.svg)

This month I'm introducing the Member Digest, which is intended to recap the prior month's refinements, call attention to timely trading and investing ideas, and evaluate the coverage ecosystem through the lens of a specific topic.

For the first month, let's explore a topic many members have asked about: What's the acquisition potential of companies in the coverage ecosystem?

Ranking Acquisition Potential

Inspired by a Discord thread from December 2023.

For acquisitions right now, it's important to understand the context of the times. There's a huge patent cliff coming in 2026 to 2030. Most of today's bestselling drugs will lose exclusivity by then. Large pharma will need to start replacing that revenue with new revenue and/or late-stage assets. Like, now.

There are a few therapeutic areas (type of disease) and therapeutics modalities (type of drug) that will be prioritized:

- Therapeutic Areas: Autoimmune, neuroscience (there's been a looong investment drought by pharma so that amplifies the need), solid tumors, and obesity

- Therapeutic Modalities: Antibody drug conjugates (ADCs), bispecific antibodies, radiopharmaceuticals (especially this in the next few years), nucleic acids, covalent small molecules, and in vivo cell therapies

Companies that are most likely to be acquired check a few boxes as well:

- Current market valuation of $3 billion to $10 billion (enabling buyout of $6 billion to $15 billion range)

- Well-designed clinical trials giving deep look at development and the commercial potential of assets

- Mid or late-stage assets

With the criteria laid out, let's rank the acquisition potential of the entire coverage ecosystem (28 biotech stocks) with four categories:

- Almost Guaranteed

- Above Average

- Average

- Below Average

- In Case of Emergency

Almost Guaranteed

These companies are very likely to be acquired in the next few years. Presented in alphabetical order.

Arvinas

Arvinas is likely to become the first company to commercialize a protein degrader. The lead drug candidate is partnered with Pfizer, the next-most advanced pipeline asset was just partnered with Novartis, it has clear and convincing data for both, and the company is now evaluating protein degraders that cross the blood-brain barrier for neuroscience applications. The recent slide in shares makes this an intriguing addition to portfolios, especially given the significant acquisition potential. I'd target at least $55 per share without any additional data readouts.

Day One Biopharmaceuticals

Day One Biopharmaceuticals earned its first FDA approval one week early for Ojemda, a treatment for pediatric brain tumors. The market is relatively small, even if plans to expand into adult populations are successful. But the ability to soon self-fund development of a more ambitious pipeline comprising a MEK 1/2 inhibitor and VRK1 inhibitor (both cancer targets) make this an intriguing time to be a shareholder.

Krystal Biotech

The husband-and-wife team at the helm of Krystal Biotech are almost certain to sell the company eventually. Now that Vyjuvek is launched and ramping and additional assets are finally beginning clinical trials, it would be a natural time for an acquisition. The business could be worth significantly more if it delivers in lung diseases or eye drops, but those will take time to cough up meaningful data. Shares seem a little overpriced at current levels, except if an acquisition were to occur.

MoonLake Immunotherapeutics

MoonLake Immunotherapeutics is developing really small antibody fragment drugs, called nanobodies, with an initial focus on autoimmune disorders. The timing couldn't have been better. Many drug developers are eager to develop next-generation autoimmune treatments, which boast more blockbuster drug products than all therapeutic areas aside from cardiometabolic and oncology. MoonLake just so happens to have a late-stage pipeline with clear and convincing data. It's richly valued now, but it could easily earn (or be acquired for) significantly more.

Above Average

These companies are slightly more likely to be acquired than to remain independent. Presented in alphabetical order.

Arrowhead Pharmaceuticals

It's easy to see Arrowhead Pharmaceuticals getting acquired. The drug developer wields a high probability of success technology platform, late-stage assets, partnerships, its own manufacturing facility, and emerging pipelines in five disease areas. Companies that reach similar size and maturity are typically gobbled up, especially when they have high-quality assets. Recent moves also suggest the business might be eager to remain independent and grow into an industry heavyweight.

