.svg)

Relay Therapeutics got rocked by the biotech winter. Then again, not many precommercial drug developers escaped the historic outflow of capital in recent years. The lucky few that emerged with only bumps and bruises almost all had mature, late-stage pipelines with at least one high-impact asset. Execution is always rewarded, but timing helps, too.

Now the protein motion pioneer gets to take its turn.

Institutional investors have been building positions in Relay Therapeutics in the last 12 months. Commodore Capital didn't own a single share until Q2 2025. By the end of the year, it owned 9.5% of the drug developer, which was its largest holding. Point72 Management owned 7.8% by the end of 2025, while biotech specialist Casdin Capital owned 7.3%.

Together with SoftBank and Blackrock, these five investors owned 47.5% of the company. Funds tend to crowd into – and out of – the same ideas. Let's hope they stick around.

Relay Therapeutics will get several chances to entertain its new audience this year.

On Monday, March 16, the drug developer will present the first in-human data for the 400 mg, fed-dose regimen of zovegalisib at the ESMO Targeted Anticancer Therapies Congress. The data readout will include 57 patients who took treatment with food, which is expected to improve tolerability without sacrificing efficacy. The cohort is larger than expected – data readouts to date included 64 total patients at the previous 600 mg fasted dose – and will be interpretable for efficacy.

In the first half of 2026, Relay Therapeutics expects to provide the first glimpse of zovegalisib in vascular anomalies. An interim readout from the phase 1 ReInspire study will include data from about 20 patients total. The study experienced higher-than-expected demand, allowing it to hit enrollment targets for the adult cohorts and open pediatric cohorts ahead of schedule.

Finally, the protein motion pioneer will share the first triplet combination data in HR+/HER2- breast cancer before the end of 2026. In a twist, these data will be from triplets in CDKi-experienced patients. Management will decide the preferred combination – atirmociclib, Kisqali, or Ibrance – based on these data.

That trio of de-risking events and cash burn math suggest Relay Therapeutics is likely to raise capital this year. Will it choose an old-fashioned stock offering? Or might it license rights to an asset? That could be zovegalisib in non-breast tumors, the NRAS inhibitor, the Fabry disease candidate, or other discovery programs now underway.

By the Numbers

Management's batten-down-the-hatches strategy is clearly reflected in cash flow statements. The business reported its lowest cash burn since Q4 2020. Although Relay Therapeutics did record $7 million in licensing revenue from Elevar Therapeutics, the primary driver of improving cash burn is reduced R&D spending and employee headcount.

R&D expenses fell to $55.4 million in Q4 2025, down from $73.8 million in the first quarter of the year. Yet, the company is spending more on clinical trials and less on employees and early-stage research ("platform") after letting the decade-long pact with D.E. Shaw Research lapse last summer.

The biotech winter forced many companies to rethink their spending habits, priorities, and cash runways. Relay Therapeutics decided that meant protecting its ability to self-fund pivotal studies for zovegalisib above all else. Multiple layoffs have reduced the company's headcount from a peak of 327 at the end of 2022 to 192 at the end of 2025.

However, the relative R&D spend has remained remarkably constant since 2021. Relay Therapeutics is spending identical amounts on other expenses (9%) and equivalent amounts on employees (40% in 2021 vs. 37% in 2025). The only change is that spending on platform technologies (40% in 2021 vs. 15% in 2025) has switched places with clinical trials (11% in 2021 vs. 40% in 2025).

The data from last year reflect full-year totals, which means the relative spending categories will likely shift even further toward clinical trials in 2026. For example, the relative share in Q4 2025 was 47% for clinical trials, 36% for employees, 8% for platform technologies, and 8% for other.

The business began 2026 with $555 million in cash, which continues to support a runway into 2029. But investors should expect a capital raise, especially in such a data-rich year.

Relay Therapeutics overhauled its pitch in the latest investor slide deck. On the second slide, a simple graphic shows the company's total addressable market (TAM) estimate for zovegalisib is at least $15 billion. That comprises the CDKi-experienced population in breast cancer ($2 to $3 billion), the CDKi-naïve population in breast cancer ($7 to $8 billion), and vascular anomalies ($6 to $8 billion).

