.svg)

Advances in RNA interference (RNAi) paved the way for CRISPR gene editing and mRNA vaccines. The ugly duckling of genetic medicines is about to do it again.

Multiple companies focused on RNAi are advancing drug candidates targeting diseases in lung, brain, muscle, and fat tissues. Some are even attempting to edit the immune system inside the body. The tools used to deliver RNAi drug payloads to specific cell types will once again be borrowed by gene editing, gene writing, and in vivo cell therapy platforms.

This is a huge development. Whereas the first six approved RNAi drug products all take aim at rare genetic diseases accessible by targeting the liver, the ability to target diverse tissues means common diseases will soon be treated by RNAi therapeutics. From asthma and alcoholism to high cholesterol and obesity, very large patient populations will benefit from advances in drug delivery in the next 10 years. People you know, people you live with, and maybe even yourself.

This is also a huge problem.

Today, the world manufactures about 1,000 kilograms of RNAi drug products – and it's a huge pain in the ass. The production process relies on a difficult, expensive, wasteful, and low-quality chemical synthesis method. Drug developers tolerate it because, hey, how many people have primary hyperoxaluria type 1 anyway?

But if the industry's next-generation pipeline earns even a handful of approvals in non-liver tissues, then global production of RNAi drug products is expected to increase to 30,000 kilograms by 2035 (and possibly as soon as 2030). That's a 3,000% increase from current levels.

This problem explains the recent pivot by Codexis, which is developing an enzymatic production process to bail out drug developers with a combined market valuation of over $500 billion. Although the ECO Synthesis platform won't be in full swing until 2026, the first de-risking events are expected in 2024.

RNAi Manufacturing Sucks

RNAi drug products targeting the liver have the highest probability of success (POS) of any therapeutic modality – and it's not even close. Drug candidates aimed at silencing gene expression in the liver have a 60% chance of earning U.S. Food and Drug Administration (FDA) approval once they begin a phase 1 clinical trial. All other drug candidates combine for a POS of just 7.8% from the same starting block.

Selectivity is the key to their success. RNAi works through RNA molecules called short interfering RNA (siRNA). These are designed to be complementary to, meaning the opposite sequence of, a specific disease-driving mRNA transcript floating around cells. An siRNA molecule is actually double stranded, but it gets unzipped once inside cells. One of the unzipped strands finds the corresponding mRNA transcript, binds to it, self destructs with existing cellular machinery, and stops disease-driving proteins from being created. It's a very precise, safe, and targeted way to treat diseases.

Those siRNA molecules are what powers RNAi drug products.

The current method for manufacturing siRNA relies on chemically synthesizing the molecules piece by piece using phosphoramidite chemistry. Each genetic base is added one-by-one to a sugar backbone, which builds the siRNA molecule. It… works. But phosphoramidite chemical synthesis results in a lot of wasted chemical byproducts, incorporates many errors that need to be weeded out during purification, and has excruciatingly low yields.

RNAi companies such as Alnylam Pharmaceuticals ($23 billion market cap), Arrowhead Pharmaceuticals ($4 billion market cap), and Novo Nordisk ($469 billion market cap) tolerate the inefficiency of chemical synthesis because they don't need much siRNA for currently-approved drug products treating rare diseases. The global industry produced roughly 1,000 kilograms, or 1 metric ton, of siRNA drug products in 2022.

If RNAi drug candidates earn approvals in more prevalent diseases, such as asthma and obesity, then annual production volumes of siRNA will swell to at least 30 metric tons by 2030 or 2035. By the way, that assumes assets currently in phase 2 and phase 3 clinical trials have a POS of just 35%, which is almost half of their phase 1 POS when directed at the liver. The field isn't mature enough to calculate a POS for non-liver assets, which could be materially lower or similar to liver assets. Just know that 35% might be a significant underestimate. The global industry might instead need 60 to 100 metric tons of siRNA by 2035, especially if the lung pipeline of Arrowhead Pharmaceuticals builds on initial early success.

Even in the "conservative" estimate of 30x growth, phosphoramidite chemistry wouldn't be able to meet that demand. It's physically and economically impossible.

- Agilent Technologies invested $725 million to expand a manufacturing facility. It will end up producing an additional 1 kilogram (0.001 metric tons) of RNAi drug products per year.

- Swiss company Bachem is spending $760 million to construct a third manufacturing facility to produce peptide (short protein fragments) and RNA products by 2030. That's after spending $560 million to expand an existing facility.