Exscientia, Recursion Pharmaceuticals, and Relay Therapeutics

This gang of technology-enabled drug discovery companies has above average acquisition potential. I'm not sure larger pharma companies are convinced about the value proposition of AI in drug discovery, which suggests they're more likely to keep an arm's distance approach with partnerships. But this trio can de-risk those decisions with their most important assets – all targeting breast tumors as their primary market opportunity:

- Exscientia's GTAEX617 program is co-owned with Asperion. It's a CDK7 inhibitor with significant potential in the race for next-generation CDK inhibitors, which are among the most important treatments for breast cancers. This program is in phase 1/2 development and hasn't announced meaningful data yet.

- Recursion's RBM39 program inhibits a protein of the same name. Previously known as "target gamma," this unknown protein is hypothesized to deliver similar outcomes as whacking CDK12 – which has humbled every attempt due to toxicity. This is the first drug candidate built with the company's next-generation technology platform, so both the market opportunity and stakes are high.

- Relay Therapeutics is almost certain to earn FDA approval for lirafugratinib (RLY-4008), but an asymmetric inflection point for investors hinges on the development of RLY-2608. The PI3K-alpha inhibitor will have important data from two separate combinations in the second half of 2024.

Average

These companies are no more likely to be acquired than to remain independent. Presented in alphabetical order.

AVITA Medical

There's a future where AVITA Medical and Vericel merge to build complimentary portfolios across burns, sports injuries, and vitiligo, but it would behoove AVITA Medical to execute and build a significantly higher market valuation first.

Centessa Pharmaceuticals

When I spoke with CEO Dr. Saurabh Saha, I got the sense Centessa Pharmaceuticals would eagerly entertain acquisition offers once it built something. It's still in the "building something" phase. The drug developer has ruthlessly culled pipeline programs since launch – a smart move – but that's left it with early-stage assets mostly lacking meaningful data.

Certara

The price certainly doesn't seem right for an acquisition, which likely keeps potential suitors at bay. Otherwise, Certara is relatively attractive for the right company. The business is profitable and well positioned for biosimulation's widespread adoption in the coming years. It might be a labor-intensive business, but it's one that generates cash.

Oxford Nanopore

The management team can be "prickly," but Oxford Nanopore still has average acquisition potential. A choppier-than-expected growth trajectory appears to be certain in 2024 at least, which could push down the valuation enough for management to consider a splash transaction.

Twist Bioscience

CEO Emily Leproust has the business trending in the right direction. Operating expenses are barely growing, but a lack of investment hasn't impeded revenue growth or the ability to grow gross margin. That's leading to a swift improvement in the quality of revenue and cash outflows. The so-so acquisition potential stems from a crowded competitive landscape and lack of obvious suitors.

Below Average

The companies are unlikely to entertain buyout offers. Of course, now all three will be acquired by the end of next week. Presented in alphabetical order.

Exact Sciences

Exact Sciences has the most successful genetic test ever, one of the largest precision oncology portfolios globally, a massive R&D footprint spanning multiple continents, and is fast-approaching profitability. It would be a nightmare to acquire, especially the part about appeasing regulators. Management is much more likely to execute and reap significant gains in the stock price.

Repligen

A boring but strategic bet to focus on bioprocess tools has paid off handsomely for Repligen. The former drug developer makes the filters, purification columns, and sensors needed to manufacture biologic drugs such as antibodies and cell therapies. The profitable $9 billion business is expected to generate $650 million in full-year 2024 revenue. It would take a much larger R&D inputs company to close an acquisition – or a private equity firm.

Vericel

I can see Vericel getting acquired. It has a growing burns treatment business and a large, stable foundation from its sports injury business. But the most likely suitors (larger medical device companies) might be more hesitant to wheel and deal in a high interest-rate environment.

In Case of Emergency

A handful of companies might be acquired for parts or as a rescue if things go off the rails. This ranking is purely considering acquisition potential, not necessarily the overall opportunity for investors. Presented in alphabetical order.

