.svg)

Market downturns can be a great time for industry leaders to consolidate a fragmented competitive landscape. Certara is taking advantage of profitable and cash flow positive operations to do just that.

The biosimulation leader announced the acquisition of Applied BioMath for an undisclosed amount. The smaller competitor is a leader in biosimulation tools for biologics drug development, including fast-growing therapeutic modalities such as antibody-drug conjugates (ADCs) and the full gamut of genetic medicines. In fact, it was beginning to snag important customers such as Sanofi and Xencor. Its offerings in mRNA lipid nanoparticle development were beginning to turn heads as well.

Certara's seventh acquisition since 2020 removes the emerging threat – and turns it into an advantage by creating the industry's largest dose optimization software suite. But the addition to the tech stack won't provide much relief from continuing headwinds in 2024.

How Will the Applied BioMath Acquisition Impact Certara?

It won't. Well, not anytime soon.

No financial details about the acquisition were announced. Shareholders don't know the acquisition price, terms, or how much revenue might be added in 2024. That's a bit frustrating, although common for acquisitions of smaller companies.

Intangibles – the people (technical know-how), technology platform (uniquely focused on biologics), and customer relationships (within biopharma) – were the key to the transaction. That's great for shareholders in the medium and long term.

Applied BioMath was a leading provider of quantitative systems pharmacology (QSP) software and services. QSP is used to optimize drug dosing ("quantitative") in clinical trials. It combines computational and experimental data to model groups of tissues ("systems"), including how they respond to exposure to a new drug compound ("pharmacology"). That information is then used to balance dosing levels with predicted side effects to create an effective therapy with favorable tolerability.

It's nerdy stuff to be sure, but the combination makes Certara the industry's largest QSP provider from preclinical to late-stage development.

