.svg)

Despite exiting June with strong commercial momentum, investors haven't been rewarding buy-and-build technology platforms in the Solt DB coverage ecosystem.

Harmony Biosciences has the fastest-growing narcolepsy treatment and expects four phase 3 data readouts by the end of 2026. It trades at just 10x earnings. Exact Sciences set records across a dozen operating metrics in the second quarter and will soon be profitable. It sold off as investors worried about a test that won't launch until 2027.

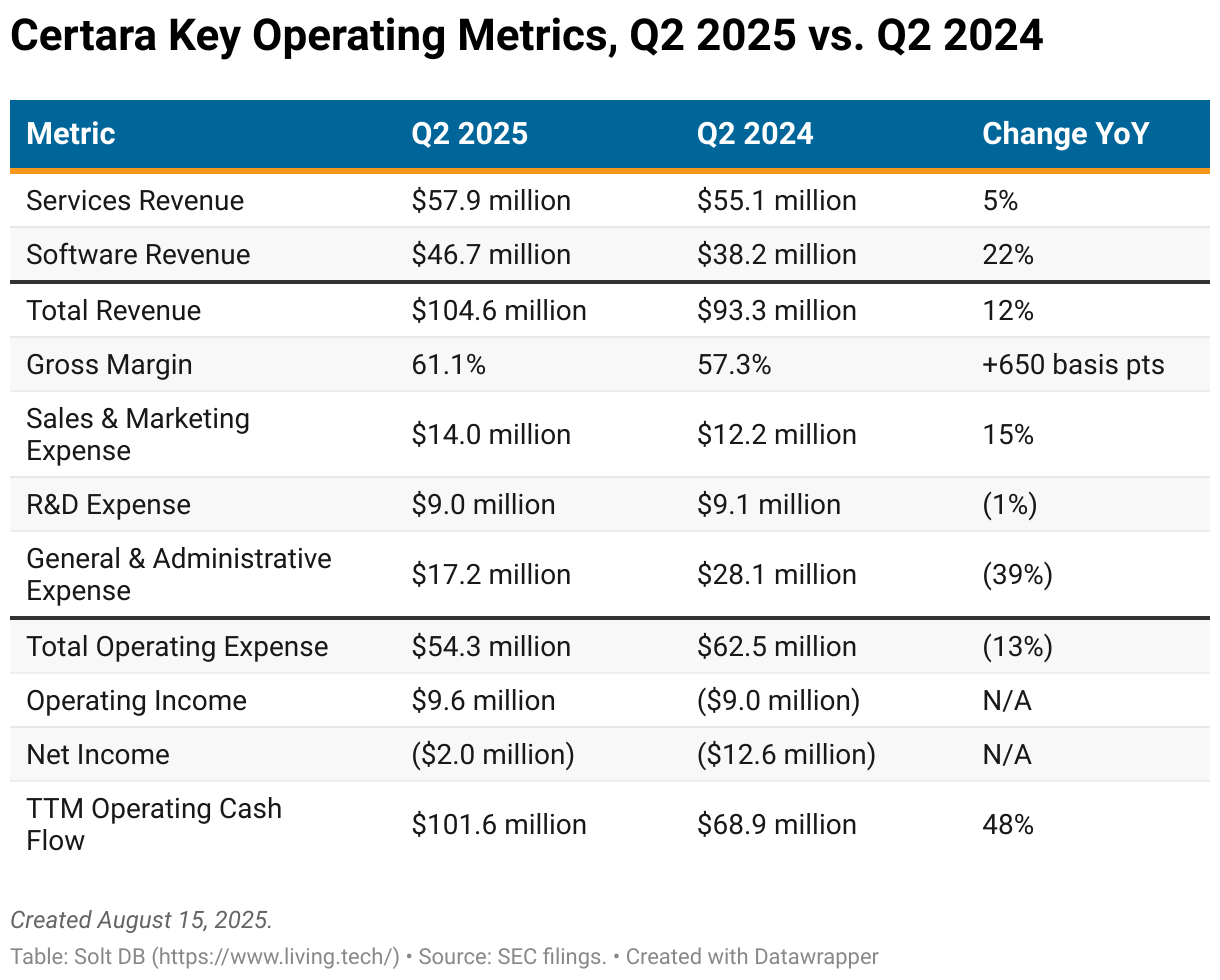

Certara just delivered the strongest quarterly performance since the biotech winter began in 2022. Although shares surged on Q2 2025 results, they sit just 7% above their pre-tariff-tantrum close.

