.svg)

If you find yourself wanting to riot against the authorities lately, then you might be interested in Relay Therapeutics. It questions long-held beliefs in drug development and runs toward danger.

Competition is omnipresent in drug development. The largest market opportunities attract the most competition. Even when a company stumbles into a rare wide-open market opportunity, challengers are never far behind. Best to throw elbows, kick some ass, and take souls as standard operating procedure.

Easier said than done.

Relay Therapeutics adopted a strategic approach that tackles competitive landscapes head on. Instead of playing it safe and trying to find a less competitive niche, the protein motion pioneer ran towards commercially-validated markets with suboptimal treatment options – and plenty of competition. If it could use protein motion to make novel discoveries about disease-driving proteins, and design more selective drug candidates against those targets, then it could quickly steal market share and build a portfolio of blockbusters.

To ramp up the difficulty settings, Relay Therapeutics focused on by far the most competitive therapeutic area (oncology) with the lowest probability of success (only 1-in-20 assets to begin clinical trials earn approval), wields a platform technology (the approach most likely to fail), has largely shunned large pharma partnerships for early-stage assets (the primary way to raise cash for platform companies), and has concentrated R&D investments into just a handful of assets (reducing shots on goal).

Yeah, good luck with that.

Yet, the company has so far aced the tests that most commonly set back precommercial drug developers. Concentrated R&D investments have de-risked the technology platform, while unusually robust clinical studies have generated unrivaled data insights into experimental molecules. A lack of partnerships hasn't forced it to relinquish control over its most valuable asset (as of this writing…), which is unheard of.

And running toward danger wasn't an analogy. The first phase 3 program for zovegalisib (formerly RLY-2608) is aggressively going head-to-head not against placebo or the struggling Piqray, but against the current market-leading therapy Truqap.

Yet, the company's magic seems endless in commercial positioning, too. After recent cascading stumbles within the competitive landscape for the five most-advanced competitors and challengers, the data landscape now strongly favors zovegalisib in CDK inhibitor (CDKi) experienced patients with HR+/HER2- breast cancer.

That could be a $2 billion market by 2029, when the asset potentially launches. The leading treatment Truqap could have over $1 billion of that – which would almost immediately be forfeited to zovega.

The unusual degree of data certainty for zovegalisib ahead of its first phase 3 dataset, combined with the aggressive study design going against the market leader, creates a unique investment opportunity in the next few years.

What's the PI3K Opportunity in HR+/HER2- Breast Cancer?

Relay Therapeutics is developing zovegalisib for advanced cases of hormone receptor positive, HER2 negative (HR+/HER2-) breast cancers with a PI3K-alpha mutation.

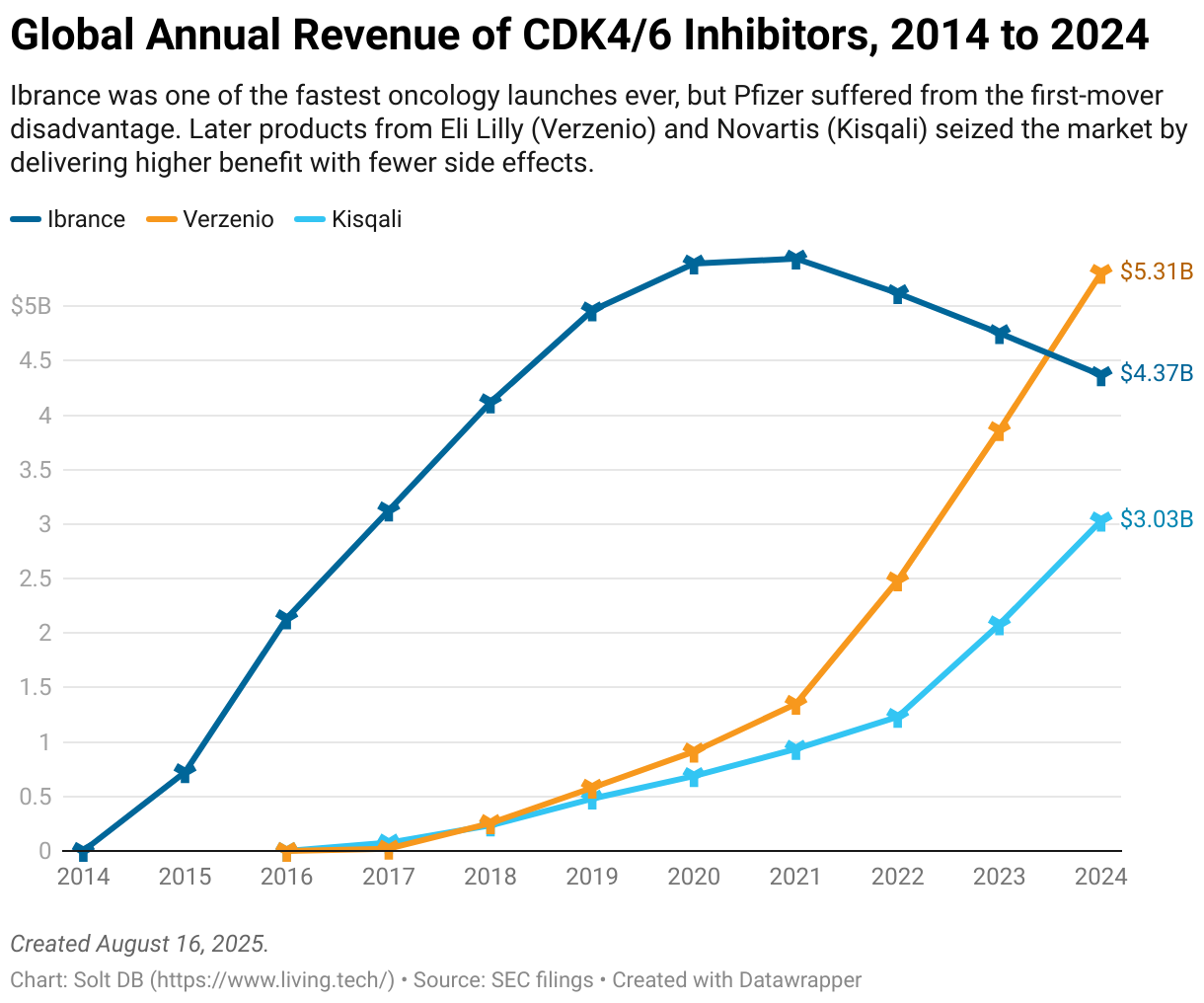

The availability of CDK4/6 inhibitors has significantly improved patient outcomes. Similar to the aspirations for PI3K-alpha inhibitors, CDK inhibitors became some of the bestselling drugs in the world virtually overnight thanks to their potential as a backbone treatment in HR+/HER2- breast cancer.

Pfizer's Ibrance paved the way with one of the fastest-ever drug launches, proving the vast commercial opportunity was desperate for solutions. It eventually suffered the first-mover disadvantage though. Emerging CDK4/6 inhibitors were slightly more selective, which resulted in improved benefits as well as fewer side effects.

Even in the face of those competitive pressures, Ibrance generated $4.4 billion in revenue in 2024. Eli Lilly's Verzenio leapt ahead with $5.3 billion, while Novartis' Kisqali built on the prior year's momentum to climb over the $3 billion mark.

