.svg)

When everyone in drug development zigged, Arrowhead Pharmaceuticals kept on zagging. It's now ready to fall in line. Sort of.

The deflating liquidity bubble from pandemic-era fiscal policy smacked drug developers from multiple angles. First, valuations across the industry needed a reality check. Investors must accept that some biotech stocks have already reached their all-time peak. That includes several trendy stocks, including one or two in our coverage ecosystem.

Second, the days of showing up and leaving with fistfuls of cash from venture capitalists and Wall Street banks are over. A record number of biotech companies went public in 2020 and 2021. Although many were wisely accelerating their timelines to hit a sweet, sweet economic window, there was an unusual number of preclinical drug developers going public. Now, investors are demanding companies have clinical-stage assets before attempting a public debut.

Third, broad pipelines that used to be viewed as ambitious are now seen as unwieldly. A high number of shots on goal can increase the chances of getting something to market eventually, but investors have grown uncomfortable with the high costs of developing large pipelines. It's even more expensive when lower valuations (meaning fundraising terms aren't as generous) and earlier-stage pipelines (meaning development timelines are the longest they'll ever be) are factored into the calculus.

That's why most drug developers have recalibrated in the last two years. Most have announced layoffs, refocused resources on core assets, and pivoted strategies in case they need to hunker down through 2024 or 2025 or…

Arrowhead is one of the last drug developers to announce a prioritization of core assets. Sort of. The RNA interference (RNAi) leader has generally escaped fiscal scrutiny from investors thanks to its unusual strategy. The business has leveraged the broad applicability of RNAi to develop dozens of drug candidates, sell the rights to at least one asset per year, and greatly reduce cash burn with the cash received in those transactions.

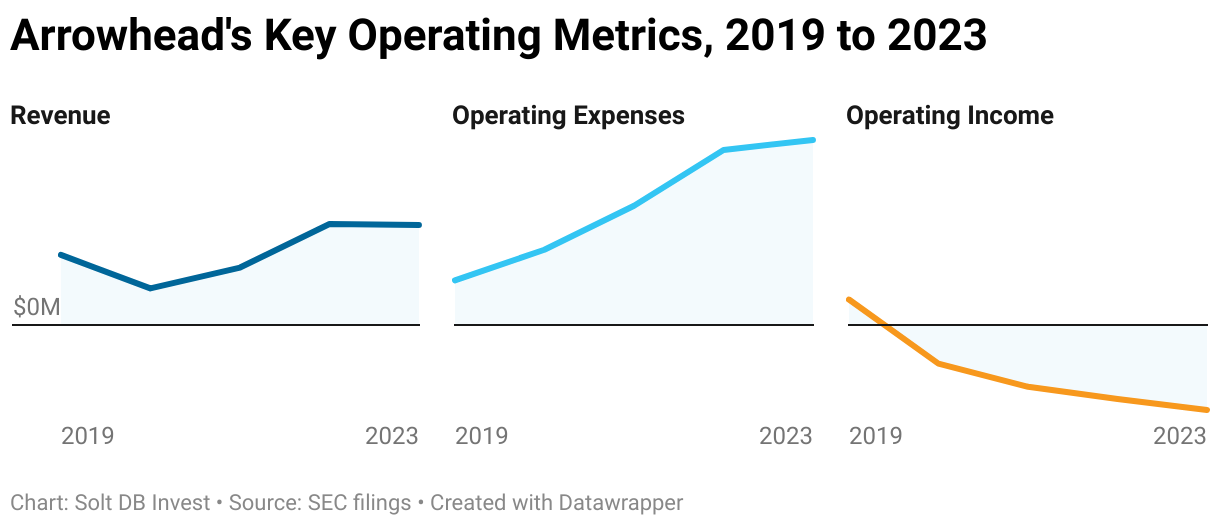

That might sound like what every drug developer attempts to do, but none have mastered it quite like Arrowhead. The company has offset $879 million in operating expenses in the last five years by monetizing its R&D platform through licenses and royalty transactions.

The partnering strategy will remain intact for non-core assets in 2024 and beyond, but it won't be enough to fund an increasingly expensive roster of RNAi drug candidates. Annual operating expenses increased from $107 million in fiscal 2019 to $445 million in fiscal 2023. And that's before the company needed to build out commercial infrastructure to support the likely launch of its first drug product in 2025, or pour resources into the emerging pulmonary (lung) pipeline.

That's why the drug developer clarified how it will deploy resources in the next few years. For Arrowhead to retain its premium valuation, it'll need to convince investors it's funded and structured to support the full vertical of operations, from early-stage drug discovery efforts to selling approved drug products.

