.svg)

Modern boards of directors are usually a corporate grift with a collection of logos attached.

They rarely do their job – like, you know, removing ineffective management. Or worse, they remove management out of impatience instead of ineffectiveness, while rewarding decisions that optimize short-term thinking. Look at Verizon, Starbucks, and Chipotle to name a few. Or Amyris, Ginkgo Bioworks, and Recursion Pharmaceuticals in our neck of the woods.

Directors are often hired for the logos on their resume, instead of, you know, their ability to help a business at its current state of maturity. The most important driver of success for a living technology company, whether in biopharma or industrial biotech or research inputs, is its ability to commercialize its technology. Curiously, few directors ever have deep commercial experience or strategy knowledge. Nice logos, though.

Directors show up a handful of times a year, vote in unison with the same stale group think, collect a check and some stock options, and bounce after patting themselves on the back.

Well, that's not entirely true. Directors usually have to catch a flight to their next meaningless board meeting.

I think Relay Therapeutics has the potential to grow into one of the largest drug developers on the planet. You can't say that about very many companies over the course of a lifetime, especially in a sector that primarily optimizes for exits and acquisitions. Strategic moves in recent years suggest the management team isn't optimizing for that. It would be a rare opportunity to own one of those during its precommercial stage.

That said, the board of directors is probably the same as most others. There could still be some value to recent additions, but it's difficult to quantify and impossible to objectively gauge. That's because individual executives and directors add value through their relationships and networks.

For example, it was no fluke that Scorpion Therapeutics sold its pan-mutant PI3K-alpha inhibitor to Eli Lilly. The CEO was the founder of Loxo Oncology, which was acquired by Eli Lilly for $8 billion in 2019 – a significant valuation for pre-pandemic takeovers. Loxo Oncology is now the basis for the large pharma's fast-rising oncology division. Relationships matter.

Relay Therapeutics added two experienced directors to its board: Habib Dable and Lonnel Coats. Both were on the board of Blueprint Medicines prior to its $9.5 billion acquisition by Sanofi – a company aggressively building its oncology pipeline. Through the acquisition, Sanofi now owns one of the most advanced CDK2 inhibitors in the global pipeline, which is a high-value target that Relay Therapeutics shelved due to funding and timing dynamics. Noted.

Mr. Dable was also the CEO of Acceleron Pharmaceuticals when it was acquired for $11.5 billion by Merck in 2021, and currently sits on the board of Day One Bio. Mr. Coats was the former CEO of Lexicon Pharmaceuticals and Eisai, while he was also on the board of directors of Verve Therapeutics prior to its $1.3 billion acquisition by Eli Lilly. I guess the coverage ecosystem is increasingly incestuous.

At any rate, the only thing investors can do with news of the board additions is nod and get on with their lives. It could matter. We probably won't be able to tell anyway.

More importantly, Relay Therapeutics is preparing a data update for its zovegalisib doublet in CDK inhibitor-experienced patients with HR+/HER2- breast cancer. The data will be formally presented at the San Antonio Breast Cancer Symposium (SABCS) from December 9 to 12, although it's likely to issue a press release when the data-containing abstract text is made available by the conference on Monday, November 24. The update might not be too meaningful, but investors can expect slight improvements in response rates across all cohorts.

