.svg)

Shares of Krystal Biotech fell by double digits after the company held its first-ever quarterly earnings conference call. There were some awkward exchanges with analysts, but investors looking to pinpoint why the stock tumbled might not find one.

The gene therapy developer generated its first dollar of commercial revenue during the third quarter as Vyjuvek recorded $8.6 million in net sales. Although that outperformed Wall Street expectations, there are usually too many variables and too much uncertainty to accurately gauge product launches. Therefore, the "beat" wasn't reflected in the share price.

Krystal Biotech set expectations for the next 18 months of development, regulatory, and commercial activities. Then again, given the company's recent history of failing to advance assets in clinical trials, Wall Street's muted response makes sense. That could change in 2024.

The most important asset in the portfolio or pipeline, gene therapy candidate KB407 in cystic fibrosis, completed enrollment in the first of three cohorts in a phase 1 clinical trial. It'll take time – and data – to contribute to the company's valuation, but it could more than double the current market cap.

Let's review where things stand after the third-quarter 2023 business update.

By the Numbers

The business held its first-ever quarterly conference call and delivered its first-ever quarter of profitable operations.

Kind of.

Krystal Biotech reported net income of $80.7 million for the quarter, but primarily driven by the sale of a priority review voucher (PRV) earned when Vyjuvek earned regulatory approval. The voucher fetched $100 million when sold this summer. As a result, the business ended September 2023 with $562 million in cash.

For the foreseeable future, investors will be more focused on operating margins. The gene therapy developer reported a quarterly operating loss of $26 million, which is remarkably efficient. However, considering research and development (R&D) expenses declined from the year-ago period, the operating efficiency likely won't last. A slate of clinical trial starts will be expensive to pursue.

Krystal Biotech also reported commercial metrics for the early ramp of Vyjuvek. The two most important terms:

- Patient Start Forms are submitted when an individual requests access to the drug.

- Patients on Drug is the number of individuals who are receiving treatment.

Investors can think of the commercial ramp for Vyjuvek as a pipeline. The company must properly vet individuals requesting access to treatment. Although most will be successful, Krystal Biotech said it was considering a patient's insurance coverage during the initial phase to mitigate financial burdens for families. This should be resolved in early 2024 when payer coverage is greatly expanded.

In the third quarter of 2023, the company reported:

- 284 patient start forms, representing 9% of the estimated U.S. patient population and roughly 19% of the company's targeted U.S. treatment population. Not all of these patients were on Vyjuvek or paying for the drug.

- 46% of patient start forms were received from centers of excellence, or specialty hospitals. This is promising because the remaining 54% of patients requesting access to treatment did so through community hospitals, which are more difficult to penetrate.

- 45% of patient start forms were from commercial insurance, with the remaining 55% on government insurance.

- Over 88% of patient start forms requested at-home dosing.

Perhaps the clearest sign of the drug product's short commercial life so far is the fact the first patient payment wasn't recorded until August 2023. Management said it will begin reporting Patients on Drug in early 2024, which is more indicative of product revenue. It's simply too early in the ramp to make sense of those numbers.

Revenue will increase in subsequent quarters, but investors might not see meaningful progress until the second quarter of 2024 (reported in August 2024). If the company executes and achieves a relatively smooth U.S. ramp through 2024, then it'll help to de-risk expected launches in the European Union and Japan in 2025.

