.svg)

Codexis the company has staked its future to its enzymatic RNAi manufacturing platform, ECO Synthesis. Codexis the business currently has essentially zero dependence on it.

Most companies invest in new growth opportunities, so that alone isn't noteworthy, but the stakes are higher considering the legacy business isn't delivering steady, predictable performance. If ECO Synthesis doesn't pan out, then Codexis is unlikely to be a good investment.

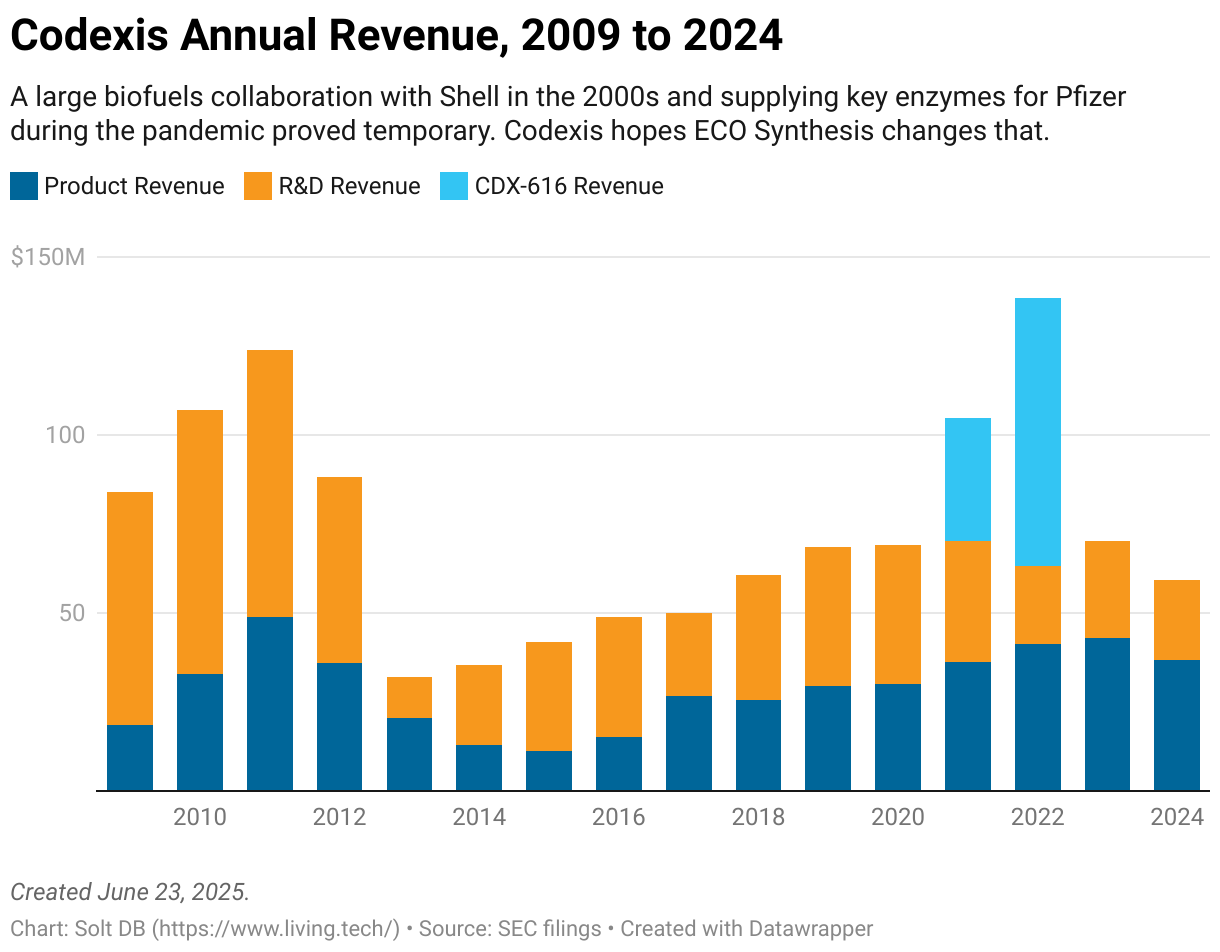

This isn't a new headwind. The defining characteristic of the business for the last 20 years has been choppy, inconsistent revenue. In 2010, it reported $32.8 million in product sales. Last year, just $36.8 million. The annual figure has sunk as low as $11 million and soared as high as $117 million in that span.

Why can't the business deliver consistent performance?

Codexis engineers enzymes that make chemical manufacturing processes more efficient. Industrial enzymes have many advantages, but they suffer from two primary disadvantages.

First, enzymes are relatively expensive to produce. Supplying high volumes for large market opportunities can quickly sour overall process economics. This is why industrial enzymes are primarily used in low-volume niche applications, such as drug manufacturing and scientific research tools.