By the Numbers

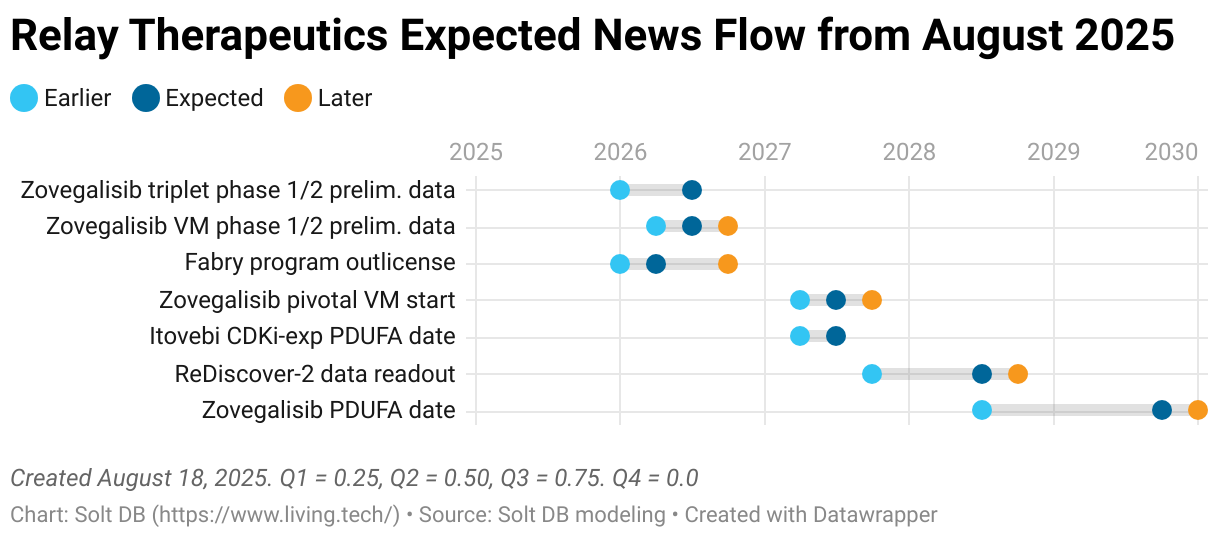

Relay Therapeutics will have meaningful de-risking events in the next few years and at a more regular cadence than in the past.

There will be go/no-go decisions for zovegalisib triplets, updates for zovegalisib in vascular malformations, and the potential to expand zovegalisib beyond breast tumors (ideally through licenses). There will be clinical starts and/or licensing deals for the NRAS program (RLY-8161) and Fabry disease asset. There's a single, mysterious preclinical asset in development (most likely a backup PI3K-alpha inhibitor for vascular malformations).

Unfortunately, the timing of these events is unknown. The known de-risking events are either financially insignificant (lirafugratinib earning an initial FDA approval in early 2027) or sufficiently far away (ReDiscover-2 won't read out until 2H 2028… well, maybe mid-2027…).

Investors can keep an eye on two metrics in the meantime:

- Cash runway management

- R&D expenses

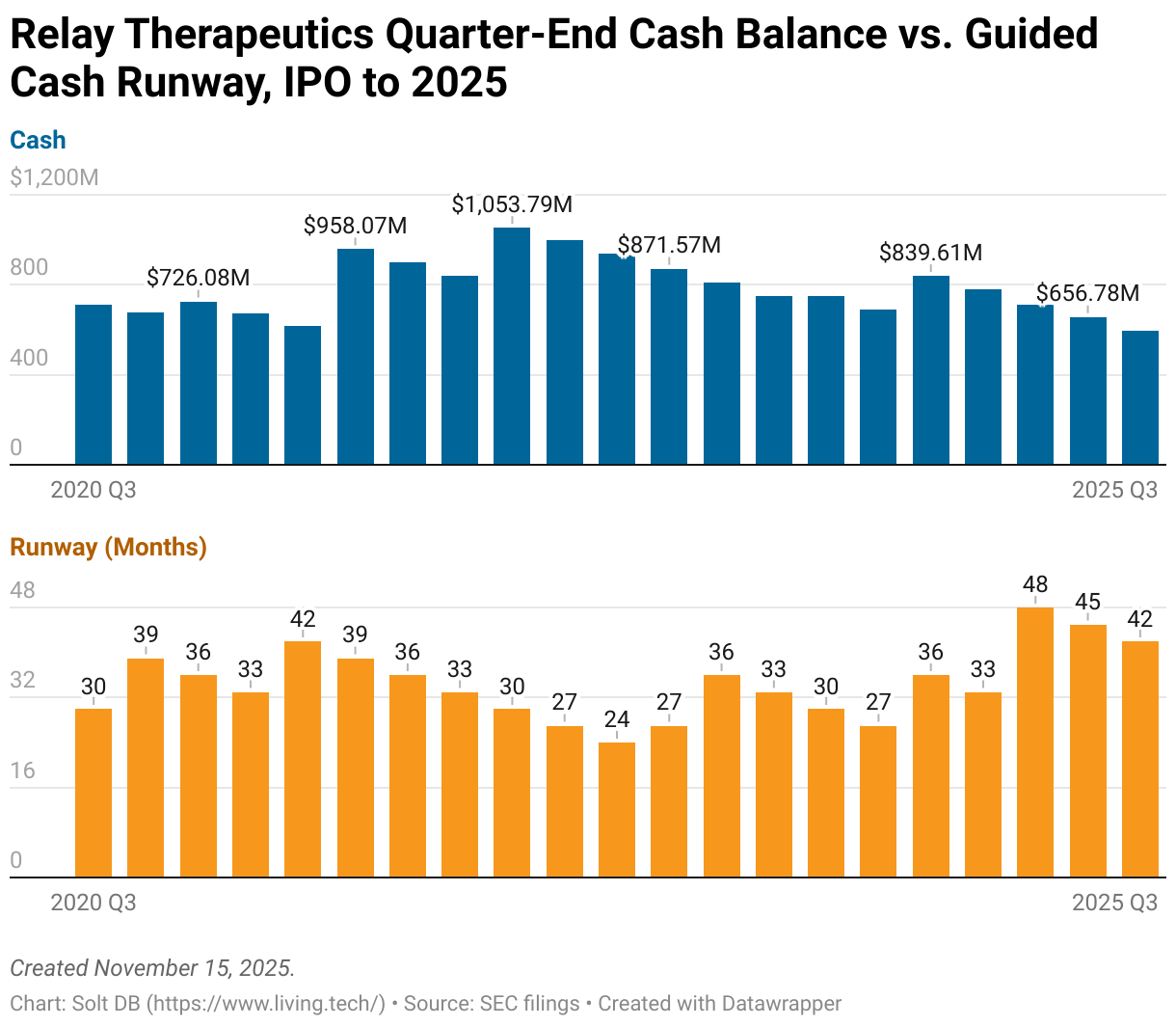

Relay Therapeutics reduced its team, pipeline, and short-term ambitions to protect its prized asset zovegalisib. The business can fund itself into 2029, which extends past the expected topline data readout for ReDiscover-2 in the second half of 2028.

Investors can expect additional cash injections prior to the runway being exhausted, including potential milestone payments from Elevar Therapeutics for lirafugratinib and potential licensing deals for other assets, indications, and/or geographies. As is typical, it's also likely to secure debt financing within 12 months of the topline data readout to support launch and commercialization activities. Relay Therapeutics could also sell its royalty and milestone rights to lirafugratinib ($500 million total) for $200 million to $250 million much sooner. That might be a great idea.

One crucial detail: The length of the cash runway is more important than the absolute value of cash on the balance sheet. I can't guarantee the market will properly interpret the nuance of a dwindling cash balance, but we can visualize it to be objective.

The business ended Q3 2025 with $596 million in cash, which is the lowest quarter-end balance since its IPO. However, that supplies a runway of 42 months from the end of the quarter with the current operating plan – one of the longest since its IPO.