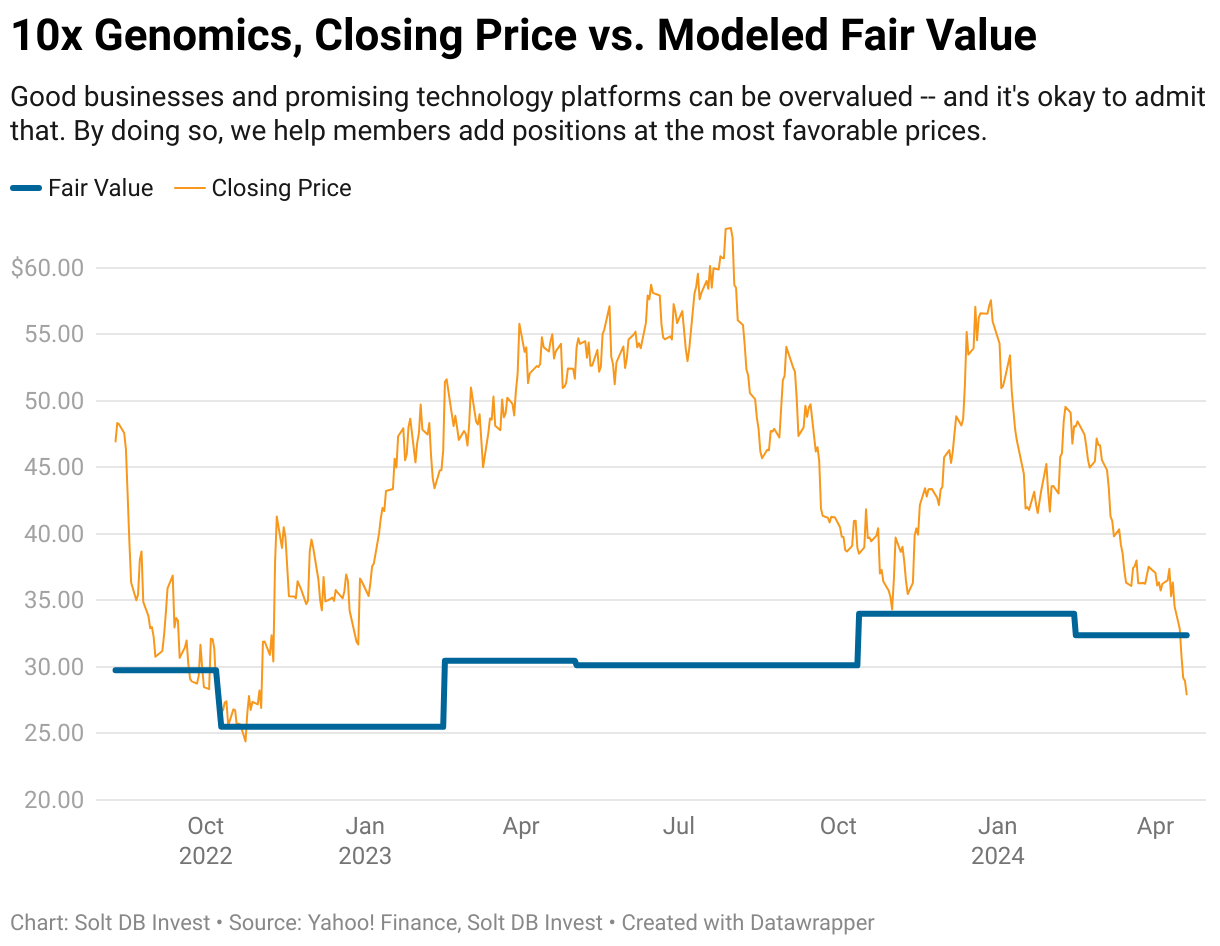

10x Genomics

10x Genomics is in relatively good shape compared to all others on this list, but there are early signs the product portfolio's recent expansion might not be going according to plan. Revenue is barely budging, gross margins are down, operating expenses are up, and cash outflows are picking up momentum. Given how broadly the company's footprint spans, it might be difficult for an acquisition to pass regulatory muster in "normal" times. Investors would rather see the company succeed.

AbCellera and Ginkgo Bioworks

AbCellera and Ginkgo Bioworks are building important technology platforms, but the current business models are challenged at best. It's difficult seeing either become a sustainable business anytime soon. Who might acquire them in the event things go horribly wrong? A deep pocketed drug developer might take a crack at either.

