.svg)

Big pipelines require big budgets.

At least in the case of Arrowhead Pharmaceuticals, a focus on RNA interference (RNAi) suggests the ambitious plans will be a good long-term investment. It's the "long-term" part that will test the resolve of investors.

According to my datasets, an estimated 60% of all liver-directed RNAi drug candidates that enter a phase 1 clinical trial earn U.S. Food and Drug Administration (FDA) approval – 7.5x the industry average. No other therapeutic modality is even close.

To be fair, that statistic is based specifically on drug payloads guided to the liver. A pipeline now targeting cells in the lungs, muscles, and brain means investors cannot yet expect the same level of sweeping success. But from a nerdy science perspective, if you can design a selective RNAi payload and deliver it to the right place, then it should efficiently silence genes for a meaningful amount of time with limited side effects.

A higher probability of success (POS) translates into a higher valuation and higher premium. Investors can be confident in that. Unfortunately, it doesn't directly address the challenges of managing cash flow for a pipeline expanding from top (with assets maturing into late-stage studies) to bottom (with new assets).

The late-stage drug developer's commitment to an internal drug pipeline could generate significant value over time, but it sure is expensive. When Arrowhead slipped the bill across the table after announcing fiscal second-quarter 2024 operating results the company's date on Wall Street balked at the price.

Here's a little Band-Aid ripping: If investors are excited by the near- and long-term potential of Arrowhead (as am I), then they must accept the cost. It helps to understand some additional context about the surge in R&D expenses and timing of licensing and milestone revenue.

