.svg)

Shares of AVITA Medical popped over 50% after the company announced its flagship ReCell GO device has earned regulatory approval in the European Union.

If I had a tail, I'd wag it.

This is a positive development, but AVITA Medical will remain in the doghouse until it earns forgiveness through commercial execution. The blunt reality is that a regulatory green light in Europe is only as valuable as the company's ability to sell its products. In the last 12 months, the business reported European revenue of just $50,000 from its prior-generation ReCell device – including three quarters with sales of $1,000 or less. Those aren't typos.

If the company's international distributors have been twiddling their thumbs while waiting for ReCell GO to earn approvals, then approvals like this could help to offset rising uncertainty in the United States. But none of the previous three distribution agreements in Japan, Europe, or Australia have led to noticeable traction. The business generated just 3% of total revenue from international markets in the last year.

Investors can be confident ReCell GO works. It just would be easier to be confident in AVITA Medical's near- and long-term trajectory if it had a meaningful cash runway to absorb uncertainty and bumpy product launches.

AVITA Medical Has Little to Show for Global Ambitions

Management isn't necessarily wrong with its commercial strategy. It made sense to transition to a semi-durable device (ReCell GO) capable of generating high-margin consumables revenue – the ol' "razor-and-blade" business model. Similarly, it makes sense to sling products across the globe to diversify revenue. Given the high margins across the portfolio, the economics still work really well even when distributors are taking a cut.

Execution has been the problem.