Bolt Threads

The company is going public through a SPAC in part because it struggled to raise another private round. Now that the public debut is delayed too, Bolt Threads might be forced to sell itself for parts or survival.

Codexis

I think Codexis could easily reclassify itself to an "Above Average" acquisition potential with execution in the next 18 months. But there's still a lot to prove commercially. If the company stumbles or the technical roadmap becomes blurry, then it might still find a suitor for its existing core business.

Cognition Therapeutics

Until and unless the company's development pipeline yields meaningful clinical results, Cognition Therapeutics is more likely to close up shop than to be acquired. Investors will get their first big data readouts in 2024 and 2025.

.png)

Coherus BioSciences

I don't think Coherus BioSciences is an attractive acquisition target. Any would-be suitor would need to take on the company's biosimilar pipeline, which would pose problems for those with their own biosimilar brands. Similarly, the acquirer would pick up rights to anti-PD-1 / L1 drug Loqtorzi, which would be untenable for the eight companies with their own PD-1 / L1 assets.

The only sensible suitor would not have a biosimilar portfolio or a PD-1 asset, but have experience commercializing oncology drugs. Eli Lilly and Takeda come to mind, but the former is busy cranking out obesity drugs and the latter is might find easier targets for its relatively small cash position.

IGM Biosciences

Poor IGM Biosciences has been beaten up by pipeline consolidation and partner break ups. It lacks meaningful clinical data to suggest its unique antibody structures are a viable therapeutic modality. Without data, this is more likely to be shut down than acquired. But with meaningful data, this could become an intriguing acquisition target for a number of large pharmas.

LanzaTech

Although LanzaTech is discussed for its carbon emission-eating microbes made with synthetic biology tools, the company generates almost all revenue from engineering services and technology licensing. It only generated $5.3 million in product revenue in all of 2023 – and at a gross margin of just 8.4%. Nonetheless, there are interesting subsidiaries and pieces of LanzaTech that could be attractive to the right players. If the U.S. government continues cracking down on biotech companies with international operations, then those divestitures could happen sooner than later.

PacBio

The hits keep coming for PacBio. The DNA sequencing company's new product platforms are off to a sluggish ramp during what was supposed to be the beginning of an epic growth trajectory. I wouldn't be surprised to see the Onso (short read) technology platform discontinued to prioritize resources for Revio (long read). Meanwhile, new data for a synthetic long read technology from Illumina suggest PacBio might face a more challenging competitive landscape than thought.

Schrodinger

Schrodinger still needs to figure out what it wants to be when it grows up. Is it a software company or a drug developer?

It wields one of the leading technology platforms for molecular dynamics simulations used throughout drug development and materials science applications, but the competitive gap is closing rapidly thanks to the proliferation of artificial intelligence tools. Before it proved the viability of the software business, the company decided to build its own drug pipeline. Now it's not quite exceeding at either. If anything, an acquisition for parts seems most likely.

Verve Therapeutics

Although CRISPR base editing pioneer Verve Therapeutics has stumbled recently, investors can be more confident in the company's second-generation drug candidate VERVE-102. You know, once it has phase 1 data in 2025. Given the pipeline focus on cardiometabolic diseases (requiring large and expensive clinical trials), an acquisition could make sense if things go well. Until the first meaningful data readout, investors can only expect a sympathy buyout.

De-Risking Events to Watch

Here's what I'm watching during May and June:

Earnings Season

It's that time of the every-three-months again – earning season. Many small-cap biotech companies provide first-quarter updates every May. Those with non-standard fiscal years provide quarterly updates, too, such as Twist Bioscience. I track the calendar and events on Discord!

Bolt Threads Goes Public... ?

Bolt Threads is an industrial biotech company developing engineered materials using genetically engineered microbes. It was one of the first companies to manufacture spider silk through fermentation. The company is now focused on commercializing B-silk, its B2B ingredient for cosmetics and personal care applications.

The industrial biotech company agreed to go public with a SPAC called Golden Arrow Acquisition Company, which was expected to close in late March. Unfortunately, it hit some snags. I've confirmed the plan for a SPAC remains in place – eventually.

