.svg)

A careful reading of first-half operating results and commercial metrics pointed to a boom or bust second half for Certara. Unfortunately, it's looking like a bust.

Bookings were on track to eclipse revenue guidance by an uncomfortable margin, which suggested sales expectations were conservative or bookings needed to be written off. The business kept bookings intact, citing "hesitancy" among customers, and instead slightly reduced annual guidance. Whereas bookings predicted full-year 2025 revenue of $445 million, Certara is now expecting $417.5 million at the midpoint.

That would represent a gap of 6.2%, which would be the highest since the third quarter of 2023. More concerning, the relationship was on its way to normalization at that time. Right now, the gap is widening once again – similar to the trend when the biotech sector entered its ongoing recession in 2022.

Certara maintains a dominant position within the field of model-informed drug development (MIDD). It remains a strong business with profits and cash flow. But investments require good businesses that are also growing, which is frustratingly out of reach.

Management appears cognizant of investor angst. The company has deployed $38.7 million for share buybacks in the first nine months of 2025. There's another $61.3 million remaining in the current program, which might be a good investment with shares at all-time lows, especially with tax-loss harvesting likely to add to the downward pressure on shares. The business is on pace to generate $80 million to $100 million in operating cash flow this year, so it could confidently exhaust its current authorization.

Of course, share buybacks would only provide temporary relief. And if growth is the key concern, then perhaps cash is best spent on more acquisitions. Or maybe not. Can the launch of Certara IQ build momentum and reinvigorate organic growth heading into 2026?