The company has built the leading model-informed drug development (MIDD) platform through 21 acquisitions. The latest addition, biosimulation software specialist Chemaxon, was a great strategic addition.

Whereas Certara's biosimulation capabilities have primarily focused on preclinical development, Chemaxon specializes in the preceding R&D stage of drug discovery. The acquisition will add new features to the parent's existing software packages, including the D360 drug discovery engine and the flagship Simcyp PBPK Simulator.

Chemaxon will contribute full-year 2025 revenue of roughly $24 million. That'll be roughly 13% of total Software segment revenue this year, which will accelerate the overall revenue mix's shift to higher-margin software sales. The acquisition has already led to a noticeable increase in profitability. In the first three quarters of contributions, Certara's overall gross margin has increased to 61.2%, compared to 59.3% in the prior-year period. That's worth an extra $6 million of gross profit in nine months.

The 21st acquisition is also based in Hungary, which brings a customer roster more heavily concentrated in Europe. That, too, is already showing up in the data. Certara's revenue from the Europe, Middle East, and Africa (EMEA) region jumped from 19.8% to 22.4% in the same comparison period as above. It could also help to ease negative impacts from tariffs as humanity's new global trade overlord decides policy with social media posts.

Some of the numbers don't add up though.

Chemaxon's impact on bookings doesn't appear to be reflected in full-year 2025 revenue guidance. Certara is either being conservative and will meaningfully outpace guidance, or it needs to write off bookings.

By the Numbers

Certara got smacked by the biotech winter. Everyone loves a picks-and-shovels play until the whole ecosystem is in a downturn, eh? The good news is there are signs of improvement – and maybe even normalization, although I'm hesitant to make that claim.

The business objectively delivered a strong first-half performance. Revenue and margins were up, expenses were down.

Management has never focused on increasing net income, but rather operating near breakeven. That hasn't changed. But operating income has been positive for four consecutive quarters and increased in four consecutives quarters – the second-longest and longest streak in the company's history.

Operating cash flow has improved to $101 million in the last 12 months, compared to $69 million in the year-ago period. Certara is converting about 17% of revenue into operating cash flow. While healthy, that's below the >20% levels achieved in its heyday despite a higher proportion of software revenue today.

This is likely explained by permanently higher post-pandemic labor expenses, suggesting 17% to 20% might be as good as it gets for a while.

The team made progress integrating disparate software platforms, while new product launches on the horizon have intriguing potential to accelerate growth. Regulatory changes should provide a tailwind, too.

Acquisitions will continue to be attractive sources of growth, especially given the highly-fragmented landscape comprising many smaller players. Still, investors don't want Certara to be overly dependent on buyouts for growth.

There are signs Certara is striking a good balance between acquired growth and organic growth.

