.svg)

It was founded as a nanotechnology holding company, pivoted to three separate technology platforms for RNA interference (RNAi), and took its lumps in antivirals and oncology. But after a long trek Arrowhead Pharmaceuticals is finally nearing the mountaintop.

The RNAi pioneer has now advanced four unique assets into late-stage studies – an accomplishment in itself. That includes plozasiran, which is poised to clinch the company's first-ever approval in November 2025. Data from the pivotal PALISADE study – named after a mountain peak – support approval in familial chylomicronemia syndrome (FCS) and suggest it will become the dominant treatment.

Yet, with a U.S. patient population of less than 1,000 individuals, an approval in FCS alone would be more symbolic than commercially-meaningful. Plozasiran needs additional approvals in larger market opportunities to become a high-impact asset. There's good news on that front.

The pivotal SHASTA-3, SHASTA-4, and MUIR-3 studies – all named after mountain peaks – have each completed enrollment. If topline data readouts expected in mid-2026 demonstrate plozasiran's ability to help individuals with severe hypertriglyceridemia (SHTG) lower triglyceride levels, then the asset's commercial opportunity would expand to 3.5 million Americans in 2027. Not a bad step up.

Although plozasiran is a key driver in the next few years, Arrowhead is brimming with potential beyond the lead asset.

The pivotal YOSEMITE study – named after a mountain peak… are you guys catching on yet? – evaluating zodasiran in homozygous familial hypercholesteremia (HoFH) recently began enrolling patients. Topline data could be available in the second half of 2027, setting up licensing opportunities.

The first-ever data for two wholly-owned obesity assets, ARO-INHBE (liver) and ARO-ALK7 (adipose), are expected by the end of 2025. Additional assets across complement-mediated (CM) diseases, lung inflammation, fatty liver disease, and four separate partnerships help to diversify the company's potential, too.

Then again, no one doubts the potential of RNAi as a drug class. Not anymore. The big question investors keep asking: "Can Arrowhead fund all these obligations?" I would counter with, "Has management given investors any reason to doubt its ability to raise capital?"

At a time when most drug developers are stuck at base camp trying to stretch supplies and wait out the biotech winter, Arrowhead has pushed further down the trail – resisting layoffs, pipeline prioritization, and funding cuts. It has a few mountain peaks to scale.

By the Numbers

I couldn't bring myself to write an intro about Sarepta's baby mamma drama, but it cannot be avoided. Importantly, the newest partner's incompetence has no meaningful impact on Arrowhead as a business.

Shares of Arrowhead were dragged lower when Sarepta encountered regulatory trouble for Elevidys. The gene therapy for Duchenne muscular dystrophy (DMD) led to two patient deaths, while a separate gene therapy candidate in Limbe-Girdle muscular dystrophy (LGMD) led to an additional patient death. The FDA forced the company to pause shipments of Elevidys in patients who cannot walk and revoked the coveted platform technology designation for the company's AAVrh74 gene therapy vector.

Investors sold the news – for Arrowhead.

The concern was that Sarepta's regulatory troubles would jeopardize its financial position and ability to make future milestone payments to the RNAi pioneer, potentially unraveling the lucrative collaboration finalized in February 2025. But that never made much sense.

The collaboration with Sarepta has upfront, near-term, and long-term potential for Arrowhead. As explained in the December 2024 research note analyzing the collaboration, there wasn't much that could threaten the near-term value of the deal. Sarepta tried its best though.