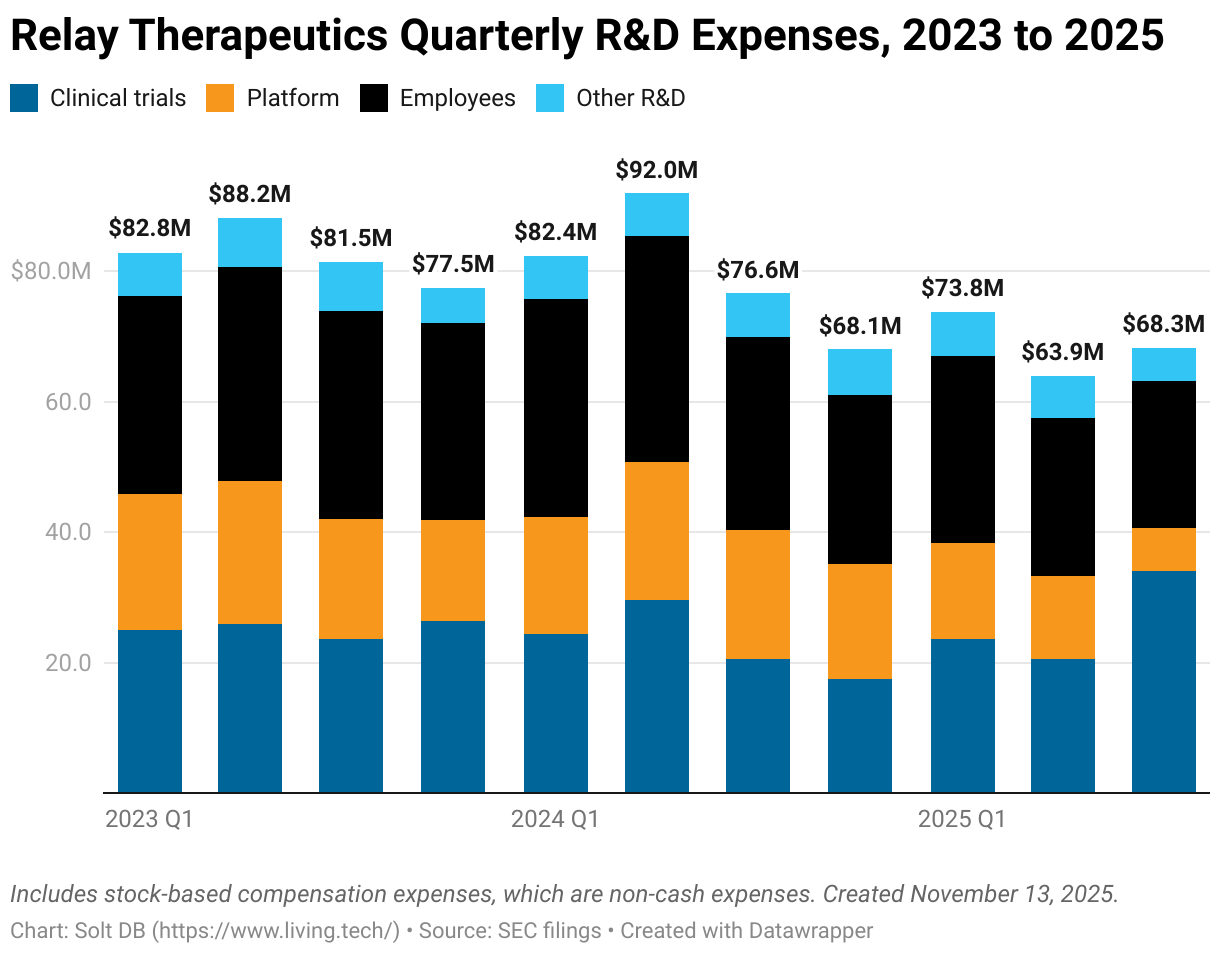

Similar to the company's cash runway, its R&D expenses also reflect prioritization of zovegalisib in breast cancer.

Relay Therapeutics has reduced total R&D spending while increasing the budget allocated to clinical trials, which will include the phase 1/2 ReDiscover study into mid-2027, as well as the phase 1/2 ReInspire study and the phase 3 ReDiscover-2 study into the early 2030s. The phase 1/2 study is still generating data required for a regulatory submission, evaluating zovegalisib triplets, and is cleared for tumors beyond breast (although deprioritized).

The business spent $34 million on clinical trials in Q3 2025 – by far the highest ever. To ease digestion, the drug developer shrank its budget for platform & preclinical activities by shelving pre-IND assets in breast cancer, prioritizing two IND-ready assets beyond breast cancer for diversity, letting the 10-year collaboration with D.E. Shaw Research expire, and toiling away with one final preclinical asset.

Meanwhile, multiple rounds of layoffs have reduced employee expenses with the R&D budget to $22.5 million. That includes $12.9 million in direct cash expenses and $9.5 million in non-cash stock-based compensation expenses.

New Data for CDKi-Experienced Setting at SABCS

Relay Therapeutics will present new data from the phase 1/2 ReDiscover study at SABCS in December, although full text of the abstract will be available on Monday, November 24. Investors can likely count on a press release around then detailing the data.

What can investors expect?

These will be additional data for zovegalisib plus fulvestrant in the CDKi-experienced population of patients with HR+/HER2- breast cancer. The readout is likely to include (still) preliminary data from a larger number of patients, with longer follow up, and primarily focus on the 600 mg twice-daily fasted dose.

The last readout had a data cutoff of March 26, 2025. Given the timing submissions for SABCS, the upcoming update should include data through at least late July or into August – a meaningful extension.

Relay Therapeutics has historically reported increasingly better data with each update. Although further improvements will be increasingly difficult to achieve, the company is likely to squeak out one final step up in objective response rates (ORR) across all major populations.

Be mindful of the context. Improvements are expected within the previously-reported enrollment. If data from additional patients are reported for the first time, then they will have less duration of treatment and may dilute the overall ORR. It'll all balance out in the end, and the company has carefully reported data to date, so this shouldn't be an issue.

- (2L+, all mutations): The last reported ORR in this patient population was 38.7% (12/31). Among the existing enrollment, four patients had ongoing responses that were shy of an objective response. At least one additional patient is likely to have an objective response and plausibly up to three. That would increase the ORR to between 42% (13/31) and 48.4% (15/31). The highest in the competitive landscape is 26%.

- (2L, all mutations): The last reported ORR in this patient population was 42.1% (8/19). Among the existing enrollment, three patients had ongoing responses that were shy of an objective response. At least one additional patient is likely to have an objective response and plausibly up to two (both patients overlap with the population above). That would increase the ORR to between 47.4% (9/19) and 52.6% (10/19).