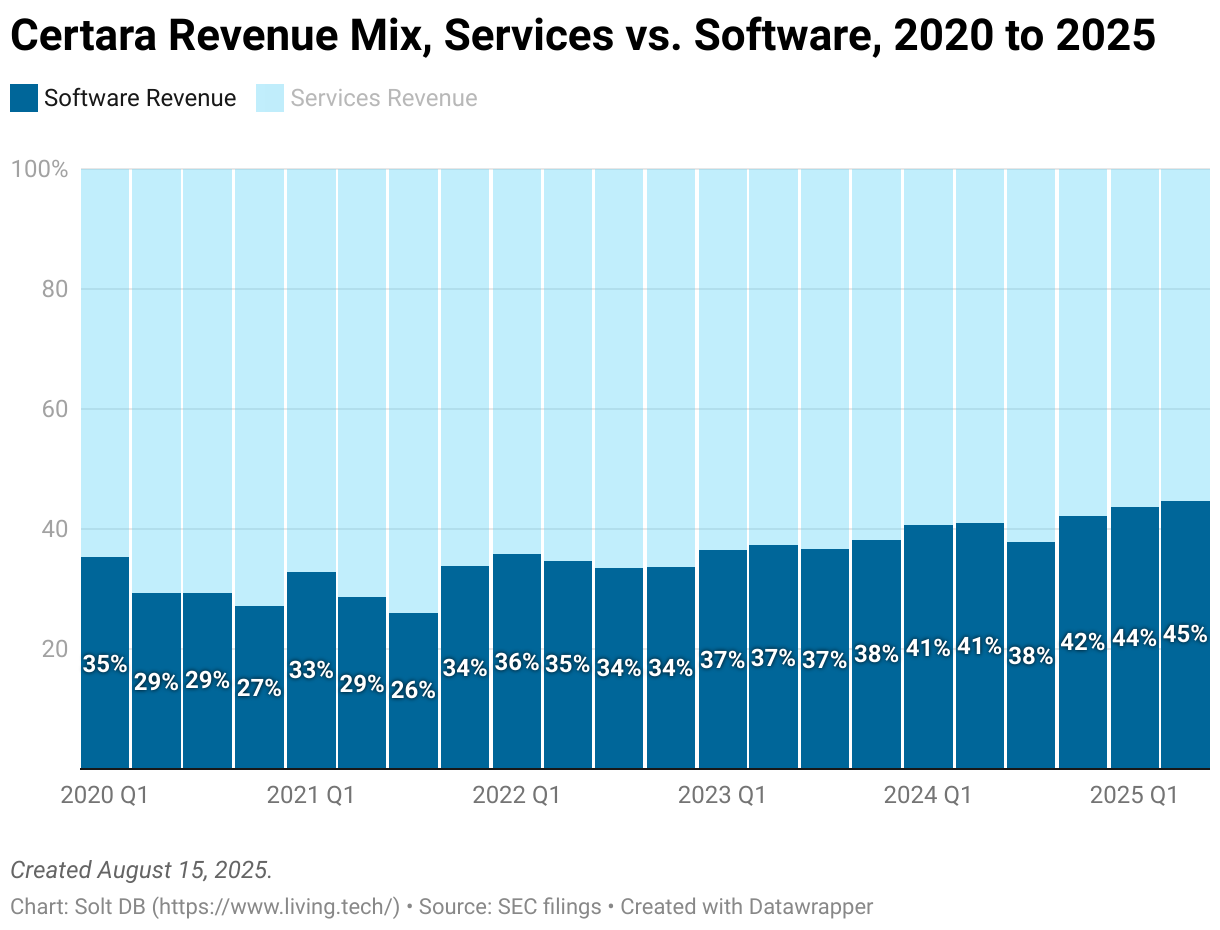

Software revenue grew 22% year over year. While Chemaxon was responsible for 13% of that (every dollar of revenue counted as growth because it didn't contribute during the year-ago period), Certara's existing software products still grew a respectable 9% in the comparison period.

The overall segment's growth led to a steady increase in the revenue mix toward software. At the end of June 2025, software revenue comprised a record 44.7% of total revenue.