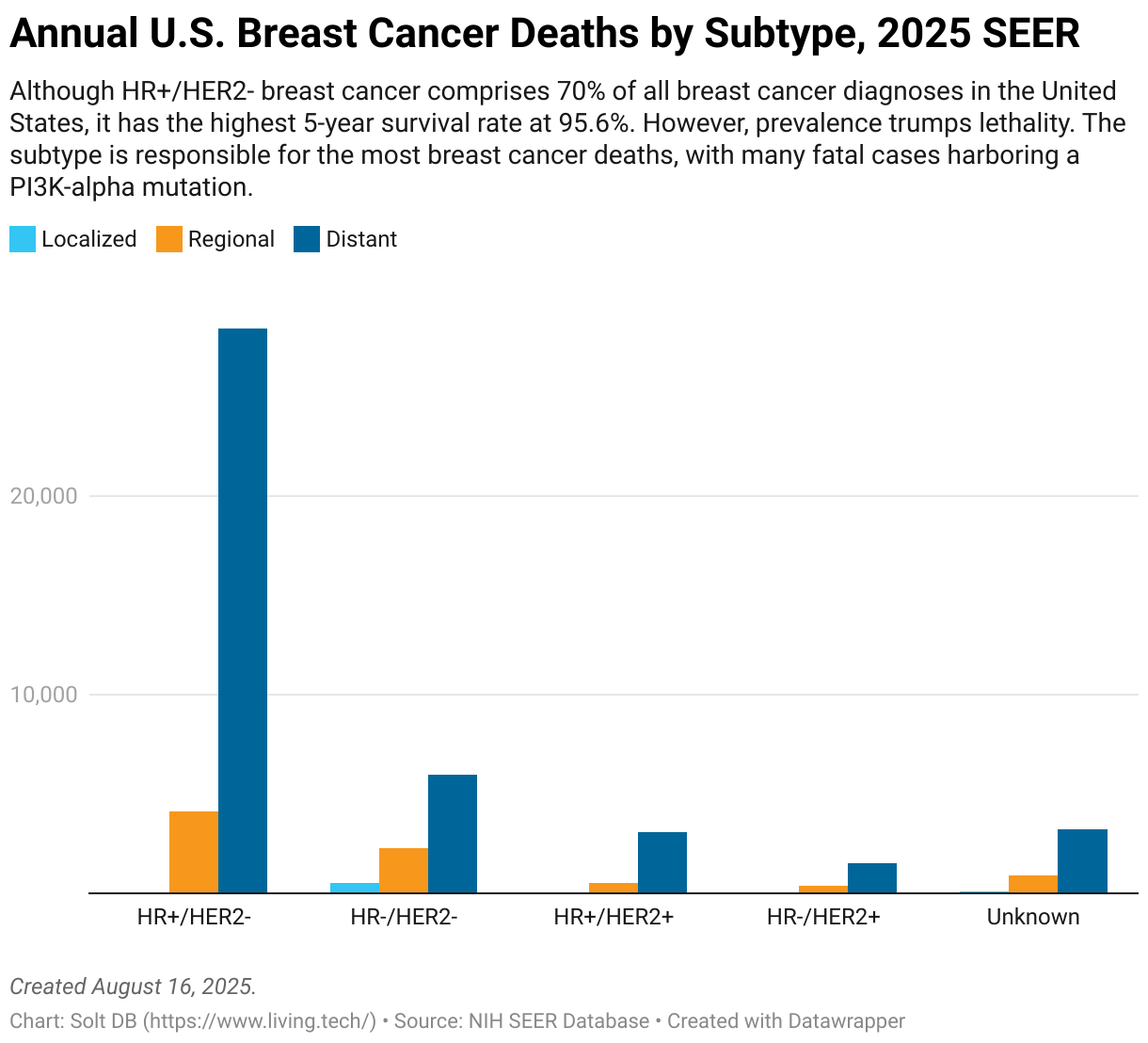

Whereas HR+/HER2- breast cancer comprises 70% of all breast cancer diagnoses in the United States, it also has the highest five-year survival rate at 95.6%, according to the National Institutes of Health (NIH) SEER database. Improved screening rates have helped catch more cancers early, when they're easiest to treat.

However, prevalence trumps lethality. Most breast cancer deaths are still caused by metastatic HR+/HER2- breast cancer, meaning it has spread beyond the primary tumor to regional lymph nodes and/or distant tissues. The majority of lethal cases harbor a PI3K-alpha mutation, which is present in an estimated 40% of all HR+/HER2- breast cancer tumors.

PI3K-alpha regulates how cells capture glucose from the bloodstream, which is converted into molecular energy to power cells. Its biological importance has significantly hindered attempts to inhibit mutated PI3K-alpha proteins, as therapeutic molecules must selectively spare healthy versions of the protein ("wild-type" or WT).

To design a selective drug, scientists must exploit structural differences between the target protein and possible off-target proteins. That would give a drug candidate a unique place to dock onto a target protein, reducing off-target binding. Unfortunately, there are few meaningful differences between the 3D structures of WT and mutant PI3K-alpha proteins.

Failing to discriminate between WT and mutant PI3K-alpha proteins causes hyperglycemia, or too much glucose in the blood. Makes sense. If a drug inhibits PI3K-alpha, and PI3K-alpha is how cells retrieve glucose from the bloodstream, then blanket antagonism will result in a lot of glucose in the blood with nowhere to go.

Hyperglycemia is doubly troublesome in HR+/HER2- breast cancer because half of all patients are prediabetic or diabetic – two conditions characterized by poor glucose metabolism. Giving patients a non-selective PI3K-alpha inhibitor can quickly worsen glucose control and lead to ketoacidosis as the body switches from glucose to ketones for fuel. Ketoacidosis can be fatal.

It gets more difficult.

In addition to sparing WT PI3K-alpha proteins, an ideal drug would also selectively distinguish between isoforms. These are slightly different structural versions of a parent protein with unique functions. They're usually designated by Greek letters. For example, the PI3K gene encodes four isoforms: alpha, beta, delta, and gamma.

Drugs that inhibit beta, delta, and gamma can cause higher rates of gastrointestinal and immune side effects. Multiple PI3K-alpha drug candidates have been terminated due to unacceptable side effects caused by PI3K-gamma inhibition.

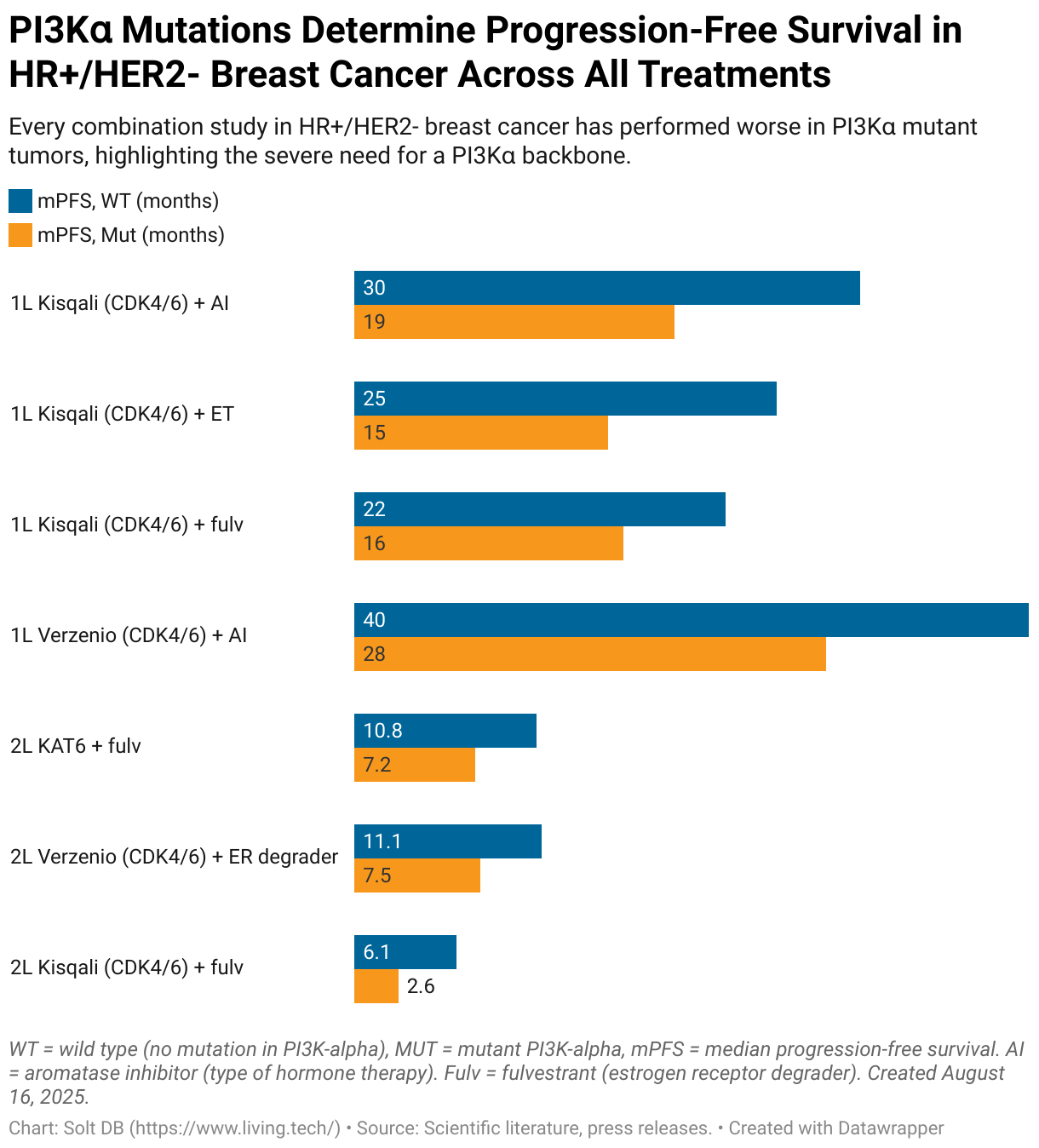

The biological importance of PI3K-alpha and difficulty in targeting mutant isoforms has resulted in consistent clinical failures.

Each time a promising combination is evaluated in HR+/HER2- breast cancer, it performs significantly better against tumors with WT PI3K-alpha (meaning no mutations) than in tumors with mutant PI3K-alpha.

This highlights the severe need for mutant-selective PI3K-alpha inhibitors that can be used as backbones in combination treatments, similar to how CDK4/6 inhibitors have proliferated across treatment settings on their way to nearly $13 billion in annual revenue.