By the Numbers

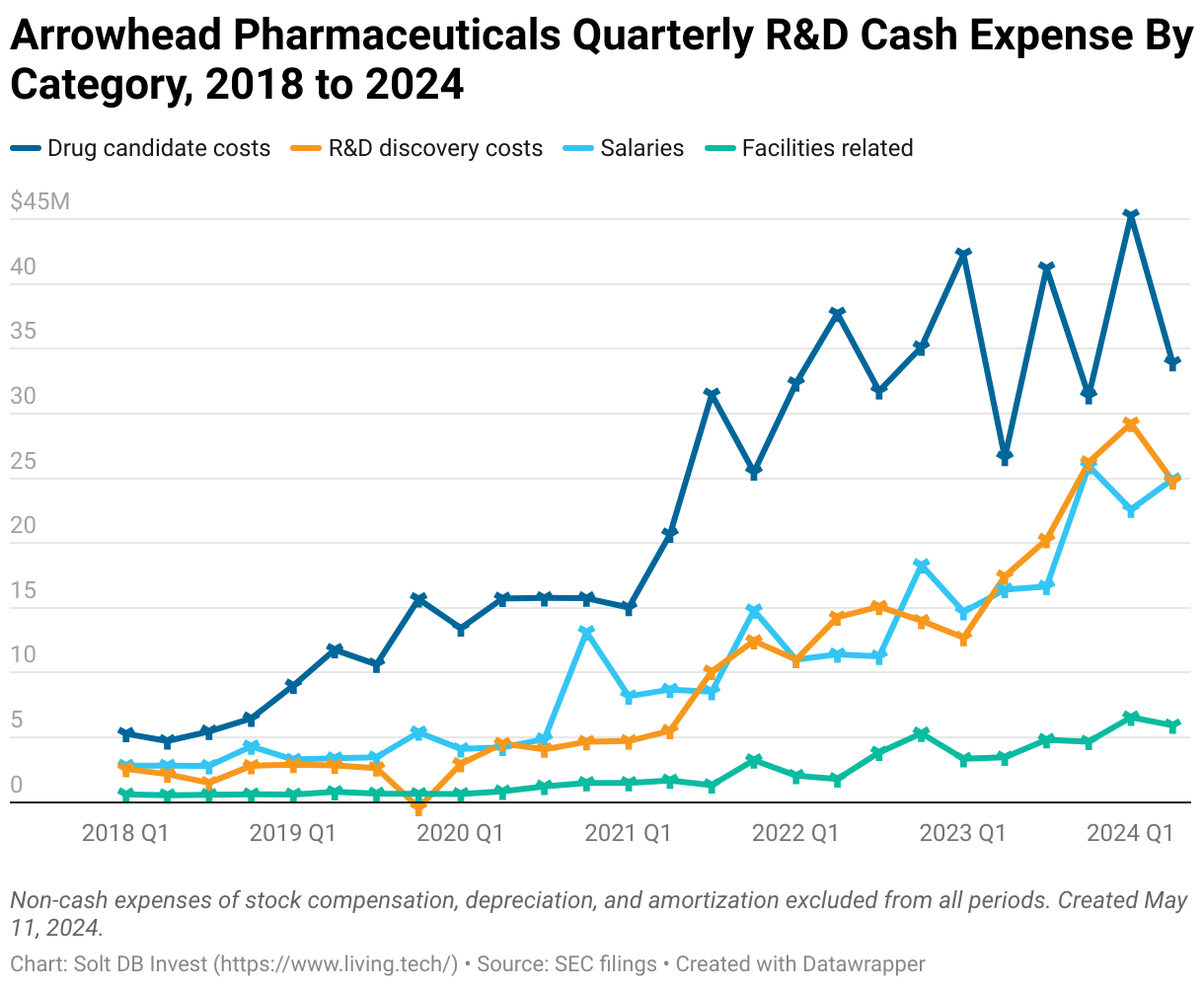

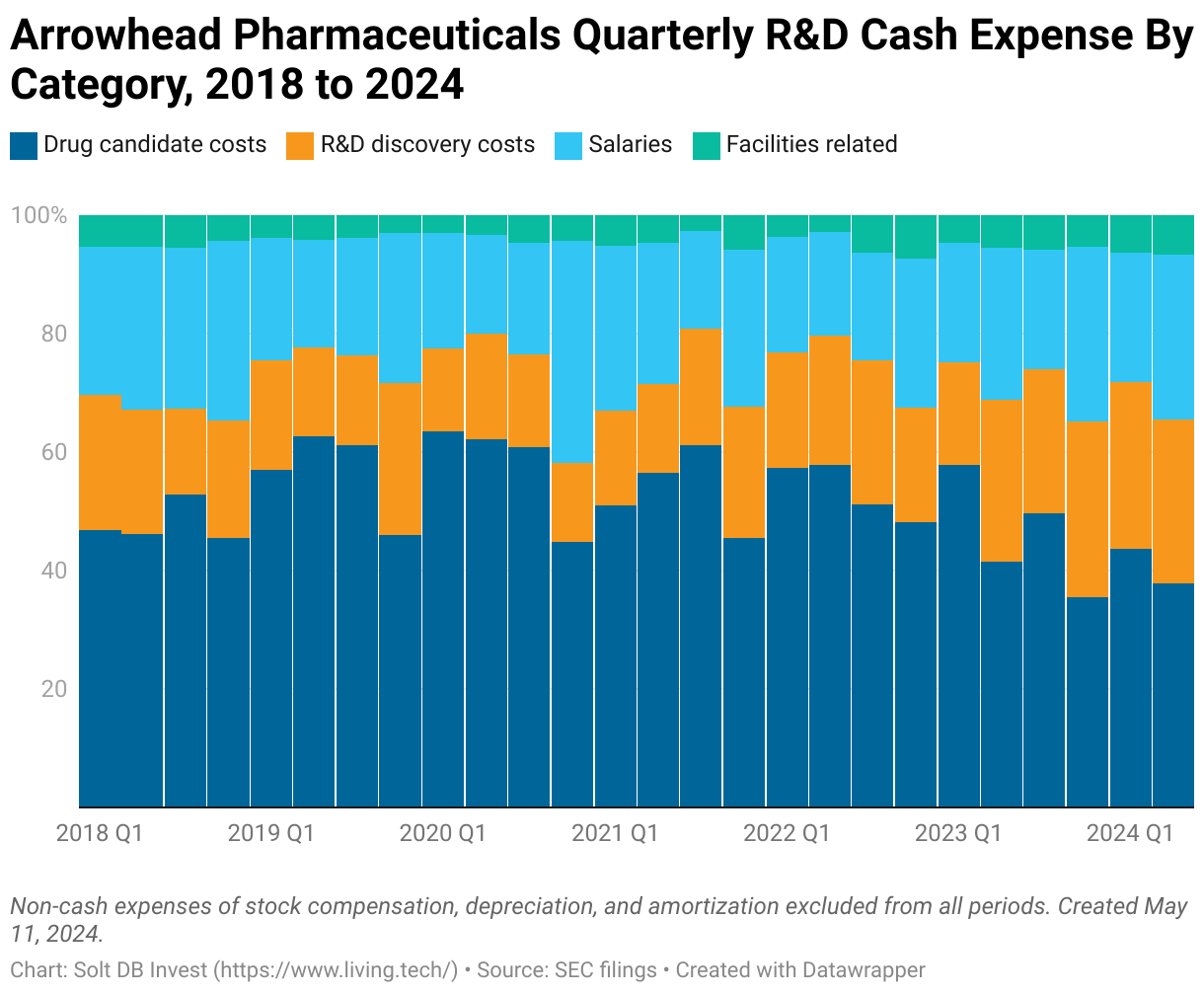

Arrowhead Pharmaceuticals ended March 2024 with $534 million in cash. Is that a lot? A little? It's all relative. The business reported a fiscal first-half 2024 operating cash burn of $210 million. That exceeded the annual total from 2023 by 37%. Swelling investments in R&D explain the rise – with no shortage of striking historical comparisons when spending is broken down by category.

In the first six months of this year, the company paid $54 million for discovery-stage R&D and $79 million for clinical-stage R&D. Spending on those individual categories match or exceed the company's entire R&D budget from fiscal 2018 and fiscal 2019, respectively.

Total R&D cash expenses grew from $46 million in 2018 to $308 million in 2023. While all categories grew in that span, discovery-stage R&D has represented at least 24% of total R&D cash expenses for five consecutive quarters. That level has only been met in two other quarters since the beginning of 2018.

Meanwhile, total compensation per employee rose more than 58% from 2018 to 2023. That has compounded with a 352% jump in headcount in that span.

Wall Street analysts are frustrated management has bucked the industry trend by deciding against layoffs (so far), choosing to instead cut costs by nixing early-stage assets while continuing investments in its people. I think in many cases layoffs are a sign of poor management, so we'll see who blinks first.