Second, enzymes are powerful – almost too powerful. A volume that fits in a shot glass can power a small-scale chemical manufacturing facility for a day or longer. In niche applications such as drug manufacturing, customers typically place orders once or twice per year. That means operating performance is dictated by the painfully-slow timing of orders.

To be sure, there are mass market food, beverage, and personal care applications where enzymes play a tiny role. They're why your laundry detergent works at cold temperatures, or why some ice cream brands keep a creamy consistency no matter how long that tub sits in your freezer. But industrial enzymes generally struggle to find goldilocks markets: not too niche, not too enormous, just right.

Codexis thinks using enzymes to manufacture RNAi drugs could represent one of those opportunities – and I think it could be right. It only has to achieve technical benchmarks no one else has ever achieved before. Easy.

By the Numbers

Choppy business performance makes it easy for investors and analysts to lose interest in Codexis. It also makes the company a likely terrible investment if ECO Synthesis doesn't pan out.

The business generates two types of revenue: R&D revenue and product revenue.

R&D revenue is generated when Codexis licenses its enzyme engineering technologies to partners for internal use in their own labs. It provides high-margin revenue – usually having no cost of goods sold – and keeps large partners, such as Merck and Novartis, on the platform. It's nice to have, but it won't be the reason the company succeeds. Recognition of R&D revenue depends on when licenses renew, meaning this is also choppy.

Product revenue is the most important type of revenue for living technology companies. It has the potential to be recurring, growing, and high margin. Due to the bespoke, small-scale nature of pharmaceutical ingredient manufacturing, Codexis has struggled to grow product revenue for most of its history. Efforts to diversify into biofuels (it once had a massive partnership with Royal Dutch Shell), renewable chemicals, DNA synthesis, and clinical diagnostics have each failed to deliver meaningful results.

The company's technical chops have never been disputed. Codexis has earned three Presidential Green Chemistry Awards from the U.S. Environmental Protection Agency (EPA). Only Merck has won more – and they earned one together. Codexis also engineered an enzyme, dubbed CDX-616, that simplified the manufacturing process for a key ingredient in Paxlovid during the pandemic, which led to a massive windfall and subsequent hangover.

The inconsistent performance is easy to see when visualizing the long-term revenue trend. Living with it on a quarter-to-quarter basis is even more frustrating.

Consider how this year began. Codexis expects full-year 2025 revenue of $66 million at the midpoint, which averages out to $16.5 million per quarter. But averages mean little here.

The business reported first-quarter 2025 revenue of $7.5 million. Both product revenue and R&D revenue fell sharply from the year-ago period. Management said the company is on track to meet guidance. That's probably true – this is normal for Codexis – but constantly babysitting the business is stressful for investors. And if most other investors get bored and leave, then it can be uncomfortable to maintain an idiosyncratic position.

Complicating matters further is the short cash runway: $60 million at the end of March 2025.

Management says that can fund the business to cash flow positive operations by the end of 2026, which pencils in commercial traction and a meaningful revenue ramp for ECO Synthesis. But there's not much room for error. This is a tricky market environment to be redlining your cash runway and banking on a new technology ramping in the marketplace – look at what happened to AVITA Medical.

I'd feel more comfortable if the company had a bigger cash cushion, as delays and scale-up issues are almost a certainty. Either way, survival may very well depend on the success or failure of ECO Synthesis.

What Makes ECO Synthesis Different?

Although it might appear to fall under the niche of drug manufacturing, producing commercial volumes of RNA molecules is much different than doing so for a small molecule.

A handful of engineered enzymes might be needed to manufacture a single short-interfering RNA (siRNA) drug product. That's because a siRNA molecule needs to be synthesized from scratch using the building blocks of the genetic alphabet, then modified at specific base pairs so it can survive the journey through the bloodstream. By comparison, past and present pharmaceutical customers typically need one enzyme added to existing processes.

.avif)

Additionally, ECO Synthesis can be applied to an entire therapeutic modality (RNAi). That provides better and faster scaling potential across the industry. Even though each siRNA molecule is unique, efficiencies and refinements will compound over time across the entire platform.

This isn't always possible when using enzymes to manufacture small molecules, which can encompass thousands of unique chemical classes. The enzymes needed to produce an antiviral like nirmatrelvir, one of the active pharmaceutical ingredients of Paxlovid, are very different from those needed to manufacture sitagliptin, the active pharmaceutical ingredient of type 2 diabetes medication Januvia.

Most important, whereas Codexis may supply a key enzyme or two as part of a much larger manufacturing process for a small molecule drug, ECO Synthesis is the manufacturing process.

And enzymatic synthesis of siRNA molecules doesn't just represent a minor improvement.

Today, RNAi drugs are manufactured using a chemical synthesis process based on phosphoramidites, which are stitched together to build each RNA molecule. The process is slow, inefficient, and expensive.