By the Numbers

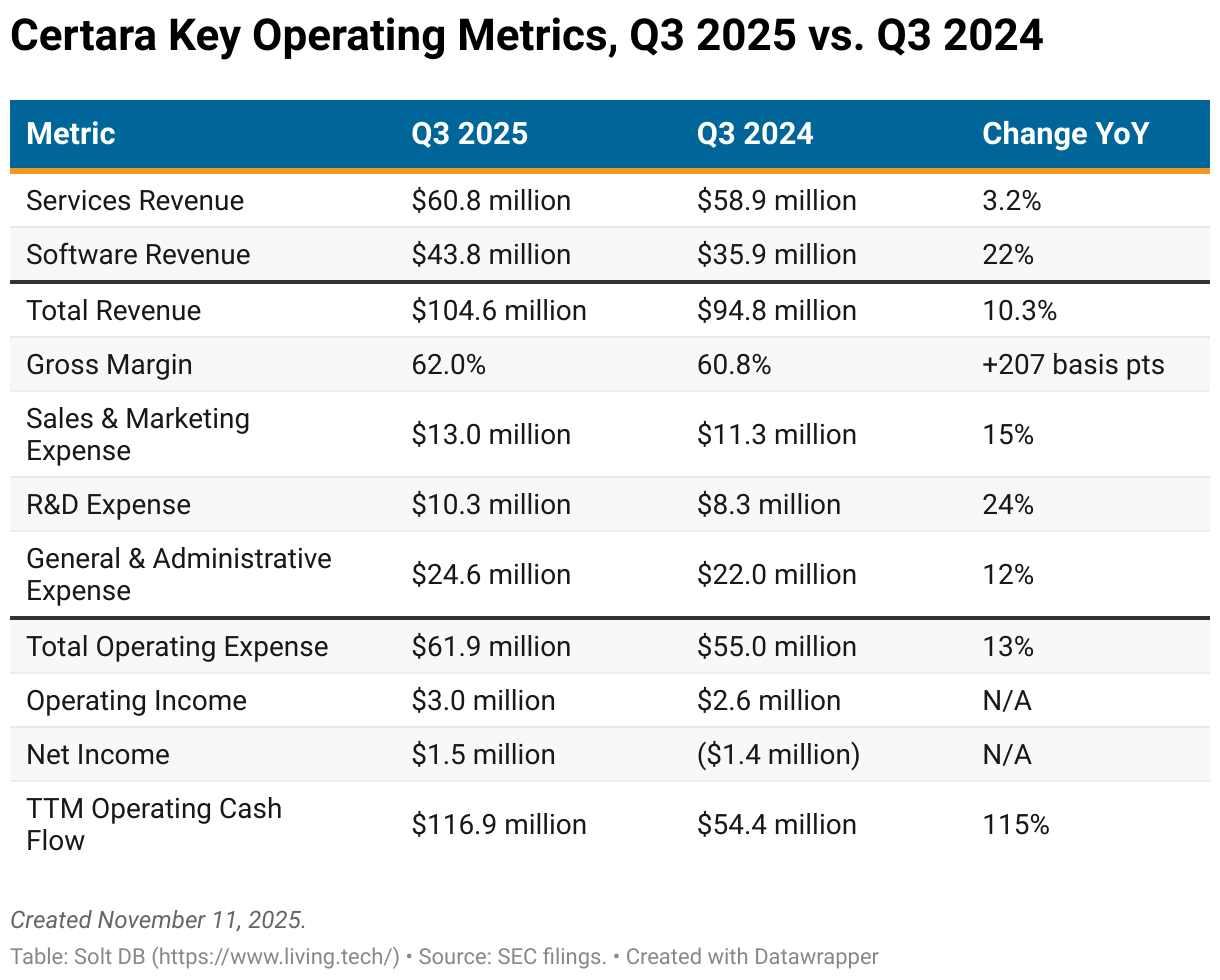

Shares of Certara took a tumble because investors are concerned about growth headwinds and the widening gap between bookings and revenue. But the business is performing well right now and in line with my current model. We don't play for participation trophies though.

The Services segment had its weakest performance in five quarters, growing revenue just 3% from the year-ago period. In a familiar trend, the Software segment put the business on its back with 22% revenue growth from the year-ago period. Overall revenue grew 10% – the fifth consecutive quarter with double-digit growth – but still behind the 15% to 20% growth rate prior to the biotech winter.

Gross margin was the third-highest ever at 62.0% and has been above 60% for five consecutive quarters – a record. Rising margins and cost discipline have delivered operating income of $26.2 million and operating cash flow of $117 million in the last 12 months. That's real-world proof that a rising share of software sales in the overall revenue mix is helping the business slightly outpace rising labor and technology costs. Not much, but it could certainly be a lot worse in the current environment.

Certara often benefits from acquired assets, which isn't surprising considering it has successfully integrated nearly two dozen acquisitions. For additional insights, it's helpful to separate contributions from existing business (referred to as "organic") and recent acquisitions (completed in the last 12 months).

The Services segment was entirely powered by existing business – no surprise there. Of the 22% year-over-year revenue growth for the Software segment, roughly 6% came from organic business and 15.6% came from Chemaxon. The software business was acquired one year ago, which means it will now fold into the existing business in future reporting periods – and contribute significantly less to growth.