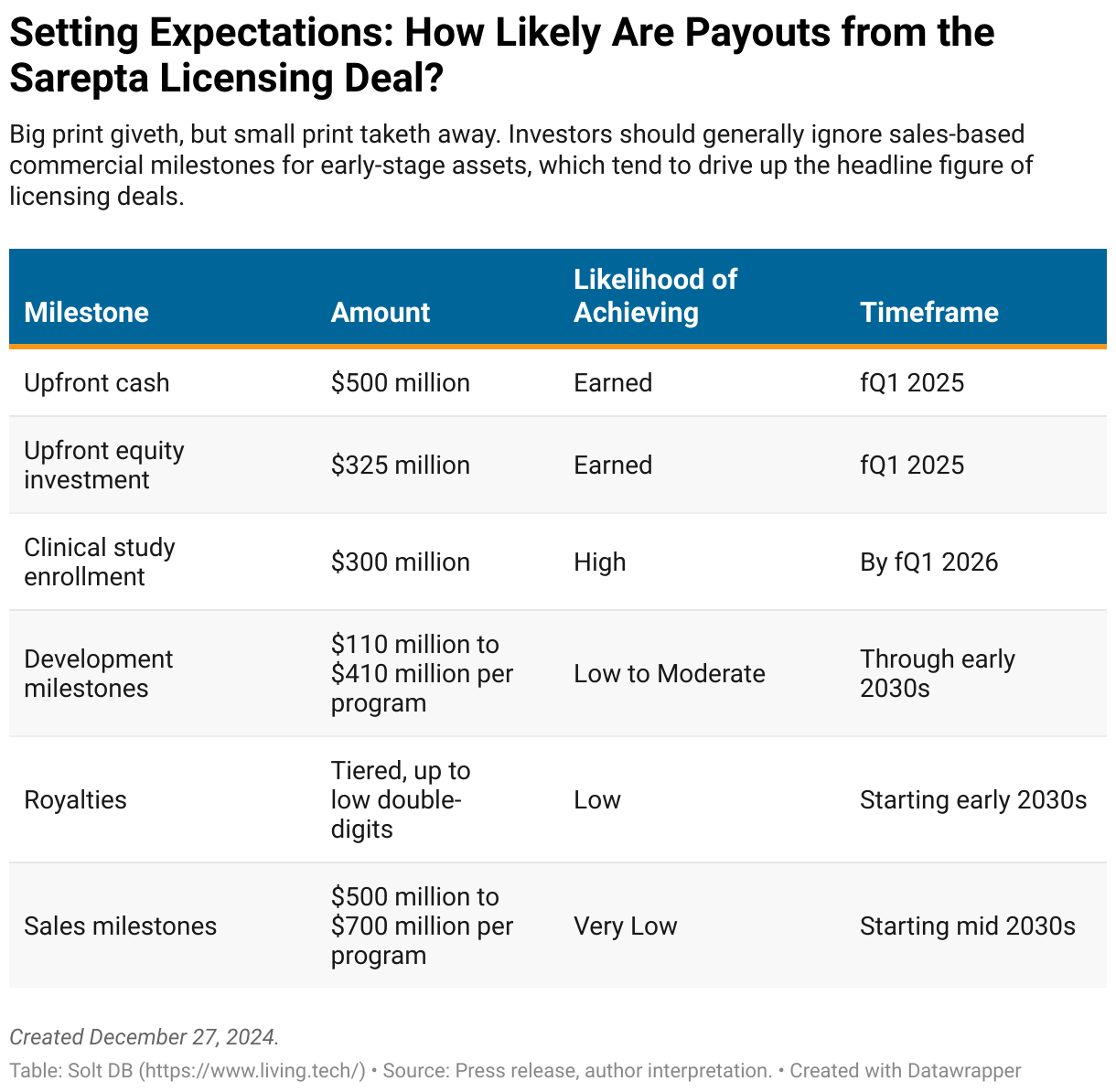

Arrowhead earned $500 million upfront as cash, $325 million upfront as an equity investment at $27.25 per share, and has since earned a $100 million clinical trial enrollment milestone. It expects to satisfy an additional enrollment milestone by the end of this year, which would earn an additional $200 million cash milestone in early 2026.

That's $1.125 billion in cash in the first 12 months of the collaboration – an enormous haul.