- (2L+, kinase mutations): The last reported ORR in this patient population was 66.7% (10/15). Among the existing enrollment, two patients had ongoing responses that were shy of an objective response. At least one additional patient is likely to have an objective response and plausibly up to two (both patients overlap with the populations above). That would increase the ORR to between 73.3% (11/15) and 80% (12/15).

Shares could respond to an increasing ORR, but investors haven't exactly taken past data readouts seriously. Shares have risen by double digits on all but one previous data readout across the pipeline, although the gains haven't proven durable.

Management could pull the trigger on a public offering to raise additional capital. I selfishly want the company to retain as much of the economic rights to its assets as possible, which investors and analysts don't always interpret positively in the near term. To do so, it'll need to raise more capital from markets instead of potential partners.

On the one hand, a capital raise might be less likely on a data update. Past capital raises piggybacked on meatier data readouts when investors were seeing data packages for the first time.

On the other hand, vaulting the zovegalisib doublet past an ORR of 40% in the overall patient population (of the study) would be an important milestone for the competitive landscape.

Meanwhile, the previously-reported ORR of 66.7% in kinase mutations is incredible, but doesn't 75% or 80% sound a helluva lot better? That would put zovegalisib on a trajectory to deliver landmark data, meaning paradigm shifting results. I'm not sure the market will make the connection yet, but the pivotal study's hierarchal primary endpoints run first through median progression-free survival (mPFS) in kinase mutants – and are key to the potential for "stopping early" sometime after mid-2027.

News Flow & Modeling Insights

(No change.)

Many investors go clinically insane owning biotech stocks. The timelines are extended, de-risking events can be sparse, dilution is a necessary evil, and volatility can be triggered by a slight breeze. This combined with a noisy internet contributes to a poor perception of biotech investing. Properly sizing positions, building them over time, and ruthlessly focusing on the margin of safety are crucial – all things I can do better communicating and setting expectations for as Solt DB finds its groove.

For example, had lirafugratinib earned a broad tumor-agnostic approval in FGFR2 mutated cancers, then we would be sitting here right now evaluating the asset's commercial revenue ramp. While not a high-impact asset, Relay Therapeutics could've generated full-year 2025 revenue in excess of $100 million from lirafugratinib – more than seven other companies in the current coverage ecosystem.

But the FDA hates the finch.

Kidding, but that did alter the trajectory and delay meaningful share price appreciation by a few years. The silver lining is investors now have more time to build a position and at more favorable prices. So, it's important to understand the context behind the share price (including biotech's lingering recession) and strategically adjust, rather than being upset it's not a meme stock. I think the wait will be worth it.

The current model hasn't changed since I rebuilt it to focus on the zovegalisib doublet in CDKi-experienced HR+/HER2- breast cancer in August 2025. I'll add additional indications, geographies, and assets to the model when it makes sense to do so.

The current model makes the following assumptions:

- The pivotal ReDiscover-2 study has a topline data readout in Q3 2028.

- Zovegalisib is submitted with a standard 10-month regulatory review. (It takes a few months from data readout to regulatory submission.)

- Zovegalisib launches in Q4 2029 with an approval in at least kinase mutations. A companion diagnostic required for this label claim is developed without delays.

- Zovegalisib generates full-year 2029 revenue of at least $45 million and full-year 2030 revenue of at least $600 million.

The expected news flow for Relay Therapeutics is as follows.

Margin of Safety & Conviction

Relay Therapeutics is considered a Future Compounder position with the following Conviction rating.

- 1 = High (no change)

- 2 = Above Average

- 3 = Average

- 4 = Below Average

The estimated fair valuation based on my current model is below:

- Market close November 14: $6.29 per share

- Modeled Fair Valuation: $17.68 per share

- Allocation Range: Up to 15%

Relay Therapeutics reported 173.322 million shares outstanding as of October 31, 2025. The modeled fair valuation above assumes 237.500 million shares, which is equivalent to 3% dilution per year plus a 20% dilutive public stock offering.

Further Reading

- November 2025 press release announcing Q3 2025 operating results

- November 2025 regulatory filing (10-Q) detailing Q3 2025 operating results

- October 2025 quarterly earnings preview for the Solt DB coverage ecosystem

- August 2025 research note introducing the new, rebuilt model and a deep dive into the CDKi-experienced competitive landscape

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)