TIDES USA Meeting

The TIDES Meetings are focused on nucleic acid medicines -- things based on RNA and DNA. Codexis plans on presenting world-first data at the conference. However, wording in its recent Q1 2024 earnings press release doesn't exactly instill confidence in the timing. The company says it's "in the final stages of enzymatically synthesizing a full-length" building block for RNAi therapeutics. That's great, but TIDES USA is May 14 to 17.

Although the stock isn't overvalued and missing an overpromised deadline doesn't say much for the validity of the technology platform, the data showcase at TIDES USA was supposed to kick off an epic ramp of data readouts and commercial-readiness updates for the ECO Synthesis platform. Starting off by missing a self-imposed deadline could squeeze some momentum out of the stock.

Updated Models

Models were reduced for:

- AVITA Medical

- Oxford Nanopore

- PacBio

There will be many updated and introduced models after earnings season.

Most Intriguing Ideas for May 2024

There are many ways to be active in the stock market. Solt DB Invest takes a strategy-agnostic approach to biotech investing, which requires valuation discipline and a more active style (even for long-term positions). Here are several timely ideas for members.

Long-Term Stocks

Codexis $CDXS

- The long development timeline works in favor of investors willing to be patient. If you can ignore FOMO during spikes and add when the margin of safety is favorable, and the company executes with the ECO Synthesis platform, then I don't think investors will miss with Codexis under its current fair value of $5.53 per share.

- After Q1 earnings and before the expected progress update at the TIDES USA Meeting, I'd be looking to add near (and likely under) $3 per share.

Exact Sciences $EXAS

- This is such a no brainer. Exact Sciences is one of the safest growth stocks on the market right now. Returns on money invested near the current price of $60 per share should easily wallop the S&P 500 in the next few years.

"Almost Guaranteed" Crop $ARVN $DAWN $KRYS $MLTX

- I'd bet a portfolio concentrated in the four "Almost Guaranteed" acquisition potential companies would easily outperform the S&P 500 in the next 24 to 36 months. Let's track this informal model portfolio from closing prices on May 2, 2024 into the future to see if that proves true.

Short-Term Plays

Arrowhead Pharmaceuticals $ARWR, Arvinas $ARVN

- Both Arrowhead Pharmaceuticals and Arvinas have very important de-risking events in the next 18 months. The former has a pipeline bulging with undervalued potential, while the latter is one of the most obvious acquisition candidates on the stock market.

Coherus BioSciences $CHRS

- See the recent Finch Trades for more detail.

Day One Biopharmaceuticals $DAWN

- Day One Biopharmaceuticals earned its first FDA approval one week early for Ojemda, a treatment for pediatric brain tumors. The market is relatively small, even if plans to expand into adult populations are successful. But the ability to soon self-fund development of a more ambitious pipeline comprising a MEK 1/2 inhibitor and VRK1 inhibitor (both cancer targets) make this an intriguing time to be a shareholder.

Swing Trades

10x Genomics $TXG

- I don't find 10x Genomics terribly attractive as a long-term investment, but Wall Street has historically assigned it a healthy premium. It has healthy gross margins and expects to achieve positive operating cash flow in 2024. I just don't find the valuation attractive, as I think the growth trajectory will slow significantly in the next few years. That would be a bad time to be holding onto shares.

- That said, 10x Genomics has an interesting relationship with my models. It has rarely traded below my fair value, but has always bounced back quickly when that happened. This is due to the differences in the discount rates and valuation premiums assigned to financial metrics in my model vs. those from the average Wall Street analyst.

- Members are cautioned that this relationship may not hold forever, especially with the product portfolio in flux and recent earnings. But it could be a quick way to make 10% to 20% and move on.

PacBio $PACB

- I don't find PacBio terribly attractive as a long-term investment either. You probably couldn't gift me shares to hold onto. It's reasonable to question if the business will survive the next few years.

- That said, the recent plunge in shares might be a slight overreaction in the short term. I could see this bouncing back to over $2 per share in the next few weeks or months. It might not be a bad way to make a quick 10% to 20%.

.svg)

.svg)

.svg)

.png)

.svg)

.svg)

.svg)