Ambition is Expensive

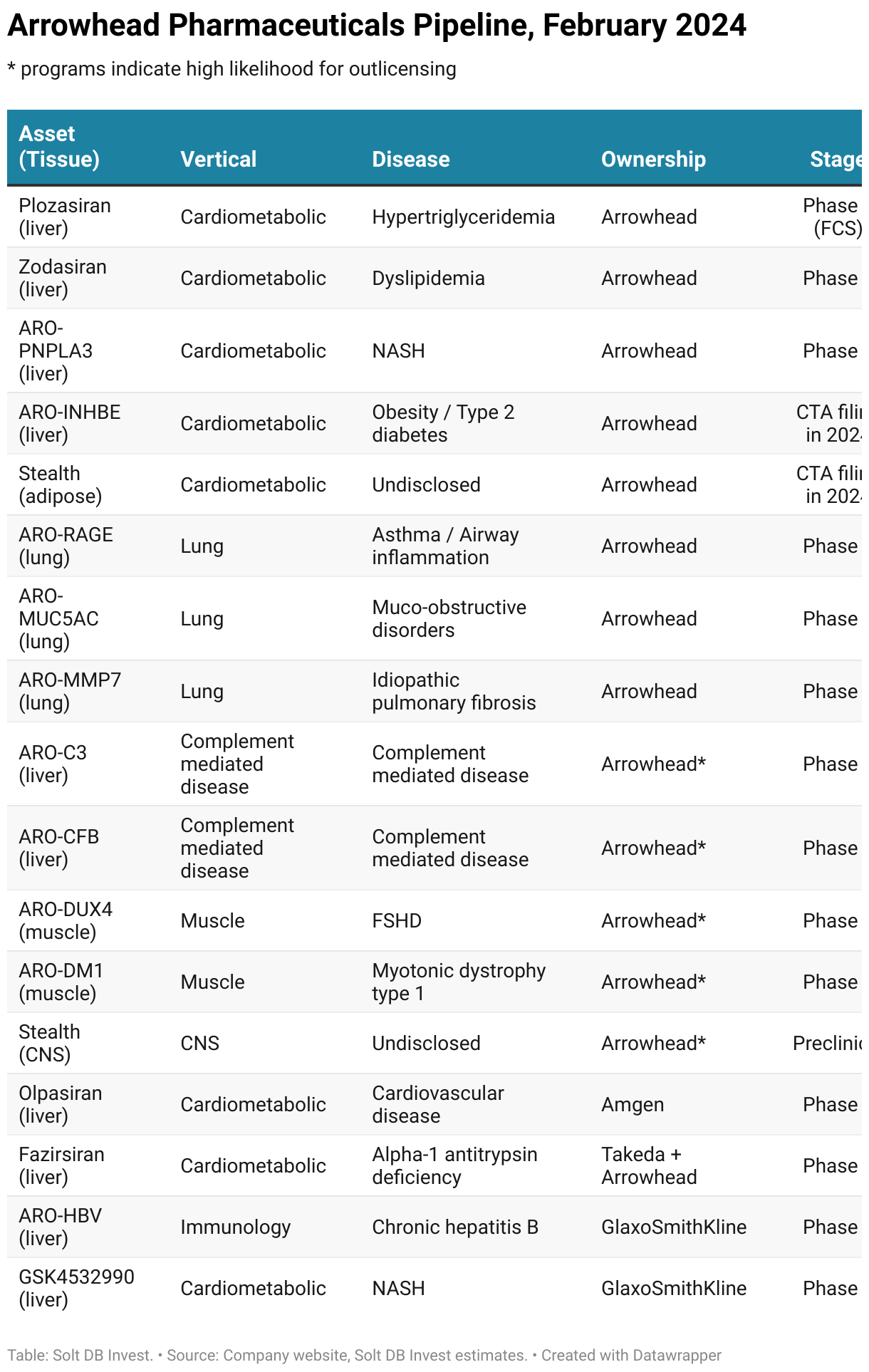

Arrowhead has an ambitious strategy called "20 in 25," which aims to have 20 assets in development or on the market by 2025. The drug developer has 16 assets in development after the fiscal first-quarter 2024 update, which suggests it will unveil at least four (4) new programs in the next year or two. The overall pipeline spans multiple therapeutic areas or verticals.

Resources will be focused on two core verticals: cardiometabolic and lung. Management said it's open to adding a new vertical to the core focus if data support such a decision. Until then, the company will advance non-core drug candidates to stages where partnerships become attractive, and no further. It expects at least one new significant licensing agreement in 2024.

That would continue the company's long track record of monetizing early R&D efforts through partnerships. That's how the precommercial drug developer reported between $88 million and $243 million in annual revenue in each of the last five fiscal years. Without it, the business would've reported an additional $879 million in operating losses from fiscal 2019 through 2023.