- Arrowhead Pharmaceuticals spent $200 million building a new manufacturing facility to support its yet-to-be-commercialized liver-directed RNAi drug candidates.

The numbers simply don't scale for the status quo. That's where enzymatic RNA synthesis comes into play.

How Codexis Can Win with the ECO Synthesis Platform

If you look up the definition of a company finally putting it all together, then you'll see Codexis and the ECO Synthesis platform. I'm being silly, but it really is a sneaky amazing niche to focus on.

Codexis has absolutely crushed its niche in enzyme manufacturing in recent decades. It works with drug manufacturers to design enzymes that make pharmaceutical ingredient production more efficient. Customers include Merck, Pfizer, Novartis, and others. Products include Janumet, Januvia, and Paxlovid.

Much like the problems with synthetic chemistry in RNAi, Codexis has already helped customers such as Merck avoid building new manufacturing facilities by simply making existing infrastructure more efficient. There's a reason Codexis has won three Environmental Protection Agency (EPA) Green Chemistry Challenge Awards (2006, 2010, 2012). Only Merck, BASF, and The Dow Chemical Company have won more.

But what makes enzymes great also makes them terrible products to build a business around. Namely, a very, very, very small amount goes a long way. Enzymes use quantum tunneling (seriously) to reduce the amount of energy required to complete a chemical reaction. They're what makes biology so powerful.