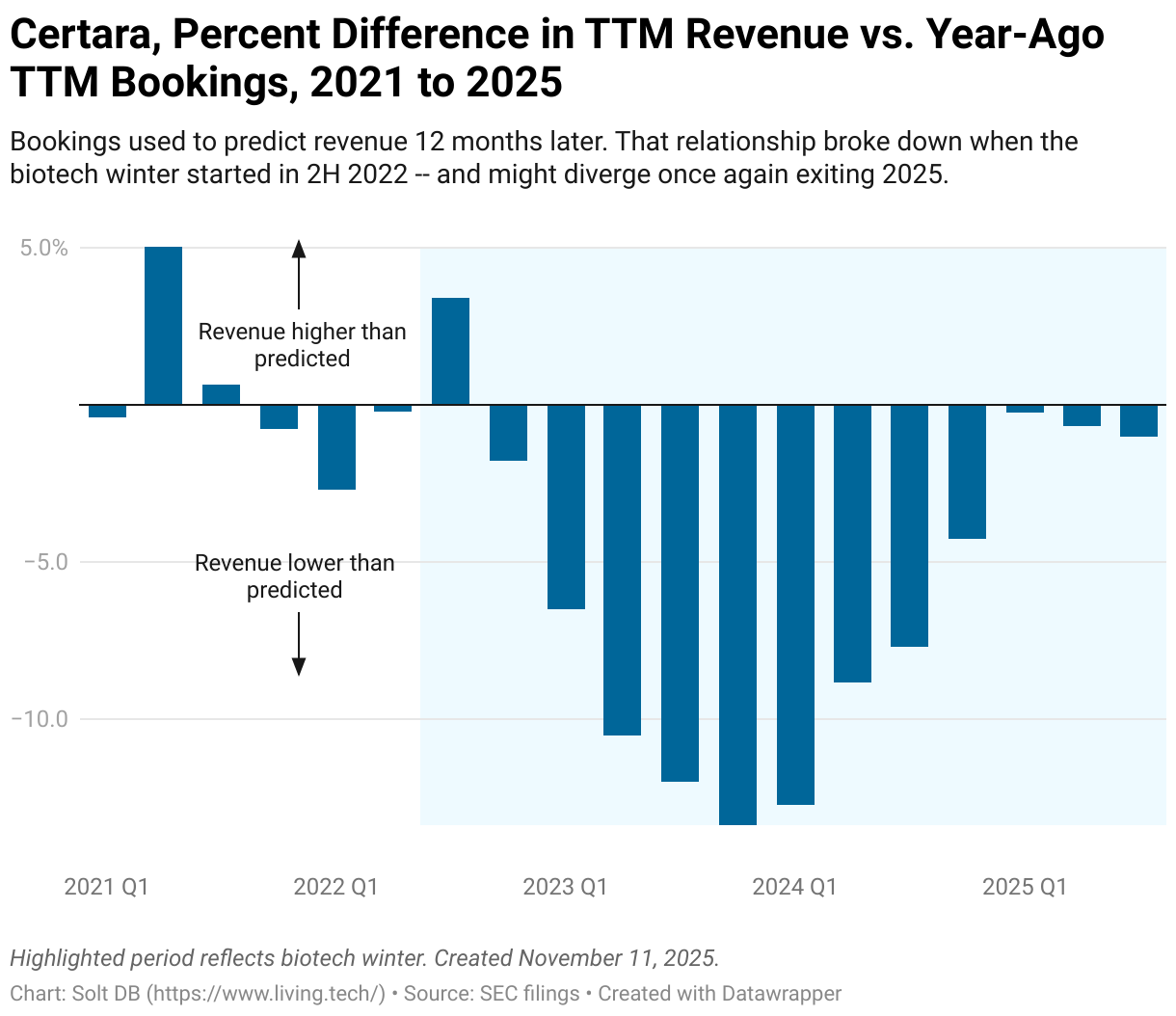

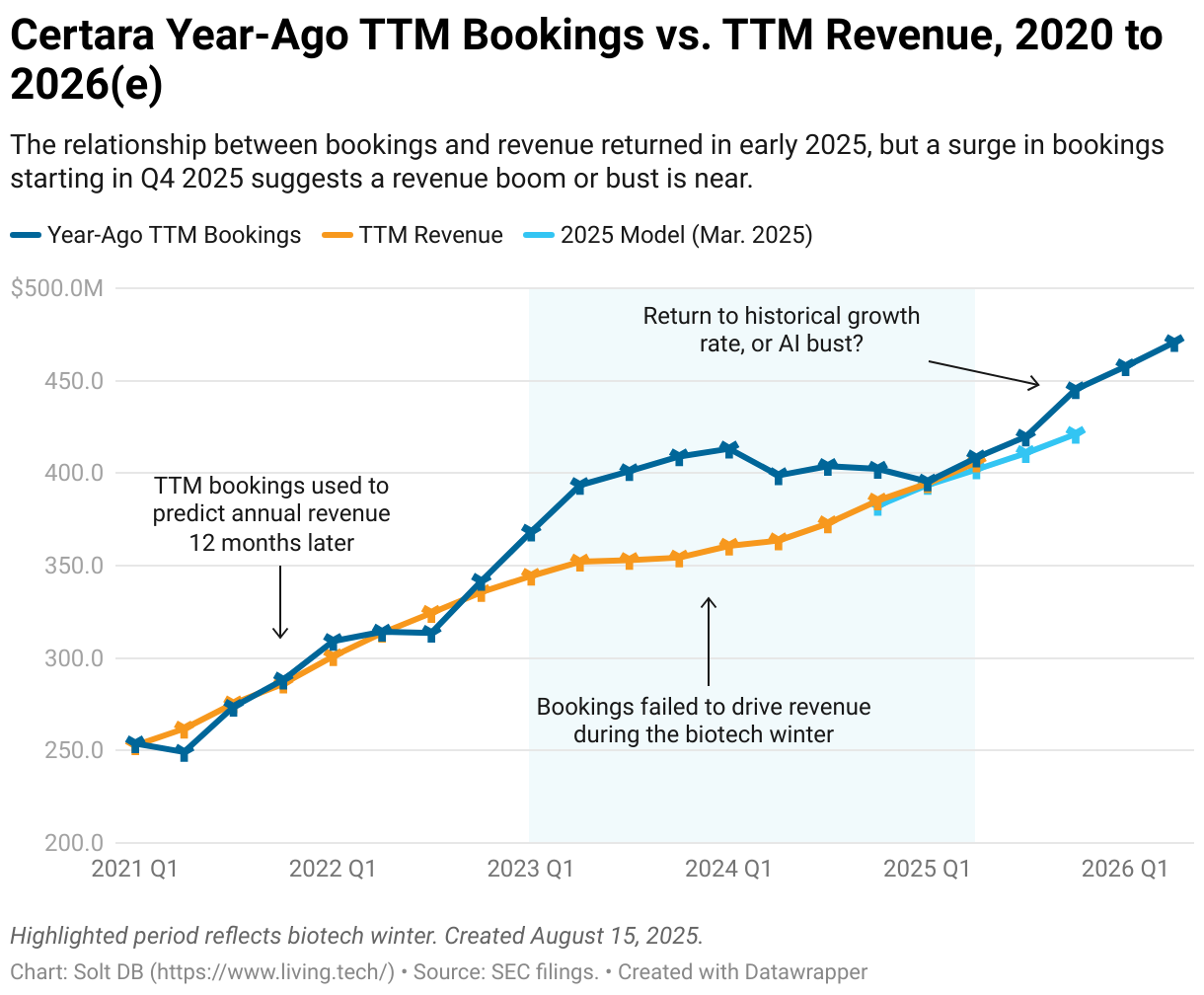

The biggest question for investors heading into the second half of the year is whether the relationship between bookings and revenue holds or breaks down.

Bookings is a metric that tallies revenue likely to be generated in the next 12 months, based on customer contracts and licenses. For Certara, trailing 12-month (TTM) bookings have historically predicted TTM revenue one year later with +/- 2% accuracy – pretty darn good.

This relationship imploded when the biotech winter iced the landscape. The late-pandemic enthusiasm for soaring drug development budgets quickly evaporated when central banks began raising interest rates in 2022. As a result, the biosimulation leader had to contend with customers reneging on year-ago promises to spend more. That led to a record divergence between bookings and revenue in 2023 and 2024.

Certara and customers adapted, somewhat painfully. But beginning in the first quarter of 2025, the relationship between bookings and revenue snapped back to its historical predictive value. Is this a durable change or an artifact in the data?

Investors will soon find out.

The Chemaxon acquisition didn't just add revenue, it added bookings too. Certara's bookings jumped when the acquisition closed in Q4 2024. Nothing unusual about that.

However, bookings predict revenue. At the end of 2024, TTM bookings were $445 million. If the historical relationship holds, then investors would expect Certara to report full-year 2025 revenue in the ballpark of $445 million.

Management maintained full-year 2025 revenue guidance with a midpoint of $420 million. That's 6% lower than bookings, a gap that's much larger than the historical trend.

This suggests the future will play out in one of three ways.