Devoting resources to develop non-core assets has risks, but these activities don't have to be prohibitively expensive.

For example, when Arrowhead sold the rights for ARO-LPA to Amgen in 2016, the program was only in preclinical development. The asset, now known as olpasiran, is nearing full enrollment in a phase 3 clinical trial and has generated $362 million in cash payments for Arrowhead to date. Amgen is likely to hand over an additional $50 million in the first half of calendar 2024.

Licensing the rights to olpasiran has generated a more than 10x return (so far) for the early R&D efforts. Not bad.

A continuation of the partnering strategy also makes sense for the current crop of non-core verticals:

- Complement-mediated diseases (liver tissues): It'll be difficult to compete directly with Alexion Pharmaceuticals (acquired by AstraZeneca for $39 billion) or the tie-up between Alnylam and Regeneron. A broad partnership in complement-mediated diseases makes sense, as Arrowhead won't be able to compete by itself.

- Muscle disorders (muscle tissues): Management has singled out the muscle pipeline as possibly becoming a core vertical in the future, but it'll be difficult to compete with Sarepta Therapeutics, Roche, Pfizer, and others eager to direct genetic medicines at rare muscular disorders. There's also significant development risk given the difficulty in measuring treatment effect (efficacy measures are largely subjective) and reducing side effects (from immune dysregulation to organ toxicity).

- Central nervous system (CNS) (nervous system tissues): The global industry has shown renewed interest in neuroscience after years of underinvestment. But drug development in these areas requires large, complex, and expensive clinical trials. Barring industry-leading efficacy signals, it probably doesn't make sense for Arrowhead to develop these assets on its own. Even Ionis Pharmaceuticals (full-year 2023 revenue of about $630 million) decided to tap AstraZeneca for help developing and commercializing its CNS pipeline. Ionis uses antisense oligos (ASO) to silence gene expression, similar to RNAi.

Management's execution over a meaningful period should make investors confident in the partnering strategy going forward, but the risks shouldn't be ignored, either.

For example, every asset the company has outlicensed to date targets gene expression in the liver. Delivering RNAi drug payloads to the liver is about as easy as it gets in drug development. That allowed Arrowhead to have some unusually favorable outcomes for relatively low effort and R&D spend, such as with ARO-LPA (olpasiran) and Amgen.

Some non-core assets, such as those taking aim at complement-mediated diseases, also target the liver. These will probably be partnered off first. But potential partners might be more cautious when poking around early-stage assets in CNS diseases or muscle disorders.

That could require Arrowhead to take non-core assets in certain verticals further into clinical development before partners feel comfortable acquiring rights, which would be more expensive and take longer. A lack of commercialized genetic medicines in non-liver tissues (such as CNS and muscle) could also reduce the value of future licensing agreements, since the probability of success will be less certain.

Recalibrating to Build and Support Commercial Operations

Management has essentially placed a ceiling on non-core R&D expenses. That doesn't mean operating expenses are done growing.

The ability to consistently monetize R&D efforts through licensing agreements has masked a sharp increase in operating expenses, which highlights the risks if management fails to complete new large transactions each year. Even if management maintains the partnering streak, each licensing deal will feel comparatively less valuable against increases in core operating expenses.

- Operating expenses grew from $107 million in fiscal 2019 to $445 million in fiscal 2023. That will increase in the years ahead.

- Arrowhead needs to invest in building commercial infrastructure for its late-stage cardiometabolic assets, which could receive the company's first-ever regulatory approval in 2025. Drug developers typically see larger operating losses in the two years following their first drug launch.

- The company also needs to fund the development of an emerging pulmonary (lung) pipeline. Retaining full rights to the assets can allow the drug developer to capture a larger economic opportunity years from now, but it'll be an expensive multi-year journey through the clinic.

Here's the data visualization from above showing key operating metrics in recent years.

It's important to remember that currently partnered assets can generate seven-figure milestone payments here and there, including an expected $50 million payment from Amgen in mid-2024. But there's less certainty here than investors might expect.

Horizon Therapeutics (Amgen) terminated an early-stage gout candidate licensed from Arrowhead. GlaxoSmithKline is evaluating a NASH drug candidate, but the competitive landscape looks less favorable since the licensing deal was struck. Meanwhile, the license for a chronic hepatitis B drug candidate has changed hands from Janssen (Roche) to GlaxoSmithKline amid pipeline prioritization decisions at industry leaders.

That raises the stakes for a phase 3 data readout for fazirsiran in alpha-1 antitrypsin deficiency (A1AT). The asset is being developed by Takeda, although Arrowhead will split profits 50/50 if the drug candidate reaches market. The RNAi drug candidate works as expected in terms of reducing the buildup of misfolded proteins that are the hallmark of the disease.