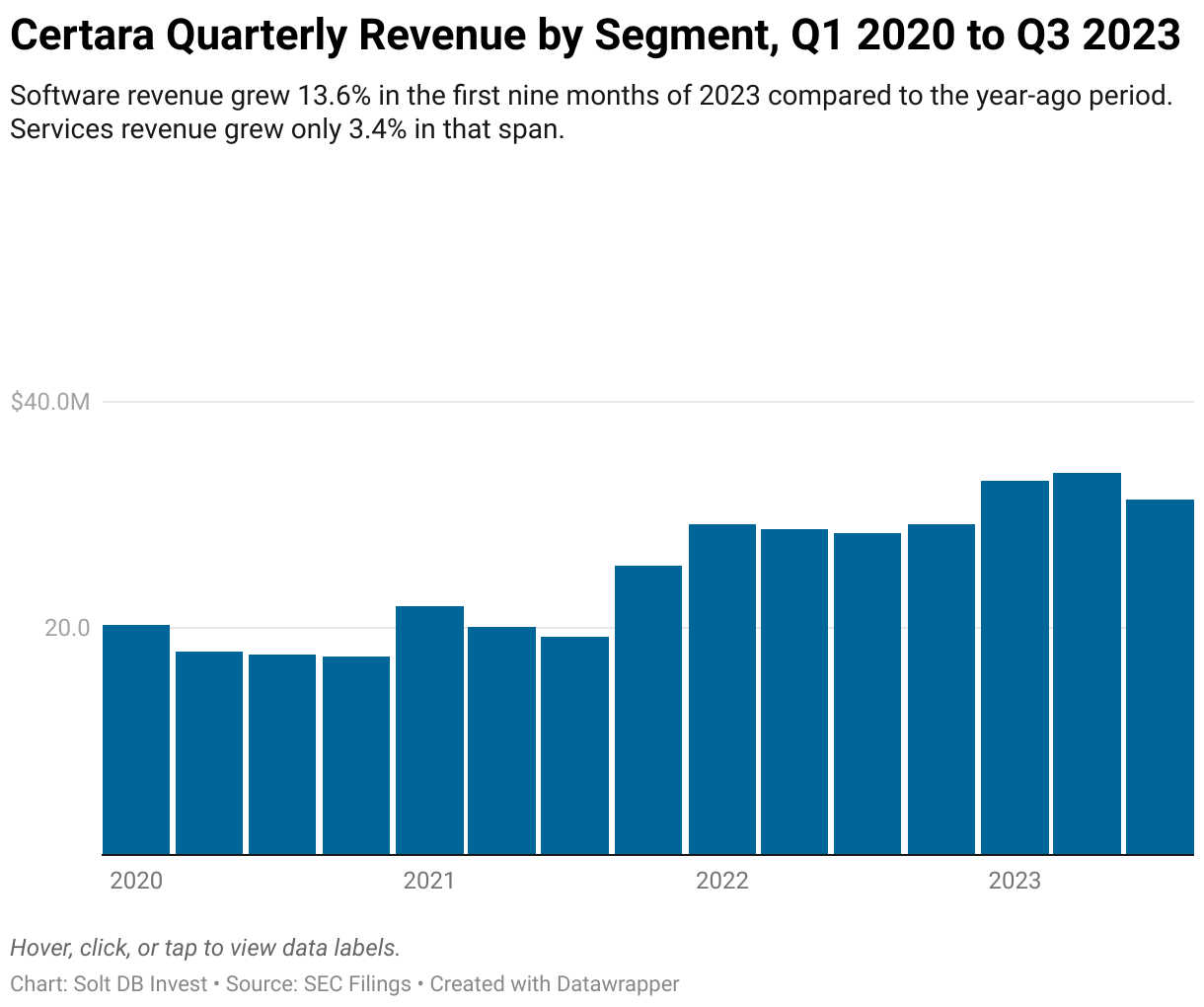

Certara will benefit from a greater focus on biosimulation software (which has higher margins than services revenue), and specifically software for the fast-growing verticals within biologics drug development. Software has been the one bright spot for the business recently, growing 13.6% in the first nine months of 2023 compared to the year-ago period. Services revenue grew only 3.4% in that span.

While Applied BioMath represents a meaningful addition to the software tech stack, the acquisition is unlikely to have an immediate impact. That means investors will need to remain seated with their seatbelts fastened in 2024.