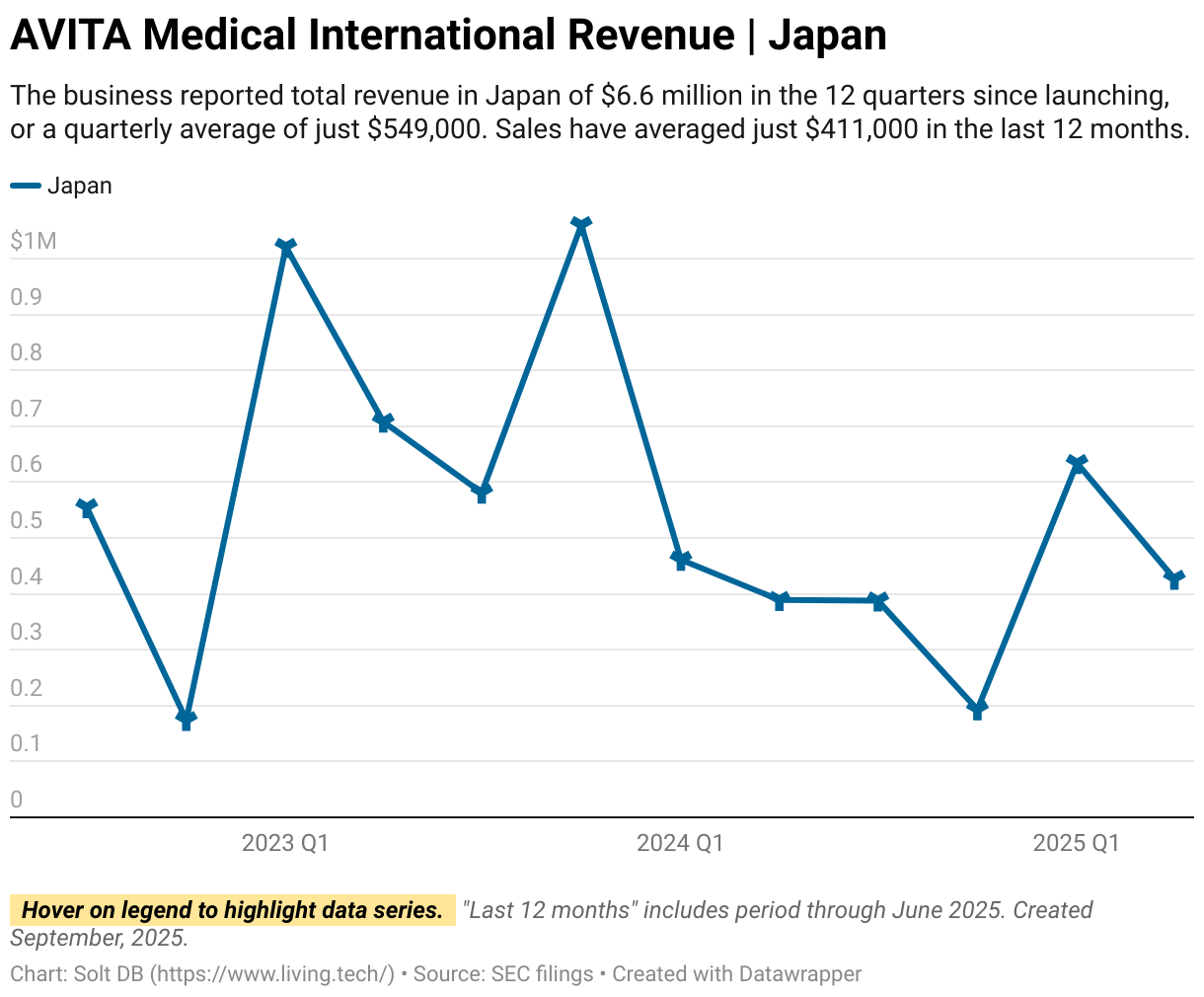

In February 2022, AVITA Medical announced regulatory approval of the prior-generation ReCell device in Japan and a distribution agreement with COSMOTEC.

Although it took two quarters to earn reimbursement, ReCell earns similar pricing in Japan and the United States. That's important considering Japan represents the second- or third-largest market depending on the basis used.

The skin grafting product has now been generating revenue in Japan for 12 quarters. The business reported total revenue of $6.6 million in that span, or a quarterly average of just $549,000. Sales have averaged just $411,000 in the last 12 months.

