.svg)

If you checked the front page of The Wall Street Journal today, then you know Zach Kirkhorn stepped down as CFO of Tesla just ahead of the Cybertruck launch. I'm more concerned with a different C-suite departure during a different commercial ramp.

Krystal Biotech disclosed today in a regulatory filing that Andy Orth stepped down as Chief Commercial Officer (CCO). The CCO at a drug developer is tasked with preparing for and executing commercial activities for therapeutic assets, such as launching and ramping sales of a new drug product. Considering Vyjuvek is just six weeks into its commercial launch, and the company has struggled to advance the rest of its pipeline, this is terrible news.

Andy Orth Abruptly Resigns

It helps to understand that Andy Orth isn't just "some guy." His career stops include leading commercial finance and commercial operations at Genzyme (2005 to 2007), Biogen (2009 to 2015), and Alnylam Pharmaceuticals (2016 to 2021). For example, he was Senior Vice President of U.S. Business at Alnylam Pharmaceuticals during the company's first product launches, which were also for rare diseases. He oversaw teams across business account teams, market access, marketing, patient services, and operations.

If there was no Andy, then Alnylam Pharmaceuticals might not be a $23 billion business today.

He left Alnylam Pharmaceuticals to join Krystal Biotech as CCO in May 2021 – it was a great haul for the emerging gene therapy developer. As noted in the press release at the time of his hiring:

We are excited to welcome Andy to the Krystal team at such an exciting time for our lead investigational program B-VEC [Vyjuvek] for DEB, and the rest of our growing rare disease pipeline,” said Krish S. Krishnan, chairman and chief executive officer of Krystal Biotech. “He is an accomplished biotechnology executive who has successfully launched several genetic medicines in the rare disease space and will be a key asset for Krystal as we work towards our goal of building a fully integrated biotechnology company with a strong commercial capability.

His departure a little over two years later, and during the commercialization of Vyjuvek, raises some questions at the very least.

Worse, the SEC filing didn't contain the customary "this was not the result of a dispute with the company" language. The disclosure was one sentence. Nor did Krystal Biotech mention his departure in the press release today summarizing the second-quarter 2023 business update. These details don't necessarily mean there was a dispute or disagreement, and it's possible the company terminated the CCO, but the optics certainly aren't favorable.

Krystal Biotech has struggled to advance clinical trials for assets aside from Vyjuvek and has a history of "strange" appointments (read: incompetent individuals) in important positions. Solt DB Invest has flagged the chronically-delayed pipeline multiple times, including in November 2022 and again in May 2023. The latter was accompanied by a downgrade of the company to Growth (Speculative) and a reduction of the allocation suggestion from 10% to 5%.

How Does This Impact Krystal Biotech?

Well, it's hard to adjust probabilities without knowing why the CCO resigned. Are there severe deficiencies in the commercial readiness of Krystal Biotech? That would be bad. Did the CCO resign to care for a loved one with a disability? That would be less bad, but that doesn't make it any easier to replace Andy Orth during the commercial launch of Vyjuvek.

What I can say is that the CCO's departure increases the downside risk of our model.

Forecast & Modeling Insights

Solt DB Invest explained its preliminary model and peak global sales estimate for Vyjuvek in December 2022. The drug candidate hadn't earned U.S. Food and Drug Administration (FDA) approval and pricing hadn't been set at that time. We estimated at least $540 million in peak global sales on an annual basis and valued Krystal Biotech at $3.2 billion upon approval. That's almost exactly the valuation shares settled at in the months following approval, but things have changed.

Investors now know more information:

- Vyjuvek has a list price of $24,250 per vial. This works out to roughly $631,000 per year on a steady-state basis, meaning a patient that uses the product continuously for one year. (It's not so simple.)

- As of today, investors know how many patients have expressed interest in using Vyjuvek. We even know the breakdown of patient start forms submitted by the type of dystrophic epidermolysis bullosa (DEB).

- Krystal Biotech has finally dosed the first patient in a phase 1 clinical trial of KB407 in cystic fibrosis, which has the potential to become the company's most valuable and important asset.

- Krystal Biotech has also unveiled a new foray into gene therapy for cancer indications, starting with skin and lung cancers.

For now, let's focus on the revenue model for Vyjuvek since that dominates the valuation model for the company. Before the end of 2023, Solt DB Invest will unveil a forward-looking model for Krystal Biotech to prepare for different scenarios of phase 1 clinical data readouts for KB407 in cystic fibrosis.