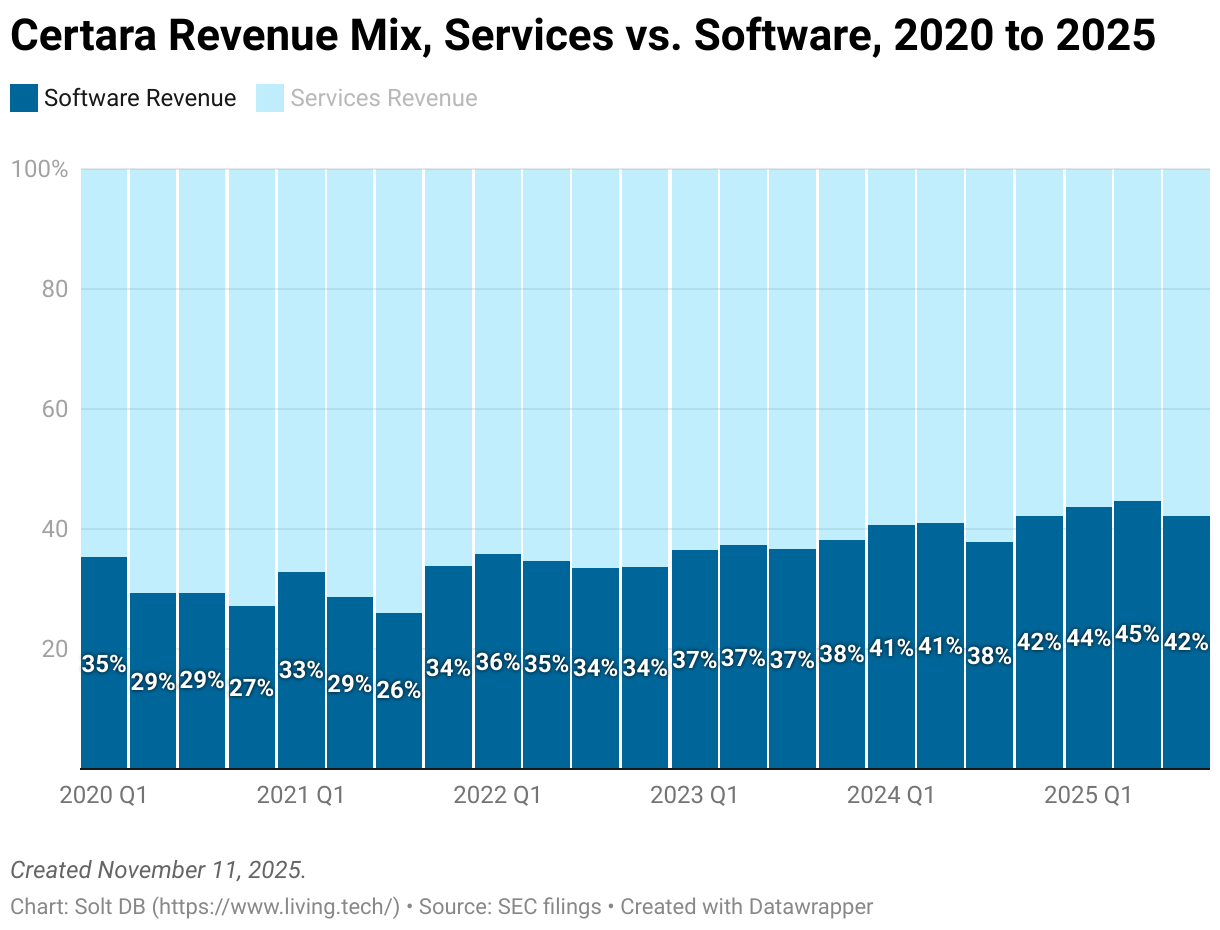

Despite healthy year-over-year growth for software, it actually fell as a share of the overall revenue mix from Q2 2025 to Q3 2025. This is entirely explained by the timing of customer renewals, which historically haven't aligned with the third quarter of any calendar year. Certara generated 41.9% of revenue from software and the remaining 58.1% from services during the quarter. This will snap back to a roughly 45% / 55% split in the final quarter of the year.

For this metric, annual periods and the longitudinal trend are more important than quarter-to-quarter changes.