Too Soon to Expect a Revival in 2024

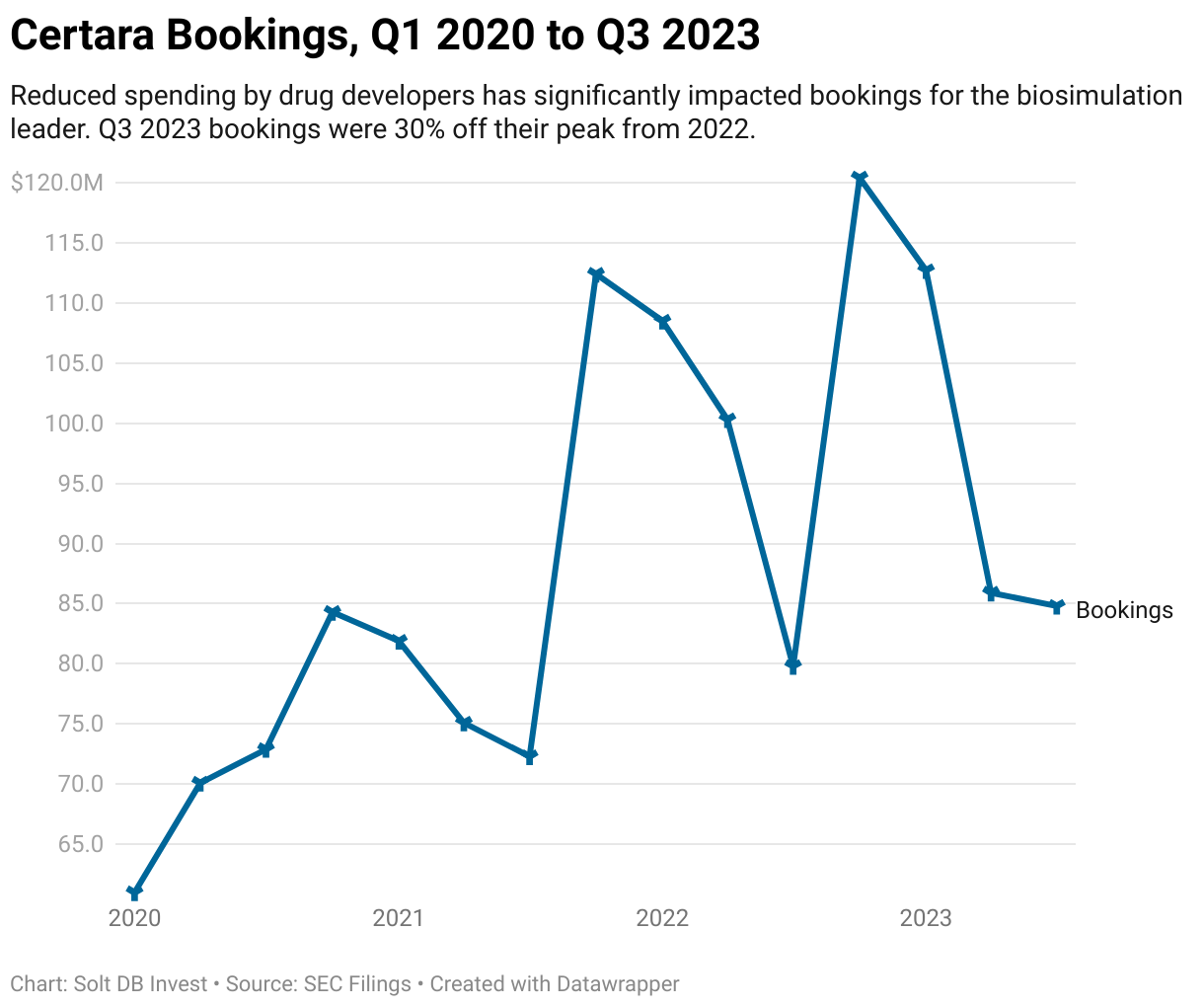

Certara faced significant headwinds in 2023 as drug developers reduced spending while recalibrating to higher interest rates. This is perfectly captured by the deterioration of gross margins and bookings for the biosimulation leader.

Software revenue represented 36.8% of total revenue in the first nine months of 2023, up from 34.7% in 2022 and 29.1% in 2021 on the same basis. Investors might expect the beneficial shift in revenue mix to drag overall gross margin higher, but the opposite happened. Strong growth from higher-margin software revenue surprisingly wasn't enough to offset weakness for biosimulation services, which were negatively impacted by higher labor costs and stagnating revenue.

Unfortunately, the sellers of picks and shovels won't see much relief in 2024 – that's when drug developers expect to realize the full effect of cost-cutting measures taken this year. It's tempting to think biosimulation tools will become more attractive in the current environment, especially if software can help drug developers accomplish more with a lower headcount. However, there's no indication of that happening so far given the trend in bookings.