- Scenario 1: Management is being conservative with revenue guidance, which isn't a bad idea given economic and ecosystem uncertainty. Fourth-quarter 2025 revenue surges as predicted by bookings, which wouldn't be crazy, as the business would simply be returning to its historical annual growth rate of 15% to 17%. The business is currently tracking closer to bookings than my model or internal guidance.

- Scenario 2: Revenue guidance is accurate, but bookings are overestimating revenue and will need to be adjusted lower. Maybe Chemaxon had more optimistic accounting for bookings, which wouldn't be unusual for a startup trying to project strength.

- Scenario 3: Ah shit, here we go again. The sudden increase in bookings is measuring enthusiasm for AI tools in drug discovery as middle managers look to keep their job by chasing shiny objects. Similar to the excessive optimism coming out of the pandemic in 2022, perhaps there's excessive optimism for AI tools today. That could lead to a future decline in both bookings and revenue.

In my expert opinion as an analyst, I have no f*nching clue how the next two quarters will unfold. There aren't enough data available to say if the trend is durable.

I'll be watching a couple data points in the near term.

First, trends in bookings growth. Certara's organic software offerings actually saw a 1% decline in bookings in Q2 2025 compared to the year-ago period. Chemaxon added a whopping 12.5% though.

Meanwhile, services bookings jumped 15% – a record leap. Chemaxon added just 0.3% to services bookings. This could suggest customers are eager to tap Certara's expertise in a changing regulatory landscape that favors MIDD. Or, the seasonal decline every second quarter just happened to be much lower last year, making this year's bookings appear better.

