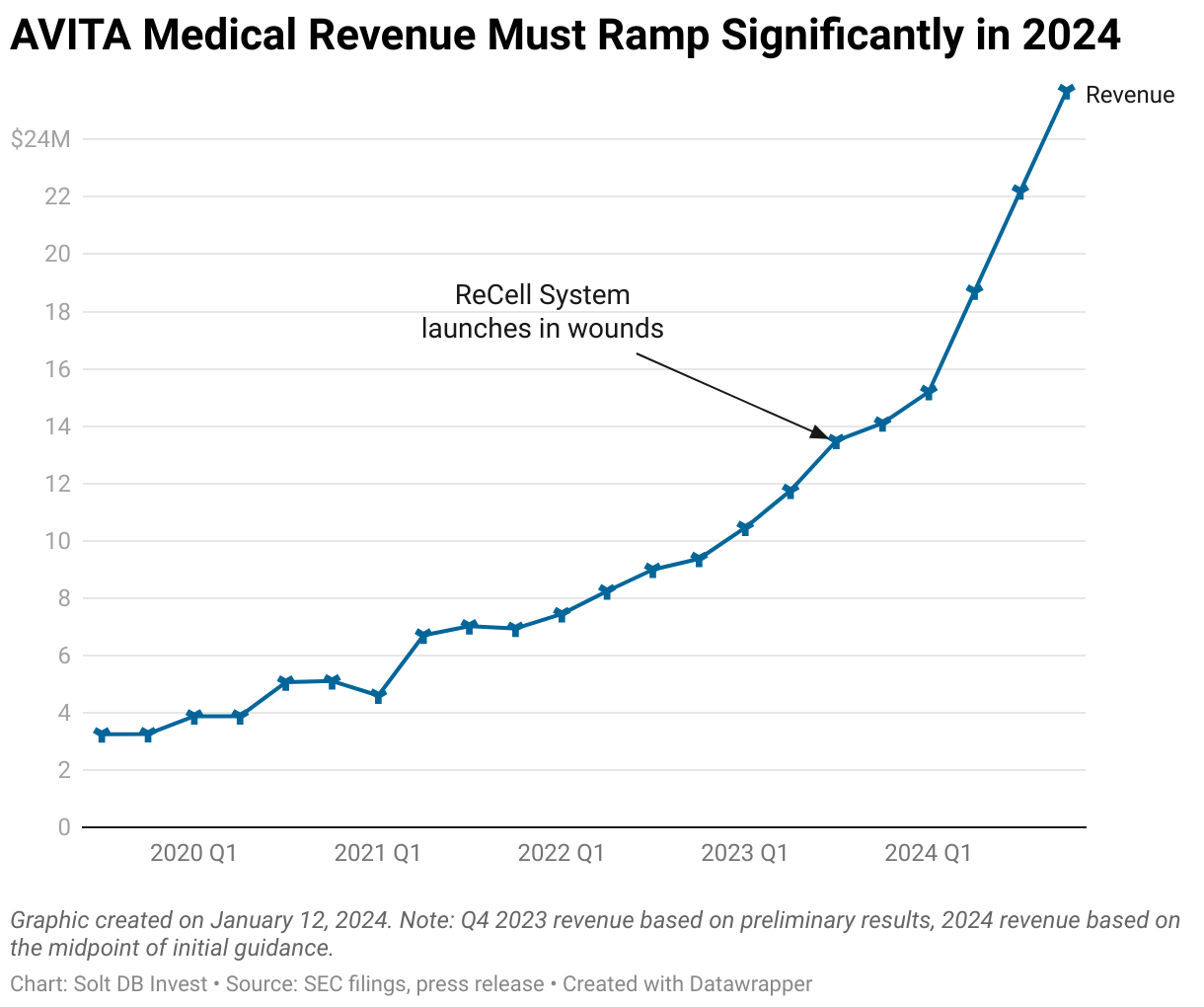

The business will need to execute very well to meet guidance. Consider that first-quarter 2024 revenue is expected to be roughly $15.2 million, which would mark the first time quarterly revenue exceeded $15 million. That means AVITA Medical will need to average $22 million in revenue for the next three quarters to meet the midpoint of guidance.

Here's how that would look within the historical context if the ramp occurs in a linear manner (it won't but this helps visualize the required performance).

A few drivers instill confidence in achieving full-year 2024 revenue guidance. First, AVITA Medical is still ramping sales in the wound indication, which is several times larger than the market opportunity in burns. This will be the first full year with an expanded sales team in place.

Second, international expansion will have a larger impact on commercial revenue. The business' relationship with COSMOTEC in Japan should deepen as the partner ramps sales in burns and expands into wounds. Meanwhile, a new agreement with distributor PolyMedics can generate revenue on the European continent for the first time beginning with Germany, Austria, and Switzerland. Distribution agreements are generally not that lucrative, but Japan and Europe can add up to $5 million in revenue in 2024 (vs. $2.8 million in 2023).