All numbers reflect the revenue opportunity in the United States and exclude the value of international market opportunities.

The company could remove uncertainty for all three of those high-impact opportunities within a nine-month stretch. It will at the very least have the option to issue a public offering at a favorable price. Doing so could allow it to thrust RLY-8161 (NRAS inhibitor) into phase 1 study and accelerate pivotal programs for zovegalisib.

Commercial Landscape

PI3K pathway inhibitors

The market opportunity for PI3K pathway inhibitors is very large, but cannot be accessed due to poor tolerability of existing treatment options. The best-tolerated treatment, Truqap from AstraZeneca, has the opportunity to become a blockbuster in 2026. That's impressive considering all revenue is generated from the CDKi-experienced population, the opportunity is estimated at up to "only" $3 billion, and this will be just the third full year on the market.

The only approved competitor in the CDKi-experienced population is Piqray from Novartis. Although it was the first PI3K pathway inhibitor approved, it's also the worst-tolerated treatment. The asset's revenue peaked at $505 million in 2023, but slid all the way to $382 million last year. That still seems high.

And although Itovebi from Roche is the only PI3K pathway inhibitor approved in the CDKi-naïve population, doctors appear hesitant to use it. The reason: tolerability. While Itovebi has fewer side effects than Piqray, the bar is also significantly higher in the first-line setting than later treatment lines.

Investors should be cheering for Truqap's commercial success. If zovegalisib outperforms the competitor in its head-to-head pivotal study, then it has the potential to steal significant market share unusually quickly. Relay Therapeutics could grab significant market share even if it only obtains an approval specifically for kinase mutations, which are present in half of all patient tumors. Only zovegalisib would have a specific mutation on its label.

CDK inhibitors

Drug developers are trying to disrupt the CDK inhibitor market by making more selective CDK inhibitors. In other words, they'll remain important components of HR+/HER2- breast cancer combinations for the life of zovegalisib. Best to keep up with landscape dynamics.

Ibrance from Pfizer continued to cough up market share in 2025. Of course, a bad year for the drug is still $4.1 billion in annual revenue. That fell behind Kisqali from Novartis for the first time, which hauled in $4.8 billion last year. It added the most revenue in the drug class following supplemental approvals and international expansion.

Verzenio from Eli Lilly kept the crown with $5.7 billion. It's an important piece of the company's overall breast cancer strategy, which includes the best potential competitor to zovegalisib (tersolisib) and an oral selective estrogen receptor degrader (imlunestrant) to potentially replace intramuscularly-injected fulvestrant.

Fabry disease (peak sales potential >$2 billion)

It looks like the NRAS program RLY-8161 will beat the Fabry disease program to the clinic. That makes sense considering the latter requires whole new teams to manage clinical trials and eventually (hopefully) sell. It still represents a great commercial opportunity made uniquely accessible by the Dynamo platform.

The GLA gene encodes an important enzyme called alpha-Gal (alpha-galactosidase A) that breaks down a naturally-occurring fatty substance called Gb3 (globotriaosylceramide). Fabry disease is caused by mutations in the GLA gene, which leads to deficient alpha-Gal and the accumulation of Gb3.

One giant challenge: there are over 1,000 known GLA mutations. How do you effectively treat Fabry disease then?

There are two primary treatment options: enzyme replacement therapy (ERT) and alpha-Gal chaperones. The nerds in lab coats often make things too complicated, but they nailed these names.

As the name implies, ERT replaces the defective alpha-Gal enzyme by giving patients working copies of alpha-Gal. ERT is administered through intravenous infusions every two weeks. While inconvenient for a chronic condition, there aren't many treatment options available. Fabrazyme from Sanofi, Replagal from Takeda (not approved in the United States), and Elfabrio from Chiesi Pharmaceuticals combined for full-year 2025 revenue of $1.7 billion.

And as the other name implies, chaperones bind to mutated alpha-Gal enzymes, bend them into a working structure, and allow them to break down Gb3. Galafold from Amicus Therapeutics is an inhibitory chaperone though, which means it only results in a small increase in alpha-Gal activity and only works in less than 50% of all mutations.