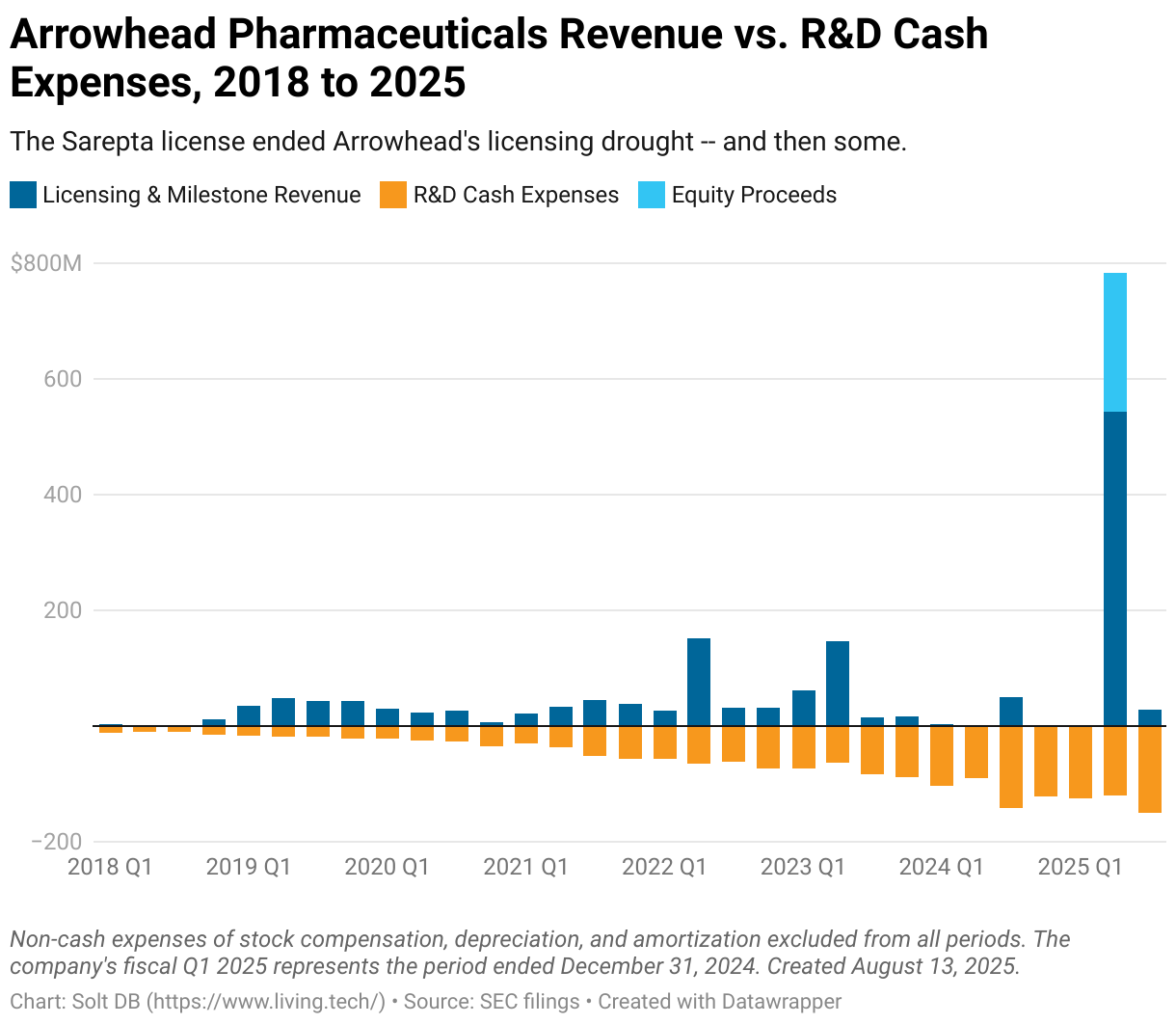

If you have a memory slightly longer than a goldfish, then you'll remember analysts and investors pelted management with questions about the company's financial health prior to the Sarepta deal. Arrowhead was spending increasingly more on R&D while simultaneously bringing in less licensing revenue. It was definitely in a drought, but that emphatically ended by monetizing assets with the gene therapy developer.

The upfront payments from Sarepta ($812 million net) almost offset all R&D cash expenses incurred since October 1, 2023 ($849 million). Zoom out even further and the RNAi pioneer has nearly offset all R&D cash expenses ($1.81 billion) with licensing and milestone revenue ($1.76 billion) since October 1, 2017.

That's epic, first-ballot Hall of Fame strategic execution.

As for the mid-term and long-term development milestones, the likelihood of achievement isn't any different than any other licensing deal.

Arrowhead can earn development milestones of $110 million to $410 million per program over the next decade. Meanwhile, sales milestones tend to drive up the headline figure of any drug development collaboration – thrusting this one over $10 billion – but are heavily back weighted and rarely achieved. These cannot be earned until the mid-2030s at the earliest.