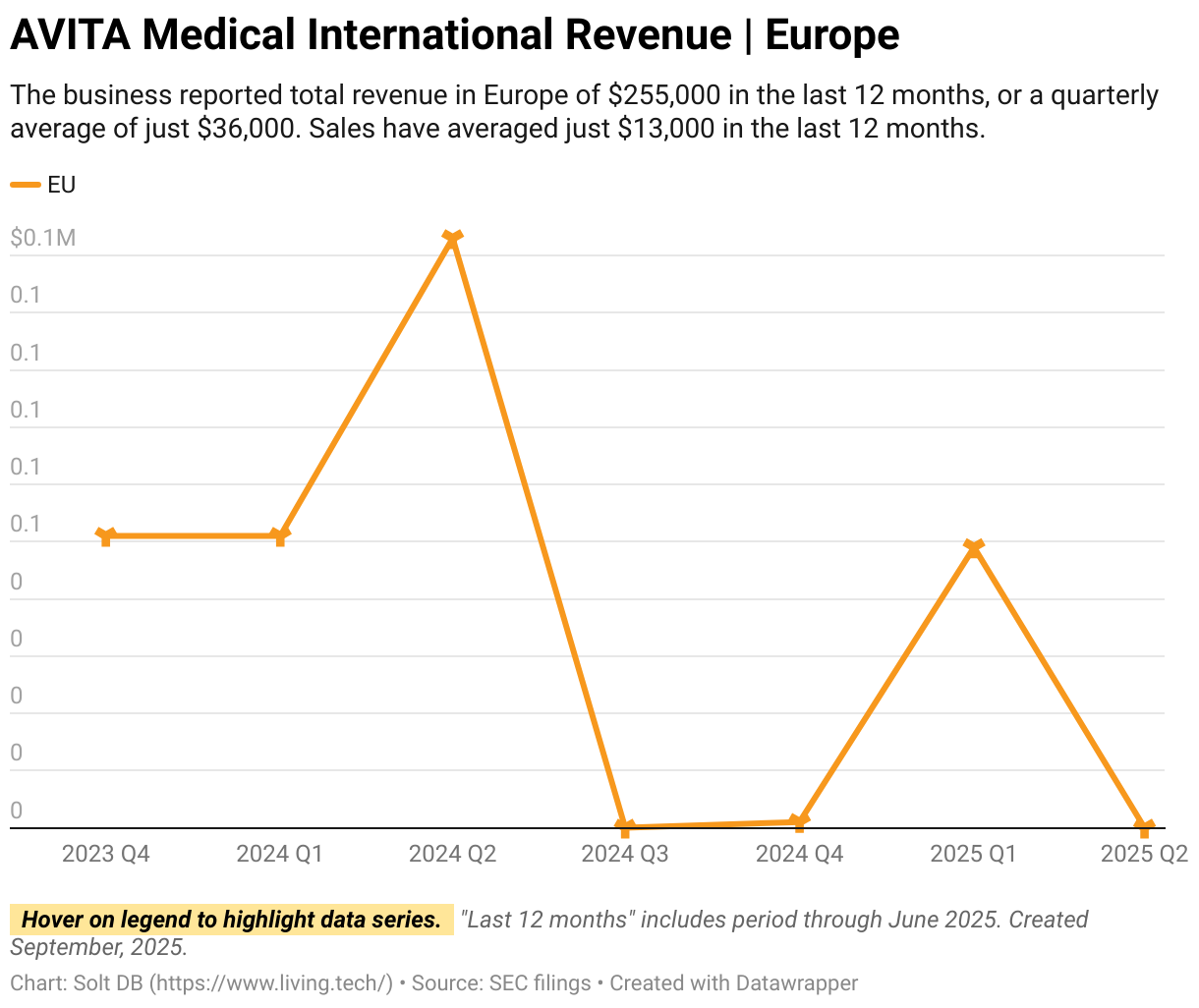

In November 2023, AVITA Medical announced a distribution agreement with PolyMedics Innovations in Europe. The agreement included Germany, Austria, and Switzerland with the option to expand into additional countries.

The prior-generation ReCell device has been available in Europe for seven quarters. The business reported total revenue of $255,000 in that span, or a quarterly average of just $36,000. Sales have averaged just $13,000 in the last 12 months.