It can take 12 months and over 3,000 kilograms (kg) of chemical inputs to manufacture 1 kg of drug product. The chemical inputs are highly flammable organic solvents, which means each manufacturing facility needs to be explosion proof and is highly regulated. If a contract development and manufacturing organization (CDMO) or drug developer wants to build a new manufacturing facility, then it needs to set aside roughly $500 million per kilogram of capacity.

Drug developers haven't bumped up against the technical and economic limitations of phosphoramidite processes because most RNAi drug product approvals have been for small, ultra-rare indications like primary hyperoxaluria type 1. The math doesn't work for larger indications like high cholesterol, asthma, or obesity.

Let's use Novartis' Leqvio (inclisiran) as an example. Approved to treat high LDL-cholesterol and atherosclerotic cardiovascular disease (ASCVD), it'll become the first blockbuster RNAi drug product (>$1 billion in annual revenue) in 2025.

- Leqvio is dosed at 0.284 grams twice-yearly, so 0.586 grams per patient per year. That's 0.000568 kg per patient per year.

- There are an estimated 20 million Americans with ASCVD. If Leqvio is administered to 1% of the overall patient population, then Novartis will need to manufacture 114 kg per year.

- That would require capital expenditures (CapEx) of $57 billion to build facilities using phosphoramidite chemistry. Likely less if you consider economies of scale for equipment purchases and construction, but you get the idea.

This is exactly the type of goldilocks application that has been so elusive for industrial enzymes.

Enzymatic synthesis could manufacture 5x more siRNA molecules per batch, in half the time, and with 70% less CapEx compared to existing methods. That would drop the cost for Novartis' Leqvio expansion in the example above from $57 billion to $17 billion – roughly in line with investments required to support massive indications like mRNA vaccines and obesity.

Recent ECO Synthesis Technical Milestones

Codexis is developing ECO Synthesis in stages.

The first stage will enable a hybrid production process for siRNA molecules. Chemical synthesis is used to manufacture the initial building blocks and/or RNA strands, then enzymes are used to create a specific RNAi drug product. Think of it like a bridge to full enzymatic synthesis, which also allows early adopters to provide valuable feedback (and revenue).

The second stage will enable full enzymatic synthesis of siRNA molecules. That means synthesizing building blocks, stitching them together in exactly the right order, and attaching ligands for tissue-specific delivery.

Codexis recently demonstrated the ability to manufacture Leqvio using four distinct manufacturing routes:

- Full enzymatic synthesis of siRNA molecules, modifications, and targeting ligands.

- Chemical synthesis for building blocks, then ECO Synthesis for producing the final product.

- Using both chemical synthesis and ECO Synthesis for building blocks, then ECO Synthesis for producing the final product.

- ECO Synthesis for building blocks, then existing methods to produce the final product.

The hybrid approach is ready to be deployed today. Codexis has seen early adopters primarily from the CDMO space, with a large RNAi drug developer or two.

The full enzymatic approach currently has an output of up to 100 g per batch. It's still in development and needs to work out a few technical challenges, like losing too much product during purification steps. The company thinks it can eventually scale up to 25 kg to 50 kg per batch (25,000 g to 50,000 g per batch).

News Flow & Modeling Insights

(Refined for first time since January 2024.)

To reiterate, Codexis will be a lousy investment if ECO Synthesis doesn't work. It's on the right path so far.

The current model estimates a fair valuation of $422 million. After factoring in 15% dilution, that works out to roughly $4.43 per share.

- The existing business has an estimated value of $188.760 million.

- The development-stage ECO Synthesis platform is valued at $233 million at its current level of de-risking. This assumes initial revenue in the second half of 2025 for the hybrid approach.

Given current market conditions, Codexis has above-average acquisition potential. That's influenced by its tenuous cash runway, which may lead management to consider selling the business. The most likely suitor at this time is a CDMO, such as Agilent.

An acquisition in the next 12 months could result in a large premium over its current valuation, but significantly lower than historical highs or what might be possible if it remains a standalone company.

Margin of Safety & Allocation

Codexis is considered a Future Compounder position with Average Conviction (3 out of 4, with 1 representing the highest conviction). The estimated fair valuation based on my current model is below:

- Market close June 20: $2.29 per share

- Modeled Fair Valuation: $4.43 per share

- Allocation Range: Up to 2.5%

Codexis reported 82.845 million shares outstanding as of May 9, 2025. The modeled fair valuation above assumes 95.272 million shares outstanding, which is equivalent to 15% dilution.

Further Reading

- May 2025 press release announcing Q1 2025 operating results

- May 2025 regulatory filing (10-Q) detailing Q1 2025 operating results

- January 2024 research note introducing enzymatic synthesis of RNAi drug products (numbers and market size estimates may / may have changed)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)