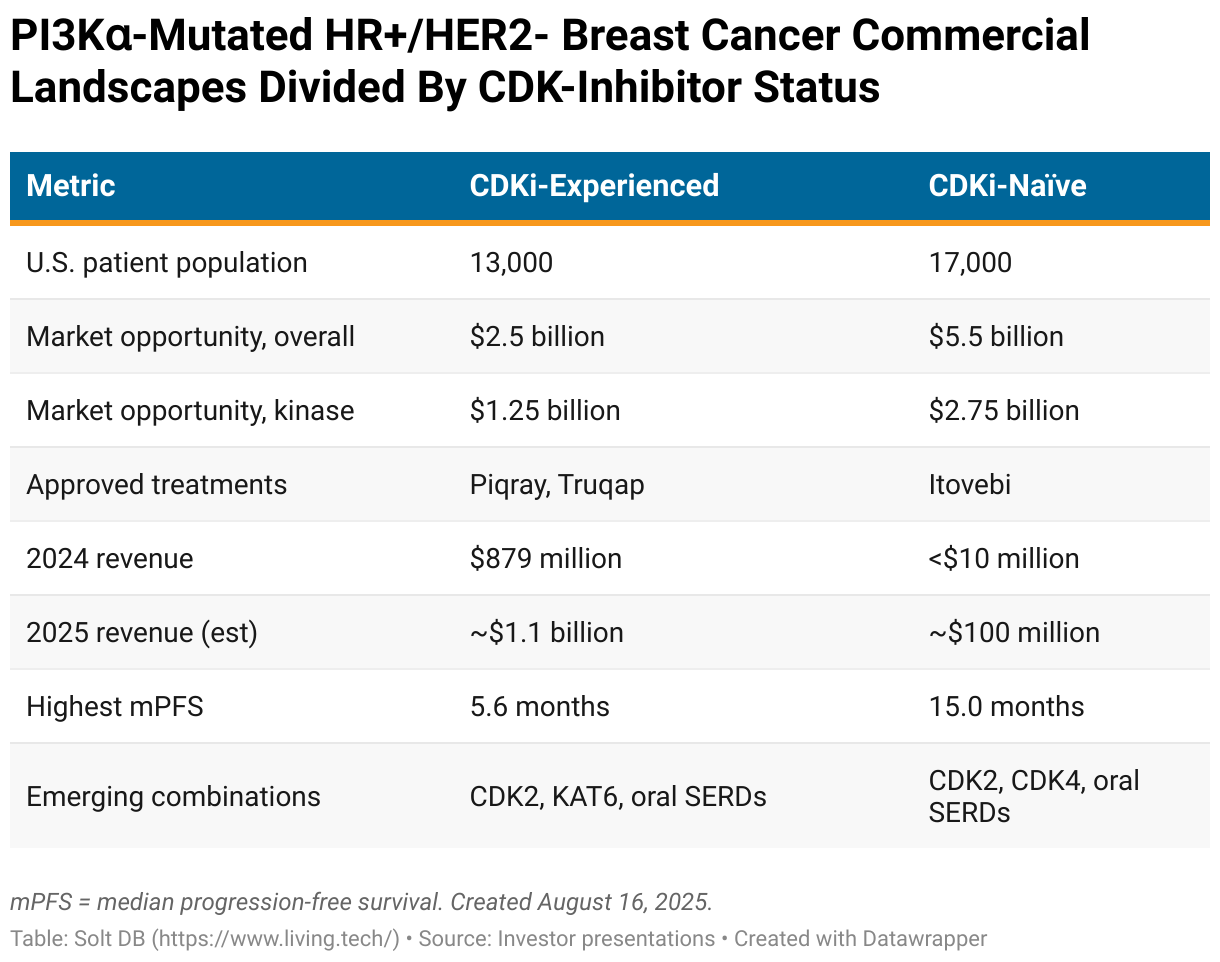

Two Patient Populations Drive Commercial Opportunity for PI3K Pathway Inhibitors in HR+/HER2- Breast Cancer

Relay Therapeutics is developing zovegalisib for two specific patient populations:

- CDKi-naïve, or individuals who have not yet been treated with a CDK4/6 inhibitor

- CDKi-experienced, or individuals who have already been treated with a CDK4/6 inhibitor

These are also referred to as first-line (1L) and second-line (2L) treatment settings, respectively, which I've commonly used in past communications. Going forward, I'll refer to these as CDKi-naïve (1L) and CDKi-experienced (2L) populations, which is a more accurate way to think of the evolving commercial landscape.

CDKi-Experienced Commercial Opportunity and Landscape

This is the initial market opportunity for zovegalisib and the patient population of the pivotal ReDiscover-2 study. Most treatment regimens in development are a doublet combination with fulvestrant, which is a selective estrogen receptor degrader (SERD).

Zovegalisib from Relay Therapeutics

- Type: Pan-mutant, PI3K-alpha inhibitor

- Advantages: Highest tolerability in landscape leads to deepest responses

- Disadvantages: Highest daily pill burden (four) in landscape

Relay Therapeutics matched its development strategy for zovegalisib to the commercial opportunity. Initial development focuses on a combination with fulvestrant in CDKi-experienced patients (2L+). Why? Because it's the most commercially-proven market.

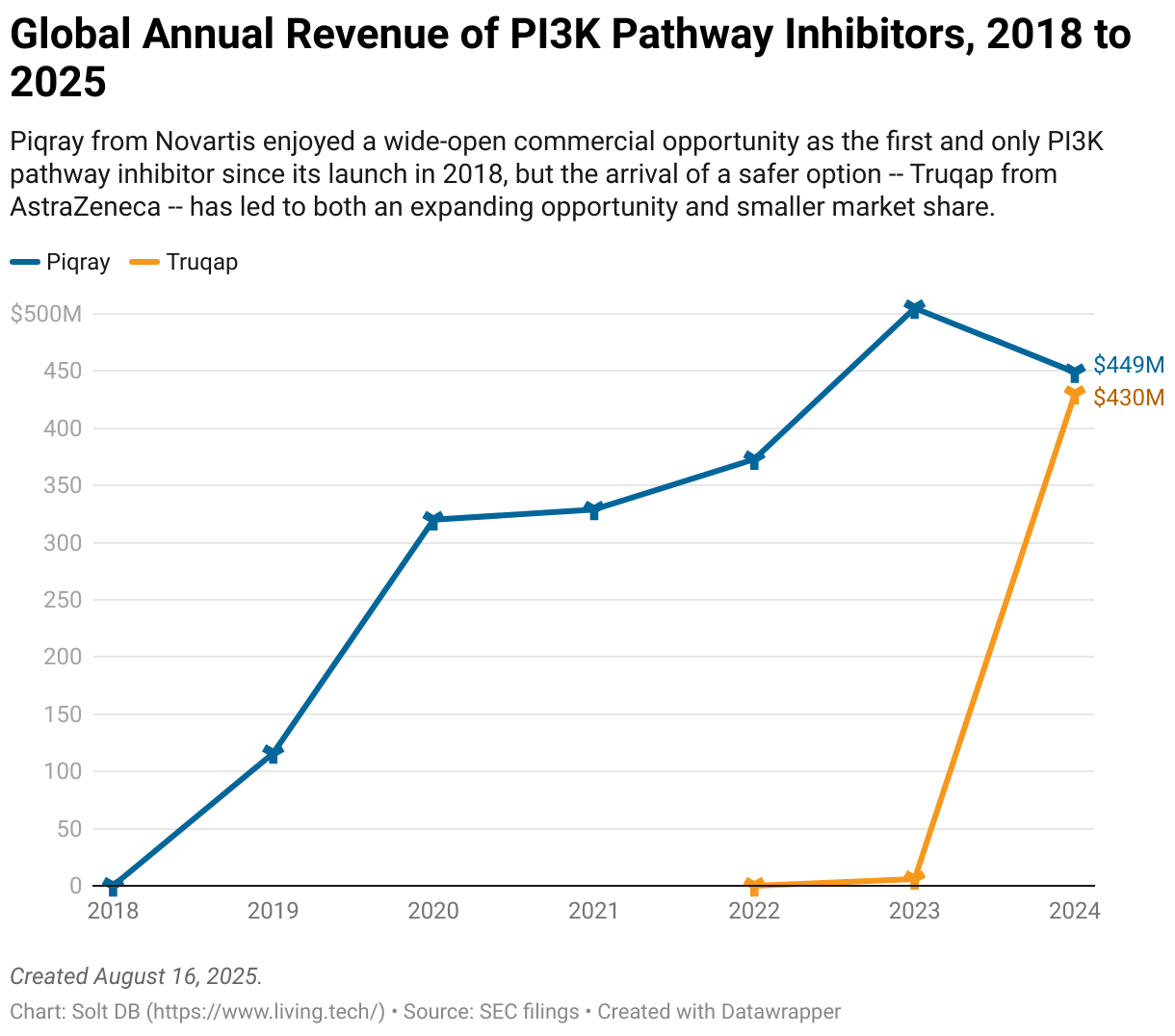

PI3K pathway inhibitors generated full-year 2023 revenue of $511 million in this treatment setting. Truqap had its first full year on the market in 2024, which lifted the landscape's total revenue haul 72% to $879 million. The market's leading treatment is on pace to generate full-year 2025 revenue of nearly $700 million.

Although competitive pressures dragged down sales of Piqray last year, the first mover generated a respectable $449 million in revenue. Novartis stopped reporting revenue on a quarterly basis in 2021, which introduces some statistical fog when evaluating the landscape during the year. The asset is expected to hover near or gradually decline from current revenue levels for the foreseeable future.