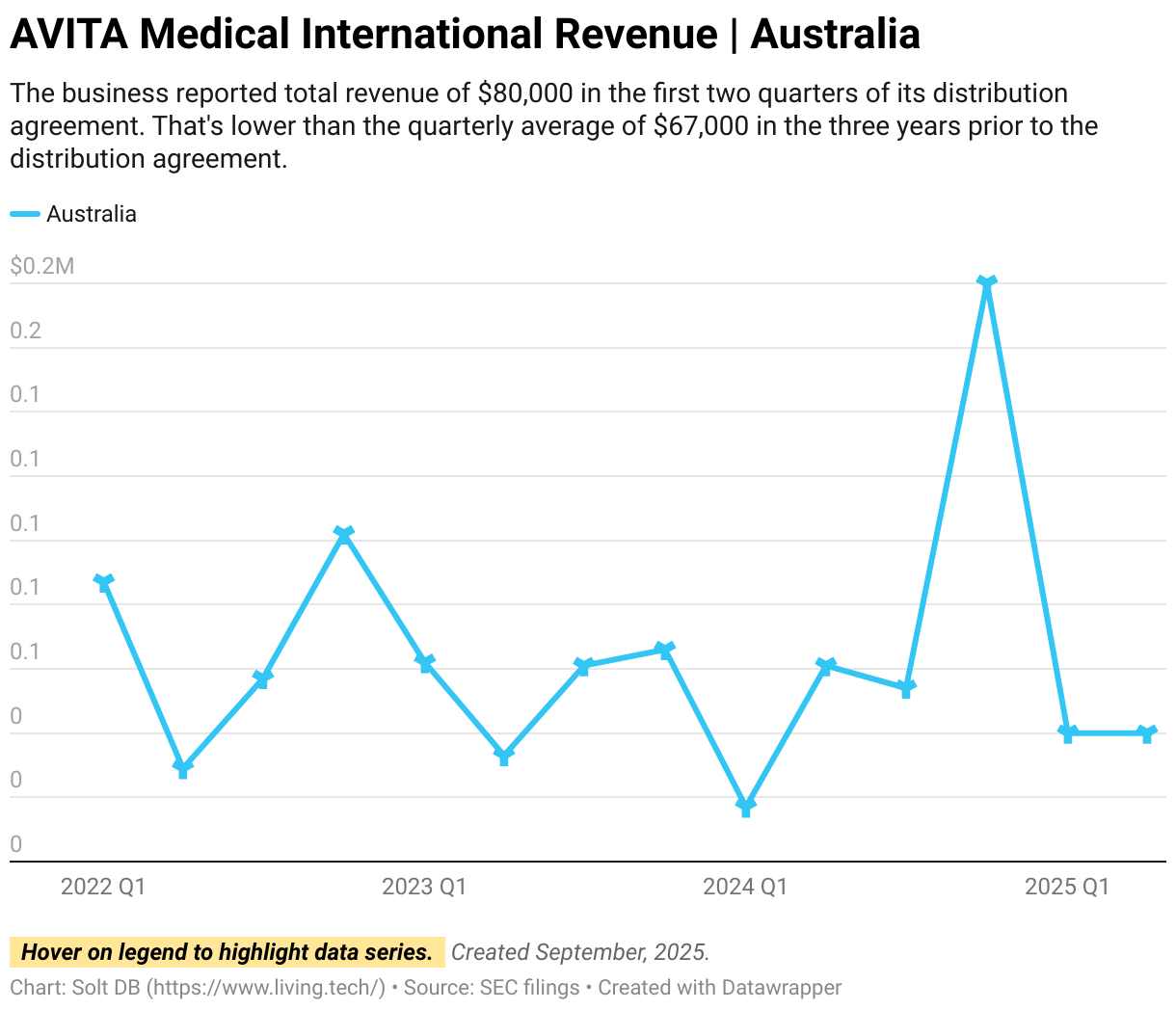

In November 2024, AVITA Medical returned home, announcing an exclusive distribution agreement with Revolution Surgical in Australia and New Zealand.

To be fair, the distribution agreement has only been active for two quarters. But the company has been selling ReCell in Australia since inception.

The business reported total revenue of $80,000 in that span, or a quarterly average of just $40,000. That's somehow lower than the quarterly average of $67,000 in the three years prior to the distribution agreement.

Is This Time Different?

It's possible AVITA Medical and its merry band of international distributors have simply been waiting for ReCell GO to earn regulatory approvals. If any product launch has the potential to change the company's fortunes, then the next-generation device is a pretty good bet.