If Sarepta fails to pay a milestone for any specific program, then the rights to the asset return to Arrowhead. If Sarepta fails to pay the $50 million per year R&D retainer in any of the next five years, then Arrowhead has the right to terminate the entire collaboration. All assets would return to Arrowhead, be more mature than before, and could be licensed out for a second time. Double bubble, baby.

However, Sarepta wasted no time pivoting its entire pipeline to focus on the RNAi drug candidates licensed from Arrowhead – not a minor detail for a company that previously had dozens of pipeline programs spread across gene therapy, gene editing, and oligos. In other words, Sarepta needs Arrowhead more than Arrowhead needs Sarepta.

In August 2025, Sarepta sold its equity stake in Arrowhead. It made the cardinal sin of investing: buying high, selling low. But the transaction works out well for the RNAi innovator.

- In February 2025, Sarepta purchased 11.92 million shares of newly-created Arrowhead common stock for $27.25 per share. The total transaction value was approximately $325 million.

- In August 2025, Sarepta sold 9.265 million shares of Arrowhead common stock to raise gross proceeds of at least $174 million.

- In August 2025, Sarepta gave the remaining 2.661 million shares of Arrowhead common stock back to Arrowhead. The total transaction value was $50 million and satisfied half of the $100 million enrollment milestone.

- Arrowhead retired the 2.661 million shares, effectively amounting to a share repurchase program.

Sarepta lost about $100 million on the equity sales in just six months, but boosted its cash position by at least $174 million. That capital will be handed back to Arrowhead through the collaboration, including the near-term $200 million enrollment milestone and annual $50 million R&D allowances.

The RNAi pioneer won't be derailed because of the drama surrounding Sarepta. It will still need to deftly manage its cash position in the next 36 months.

Arrowhead exited June 2025 with $900 million in cash, which it expects will fund operations into 2028. The business has a quarterly operating cash outflow of roughly $150 million, although that will be partially offset with additional earnouts from Sarepta. The company earned an additional $50 million cash milestone in August 2025, is on pace to earn $200 million more in early 2026, and is still obligated to receive $50 million for this year's R&D allowance.

If plozasiran earns approval in FCS and launches in late 2025, then it will actually increase expenses in 2026. Revenue in a low-impact setting like FCS won't make meaningful contributions or even offset its commercial costs in the first year or two on the market. So that asset won't provide any financial help in the near term.

Luckily, the cash runway extends beyond data readouts from partnered assets (olpasiran and fazirsiran) in 2027. And investors might expect additional assets to be outlicensed to further boost the cash balance soon.

Around the Horn

A roundup of recent and upcoming developments for key assets.

Olpasiran, partnered with Amgen

Amgen is evaluating olpasiran in atherosclerotic cardiovascular disease (ASCVD) with topline data expected in early 2027. That's the same indication that will make Novartis' Leqvio the first RNAi drug to exceed $1 billion in annual revenue.

Arrowhead sold its royalty rights to olpasiran, but can earn an additional $485 million in regulatory and commercial milestones from Amgen.

As a reminder, the majority of these milestones are based on achieving certain annual and cumulative sales milestones, which will take many years to achieve. But the blockbuster potential of olpasiran means they have an above-average potential of being paid out – years from now.

Fazirsiran, partnered with Takeda

The Amgen license's near-term economics have been squeezed dry, but the partnership with Takeda offers potential for additional monetization. Fazirsiran is being developed as a treatment for alpha-1 antitrypsin (A1AT) deficiency liver disease.

The collaborators will split U.S. profits 50/50, while the RNAi pioneer can earn 20% to 25% royalties on international revenue and $527.5 million in regulatory and commercial milestones.

I've excluded fazirsiran from my model. Whereas fazirsiran silences the genetic mutation that causes A1AT deficiency, an ideal treatment for this specific indication would fix the mutation. That's especially important considering A1AT deficiency leads to lung disease, too, which isn't addressed by fazirsiran.

Emerging drug candidates across RNA editing (Wave Life Sciences) and DNA editing (Beam Therapeutics) have the potential to be an ideal treatment for A1AT deficiency, addressing both the liver and lung diseases. Although human data are early and immature, these therapeutic modalities should translate really well in larger and longer studies.