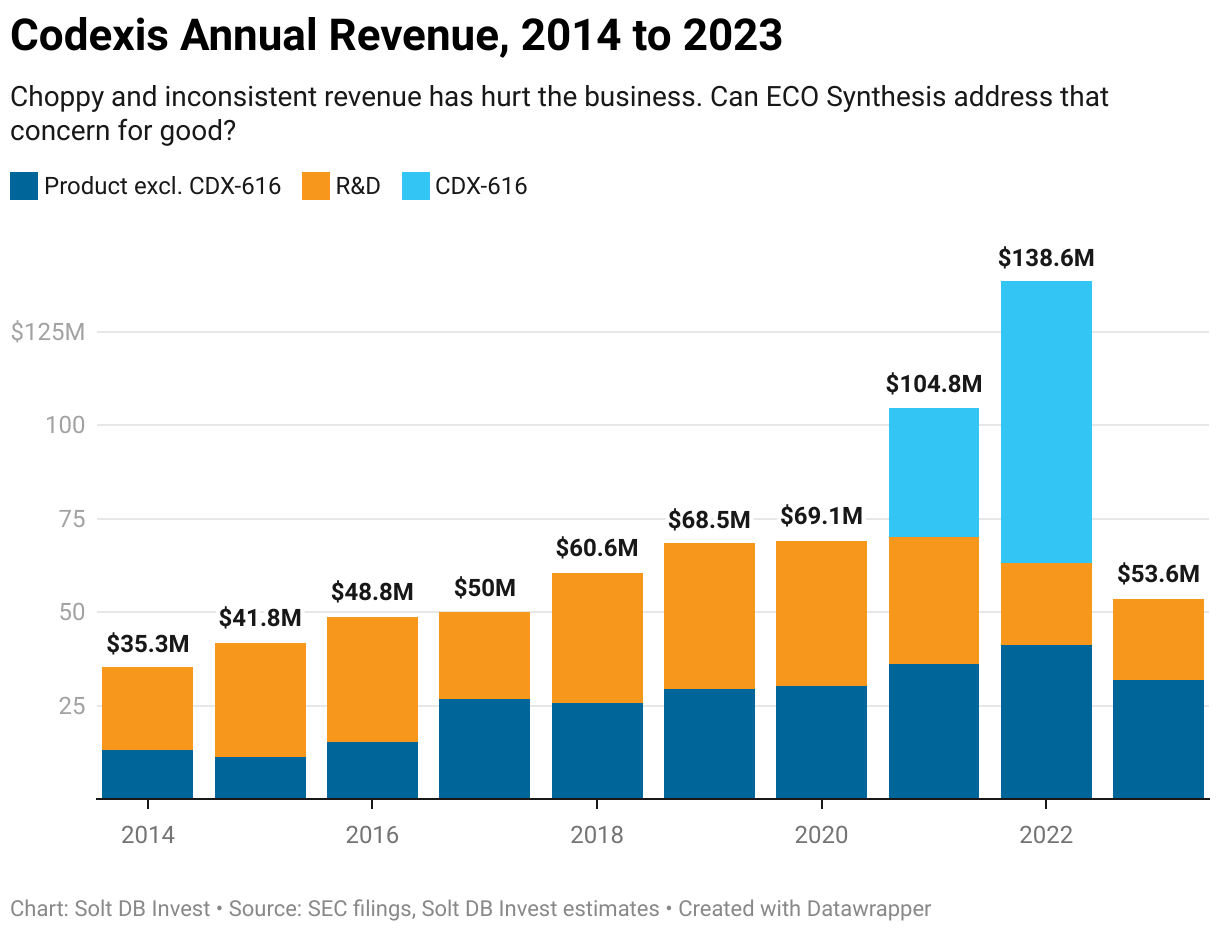

Codexis has struggled to generate consistent or meaningful revenue from its pharma enzyme business, since customers typically only make one or two orders each year for their entire manufacturing footprint. The "meaningful" problem was addressed when the business developed CDX-616, an enzyme used to manufacture Paxlovid from Pfizer, but fading demand for coronavirus medicines meant the "consistent" problem remained.

That's what makes the ECO Synthesis platform intriguing for investors. Codexis isn't targeting a single drug product; it's using enzymes to address challenges manufacturing an entire therapeutic modality comprising potentially dozens of drug products. Successfully commercializing the technology would turn the business into a picks and shovels provider, with gross margins over 70% to boot.

Using enzymes to manufacture siRNA molecules is also a technically sound approach in 2024. It would avoid the key bottlenecks for enzymatic approaches to DNA synthesis, which are hamstrung by relatively short sequences that make them commercially unviable. Whereas a gene might need to be thousands of bases long to be functional, a typical siRNA molecule is only hundreds of bases long at most – well within the current technological capabilities of enzymatic synthesis. That means Codexis won't run into the same economic bottlenecks in RNAi drug products as Molecular Assemblies (its partner) or Twist Bioscience in enzymatic DNA synthesis.

Enzymatic RNAi synthesis would also be simpler than current enzymatic approaches to manufacturing mRNA, which require a bulky DNA template. In fact, enzymatic platforms such as ECO Synthesis would boast significant advantages. They could utilize free nucelotides, or the bases that comprise nucleic acids such as RNA and DNA. What's more, siRNA molecules typically aren't encapsulated in lipid nanoparticles (LNPs), as mRNA therapeutics tend to be. That makes formulation easier, but it requires the siRNA molecules to be modified to stabilize and protect the drug payload. Enzymes can assist in the required chemical modification of siRNA molecules, too.

Codexis estimates every 1 kilogram of siRNA drug product will cost about $250,000 to manufacture with enzymatic synthesis. If the global industry requires 30,000 kilograms by 2035, then the global manufacturing opportunity would reach $7.5 billion per year. The field would need to invest more than $20 billion in existing phosphoramidite chemistry processes to meet that demand.

Enzymatic manufacturing would represent roughly 10% of that expense, or $750 million per year. That means the business would only need a market share of 19% to generate a record amount of annual revenue (>$139 million per year) – and it doesn't have many competitors.

There's an early-stage startup from the Wyss Institute called EnPlusOne, which has produced milligrams of siRNA from its enzymatic tools. Codexis has already achieved gram-scale synthesis – or 1,000x more output. Investors should probably pencil in Ginkgo Bioworks as a future competitor, although it hasn't formally announced programs in enzymatic siRNA synthesis.

There's also a slew of contract development and manufacturing organizations (CDMOs) eager to produce RNA medicines for drug developers, but these could be both competitors or customers of Codexis and its ECO Synthesis platform. It's too soon to say with much confidence how the field will shake out, but Codexis is well positioned to emerge with a leading market share.

As a reminder, the market doesn't exist right now. If Codexis is right and delivers on its first-mover advantage and existing commercial track record with drug developers, then it could play a pivotal role in market formation.

When Will ECO Synthesis Deliver?

Investors need to wait. Are you guys tired of waiting yet? Well, that's generally how you make money and beat the S&P 500 in biotech.

Market Entry Point in 2024

Codexis expects to have a double-stranded RNA (dsRNA) ligase widely available for commercial customers in 2024. This enzyme would slot into existing phosphoramidite chemistry processes and make them more efficient. It's already in testing with large RNAi drug developers, which is a relatively short list – a good sign for investors.