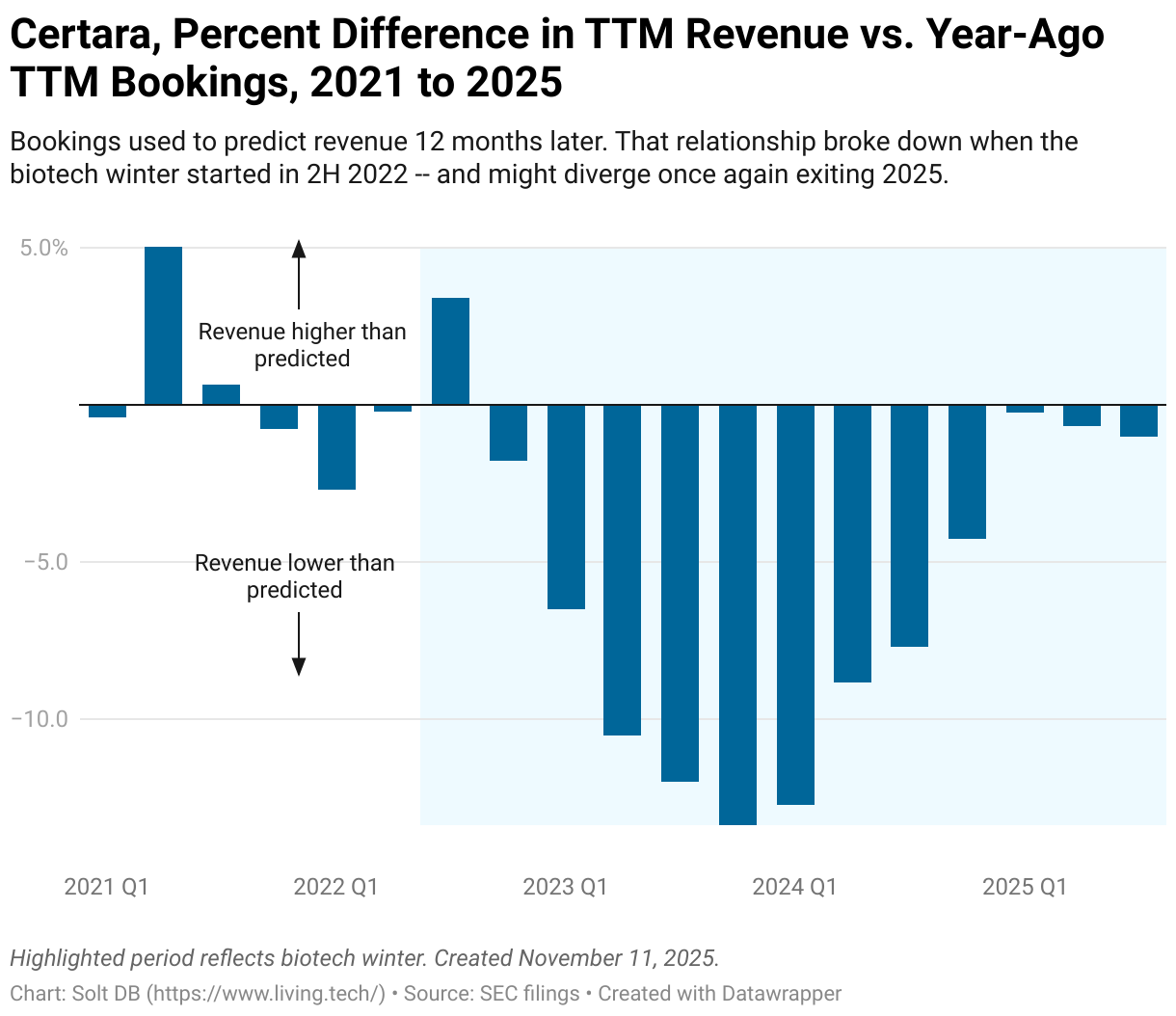

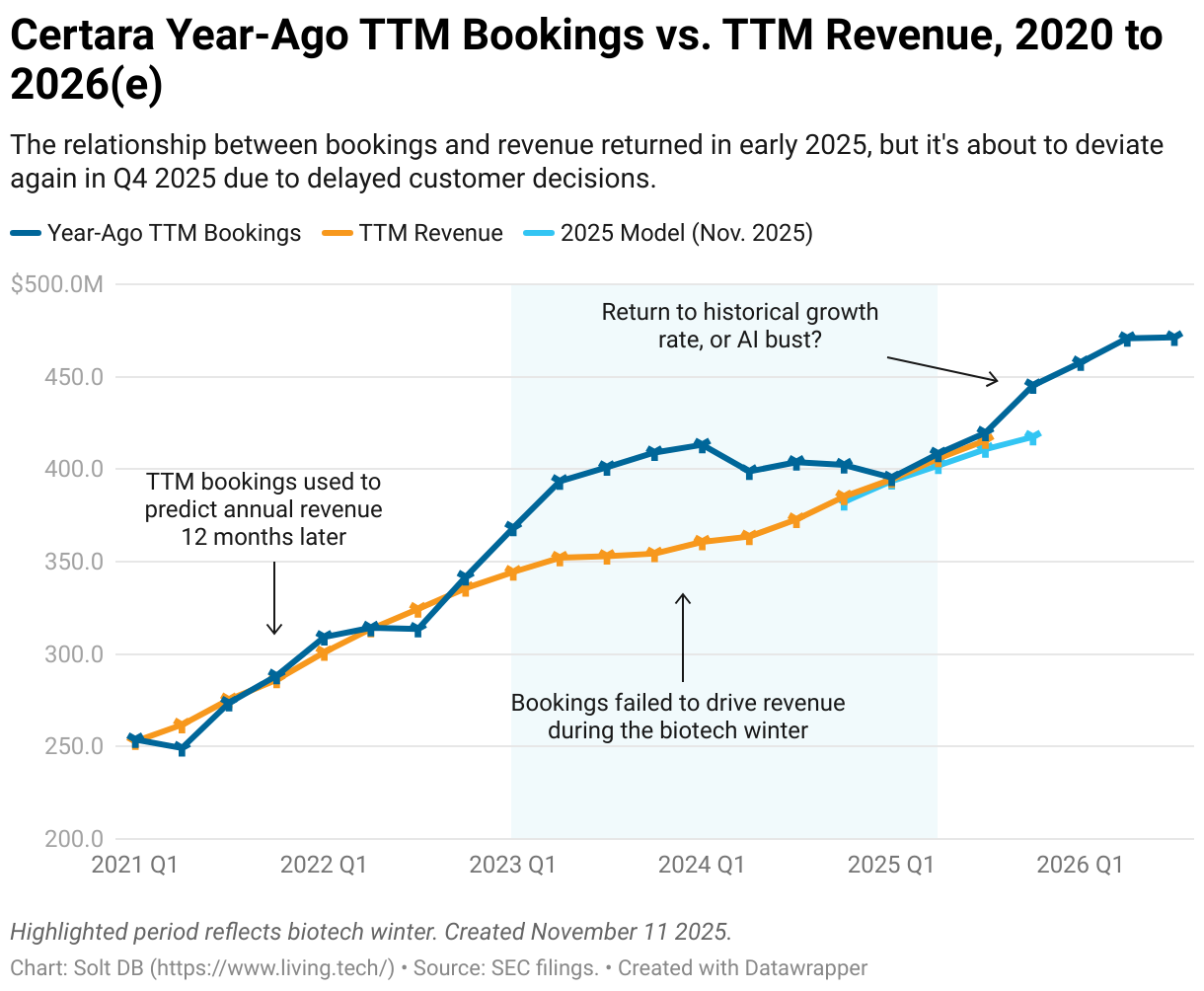

The biggest issue for Certara and investors is the relationship between bookings and revenue.

Bookings is a metric that tallies revenue likely to be generated in the next 12 months, based on customer contracts and licenses. For Certara, trailing 12-month (TTM) bookings have historically predicted TTM revenue one year later with +/- 2% accuracy – pretty darn good.

This relationship imploded when the biotech winter iced the landscape. The late-pandemic enthusiasm for soaring drug development budgets quickly evaporated when central banks began raising interest rates in 2022. As a result, the biosimulation leader had to contend with customers reneging on year-ago promises to spend more. That led to a record divergence between bookings and revenue in 2023 and 2024.

The correlation has recovered in 2025. The gap between bookings and revenue hasn't exceeded 1% in any quarter. At the end of September 2025, TTM revenue was $416 million, roughly in line with the $420 million predicted by bookings one year ago.

The punch in the face happens when investors look to the future. Largely driven by the bookings added from the Chemaxon acquisition last year, bookings predicted full-year 2025 revenue of $445 million. Management has refined full-year 2025 revenue guidance to a midpoint of $417.5 million though.

The gap might not close in the near term.

Bookings predict TTM revenue of $471 million by the end of September 2026, which would translate to growth of roughly 13% from the year-ago period. That's not impossible – TTM revenue grew 11.4% in the same period when looking at 2024 vs. 2025 – but customer hesitancy raises concerns about the predictive value of bookings going forward.

Bookings are supposed to predict revenue that's likely to be achieved in the next 12 months, but there are signs that window might be stretching to 15 or 18 months.