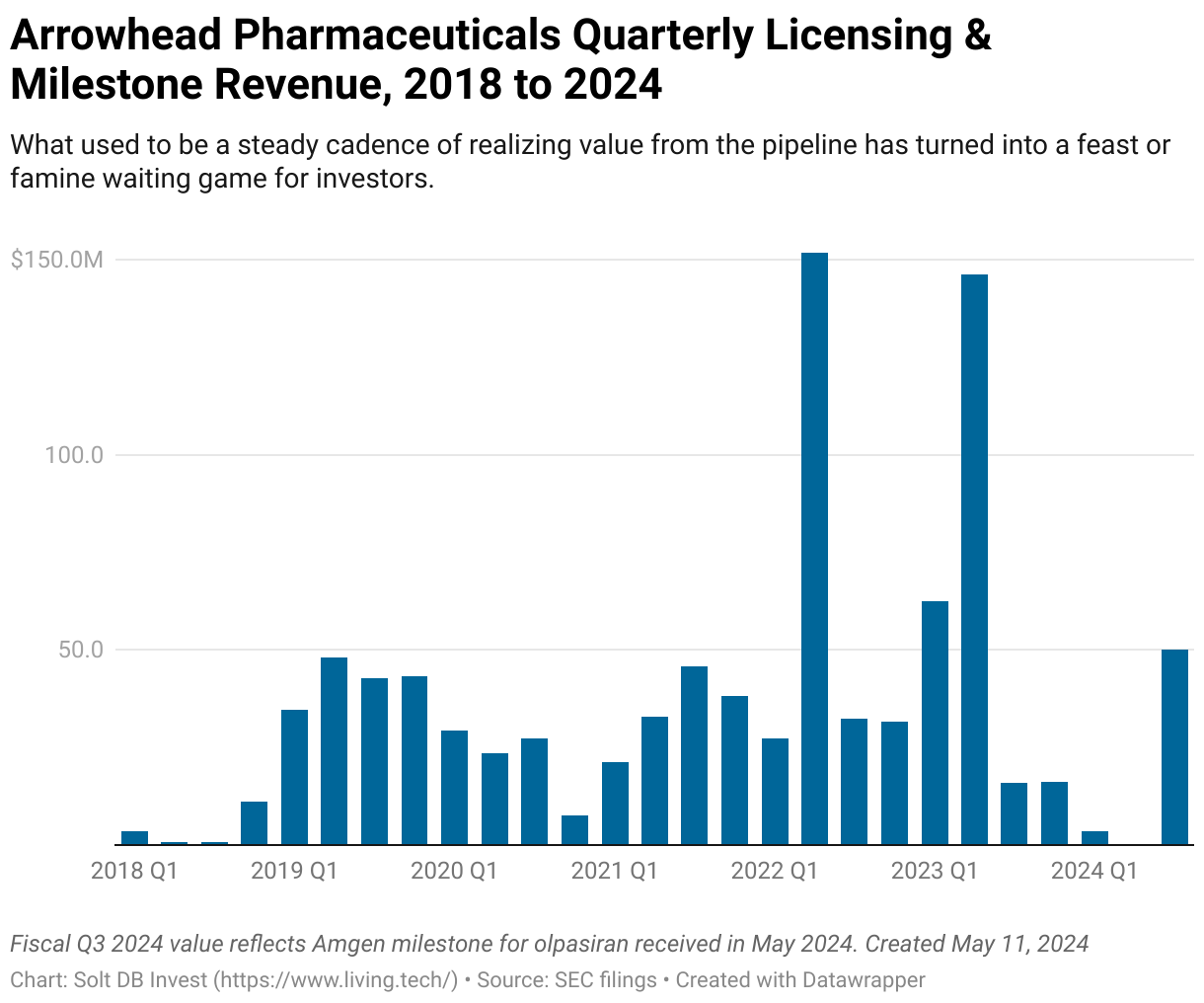

These expense growth trends aren't unusual for a maturing drug developer. They're just a little more acute for Arrowhead, which offset $879 million in R&D expenses by monetizing pipeline assets from 2018 to 2023.

The well's been a little drier recently. After hauling in $209 million in the first two quarters of fiscal 2023, the drug developer has generated licensing and milestone revenue of only $35 million in the four quarters since. That included just $3.5 million in the fiscal first quarter of 2024, which was the lowest quarterly revenue level in almost six years.

Revenue in the fiscal second quarter of 2024 was even lower – at zero – but investors will see some relief soon. Amgen completed enrollment in a phase 3 clinical trial of cardiometabolic drug candidate olpasiran, which triggered a $50 million cash payment Arrowhead will realize in its current fiscal third quarter.

Management intends to continue monetizing pipeline programs and capabilities. The current strategy is to complete initial development of assets across cardiometabolic, pulmonary (lung), muscle, and brain indications before outlicensing them for upfront payments and long-term value share.

The drought in R&D licensing revenue has coincided with a rise in R&D cash expenses, but is also occurring soon after the largest amount of stock dilution in seven years. Given that context, investors are a little more nervous about large stock offerings becoming the norm for the foreseeable future.

Luckily, my modeled price and the Margin of Safety already include an additional 15% dilution from the current number of shares outstanding.

Around the Horn

Investors can organize Arrowhead's assets into three categories:

- Core Assets: Wholly-owned assets in core verticals make the largest contribution to the company's valuation. This is primarily driven by late-stage cardiometabolic assets with the potential to enter very large patient populations. Although the lung pipeline holds asymmetric potential, the assets are still in early-stage development.

- Non-Core Assets: Wholly-owned assets in non-core verticals contribute to the company's valuation, too. But the value of these individual assets must acknowledge that development will likely be paused at a certain stage as Arrowhead courts potential partners.

- Licensed or Partnered Assets: These create immediate value through upfront cash payments when licensing agreements are initially executed. If assets advance through clinical trials, then Arrowhead can earn milestone payments. If assets earn regulatory approval years later, then Arrowhead can earn both royalties and milestone payments.

The largest contributions to the company's valuation, estimated at $4.658 billion in my current 2024 model, come from two wholly-owned, late-stage cardiometabolic assets: plozasiran and zodasiran.

Plozasiran

Since the last research note in February 2023, Arrowhead published updated phase 2 data for plozasiran. The RNAi drug candidate dampens production of apolipoprotein C-III (APOC3), which plays a key role regulating triglyceride levels.

The therapeutic goal is to bring triglyceride levels into normal ranges, which can improve cardiovascular health. The commercial goal is to initially treat rare cardiometabolic diseases characterized by high triglyceride levels, before potentially studying the asset's ability to broadly improve cardiovascular health in the general population. Arrowhead will choose either plozasiran or zodasiran (next section) for the latter development plan.

One thing that makes liver-directed RNAi drug candidates so likely to succeed is the ability to finely control dose-dependent responses. The full phase 2 data for plozasiran in patients with severe hypertriglyceridemia (SHTG) demonstrated this perfectly:

- The study evaluated three doses of plozasiran: 10 mg, 25 mg, and 50 mg.