Third, AVITA Medical will become the exclusive distributor of a new matrix product in 2024. A matrix product is a topical gel often used to protect skin during the healing process, which can accelerate healing and reduce scarring. One of the core advantages of the ReCell System is the ability to improve healing outcomes as measured by time to achieve complete healing and the reduction of scars. Nonetheless, larger or deeper burns and wounds often require a combination of treatments in addition to ReCell.

The PermeaDerm Biosynthetic Wound Matrix has earned U.S. Food and Drug Administration (FDA) clearance for use in burns and wounds and has reimbursement coverage for both inpatient and outpatient settings. The perfect overlap to AVITA Medical's commercial presence should make it easier for the sales team to sell PermeaDerm. Although the gross margin for this matrix product will be only about 50% -- much lower than the 84.5% for the core portfolio – it represents a good source of revenue growth with attractive margins. (Don't forget a mid-80% gross margin is pretty ridiculous.)

Fourth, the company is on track to receive FDA approval for its third-generation device called ReCell Go. Although I've excluded any contributions from our 2024 model, the automated device will significantly improve procedure efficiency for surgeons, operating efficiency for the business, and (believe it or not) margins for AVITA Medical's core portfolio. It'll take time for existing customers to work through inventory of prior-generation devices. Therefore, the initial impact from ReCell Go won't really be felt until late 2024, but it should make a significant impact in 2025 and 2026.

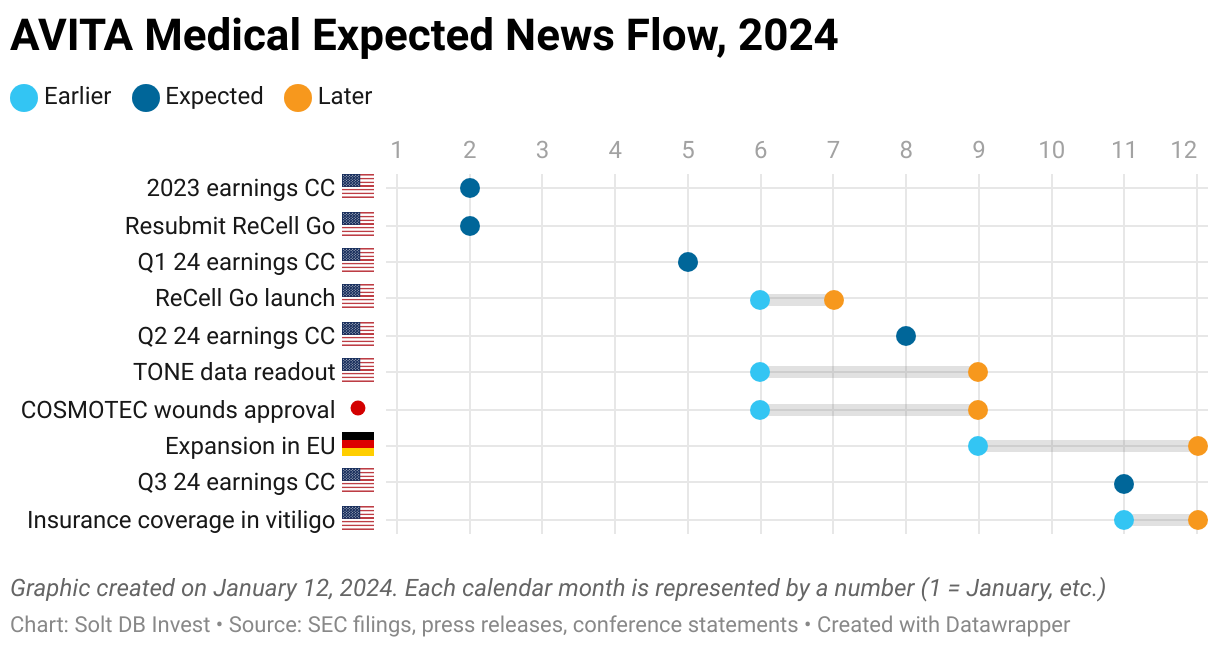

Expected News Flow for 2024

Recent years were filled with earning regulatory approvals across burns, wounds, and stable vitiligo. This year is all about delivering commercially – but there's still some meaningful news flow throughout the year.

Two events will rise to the top for 2024.

ReCell Go regulatory approval

If AVITA Medical resubmits the regulatory application for ReCell Go by February 28 and avoids additional delays, then regulatory timelines suggest the third-generation device could launch on May 31 at the earliest. That would open the entire second half of the year to introduce the device and make initial placements.