Despite offering similar clinical benefit as Piqray, Truqap ate the competitor's lunch because it has much lower rates of grade 3 or grade 4 hyperglycemia, which remains the most devastating tolerability issue for the landscape. Truqap carries a 2% risk of severe hyperglycemia, compared to 29% for the first mover.

Zovegalisib has the opportunity to do the same to Truqap by offering much better efficacy and much better overall safety. Investors will find out in a few short years.

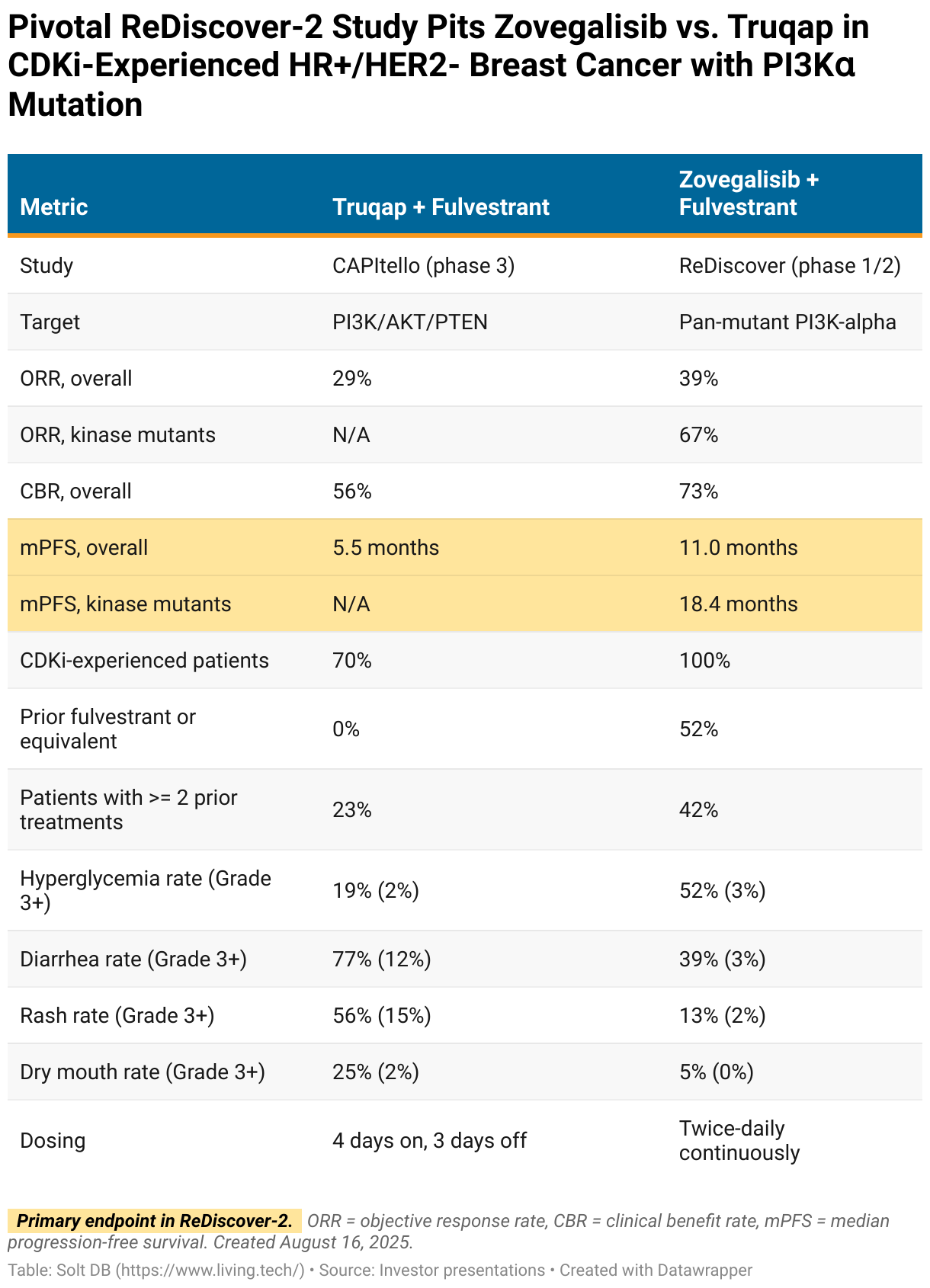

Relay Therapeutics has begun enrolling patients in the pivotal ReDiscover-2 study. The 540-patient clinical trial pits zovegalisib plus fulvestrant against Truqap plus fulvestrant in a high-stakes, winner-take-most showdown.

The study design includes two primary endpoints based on median progression-free survival (mPFS), which is the length of time patients remain on treatment without their cancers worsening.

- mPFS in tumors with kinase mutations

- mPFS in the overall patient population, meaning both kinase and helical mutations. Each type of mutation occurs in about 50% of all HR+/HER2- breast cancers, although both can be present in the same tumor.

Relay Therapeutics made a great strategic decision – if not an aggressive one.

By going head-to-head with the current market leader, zovegalisib has the potential to steal market share from Truqap immediately upon launching. That would be more difficult had the pivotal study gone against placebo or Piqray, which are less challenging clinical benchmarks but aren't commercially-relevant benchmarks.

By persuading regulators to allow a primary endpoint based on kinase mutations specifically, Relay Therapeutics is positioning for a quick commercial ramp against existing treatment options. It's also positioning itself to play defense against emerging competitors further behind.

Neither Piqray nor Truqap has a mutation-specific approval. Considering half of the patient population has a kinase mutation, the revenue opportunity upon launch could exceed $1 billion in kinase mutants alone – and only zovegalisib would be able to access it.

This isn't wishful total addressable market (TAM) math either. Piqray and Truqap could be generating $1 billion in real-world revenue in kinase mutant tumors by 2028. That could all immediately flow to zovegalisib upon approval.

Investors should remain grounded when extrapolating results from mid-stage studies to pivotal studies. Historically speaking, many drug candidates perform worse as studies get larger and longer. However, the unusually robust clinical trials conducted by Relay Therapeutics give an unusual degree of certainty. In fact, the two molecules it has advanced each delivered better results as studies matured, the opposite of the expected trend.

Zovegalisib has a significant margin of safety heading into ReDiscover-2.

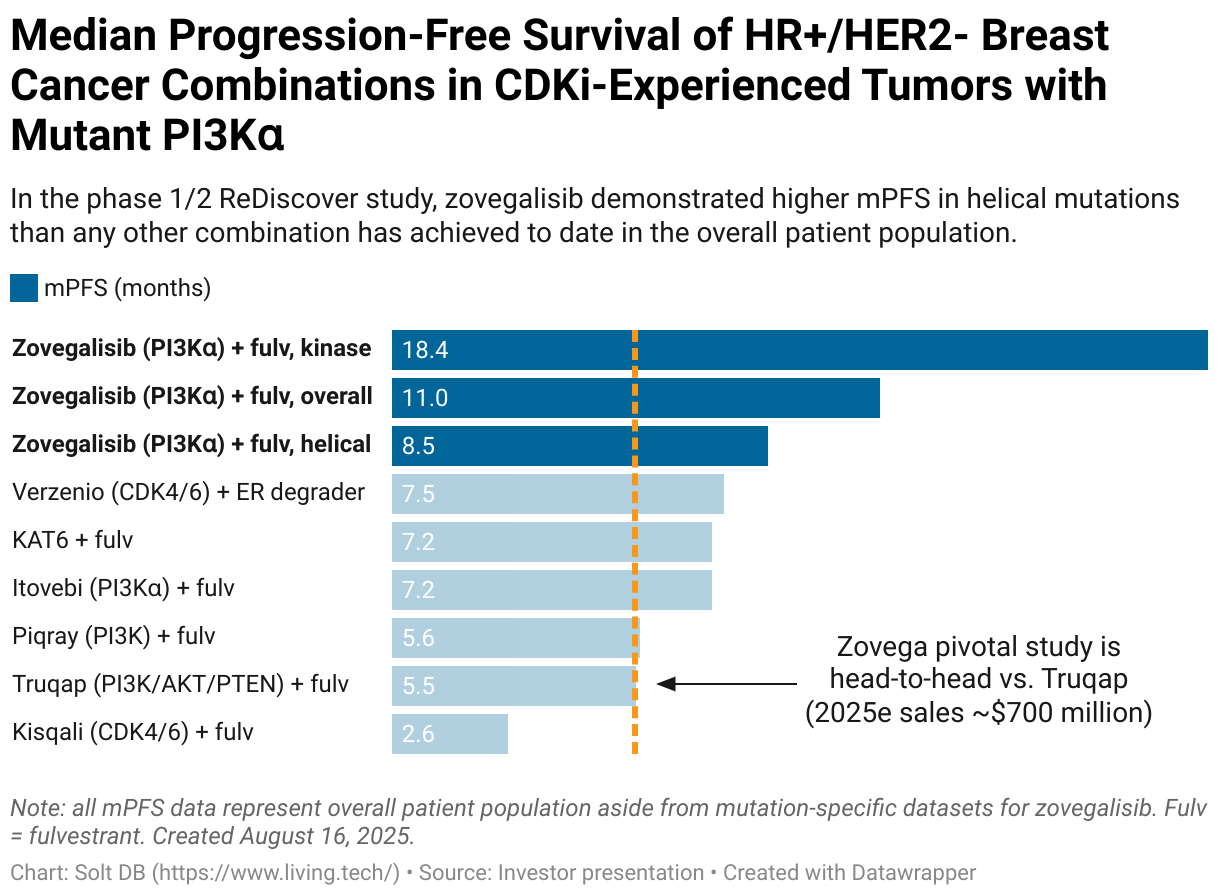

In its phase 1/2 study, the doublet with fulvestrant demonstrated an mPFS of 18.4 months in tumors with a kinase mutation and an mPFS of 11.0 months overall. These are the primary endpoints of the pivotal program. If zovegalisib replicates these metrics in the pivotal study, then it would quickly become the go-to PI3K pathway inhibitor. It could become one of the fastest oncology launches ever.