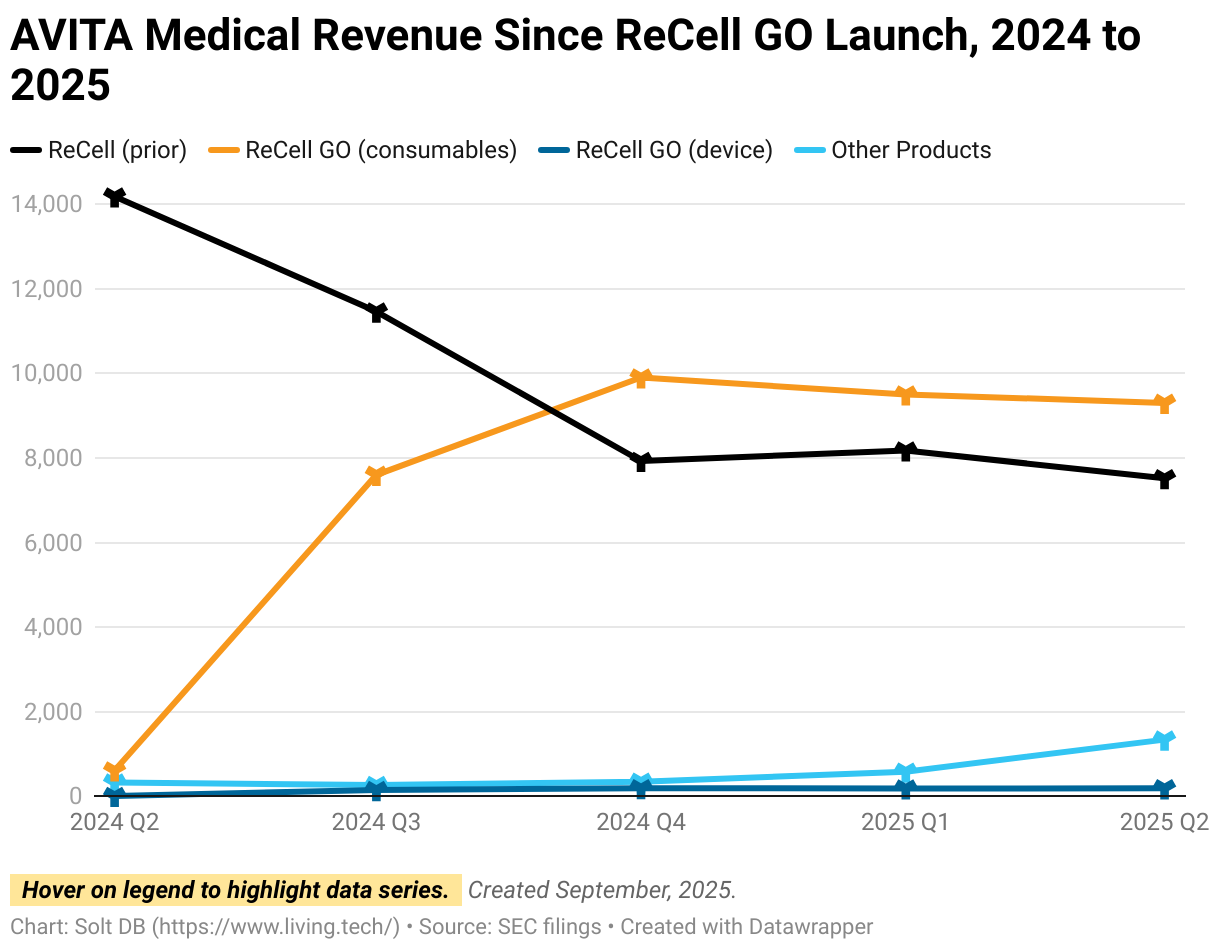

But ReCell GO hasn't exactly lived up to expectations in the United States.

In Q3 2025, the business generated 41% of total revenue and 44% of franchise revenue from the prior-generation ReCell device. The next-generation ReCell GO launched five quarters ago. We can say reimbursement woes stemming from terrible domestic policy are responsible for the poor traction and performance. I don't the negative impact.

But ReCell GO has actually generated less revenue in each of the last two quarters.

Couple ReCell GO's stalled uptake with poor commercial execution in international markets, a pattern of missing guidance, and epically mismanaging the cash runway; and investors might want to pinch themselves before getting too carried away.

Launching ReCell GO in Europe could indeed get the business back on its once-promising trajectory. Can you really trust that without seeing consistent execution though?

News Flow & Modeling Insights

(No change, new detail on share count, priced for bankruptcy.)

The business is now valued at $0 per share on a fully-diluted basis. The suggested allocation is now 0%.

The current model for 2025 operations now expects:

- Full-year 2025 revenue of $77.932 million, down from a prior model of $78.514 million, although even this may not be possible. This represents year-over-year growth of 22% – respectable, but the lowest since ReCell was commercialized. Company guidance expects $78.5 million at the midpoint.

- Full-year 2025 operating loss of $44.395 million, down from a prior model of $44.227 million.

- Full-year 2025 operating cash outflow of over $41 million, which is sharply higher than the available cash balance at the start of the year.

The current model uses an outstanding share count of 41.329 million. This is the value investors should use when determining what a future market cap level would represent as a share price.

- 619 million shares outstanding on August 4, 2025

- 400 million shares issued to OrbiMed on August 7, 2025

- 44 million shares issued to Australian investors on August 12, 2025

- 57 million shares of additional dilution expected from future capital raises

- 3 million shares issuable as stock options

Margin of Safety & Conviction

AVITA Medical is considered a Future Compounder position with the following Conviction rating.

- 1 = High

- 2 = Above Average

- 3 = Average

- 4 = Below Average

The estimated fair valuation based on my current model is below:

- Market close September 12: $4.56 per share

- Modeled Fair Valuation: $0 per share

- Allocation Range: Up to 0%

AVITA Medical reported 27.019 million shares outstanding as of August 7, 2025. The modeled fair valuation above assumes 41.329 million shares outstanding, which is equivalent to full dilution.

Further Reading

- September 2025 press release announcing CE Mark for ReCell GO in Europe

- August 2025 press release announcing a public offering of common stock of 3.44 million shares to raise gross proceeds of $15 million

- August 2025 regulatory filing (10-Q) detailing Q2 2025 operating results

- August 2025 research note analyzing Q2 2025 operating results

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)