These emerging assets have years of development ahead of them. Takeda and Arrowhead could commercialize fazirsiran for a few years until they arrive on the market, which could generate meaningful revenue. But Arrowhead might opt to sell its share of the economics for near-term cash.

As explained in a March 2025 research note, RNAi is best suited for creating beneficial loss-of-function mutations to treat diseases. That's not the therapeutic rationale behind fazirsiran, which is why it was outlicensed in the first place.

ARO-RAGE for inflammatory lung diseases

Arrowhead had three separate assets in its lung pipeline 12 months ago. Since then, one was partnered (ARO-MMP7 to Sarepta), one was terminated (ARO-MUC5AC), and one was kept (ARO-RAGE).

An important part of the ongoing phase 1/2 study for ARO-RAGE was completed earlier this year. The RNAi candidate silences the RAGE inflammation pathway, which could treat lung diseases like asthma.

However, the company has been oddly silent about the asset. It hasn't announced data from the study, nor has it acknowledged ARO-RAGE's existence in recent communications.

The radio silence could be a sign Arrowhead will terminate the asset to preserve cash or seek a partner to continue development. A potential upfront milestone payment for a license could be in the ballpark of $50 million to $100 million – or maybe more depending on data – if the asset isn't shelved.

Plozasiran in FCS

The FDA has set an approval decision date of November 18, 2025, for plozasiran in FCS. It's expected to earn approval and launch the same day.

Ionis Pharmaceuticals earned FDA approval for its FCS treatment Tryngolza (olezarsen) in late 2024. Cross-study comparisons between the antisense oligo (ASO) and plozasiran suggest the two molecules lead to a roughly equivalent reduction in triglycerides after 10 months. Plozasiran has a clear convenience advantage though: dosed once every 12 weeks vs. once every 4 weeks for Tryngolza.

The market opportunity in FCS is not enough to be meaningful for Arrowhead, especially given its spending habits. Plozasiran will generate more expenses than revenue in 2026 and 2027.