The base case expects a topline data readout from the pivotal ReDiscover-2 study in mid-2028 for both primary endpoints. That could allow for regulatory submission before the end of that year, followed by an approval and launch in summer 2029. The clinical trial will continue for several more years to generate data on important secondary endpoints, including overall survival (OS), duration of response (DoR), and quality of life (QoL).

But the study design and potential for a significant performance gap between zovegalisib and Truqap creates a tantalizing possibility: Could the pivotal ReDiscover-2 study be stopped early over ethical concerns?

- Truqap is a PI3K pathway inhibitor. It shouldn't perform meaningfully different in kinase or helical mutations. In its own pivotal CAPItello study, the asset achieved an overall mPFS of 5.5 months. It didn't collect data by mutation status. It's likely to fall between 5.5 months to 7.5 months.

- Zovegalisib is a pan-mutant PI3K-alpha inhibitor. It should perform meaningfully better in kinase mutations than helical mutations. In its phase 1/2 study, zovegalisib achieved an mPFS of 18.4 months in kinase mutations. In helical mutations, it was 8.5 months. It should demonstrate mPFS in kinase mutations between 11 months and 18 months in ReDiscover-2.

For the first primary endpoint of mPFS in kinase mutant tumors, the data would support an approval even if Truqap performed at the top-end of its range and zovegalisib near the bottom, or mPFS of 7.5 months vs. 11.0 months.

The opposite scenario is also possible.

If Truqap performs near the low-end of its range (5.5 months) and zovegalisib near the high-end (18 months), then the study could be stopped early. If the data are trending that way, then there should be enough patients enrolled by mid- to late 2027 for the Data Monitoring Board (DMB) to be statistically confident the gap won't be closed at full enrollment. That could prompt action.

After all, if patients with kinase mutations progress 5.5 months after receiving Truqap and nearly 18 months after treatment with zovegalisib, then would it be ethical to continue randomizing new patients? Probably not.

"Stopping early" might be slightly imprecise. The ReDiscover-2 study would need to continue to generate datasets for the other primary endpoint and all secondary endpoints. But the DMB, the FDA, and Relay Therapeutics could amend the study design such that only patients with helical mutations would be randomized. All patients with kinase mutations would receive zovegalisib. That would create a different path to generating the same or similar data as originally planned.

Importantly, calling the primary endpoint in mid- to late-2027 could accelerate regulatory and commercial timelines by up to 12 months. The sooner zovegalisib can get to market in the CDKi-experienced setting, the sooner it can begin generating hundreds of millions of dollars – and eventually over $1 billion – in annual revenue.

Truqap (capivasertib) from AstraZeneca

- Type: PI3K/AKT/PTEN inhibitor

- Advantages: Indirect inhibition of PI3K-alpha leads to lower rates of grade 3 hyperglycemia than Piqray

- Disadvantages: High overall rates of diarrhea, high rates of grade 3+ rash

AstraZeneca is developing Truqap in prostate cancer and CDKi-naïve HR+/HER2- breast cancer. Right now, it's only approved in CDKi-experienced HR+/HER2- breast cancer, which means all revenue reflects the exact commercial opportunity Relay Therapeutics is targeting initially.

Although Truqap has mopped the floor with Piqray, the asset encountered a regulatory setback earlier this year.

In February 2025, the FDA updated its product label with what's called a major change. Specifically, it added new information to the "Warnings and Precautions" section related to hyperglycemia. All PI3K pathway inhibitors are expected to carry a similar label though – even zovegalisib.

Piqray (alpelisib) from Novartis

- Type: PI3K inhibitor slightly more selective for the alpha isoform

- Advantages: Higher ORR, lower rates of rash than Truqap

- Disadvantages: High rate of grade 3+ hyperglycemia, low overall tolerability

Piqray was the first PI3K pathway inhibitor to earn approval in Q1 2019. An otherwise respectable launch and ramp was knocked off course during the pandemic. The brand never fully recovered.

Novartis stopped reporting Piqray revenue on a quarterly basis beginning in 2021, clawed its way to full-year 2023 revenue of $505 million, and then got trounced by Truqap.

Alpelisib was the only PI3K pathway inhibitor to earn approval in both oncology (branded as Piqray) and vascular malformations (branded as Vijoice). These are a group of chronic overgrowth disorders characterized by large, non-cancerous tumors. An estimated 170,000 cases of vascular malformations in the United States alone are driven by PI3K-alpha mutants.

While Vijoice earned an accelerated approval based on initial phase 1/2 data, the confirmatory EPIK-2 study whiffed on all endpoints in late 2024. Novartis has withdrawn the drug from the market. It was never approved in Europe due to a lack of meaningful data.

Vascular malformations are an additional, separate opportunity for zovegalisib.

STX-478 (tersolisib) from Eli Lilly via Scorpion Therapeutics

- Type: Pan-mutant, PI3K-alpha inhibitor

- Advantages: Once-daily dosing potential, Eli Lilly owns a robust breast cancer pipeline

- Disadvantages: Signs of grade 3+ liver toxicity in dose escalation could limit potential in combinations needed for commercial success

Eli Lilly wields Verzenio (CDK4/6) and imlunestrant (an oral SERD candidate), but has struggled to find development success in the emerging opportunity of PI3K pathway inhibitors. It decided to instead buy its way into the race.

The world's largest drug developer acquired the pan-mutant, PI3K-alpha inhibitor STX-478 (tersolisib) from Scorpion Therapeutics for $1 billion upfront and up to $1 billion in additional milestone payouts. From Eli Lilly's perspective, it was a low-risk, high-reward investment if it can add a third pillar to its HR+/HER2- breast cancer portfolio. That's especially true since Verzenio, imlunestrant, and tersolisib could all be combined with each other.

The acquisition also accelerates the company's development timeline. That's doubly important considering Verzenio loses patent exclusivity at the end of 2031. While tersolisib is about 12 to 24 months behind zovegalisib, that's better than the suitor's former timeline.

In late 2024, Eli Lilly terminated LOXO-783 due to off-target activity. The drug candidate was optimized for selectivity against H1047R, which is the most common type of PI3K-alpha kinase mutation. Other drug developers have taken or are taking the same route to targeting kinase mutations, but all have failed due to unacceptable tolerability, usually due to activity against PI3K-gamma.

By contrast, zovegalisib and tersolisib are pan-mutant inhibitors, meaning the class is optimized for activity against all PI3K-alpha mutants. That includes major kinase (H1047R, H1047X) and helical (E542X, E545X) mutations.

Eli Lilly had been preparing to advance its own pan-mutant, PI3K-alpha inhibitor LY4045004 into phase 1 clinical trials in 2025, but at the final go/no-go decision point it shelved the internal candidate and acquired tersolisib instead.

Investors should expect tersolisib to be the most competitive molecule to zovegalisib. It's dosed once-daily, giving it a convenience edge. It's moderately more selective for kinase domains of the PI3K-alpha protein, but attaches near the same allosteric pocket discovered by Relay Therapeutics.

There haven't been any new developments for tersolisib since the asset was acquired by Eli Lilly in January 2025. Investors can compare against the latest zovegalisib data, but these comparisons aren't apples-to-apples.

Tersolisib only has public data from its dose escalation study as a monotherapy (not combined with other agents). That means a handful of patients were treated at many different doses. As such, the efficacy and tolerability profiles will give directional signals but be difficult to interpret until a recommended phase 2 dose (RP2D) is selected.

There are no public efficacy data available for zovegalisib from its monotherapy dose escalation study, as Relay Therapeutics prioritized CDKi-experienced HR+/HER2- breast cancer from the start – and that required combinations with fulvestrant.