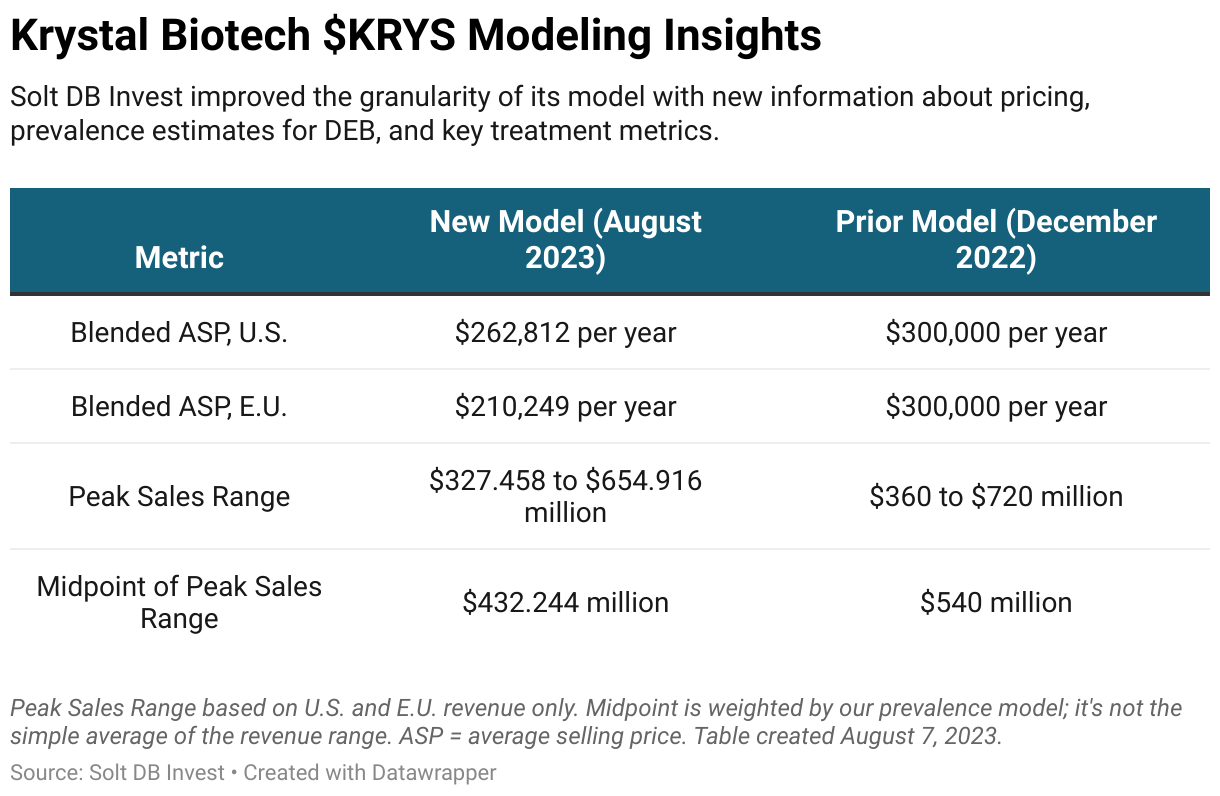

There are a few differences in our refined model being introduced today and the prior model first released in December 2022.

Solt DB Invest has refined several metrics within its model, most importantly the prevalence estimates in both the United States and European Union for both types of DEB and introduced more granularity within dose frequency and clinical benefit. Not all patients will respond to treatment, not all wounds are the same size, and not all cases of DEB have the same treatment burden. Welcome to the modeler's dilemma.

These refinements result in a more accurate blended average selling price (ASP) from the prior model (before a list price was set), although we were actually pretty close previously. Please note Vyjuvek hasn't been approved in Europe and prices haven't been set on the continent.

Our model also has a slightly tighter range of peak global revenue estimates, which are now expected to be between $327 million and $654 million. The midpoint is $432 million compared to a prior estimate of at least $540 million. This will be further tightened as more information about patient starts and discounting become known throughout launch, and after prices are set in Europe next year.

For reference, Krystal Biotech now estimates Vyjuvek has a global revenue opportunity of at least $750 million, but companies often overestimate the peak sales potential of their own assets. The company's estimate includes Japan (the third major market outside of the U.S. and E.U.) and all other global patients (minimal contributions), whereas our model only includes the U.S. and E.U. At any rate, achieving our peak global sales estimate would make Vyjuvek the most successful gene therapy product ever by a significant margin.

Investors do have some early signals about Vyjuvek's launch.

- Krystal Biotech revealed it has received 121 patient start forms through the first six weeks of market launch, including 91 patients with recessive DEB (RDEB) and 30 patients with dominant DEB (DDEB).

- Few diseases have accurate incidence (how many new cases at birth each year?) and prevalence (how many in the entire population?) rates. Estimates for rare diseases are a complete shitshow. Nonetheless...

- Depending on how Solt DB Invest counts the prevalence of DEB (both RDEB and DDEB) in the United States, Krystal Biotech has already received interest from between 3.1% and 5.0% of all patients in the United States.

- That's a good start. However, that's roughly aligned with our prevalence estimates for the number of severe DEB patients. In other words, individuals who are suffering the most are the easiest to identify and the most likely to seek treatment. It will take considerably more work to find and treat less severe DEB patients. Krystal Biotech will eventually see patient interest slow down, but how soon will that occur? It's too soon to say.

Keep in mind that should execution risk or the departure of the CCO threaten the launch and ramp of Vyjuvek, then real-world peak global revenue could be considerably lower than our model.

There's an additional risk to consider for the November 2023 earnings conference call. Wall Street will be hyper fixated on third-quarter 2023 revenue totals for Vyjuvek – the first ever released. Outperforming or underperforming expectations in the first full quarter of commercial availability won't necessarily impact the peak global sales potential, but kneejerk reactions could inject volatility in either direction.

Margin of Safety & Allocation

(Refined model.)

Krystal Biotech is considered a Growth (Speculative) position. The current modeled fair valuation is based on our refined model for the existing portfolio and pipeline, primarily reflecting Vyjuvek's ramp through the end of 2027:

- Current Price (market close August 7): $108.51 per share

- Fair Valuation: $105.69 per share

- Allocation Range: Up to 5%

Krystal Biotech reported 27.994 million shares outstanding as of July 31, 2023. The Margin of Safety range above assumes 30.094 million shares outstanding, which prices in 7.5% dilution.

Further Reading

- August 2023 press release announcing second-quarter 2023 operating results

- August 2023 regulatory filing (10-Q) detailing second-quarter 2023 operating results

- August 2023 regulatory filing (8-K) announcing departure of CCO Andy Orth

- May 2023 research note criticizing pipeline delays

- December 2022 research note discussing preliminary model for FDA approval of Vyjuvek

- November 2022 research note criticizing pipeline delays

.svg)

.svg)

.png)

.svg)

.svg)

.svg)