Plozasiran in SHTG

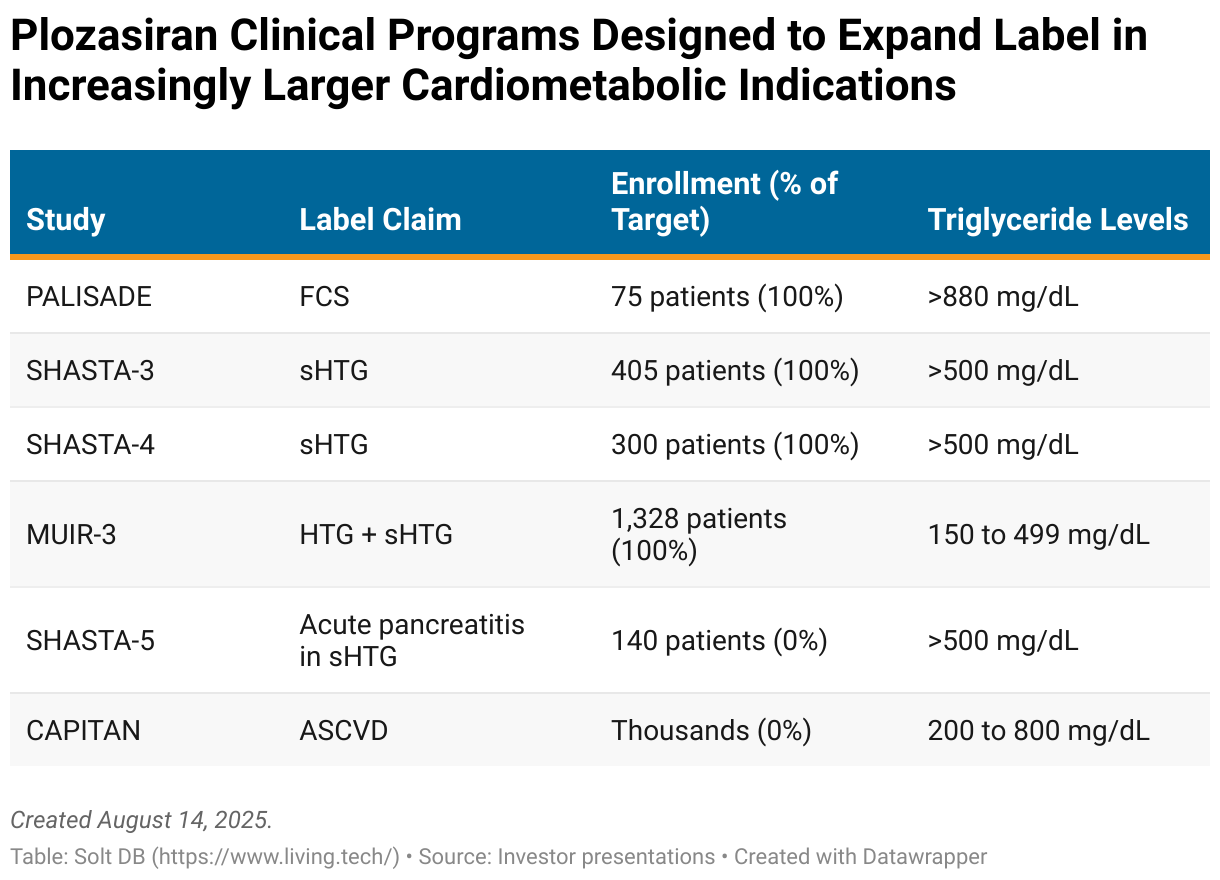

Arrowhead recently completed enrollment in three pivotal studies aimed at expanding plozasiran's commercial opportunity.