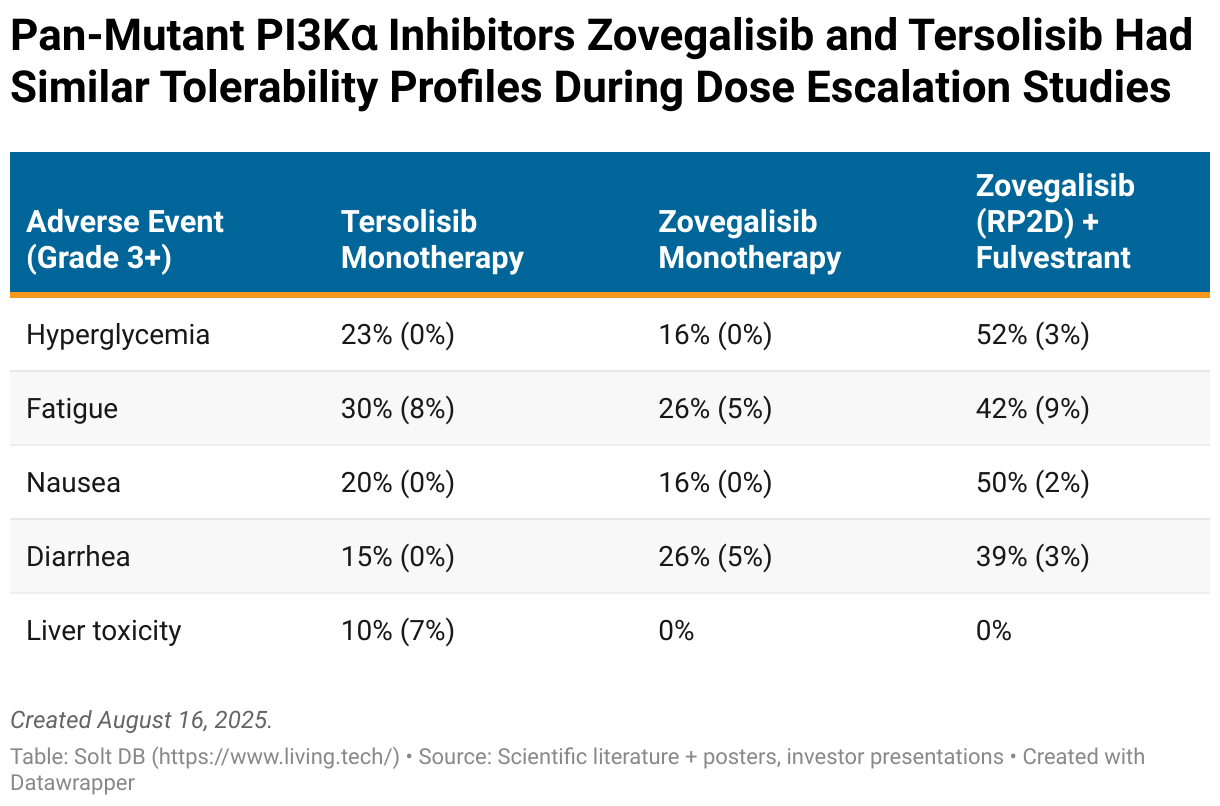

Analysts were quick to point out tersolisib's strong tolerability profile when results were reported in December 2024. As a fellow pan-mutant PI3K-alpha inhibitor, it should have a similar rate of adverse events as zovegalisib. However, efficacy data will improve and tolerability data will deteriorate as Eli Lilly settles in on an RP2D.

Relay Therapeutics followed a similar trajectory. Initial data readouts for zovegalisib demonstrated lower efficacy (an ORR of just 12.5% vs. 39% today) and higher tolerability (see table below), which both reversed as the company optimized for PI3K-alpha target engagement and bioavailability. If more drug product is floating around a patient's bloodstream than available PI3K-alpha proteins to disable, then even the most selective inhibitor will find the next-best targets. That triggers adverse events.

This is a reminder that there are almost always tradeoffs in drug development. Optimizing for one metric often comes at the expense of others. Relay Therapeutics decided to maximize efficacy while tiptoeing the line of grade 3 adverse events. The reasoning is that grade 1-2 adverse events are self-resolving or only require minimal interruptions, while grade 3 adverse events can significantly impact a treatment's commercial opportunity and approved label.

For a more apples-to-apples comparison, here's how the tolerability profiles of tersolisib and zovegalisib stack up from the initial data readouts in dose escalation studies.

The most significant difference to date is that tersolisib caused six cases of severe liver toxicity in its phase 1 dose escalation study. That included five cases of grade 3 (8%, 5/61) and one case of grade 4 (2%, 1/61). One of each occurred at a dose much higher than the maximum tolerated dose and can be excluded, but that still leaves a grade 3 liver toxicity rate of almost 7% (4/59).

It's concerning to see potential liver injury from the monotherapy. The entire commercial opportunity hinges on developing PI3K-alpha inhibitors as a backbone treatment, meaning they must be combined with various other agents to maximize benefit. Combinations often have higher rates of adverse events because the tolerability profile of multiple drugs is stacked, but they can also amplify each other.

For example, all CDK4/6 inhibitors cause at least 30% of patients to experience elevated liver enzymes. Although rates of grade 3 events are in the single digits for the established backbone therapies, combining multiple agents with moderate grade 1-2 liver toxicity could lead to much higher rates of grade 3 cases in combination.

Gedatolisib from Celcuity

- Type: PI3K/mTOR inhibitor

- Advantages: Intravenous administration results in higher target engagement and reduces risk of liver toxicity

- Disadvantages: Intravenous administration is less convenient, use of triplet combination in CDKi-experienced patients isn't comparable to doublets

Celcuity doesn't appear to be a serious competitor in the broader PI3K pathway inhibitor landscape at this time, but it is the weirdest.

Gedatolisib isn't selective for PI3K-alpha, instead hitting all four main isoforms (alpha, beta, gamma, and delta). The drug candidate is administered intravenously on a weekly basis, whereas every asset discussed above is taken orally each day or so. IV administration can bypass liver clearance and result in higher target engagement compared to oral administration, but it's less convenient and more expensive.

Comparisons to existing and emerging treatments will be trickier. Celcuity is evaluating a triplet with fulvestrant and a CDK4/6 inhibitor in the CDKi-experienced setting, which most competitors are targeting with doublets using only fulvestrant. Adding a third agent will scramble comparisons.

In late July 2025, Celcuity announced phase 3 data in HR+/HER2- breast cancer tumors with wild-type PI3K – meaning no mutations in the PI3K-alpha gene. This is not the same patient population being targeted by Relay Therapeutics or the companies discussed above, so gedatolisib will not be competing for patients based on that study alone.

The challenger expects to announce phase 3 data in CDKi-experienced, HR+/HER2- breast cancer tumors with mutant PI3K-alpha before the end of 2025. These data will be comparable to zovegalisib and the broader landscape.

On the one hand, all combinations tried to date have performed significantly worse in mutant PI3K-alpha tumors than WT PI3K-alpha tumors. On the other hand, gedatolisib is a PI3K pathway inhibitor. It probably should perform better in mutant tumors.

For the pivotal cohort in CDKi-experienced patients, Celcuity designed the study with a primary endpoint comparing a triplet (gedatolisib plus fulvestrant plus Ibrance) to a doublet (Piqray plus fulvestrant). That's a bit awkward.

The proper comparison would be a doublet vs. a doublet, or a triplet vs. a triplet. If Piqray or Truqap or zovegalisib were evaluated in triplets with a CDK inhibitor in this patient population, then they'd probably outperform doublets, too.

It also raises the regulatory risk. Will the FDA find the data clinically meaningful considering the comparator arm is lacking a major active component? Celcuity doesn't have a robust data package to counter regulatory pushback. Prior to the pivotal VIKTORIA-1 study, the triplet was evaluated in just 11 patients with mutant PI3K-alpha.

Will these data be commercially relevant? There is something called CDKi retreatment, which, as the name implies, gives CDKi-experienced patients a CDK inhibitor again. Celcuity could be eyeing that specific patient opportunity, which won't be competing for patients with the assets described above.

In the WT PI3K tumor population, the triplet (gedatolisib plus fulvestrant plus Ibrance) delivered an mPFS of 9.3 months. The doublet (gedatolisib plus fulvestrant) delivered an mPFS of 7.4 months.