The dsRNA ligase enzyme could be crucial for gaining an important commercial advantage over the competitive landscape before introducing true enzymatic siRNA production tools.

The ECO Synthesis platform should have initial pre-commercial tests with customers and partners (a subtle hint at potential CDMO customers) in 2024.

Initial Commercial Licenses in 2025

Codexis expects to announce initial commercial licenses to ECO Synthesis in 2025. This would provide a key glimpse at future economics from the technology platform, potential drug candidates throughout the industry it might be used to manufacture, and so on.

Broad Commercial Availability in 2026

Codexis expects to make the ECO Synthesis platform widely available to commercial customers and partners in 2026. That seems far away, but it's well before the potential 2030 to 2035 inflection points for RNAi drug candidates. Between now and 2026 investors will see important data readouts from pipelines wielded by Novo Nordisk (the former Dicerna Pharmaceuticals pipeline), Alnylam Pharmaceuticals, and Arrowhead Pharmaceuticals, among others. These three leaders alone account for programs across obesity, alcohol use disorder, Alzheimer's disease, asthma, and more.

Forecast & Modeling Insights

(Refined 2024 revenue expectations.)

Codexis remains a Growth (Speculative) opportunity. However, I'm upgrading the suggested allocation from "up to 1%" to "up to 5%."

Codexis expects its core pharma segment to return to growth. Jettisoning the novel therapeutics segment will preserve cash. So, although the company likely ended 2023 with only $70 million in cash, it'll get the business through a few de-risking events and into 2025. Barely.

My refined 2024 model expects:

- Total revenue of $53 million, significantly lower than the previous 2024 model of roughly $70 million.

- Product revenue of approximately $39 million, representing roughly 20% growth over 2023.

- R&D revenue of approximately $14 million, representing a roughly 33% decline from 2023. This doesn't include revenue from precommercial testing of the ECO Synthesis platform in 2024.

- Share dilution of 25%, up from previous expectations of 7.5%.

Although the current 2024 model has a lower total revenue estimate and higher share dilution estimate, it's the first to account for the ECO Synthesis technology platform. Therefore, the fair valuation increases from a previous level of $3.96 per share to $5.53 per share.

Is This Aysmmetric?

I'm tempted to make Codexis an Asymmetric Opportunity right now given its lowly valuation, but to be responsible, I'll await more complete details on the strategy. There's no reason to rush into a full position right now, especially considering the most important de-risking events aren't expected until 2025 and the ECO Synthesis platform won't be in full swing until 2026.

But, uh, there's a lot of middleground between "no position" and "full position."

Codexis is valued at only $190 million. If the company succeeds, then it has a reasonable path to a $1 billion valuation by the end of 2026. The timing might depend on when the business provides revenue growth projections for 2027 and beyond, which might not be publicly announced until February 2027.

Either way, even if the company increases the number of shares outstanding by 50% in that span, then successful commercialization of the ECO Synthesis platform means shares could be valued at $9.55 apiece by early 2027. That's a total return of 255% and an average annual return of 52.5% over the three-year period. The S&P 500 wouldn't stand a chance.

To be blunt, you only get the crazy returns by investing in things when everyone thinks you're crazy. But you need to have a crazy deep thesis and understanding of a business to confidently pull the trigger.

Codexis doesn't have the opportunity locked down. It'll face competition from startups such as EnPlusOne Bio and, most likely, Ginkgo Bioworks. The business is currently well ahead of EnPlusBio and can go toe-to-toe with Ginkgo Bioworks on enzymes. It appears well positioned to stake out a leading market share in enzymatic RNA production methods.

Margin of Safety & Allocation

Codexis is considered a Growth (Speculative) position. The current modeled fair valuation for the company based on our 2024 model is below:

- Market close January 24: $2.70 per share

- Modeled Fair Valuation: $5.53 per share

- Allocation Range: Up to 5%

Codexis reported 69.830 million shares outstanding as of October 31, 2023. The modeled fair valuation above assumes 87.288 million shares outstanding, which is equivalent to 25% dilution.

Further Reading

- June 2023 research note arguing that Codexis is an acquisition target

- November 2022 research note arguing Codexis needed to focus on reining in its cost structure

- September 2022 research note introducing coverage of Codexis and explaining the opportunity in enzymes

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)