.svg)

Want an email alert every time a Finch Trade goes live? Sign up in your profile.

If you're investing in biotech stocks, then RNAi platforms are a must-have allocation in your portfolio. Arrowhead Pharmaceuticals is the best-positioned for growth (and share gains) among its publicly-traded peers. That remains true even after the recent run up.

Unfortunately for me, I'm still searching for a real job. Selling this position locks in a 236% return and extends my personal cash runway into the spring.

To be clear, I consider Arrowhead Pharma a core position. I wouldn't recommend fully exiting the position and would be careful resizing it. Let it ride! Or, at the very least, plan on buying back any trimmed shares at a lower price.

A Word on the Current Model

I'll provide an update on the outlook for Redemplo and a refined model this month.

As a reminder, the current model only includes the value of Redemplo (plozasiran) in familial chylomicronemia syndrome (FCS) and risk-weighted contributions from the label expansion studies in severe hypertriglyceridemia (sHTG), which means it doesn't capture the full value of the business.

[I've updated company pages in the Margin of Safety Dashboard to reflect what is and isn't included in each respective model. Here's a link to Arrowhead Pharma's company page).

If Redemplo is on the path to approval for much larger indications like sHTG or broader label claims like reducing pancreatitis, then it could become the second or third-ever blockbuster RNAi drug. If you applied a probability of success (POS) equivalent to liver targets for RNAi to the entire pipeline (most of which is directed to the liver anyway), then valuation in the ballpark of $10 billion or roughly $72 per share isn't crazy.

At the same time, Arrowhead Pharma is benefitting from how the market is interpreting the impact of interest rate cuts. Lower interest rates make it easier for capital to flow into riskier assets, like the stocks of cash-burning drug developers. The issue is that when interest rates are cut heading into a recession, then that benefit evaporates. I lean toward an economic contraction on the horizon.

Additionally, merger and acquisition (M&A) activity is picking up in drug development. In the first half of 2025, companies made 20 acquisitions totaling $37.1 billion. In the second half of 2025, there have been 24 acquisitions totaling $69.2 billion (excludes Exact Sciences) -- and there are four weeks remaining. Arrowhead Pharma would be one of the most coveted platforms and pipelines to acquire, so investors are applying a rich premium. At least some of that can unwind if the speculative winds die down.

Do I Plan to Re-enter Arrowhead Pharma?

Absolutely. I intend to build a bigger position in Arrowhead Pharma in the next few years. It would be one of my highest priorities in a market downturn.

Here's a teaser: Solt DB will introduce model portfolio frameworks (once when I find a stable job).

- Model Portfolio Frameworks: Preservation, Growth, and Aggressive

- Investment Group Allocations: Cash, Index ETF, Current Compounders, and Future Compounders

- Individual Position Sizing: Each model portfolio framework will have unique allocation range suggestions for each Investment Group and for individual positions within each Investment Group.

This will allow me to communicate more nuanced information for individual positions depending on how it fits into your risk tolerance, time horizon, and portfolio size.

For example, an Aggressive Portfolio might have allocations of:

- 0% Index ETFs

- 5% Cash

- 20% Current Compounders (two individual positions)

- 75% Future Compounders (three to four individual positions)

Drilling down one more layer, each of the individual positions in the Future Compounders group would be sized based on conviction.

- Future Compounder A = 30% to 40% of total portfolio allocation

- Future Compounder B = 18% to 20%

- Future Compounder C = 10% to 15%

- Future Compounder D = 0% to 5%

Relay Therapeutics would be slotted into "Future Compounder A" as the highest-conviction position in the group. If it was acquired tomorrow, then the next company to claim the title of "Future Compounder A" might not have the same allocation range.

This long-winded explanation provides more context for how I think about Arrowhead Pharmaceuticals. The RNAi leader would make a fine Future Compounder A or Future Compounder B – it could comfortably be at least 15% of your portfolio using either the Growth (not shown) or Aggressive framework (listed above).

Don't forget, the whole point of discovering overlooked opportunities is to enjoy the power of compounding if you're proven right. There's no rule that says you have to sell or trim a position once it reaches a return of 50% or 250% or 1,000%. Outside of bubbles and speculative fervor, you don't get 250% or 1,000% returns without holding a position for a very long time.

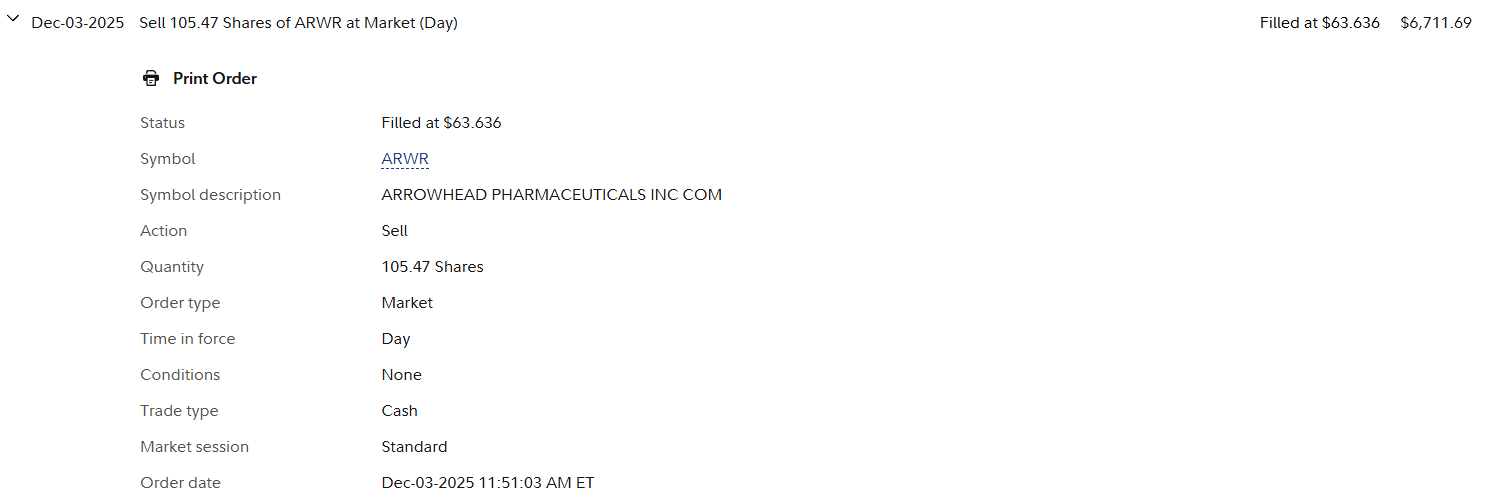

The Trade

I sold 105.47 of Arrowhead Pharmaceuticals at $63.63 per share on December 3, 2025.

This position was closed, resulting in a gain of +236% and +$4,712. The S&P 500 gained +20% while the position was active, resulting in a net performance of 216% compared to passive investing.

Margin of Safety & Allocation

Arrowhead Pharmaceuticals is considered a Future Compounder position. The estimated fair valuation based on my current model is below:

- Market close December 3: $65.07 per share

- Modeled Fair Valuation: $28.27 per share

- Allocation Range: Up to 15%

Arrowhead Pharmaceuticals reported 135.809 million shares outstanding as of November 19, 2025. The modeled fair valuation above assumes 136.953 million shares outstanding, which is equivalent to 1% dilution.

Further Reading

- Real-time announcement on Discord

- October 2024 Finch Trades transaction

- September 2024 Finch Trades transaction

.svg)

.svg)

.avif)

.png)

.svg)

.svg)

.svg)