Relay Therapeutics used Dynamo to find an allosteric pocket on the alpha-Gal enzyme that is conserved across mutations. That resulted in the first non-inhibitory chaperone, which could be used as a monotherapy or in combination with ERT. The timing of clinical entry is uncertain, and it might make sense to partner with an ERT provider like Sanofi, but an asset with the promised clinical profile could have peak annual global sales of $2 billion or more.

News Flow & Modeling Insights

(No change.)

The current model makes the following assumptions:

- The pivotal ReDiscover-2 study has a topline data readout in Q3 2028.

- Zovegalisib is submitted with a standard 10-month regulatory review. (It takes a few months from data readout to regulatory submission.)

- Zovegalisib launches in Q4 2029 with an approval in at least kinase mutations. A companion diagnostic required for this label claim is developed without delays.

- Zovegalisib generates full-year 2029 revenue of at least $45 million and full-year 2030 revenue of at least $600 million.

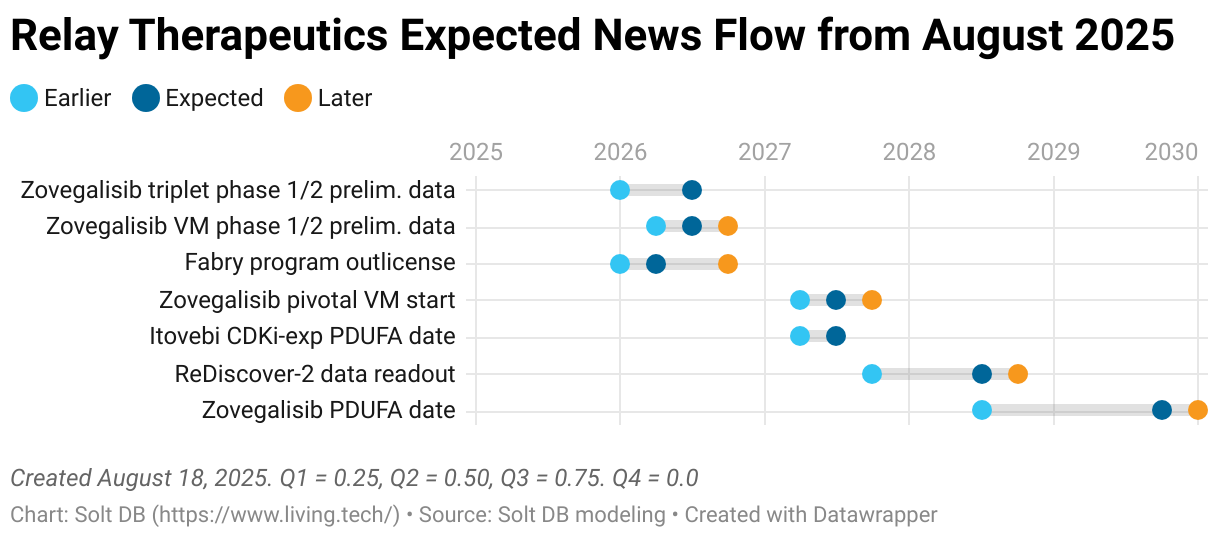

The expected news flow for Relay Therapeutics:

Margin of Safety & Conviction

Relay Therapeutics is considered a Future Compounder position with the following Conviction rating.

- 1 = High

- 2 = Above Average

- 3 = Average

- 4 = Below Average

The estimated fair valuation based on my current model is below:

- Market close March 3: $9.85 per share

- Modeled Fair Valuation: $17.68 per share

- Allocation Range: Up to 15%

Relay Therapeutics reported 178.725 million shares outstanding as of February 20, 2026. The modeled fair valuation above assumes 237.5 million shares outstanding, which is equivalent to full dilution expected through the launch of zovegalisib.

Further Reading

- February 2026 press release announcing Q4 2026 operating results

- February 2026 regulatory filing (10-K) detailing Q4 2026 operating results

- February 2026 quarterly earnings preview for the Solt DB coverage ecosystem

- August 2025 research note introducing the rebuilt model for zovegalisib

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)