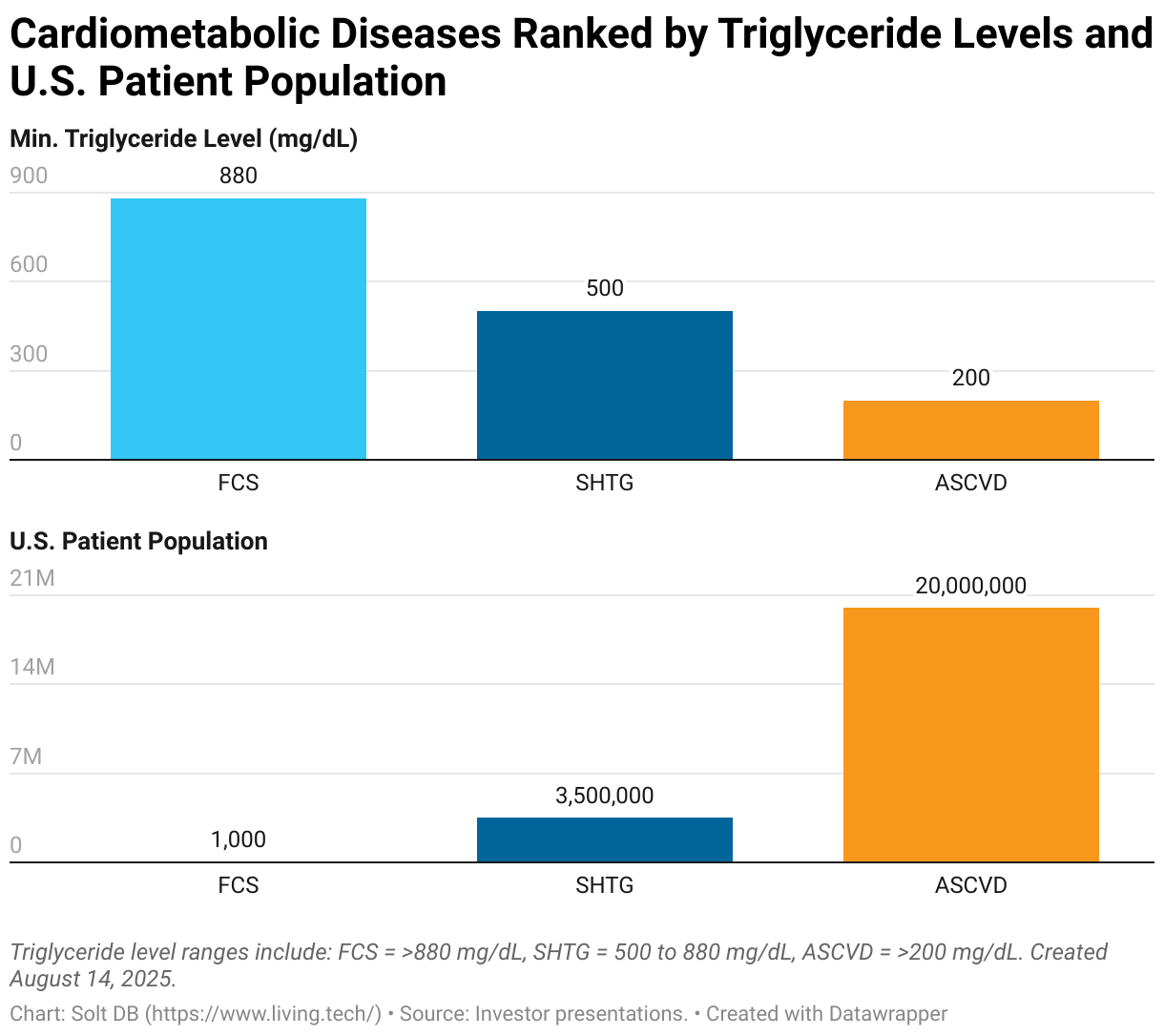

Whereas FCS affects less than 1,000 patients in the United States, HTG and SHTG impact over 3.5 million Americans. Believe it or not there's an even larger opportunity on the horizon in using plozasiran to reduce the risk of heart disease. ASCVD is estimated to impact roughly 20 million Americans.

All four indications differ by the level of triglycerides in the blood. In addition, FCS is caused by a rare genetic mutation. The others are caused by natural aging (in males) and lifestyle (diet and exercise).

Arrowhead has focused its development programs on SHTG in the near term. That includes the MUIR-3 study even though all enrolled patients technically have less-than-severe hypertriglycerdemia (HTG).

However, the MUIR-3 study – the largest so far – is important for generating data in a patient population that will mirror that of ASCVD. The company has readied but not yet started the pivotal CAPITAN study, which will be needed to earn approval in ASCVD. It will need to enroll thousands of patients.

Zodasiran in HoFH

Both zodasiran and plozasiran were developed side-by-side with only one advancing into broader pivotal studies. Plozasiran won. That prompted Arrowhead to pause development of zodasiran and explore partnering opportunities.

It changed that stance recently. Patient enrollment has begun for the pivotal YOSEMITE study evaluating zodasiran in HoFH. Similar to FCS, the cardiometabolic disease is caused by a rare genetic mutation, impacts about 1,000 patients in the United States, and won't be a commercially-meaningful opportunity.

But the YOSEMITE program has meaningful strategic value.

The pivotal study will enroll just 60 patients and should be completed by fall 2027. In other words, it won't be expensive. It does create a path to regulatory approval for zodasiran, which makes it easier to earn additional approvals in larger and more commercially-meaningful indications. That increases the value if Arrowhead decides to outlicense rights to the asset – and the additional R&D spend is relatively minimal. It's a great strategic investment.

News Flow & Modeling Insights

(Refined.)

There aren't any noteworthy changes to the model, although I expect upcoming events will trigger larger changes that will require dedicated research notes.

Arrowhead Pharmaceuticals still has an estimated fair valuation of $3.871 billion. However, a lower share count following the retirement of 2.66 million shares increases the modeled fair value from $27.75 per share to $28.27 per share.

Margin of Safety & Conviction

Arrowhead Pharmaceuticals is considered a Future Compounder position with the following Conviction rating.

- 1 = High

- 2 = Above Average

- 3 = Average

- 4 = Below Average

The estimated fair valuation based on my current model is below:

- Market close August 13: $19.99 per share

- Modeled Fair Valuation: $28.27 per share

- Allocation Range: Up to 15%

Arrowhead Pharmaceuticals reported 138.257 million shares outstanding as of August 1, 2025. The modeled fair valuation above assumes 136.953 million shares outstanding, which accounts for the retirement of 2.661 million shares and 1% dilution.

Further Reading

- August 2025 press release announcing fiscal Q3 2025 operating results

- August 2025 regulatory filing (10-Q) detailing fiscal Q3 2025 operating results

- March 2025 research note analyzing the competitive landscape for fazirsiran in A1AT deficiency liver and lung diseases

- December 2024 research note analyzing the collaboration with Sarepta Therapeutic

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)