However, a phase 2 clinical trial showed 39% of individuals receiving placebo reported reductions in liver scarring (fibrosis), compared to an expected rate of 15%. This unusual benefit in the placebo group made the comparison to fazirsiran less favorable, as 50% of individuals receiving treatment saw fibrosis reductions (50% vs. 39% isn't a great separation, whereas the expected 50% vs. 15% is more significant).

That cannot happen in the phase 3 study. Fibrosis reduction was a secondary endpoint in the mid-stage trial, but it's the primary endpoint in the pivotal study now underway. There could still be a path to approval, especially since Novo Nordisk dropped out of the race with its own RNAi drug candidate, but the share price would take a hit on the uncertainty and reduced label claims.

Forecast & Modeling Insights

(Introduced.)

Investors can organize Arrowhead's assets into three categories:

- Core Assets: Wholly-owned assets in core verticals make the largest contribution to the company's valuation. This is primarily driven by late-stage cardiometabolic assets with the potential to enter very large patient populations. Although the lung pipeline holds asymmetric potential, the assets are still in early-stage development.

- Non-Core Assets: Wholly-owned assets in non-core verticals contribute to the company's valuation, too. But the value of these individual assets must acknowledge that development will likely be paused at a certain stage as Arrowhead courts potential partners.

- Licensed or Partnered Assets: These create immediate value through upfront cash payments when licensing agreements are initially executed. If assets advance through clinical trials, then Arrowhead can earn milestone payments. If assets earn regulatory approval years later, then Arrowhead can earn both royalties and milestone payments.

The largest contributions to the company's valuation, estimated at $4.658 billion in our current 2024 model, come from two wholly-owned, late-stage cardiometabolic assets.

Plozasiran

Arrowhead will notch its first-ever phase 3 data readout when results for plozasiran in familial chylomicronemia syndrome (FCS) are announced in mid-2024. FCS is a rare genetic condition where individuals have very high triglyceride levels. Although it represents a small patient population, that's okay – and actually preferred.

As Arrowhead builds out commercial infrastructure for the first time, it's going to encounter missteps, setbacks, and delays. One way to minimize the risks of inexperience is to launch in a small market where the stakes are lower, implement improved workflows and procedures, and then expand into larger markets with all that newfound wisdom.

FCS is a rare genetic condition characterized by high triglyceride levels, but there are common conditions driven by similar imbalances. That's why Arrowhead plans to begin a phase 3 study in patients with severe hyperglyceridemia (SHTG) in the current quarter. SHTG impacts an estimated 3 million to 4 million patients in the United States, compared to a few thousand patients with FCS.

Investors can also have a high degree of confidence in a successful trial outcome in SHTG. Plozasiran has already proven the ability to silence its gene target (APOC3 expressed in the liver) safely and effectively. In fact, the asset achieved a 60% median reduction in triglyceride levels from baseline in a phase 2 clinical trial. No other approved treatment can reduce levels by more than 30%.

Zodasiran

The second-most advanced cardiometabolic asset is being developed to treat high cholesterol. Zodasiran delivered a successful phase 2 study in homozygous familial hypercholesterolemia (HoFH) and is expected to advance to phase 3 soon.

Similar to plozasiran, Arrowhead intends to launch zodasiran in a small market such as HoFH before expanding into potentially larger markets. The latter is the much more common version of the disease called HeFH.

Plozasiran / Zodasiran

Arrowhead intends to develop either plozasiran or zodasiran in atherosclerotic cardiovascular disease (ASCVD), which is more commonly known for its symptoms of plaque buildup in arteries. The drug developer will likely make that decision after seeing phase 3 data for plozasiran in FCS and readouts from the competitive landscape.

Even though it'll have less mature data, zodasiran might still be the choice. The asset demonstrated the unusual ability to reduce remnant cholesterol, thought to be a key contributor to ASCVD. No other drug candidate in the industry pipeline has delivered as meaningful reductions.

No matter the choice, the eventual ASCVD clinical trial will become the most important value driver for the company. That's because plaque buildup impacts nearly 20 million individuals in the United States. Earning approval in this indication could easily make an asset a blockbuster.

Margin of Safety & Allocation

Arrowhead Pharmaceuticals is considered a Growth (Quality) position. The current modeled fair valuation for the company based on our 2024 model is below:

- Market close February 7: $31.65 per share

- Modeled Fair Valuation: $32.69 per share

- Allocation Range: Up to 5%

Arrowhead Pharmaceuticals reported 123.896 million shares outstanding as of January 31, 2024. The modeled fair valuation above assumes 142.480 million shares outstanding, which is equivalent to 15% dilution.

Further Reading

- February 2024 press release announcing fiscal first-quarter 2024 business updates

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)