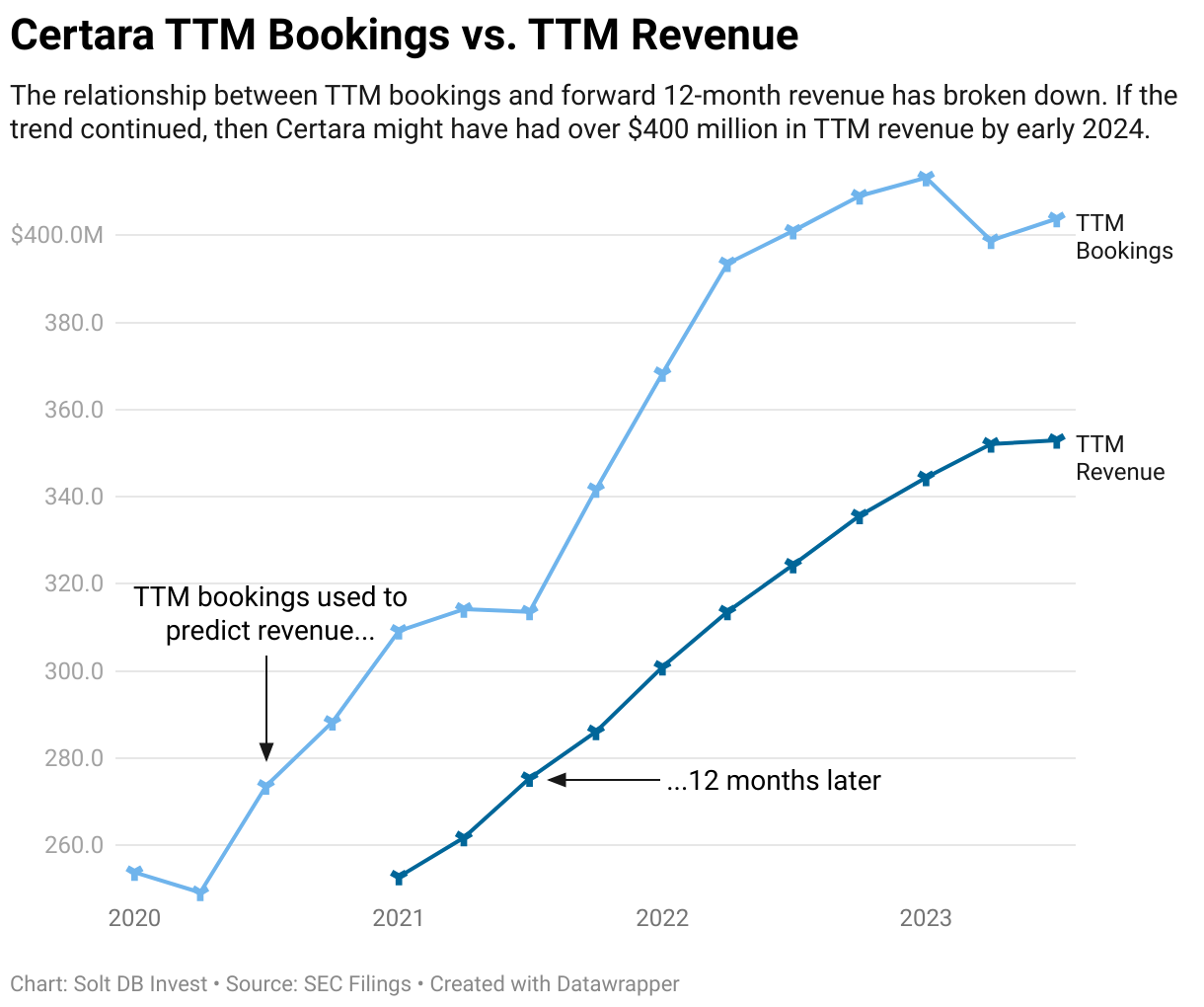

Certara's bookings on a trailing 12-month (TTM) basis have barely budged from the second quarter of 2022. And although management acknowledged quarterly bookings may have stabilized in the third quarter of 2023, they're still down nearly 30% from their peak.

Forecast & Modeling Insights

(Reduced 2024 model.)

Certara has reduced full-year 2023 revenue guidance throughout the year, but Solt DB Invest never updated its model. Therefore, this update has less to do with recent events and more to do with finally accounting for weakness experienced throughout 2023.

The midpoint of full-year 2023 guidance would represent growth of just 5% compared to 2022. That's down markedly from an average annual growth rate of 17.2% in the previous three years. Solt DB Invest expects the growth rate to sink further in 2024.

It all comes down to bookings.

Certara reported $84.8 million and $404 million, respectively, in quarterly bookings and TTM bookings at the end of September 2023. Although bookings are defined as revenue that's expected to be recognized in the next 12 months, the amount of revenue recognized is also a function of how many customers renew contracts and how many bookings were added from acquisitions. The latter is a bit murkier.

Renewal rates remain healthy, but the relationship between bookings and forward 12-month revenue has broken down since the Pinnacle 21 acquisition. The timing also aligns with the beginning of the biotech downturn in early 2022, which makes it difficult to understand the weight of each factor driving the trend.

Nonetheless, Solt DB Invest expects full-year 2024 revenue of roughly $360.8 million, representing year-over-year growth of just 2.4%. That assumes quarterly bookings rise above $90 million in the fourth quarter of 2023.

Investors can watch the trend in bookings in the next several quarters for signals of a potential return to revenue growth in 2025. Additionally, a more favorable revenue mix that increasingly leans on high-margin software is the single-most important trend for the long-term strength of the business, but it'll take time to move the needle.

The deviation from the previously-attractive growth trajectory is disappointing, but it's important to remember Certara remains solidly profitable and continues to generate cash from operations. There are still better investment opportunities elsewhere -- for now.

Margin of Safety & Allocation

Certara is considered an Anchor position. The current modeled fair valuation for the company based on our 2023 model is below:

- Market close December 14: $16.93 per share

- Modeled Fair Valuation: $10.50 per share

- Allocation Range: Up to 5%

Certara reported 159.845 million shares outstanding as of November 1, 2023. The modeled fair valuation above assumes 161.443 million shares outstanding, which is equivalent to 1% dilution.

Further Reading

- December 2023 press release announcing acquisition of Applied BioMath

- November 2023 press release announcing third-quarter 2023 operating results

- November 2023 regulatory filing (10-Q) detailing third-quarter 2023 operating results

.svg)

.svg)

.svg)

.svg)

.svg)