On the surface, the trend in forward-looking bookings appears similar to the beginning of the biotech winter in 2022. There are reasons that the future won't repeat the recent past, especially considering the sector is in a different part of the business cycle. Customer R&D budgets might not grow very much in 2026, but in 2022 and 2023 they were falling off a cliff. That's not happening right now.

Instead, Certara's biggest headwind appears to be its reliance on acquisitions for growth. That's not usually a bad thing within the highly-fragmented MIDD landscape. But the two most recent acquisitions – Applied BioMath and Chemaxon – were relatively large and took longer to integrate.

Additionally, valuations for MIDD startups are somewhat elevated due to the AI bubble. That limits the ROI for acquisitions, which puts management in a difficult spot. Does it overpay to keep growth humming along? Or should it buy back shares and wait for valuations to normalize? It appears to be leaning into the latter, which might be the proper long-term move. However, that comes at the expense of near-term growth.

Services bookings declined 9% in Q3 2025 compared to the year-ago tally, while Software bookings excluding Chemaxon increased only 5%. These suggest a growth crunch could be on the way in the second half of 2026 or early 2027 without an acquisition.

Will Certara IQ Save the Day?

Certara launched Certara IQ in October 2025. It's one of the most important developments in the coverage ecosystem in the last two years. I'll have a dedicated research note to walkthrough its importance.

Certara IQ is the world's first integrated software platform for quantitative systems pharmacology (QSP), or modeling approaches for optimizing various decisions in drug discovery and drug development. This is how Relay Therapeutics gets such robust data from phase 1/2 studies. It runs large early studies for a company of its size, but it amplifies the value of each data point and decision with QSP.