- At 24 weeks, the ascending doses led to APOC3 reductions of 68%, 72%, and 77%, which shows the drug candidate successfully hit the genetic target. Those doses led to reductions in triglycerides of 49%, 53%, and 57%, which shows hitting the genetic target successfully drove a clinical response.

- The numbers above are all placebo-adjusted. That means APOC3 and triglyceride reductions were tracked in individuals receiving placebo, too, then subtracted from the reductions in individuals who received plozasiran. In other words, these were no-doubter results (p values < 0.001).

- Importantly, the reductions in triglycerides helped individuals achieve clinically-meaningful goals. Over 90% of individuals achieved a triglyceride level under 500 mg / dL, which is a level associated with increased risk of pancreatitis. Over 48% of patients achieved normal triglyceride levels of less than 150 mg / dL. For context, the average study participant started with triglyceride levels of nearly 900 mg / dL.

Arrowhead will soon begin two, 48-week phase 3 studies of plozasiran in SHTG.

Meanwhile, an ongoing phase 3 study of plozasiran in individuals with familial chylomicronemia syndrome (FCS) is expected to be completed in summer 2024. That means investors can expect the company's first-ever phase 3 data readout later in the calendar year.

Zodasiran

Zodasiran is another late-stage cardiometabolic asset. The RNAi drug candidate dampens production of angiopoietin-like protein 3 (ANGPTL3), which plays a key role in regulating lipid levels.

The company has shown zodasiran can reduce blood levels of low-density lipoprotein (LDL) cholesterol, blood levels of triglycerides, and liver levels of triglycerides. Like plozasiran, zodasiran is being studied as a treatment for rare cardiometabolic diseases. But Arrowhead has evaluated both of its prized assets as a potential treatment for dyslipidemia, which impacts millions of Americans. It intends to advance only one into phase 3 studies.

Licensed or Partnered Assets

Arrowhead has outlicensed a handful of assets to partners across the global industry. The two most-advanced are olpasiran (Amgen) and fazirsiran (Takeda).

- Olpasiran is designed reduce the risk of cardiovascular disease by dampening production of apolipoprotein A (LPA). It could be a very valuable drug product, but it also requires very large, long-duration clinical trials. Amgen recently completed enrollment in a two-year study with 6,000 patients. Preliminary data readouts are likely before the study officially wraps up, but full results won't be available until mid-2027.

- Fairsiran is designed to treat alpha-1 antitrypsin deficiency (A1AT) liver disease by reducing levels of mutant Z-AAT proteins that are the hallmark of the disease. The asset's value is strongly driven by the fact it's partnered with Takeda, which is the global leader in augmentation therapy that provides individuals with working copies of the protein. However, that only treats lung manifestations of the disease, leaving individuals with liver damage. Arrowhead and Takeda will split U.S. profits 50/50, while the RNAi specialist will receive hefty royalties of 20% to 25% on ex-U.S. net sales. The expected completion date of the 230-week phase 3 clinical trial: 2029.

Other Assets

Arrowhead has scheduled a series of R&D webinars in each of the next five months. Each will dig into the individual pipelines and assets being developed by the company. I'll provide detailed deep dives into the assets after each event.

- May 23 – Muscular

- June 25 – Cardiometabolic

- July 16 – Pulmonary (Lung)

- August 15 – Obesity & Metabolic

- September 25 – Central Nervous System (CNS)

Note that obesity is technically a cardiometabolic indication, but given the current environment it makes sense to carve out a dedicated time for the company's efforts there.

Margin of Safety & Allocation

Arrowhead Pharmaceuticals is considered a Growth (Quality) position. The current modeled fair valuation for the company based on my 2024 model is below:

- Market close May 10: $22.08 per share

- Modeled Fair Valuation: $32.61 per share

- Modeled Fair Valuation: $4.658 billion

- Allocation Range: Up to 5%

Arrowhead Pharmaceuticals reported 124.200 million shares outstanding as of May 1, 2024. The modeled fair valuation above assumes 142.830 million shares outstanding, which is equivalent to 15% dilution.

Further Reading

- May 2024 press release announcing fiscal Q2 2024 operating results

- May 2024 regulatory filing (10-Q) detailing fiscal Q2 2024 operating results

- February 2024 research note analyzing fiscal Q1 2024 operating results

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)