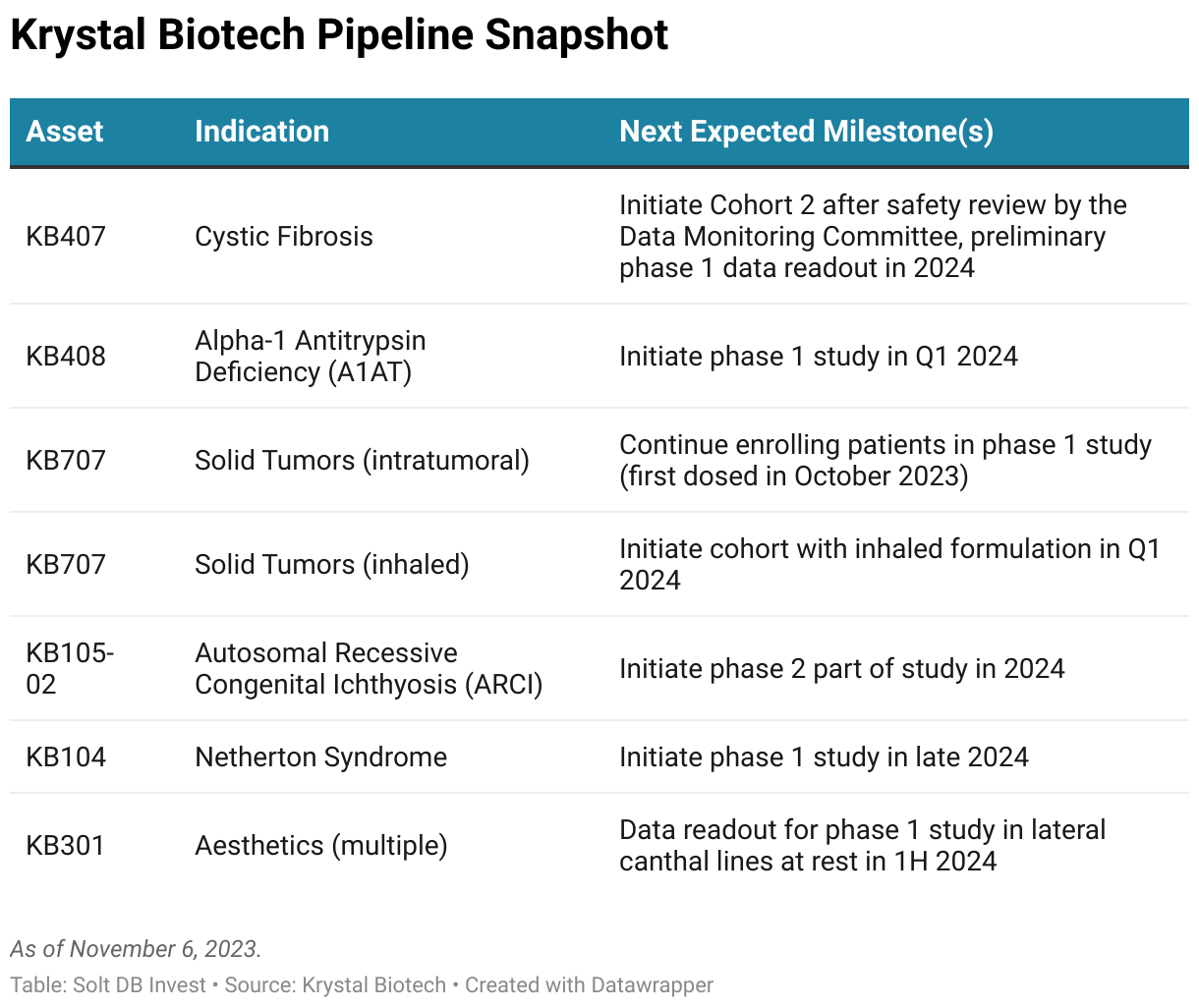

Pipeline Snapshot

Krystal Biotech also provided the latest expectations for its pipeline. On the one hand, the drug developer has been painfully slow to advance additional assets into and through clinical trials. On the other hand, the slow development execution has been partially strategic to manage operating expenses and cash burn. Either way, recent progress with patient enrollment in multiple trials is a promising sign.

As clinical trials mature, the company's R&D expenses are expected to increase significantly. That will put additional pressure on Vyjuvek's ramp, as a faster ramp could help to partially offset declining operating margins. However, it's important to note drug developers often see worse operating losses in the first two to three years after launching their first drug product.

Margin of Safety & Allocation

Krystal Biotech is considered a Flyer position. Solt DB Invest doesn't share modeling or fair valuation estimates for Flyers, which have a suggested allocation range of 0% to 0.5%.

Further Reading

- November 2023 press release announcing third-quarter 2023 operating results

- November 2023 financial filing (10-Q) detailing third-quarter 2023 operating results

- August 2023 research note downgrading Krystal Biotech from a Growth (Speculative) position to a Flyer position

.svg)

.svg)

.png)

.svg)

.svg)

.svg)