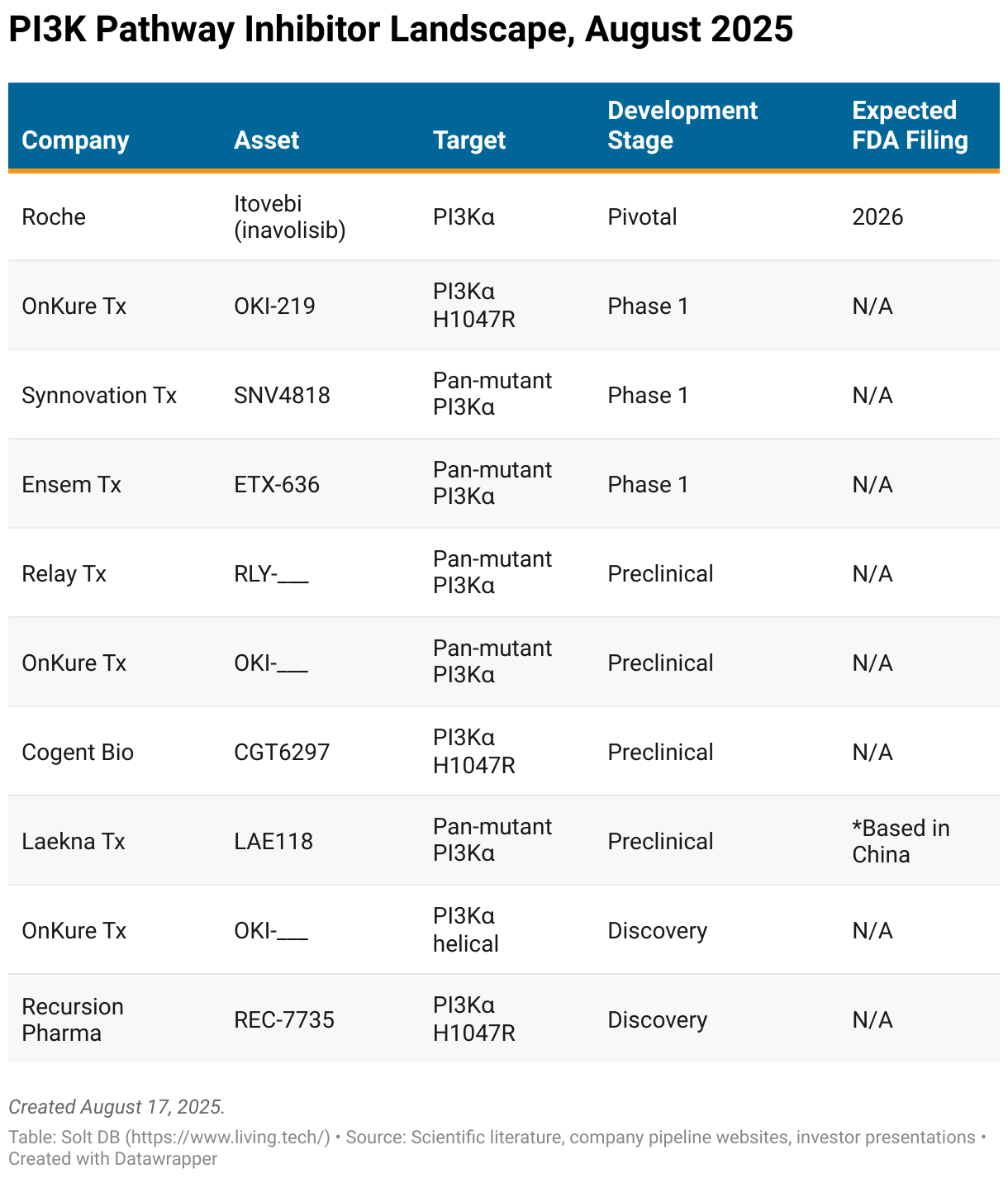

Other challengers in the CDKi-experienced landscape

The intro was about four million words ago, but remember that part about the largest commercial opportunities attracting the most competition?

There's a long list of additional, less mature competitors in the CDKi-experienced landscape. That includes Itovebi from Roche, which is approved in CDKi-naïve patients with advanced HR+/HER2- breast cancer. A combination with fulvestrant is being evaluated in a pivotal study vs. Piqray plus fulvestrant.

My intention is to publish a diabolically-detailed research note on competitive landscape dynamics once or twice per year as updates roll in. Some of these assets will be discussed in greater detail in the next few years, although most will be terminated.

CDKi-Naïve Commercial Opportunity and Landscape

Relay Therapeutics is also exploring multiple combinations of zovegalisib with unique CDK inhibitors and fulvestrant in CDKi-naïve patients (1L), but these efforts are less mature. Due to longer duration of response in CDKi-naïve patients, investors must prepare for very long development timelines and gaps between data readouts.

Investors don't have any data from zovegalisib in CDKi-naïve patient populations. This indication is not included in my current model for Relay Therapeutics.

As of August 2025, the company is evaluating the following triplet combinations:

- Zovegalisib plus fulvestrant plus Kisqali (CDK4/6 inhibitor from Novartis)

- Zovegalisib plus fulvestrant plus atirmociclib (CDK4 inhibitor from Pfizer)

The decision to change zovegalisib's dose from 600 mg twice-daily fasted (on an empty stomach) to 400 mg twice-daily fed (with food) will benefit the tolerability for all indications, including vascular malformations. It reduces the daily pill burden from six pills to four. It should also reduce the rate of upper gastrointestinal (GI) side effects such as nausea and vomiting.

The expected tolerability improvement will be most valuable in the CDKi-naïve setting in combinations with CDK inhibitors, as these drugs often have relatively high rates of GI adverse events. Stacking zovegalisib's adverse events on top could have jeopardized development in this large commercial opportunity – and could still.

Itovebi (inavolasib) from Roche

- Type: PI3K-alpha inhibitor

- Advantages: More selective than Piqray, Roche owns a robust breast cancer pipeline

- Disadvantages: Relatively high rates of grade 3 hyperglycemia

Itovebi illustrates the importance of syncing the development and commercialization strategies for new drug candidates.

Many drug candidates are initially developed in later treatment settings, then gradually expand into earlier treatment settings with additional pivotal programs. Roche developed Itovebi in reverse. It prioritized the CDKi-naïve setting, earned the first approval for a PI3K-alpha inhibitor there, and is now going head-to-head against Piqray in a phase 3 study that could expand the label into the CDKi-experienced setting.

It's still early, but that risk hasn't paid off so far. Oncologists comfortable using PI3K-alpha inhibitors in CDKi-experienced patients don't appear quite as eager to deploy Itovebi in earlier settings, at least not yet.

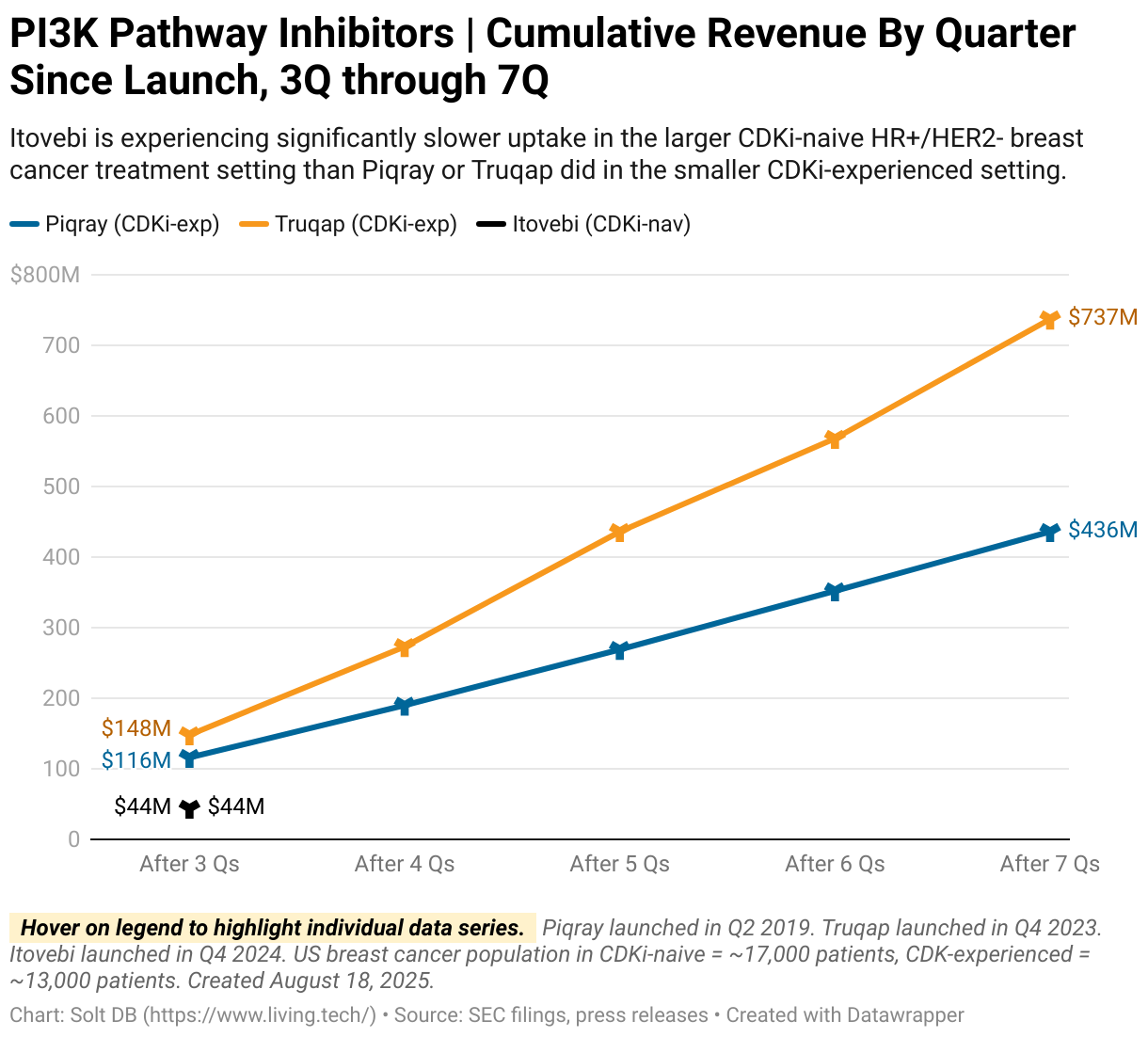

Roche reported revenue of just $44 million for Itovebi in its first three quarters on the market. That lags behind the revenue hauls from both Piqray ($116 million in 2019 dollars) and Truqap ($148 million in 2024 dollars) at the same point in their launch trajectories, albeit in the CDKi-experienced setting.