Stable vitiligo clinical trial

Although the ReCell System is FDA approved as a treatment for stable vitiligo, AVITA Medical doesn't expect to launch in the indication until early 2025. That makes sense. It needs reimbursement and insurance coverage in place to justify the additional commercial expenses, especially since a new sales team must be built. Whereas burns and wounds can leverage the same sales reps and relationships with surgeons in trauma centers, stable vitiligo requires new relationships with dermatology centers and dermatological surgeons – a completely different market.

To maximize the sales pitch and make coverage decisions easier for insurance companies, AVITA Medical is conducting a new clinical trial in stable vitiligo called TONE. The safety and efficacy of the ReCell System has already been proven and is not at stake.

Rather, TONE is a post-market study designed to understand how repigmentation of vitiligo lesions impacts quality of life for patients. The study endpoints are patient and clinician satisfaction with treatment, disease burden after treatment, and patient mental health at six months and 12 months. These are all subjective measures, which are often more difficult to quantify. That could lead to a negative surprise.

However, the pivotal clinical trial (the one that measured efficacy and was used to earn FDA approval) demonstrated an industry-leading profile for efficacy outcomes. Considering there are no meaningful treatment options, TONE is more likely than not to have a favorable outcome.

The study is fully enrolled with 109 patients as of January 2024 and should have a data readout in the second half of 2024 (after the six-month mark). The study will follow patients for 12 months, but the primary endpoints are based on the six-month mark.

How AVITA Medical Can Succeed and Fail in 2024

In 2024, AVITA Medical's trajectory will be driven by three things: Commercial execution, regulatory events, and international expansion.

Achieving success looks like

- Commercial execution for the core product portfolio in the United States is by far the most important driver for success. It will require capturing more market share across burns indications and a significant ramp in wounds procedures.

- Regulatory events need to avoid negative surprises. That means sticking close to the current timeline for resubmitting ReCell Go and earning FDA approval by the middle of the year. A minor delay might spook markets when announced, but wouldn't have a meaningful impact on the business. Meanwhile, the TONE study in stable vitiligo needs to demonstrate patients are more confident and enjoy improving quality of life six months after receiving treatment.

- International expansion is somewhat out of the company's control, but it can generate $5 million in full-year revenue (vs. $2.8 million in 2023) and could be the difference in meeting or missing guidance. COSMOTEC must continue to ramp sales of the ReCell System in burns in Japan and earn supplemental approvals in wounds. The distribution agreement with PolyMedics Innovations in Europe is less important, but Germany represents a sizable opportunity on the continent.

Failing to deliver looks like

- Commercial execution stumbles to achieve ambitious sales targets. It's unclear how much of management's expectations are driven by ReCell Go and the PermeaDerm matrix product, both of which are excluded from our model. Management set a pretty high bar for growth in 2024, and although that's in line with my model, revising guidance downward later this summer wouldn't be appreciated by the market.

- Regulatory events cough up a negative surprise. This might include another setback for ReCell Go and/or inconclusive evidence that patients with stable vitiligo see improvements in their quality of life.

- International expansion that fails to deliver higher revenue in 2024. COSMOTEC generated somewhat choppy revenue throughout 2023, which makes it difficult to predict. Meanwhile, there aren't any significant expectations for the distribution agreement with PolyMedics in Europe, so it seems unlikely to be a source of failure.

Forecast & Modeling Insights

(No change.)

Solt DB Invest's current model for AVITA Medical values the business based on expected 2024 performance, which expects:

- Full-year 2024 commercial revenue of $77.59 million

- GAAP gross margin of 84.5%

Our 2024 model doesn't include a few sources of potential upside, including:

- On October 2, 2023, we removed from the model efficiency contributions expected from ReCell Go, the company's automated third-generation device. The expected approval in 2024 will likely provide additional upside.

- No contribution from a potential new supply agreement with the U.S. Biomedical Advanced Research and Development Authority (BARDA), which may stockpile additional ReCell units following the approval in soft tissue repair. This would be accounted for as non-commercial revenue.

Margin of Safety & Allocation

AVITA Medical is considered a Growth (Quality) position. The current modeled fair valuation for the company based on our 2024 model is below:

- Market close January 11: $14.35 per share

- Modeled Fair Valuation: $16.90 per share

- Allocation Range: Up to 15%

AVITA Medical reported 25.551 million shares outstanding as of November 6, 2023. The modeled fair valuation above assumes 29.383 million shares outstanding, which is equivalent to 15% dilution.

Further Reading

- January 2024 press release announcing preliminary 2023 operating results and initial 2024 revenue guidance

- January 2024 press release announcing an exclusive distribution agreement with Stedical Scientific for the PermeaDerm matrix product

- November 2023 research note analyzing the company's decision to revise full-year 2023 revenue guidance lower

- October 2023 research note analyzing the request for more data from the FDA for ReCell Go

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)