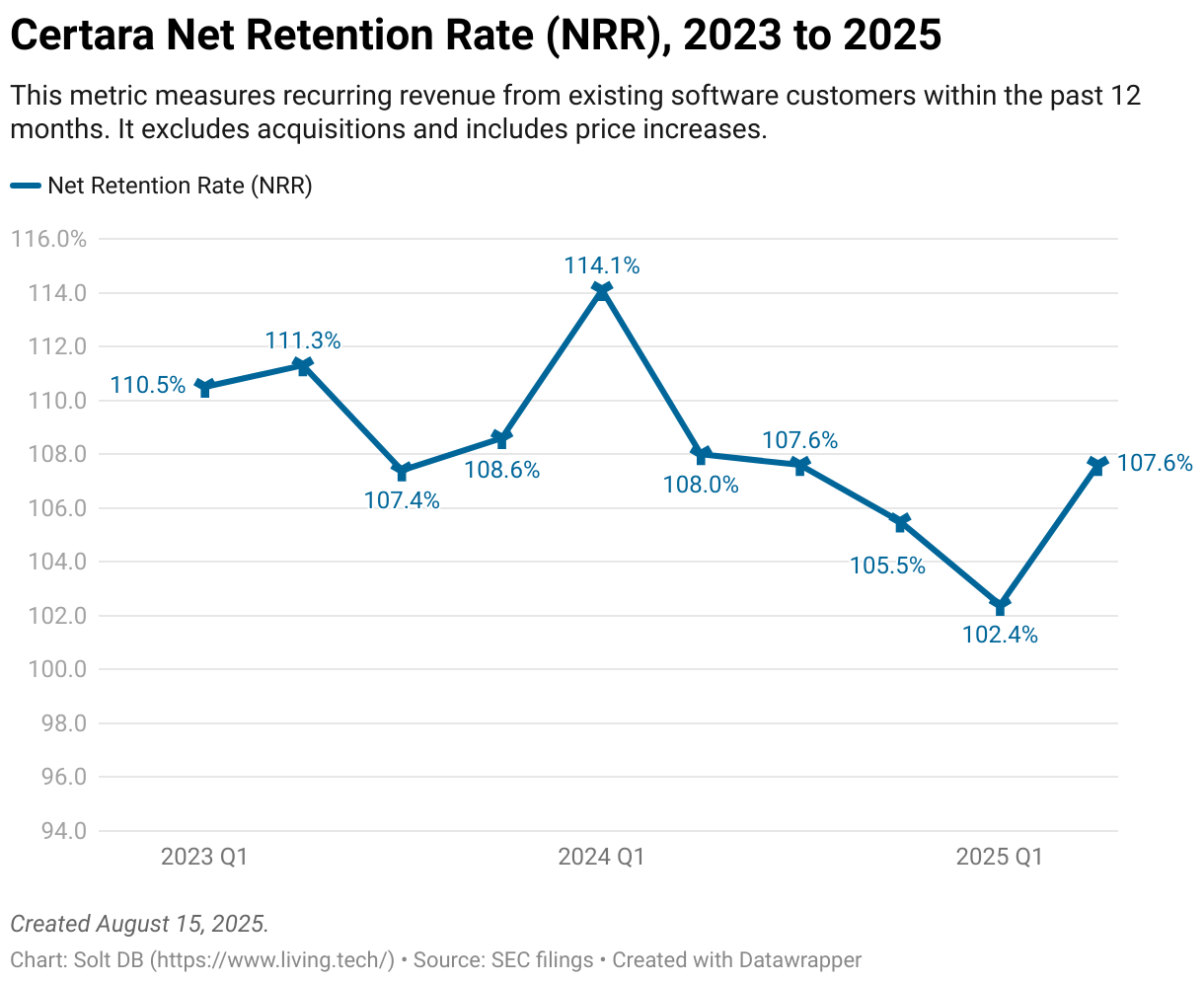

Second, net retention rate (NRR). This metric measures recurring revenue from existing software customers within the past 12 months. It excludes acquisitions and includes price increases. A rate above 100% is great, while a rate below 100% signals customers are declining to renew. The biosimulation leader shouldn't dip below 100% given its position in the ecosystem, but it will see seasonality based on the timings of renewals.

Certara didn't report NRR prior to the biotech winter, which makes it difficult to understand how the metric has evolved historically. Retention rates declined throughout 2024 and into the first quarter of 2025.

News Flow & Modeling Insights

(No change.)

There are no noteworthy changes to the model at this time, but an upcoming software launch could accelerate growth in 2026.

Certara is the global leader in quantitative systems pharmacology (QSP), which combines experimental and computational data to make important go/no-go decisions in drug discovery and drug development. The company's QSP services provide human experts that help manage and interpret nerdy data in the context of discovery, development, and regulatory review.

In the second half of 2025, the company expects to launch CertaraIQ, an integrated QSP software platform. It will combine the company's modeling tools for a growing list of therapeutic modalities, including bispecific and trispecific antibodies, protein degraders, and antibody drug conjugates (ADCs).

CertaraIQ has the potential to return the business to double-digit growth for years to come starting in 2026.

The current model assumes the following full-year 2025 operating metrics:

- Full-year 2025 revenue of $426.490 million (vs. $421.142 million previously), up 10.7% from 2024. Company guidance expects a midpoint of $420 million.

- Services revenue increases roughly 4.5% to $239.762 million (vs. $236.373 million previously). Software revenue grows 19.9% to $186.729 million (vs. $184.769 million previously).

- The revenue mix reaches 45.1% software revenue at the end of 2025. Software revenue ended at 42.1% in 2024, 38.2% in 2023, and 33.7% in 2022.

- Diluted earnings per share (EPS) of $0.46 (no change), up one penny from $0.45 in 2024. Company guidance expects a range of $0.42 to $0.46 per share in diluted EPS.

Margin of Safety & Conviction

Certara is considered a Current Compounder position with the following Conviction rating.

- 1 = High

- 2 = Above Average

- 3 = Average

- 4 = Below Average

The estimated fair valuation based on my current model is below:

- Market close August 14: $10.97 per share

- Modeled Fair Valuation: $11.73 per share

- Allocation Range: Up to 10%

Certara reported 160.624 million shares outstanding as of August 1, 2025. The modeled fair valuation above assumes 162.230 million shares outstanding, which is equivalent to 1% dilution.

The remaining $75 million on the share repurchase program is not factored into my current model.

Further Reading

- August 2025 press release announcing Q2 2025 operating results

- August 2025 regulatory filing (10-Q) detailing Q2 2025 operating results

- March 2025 research note analyzing Q1 2025 operating results

.svg)

.svg)

.svg)

.svg)

.svg)