A recent approval in Europe should boost Itovebi. That will roughly double the patient population available, although due to lower drug prices in Europe compared to the United States, it won't double the revenue opportunity.

Why did the pharma leader choose to develop the asset "in reverse"?

Hindsight is 20/20. Today we know the CDKi-experienced market opportunity has been de-risked by Piqray and Truqap, which combined for full-year 2024 revenue of $879 million. We also now know Truqap is the clear standard of care for the drug class due to greatly reduced risk of hyperglycemia, so any asset clamoring for that title needs to go head-to-head with Truqap, not Piqray.

Obviously, none of that information was available years ago when Roche designed the pivotal programs for Itovebi. This is an example of the first-mover disadvantage that's common in drug development. Companies arriving to the opportunity later – Relay Therapeutics and Eli Lilly – gain an advantage by sitting back, evaluating commercial developments, and designing optimized development strategies. Of course, many years from now they'll be exposed to disruption.

Why might Itovebi be suffering from slow uptake? It could be due to severe hyperglycemia events since launch.

In March 2025, Roche issued a "Dear Doctor" warning letter to oncologists after two patients experienced grade 4 ketoacidosis, which is caused by severe, untreated hyperglycemia. These letters remind (plead with) health care providers to follow a drug's approved label. In this specific instance, the company pointed to the known risks in patients with type 1 diabetes and type 2 diabetes, which must have stable glucose levels prior to beginning treatment.

This isn't a showstopper. Roche didn't observe any cases of ketoacidosis in its pivotal study, but investigators (are supposed to) follow strict rules in a clinical study. The real-world can be more chaotic. Humans don't always like to thoroughly read instructions or follow directions.

This at least suggests oncologists are still getting comfortable with Itovebi in the CDKi-naïve setting. It also suggests Roche needs to do a better job educating health care providers, which will de-risk the commercial opportunity for future PI3K-alpha inhibitors.

Roche has also begun evaluating Itovebi in the neoadjuvant treatment setting, which is larger and earlier than the CDKi-naïve patient population. The commercial opportunity for PI3K pathway inhibitors in the adjuvant setting could exceed $10 billion in annual revenue.

News Flow & Modeling Insights

(Rebuilt.)

The new model for Relay Therapeutics is based solely on zovegalisib in the CDKi-experienced setting of HR+/HER2- breast cancer in the United States. No other assets, indications, or geographies are included.

The current model makes the following assumptions:

- The pivotal ReDiscover-2 study has a topline data readout in Q3 2028.

- Zovegalisib is submitted with a standard 10-month regulatory review. (It takes a few months from data readout to regulatory submission.)

- Zovegalisib launches in Q4 2029 with an approval in at least kinase mutations. A companion diagnostic required for this label claim is developed without delays.

- Zovegalisib generates full-year 2029 revenue of at least $45 million and full-year 2030 revenue of at least $600 million.

A lot can change in five years. RFK Jr's head in a jar could be the FDA commissioner in five years, who knows!

But zovegalisib's early commercial opportunity is relatively protected thanks to the expected kinase-specific approval. No other drug product is expected to have the same label by 2030. ReDiscover-2 is the only active or planned late-stage program with a kinase-specific endpoint, so tersolisib might be the next in 2031. The two assets could eat the market together in the 2030s.

Strictly based on the CDKi-experienced commercial opportunity and expected full-year 2030 revenue:

- Relay Therapeutics would have an estimated fair valuation of over $4.2 billion.

- If the company uses a mix of stock offerings and debt to fund investments in commercial infrastructure, then it would have 225 million to 250 million shares outstanding in 2030. This assumes 3% dilution per year and a large public offering in 2028.

- That yields a modeled fair value of at least $17.68 per share based on this single asset, indication, and geography.

- Starting from a share price of roughly $3.50 today, the stock would have an annualized rate of return of 38% over the next five years.

Commercial drug developers ramping high-impact assets are often valued based on forward-looking prospects, not static performance from a single year.

A kinase-specific approval would give zovegalisib the potential to be one of the fastest oncology launches in history. Investors would know that by 1H 2030.

What if zovegalisib is on a trajectory that makes it a blockbuster with over $1 billion in revenue by 2031, the second full year on the market? The valuation could be two or three times higher than my modeled fair valuation in 2030.

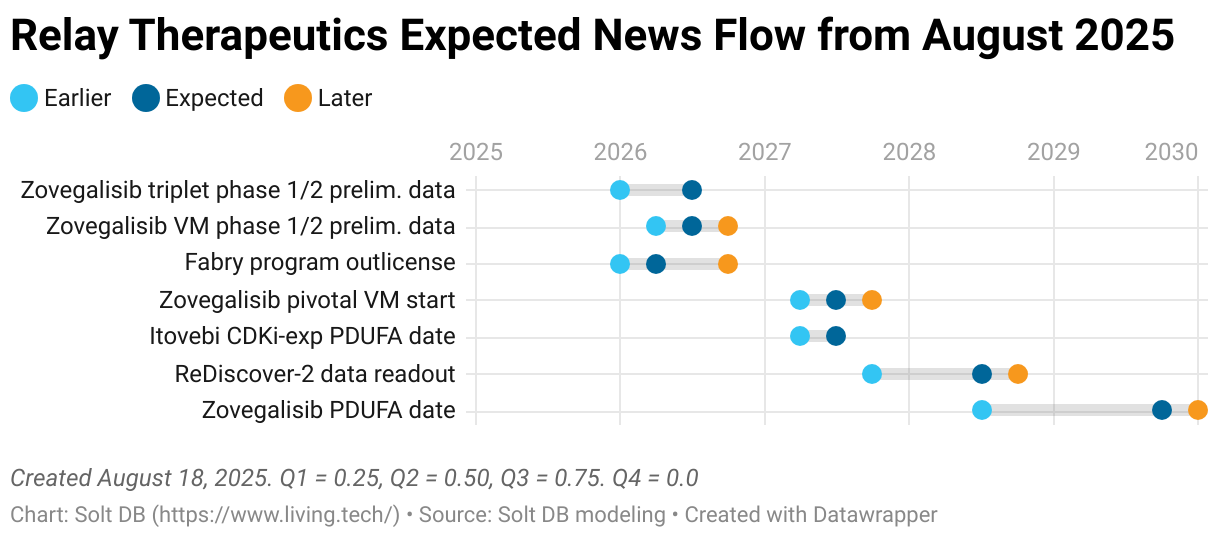

The model will adapt as more information becomes available. Investors will soon get directional signals on the prospects for zovegalisib in CDKi-naïve settings (perhaps by Q4 2025) and vascular malformations (perhaps by early 2026). Each individual indication can add over $1 billion in additional peak annual revenue.

Potential up-risking and de-risking events

A handful of identifiable events could lead to meaningful changes to the model.

- Companion diagnostic delays (up-risking): An approval in kinase mutations will be meaningless if Relay Therapeutics doesn't have a companion diagnostic available. This is a simple genomic diagnostic to determine if a patient has a kinase mutation. The company will need to tap external diagnostic developers to develop such a test on its behalf.

- Americans decide to regulate drug prices (up-risking): The current model assumes a wholesale acquisition cost (WAC) for zovegalisib of $22,500 per month. If the United States decides to join the rest of the civilized world in regulating drug prices by 2030, or that's even on the horizon, then the model and commercial opportunity would be materially lower.

- Priority review granted in 2029 (de-risking): If zovegalisib is granted priority review, then it could accelerate commercial launch and ramp timelines by four (4) months.

- Kinase mutations granted accelerated approval in 2028 (de-risking): This is complicated by the requirement to have a companion diagnostic, but if the pivotal ReDiscover-2 study is "stopped early" for the kinase mutation primary endpoint, then it could accelerate commercial launch and ramp timelines by up to 12 months.

Expected news flow

A separate research article evaluating other assets, indications, and geographies will be published soon.

Although the commercial opportunity in CDKi-experienced HR+/HER2- breast cancer is the most important and certain for investors in August 2025, other identifiable updates are on the horizon.

For example, investors should expect the Fabry disease program to be outlicensed (if it isn't terminated) as it falls outside the company's core focus in oncology. A small to moderate upfront payment could offset R&D expenses for expanded development of zovegalisib in CDKi-naïve settings and vascular malformations.

Margin of Safety & Conviction

Relay Therapeutics is considered a Future Compounder position with the following Conviction rating.

- 1 = High

- 2 = Above Average

- 3 = Average

- 4 = Below Average

The estimated fair valuation based on my current model is below:

- Market close August 15: $3.54 per share

- Modeled Fair Valuation: $17.68 per share

- Allocation Range: Up to 15%

Relay Therapeutics reported 172.411 million shares outstanding as of August 1, 2025. The modeled fair valuation above assumes 237.5 million shares outstanding, which is equivalent to 3% dilution per year plus a 20% dilutive public stock offering.

Further Reading

- August 2025 press release announcing Q2 2025 operating results

- August 2025 regulatory filing (10-Q) detailing Q2 2025 operating results

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)