What are some practical applications? QSP can be used to:

- determine or discover combination therapies for properly treating a disease or tumor, including repurposing existing drugs for new indications

- optimize dosing cohorts for phase 1/2 studies to ensure a drug candidate's maximum efficacy potential is realized while minimizing adverse events

- optimize patient populations across cohorts for phase 2, phase 3, and phase 4 studies to maximize label claims

Molecules developed with QSP have a higher probability of success from the day they enter clinical trials, take less time to generate meaningful data, and can generate revenue more quickly with less investment.

Certara IQ is important because it unifies computational tools within the same platform for the first time. Despite the value of QSP, most projects today are bespoke. Models need to be built and rebuilt for each new molecule. The new software suite could fundamentally change that paradigm – and it's true potential might only be realized because of the Chemaxon acquisition last year.

Importantly, Certara offers both software and services, as not every customer can implement MIDD projects on their own, while those that can still often want third-party experts to provide oversight as insurance for major investments in internal assets. The company's Services segment is already beginning to implement Certara IQ for customer projects, which suggests the software platform could also provide a tailwind for the lagging and cost-burdened segment.

There's also promising potential to integrate the platform with global regulatory agencies to accelerate clearance of clinical trial designs and eventual approvals. Becoming an embedded tool for global drug development could create a meaningful, long-term growth opportunity. Still early days, but exciting potential for biosimulation to finally go mainstream.

Here's a teaser with QR codes to much longer, much nerdier presentations of case studies in bispecific antibodies and immuno-oncology.

News Flow & Modeling Insights

(Refined lower.)

Third quarter earnings season sits at a crucial place on the calendar. These fiscal updates occur in late October or early November, which means management teams have final data for the first nine months of the year and visibility into trends through at least the first 10 months.

That also makes refinements to full-year guidance hurt or help significantly more, as there's less time for analysts to update models or expectations, especially since updates this late in the calendar year impact the modeled trajectories for the following calendar year.

That helps to explain why shares went cliff diving after the Q3 2025 update. Management's revised full-year 2025 revenue guidance suggests Q4 2025 performance will be very weak – sharply deviating from expectations just days prior to the call. Growth rates for 2026 suddenly look less rosy, too.

Given the uncertain environment and management's conservative refinement, the current model has been pegged to the midpoint of guidance. Certara IQ has the potential to provide a tailwind exiting 2025, but I'll let execution and real-world customer decisions drive that.

The current model assumes the following full-year 2025 operating metrics:

- Full-year 2025 revenue grows 8.3% to $417.495 million (vs. 10.7% and $426.490 million previously). Company guidance expects a midpoint of $417.5 million (vs. $420 million previously). This includes $102.305 million in Q4 2025 revenue, representing year-over-year growth of 2%.

- Services revenue increases roughly 2.3% to $234.851 million (vs. 4.5% and $239.762 million previously). This includes $56.555 million in Q4 2025 revenue, representing a year-over-year decline of 3% (vs. $61.576 million previously).

- Software revenue increases 17.3% to $182.644 million (vs. 19.9% and $186.729 million previously). This includes $45.750 million in Q4 2025 revenue, representing a year-over-year increase of 8% (vs. $50.629 million).

- The revenue mix reaches 45.1% software revenue at the end of 2025. Software revenue ended at 42.1% in 2024, 38.2% in 2023, and 33.7% in 2022.

Margin of Safety & Conviction

Certara is considered a Current Compounder position with the following Conviction rating.

- 1 = High (no change)

- 2 = Above Average

- 3 = Average

- 4 = Below Average

The estimated fair valuation based on my current model is below:

- Market close November 11: $8.58 per share

- Modeled Fair Valuation: $11.16 per share ($11.73 per share previously)

- Allocation Range: Up to 10%

Certara reported 159.273 million shares outstanding as of November 1, 2025. The modeled fair valuation above assumes no change in the number of shares outstanding through early 2026.

Further Reading

- November 2025 press release announcing Q3 2025 operating results

- November 2025 regulatory filing (10-Q) detailing Q3 2025 operating results

- October 2025 quarterly earnings preview for the Solt DB coverage ecosystem

- August 2025 research note analyzing Q2 2025 operating results

.svg)

.svg)

.svg)

.svg)

.svg)