.svg)

Krystal Biotech originally declined to include at-home dosing for Vyjuvek in its regulatory application for fear of a daunting regulatory pathway. Good thing the U.S. Food and Drug Administration (FDA) insisted.

As of February 2024, the dystrophic epidermolysis bullosa (DEB) treatment boasted 98% at-home administration. That carried Vyjuvek to a 96% compliance rate at the end of 2023 (note the different cutoffs for those metrics). It helps that there are no other meaningful treatment options for the rare skin disease, but sweeping the trifecta of safety, efficacy, and convenience is the Holy Grail of drug development.

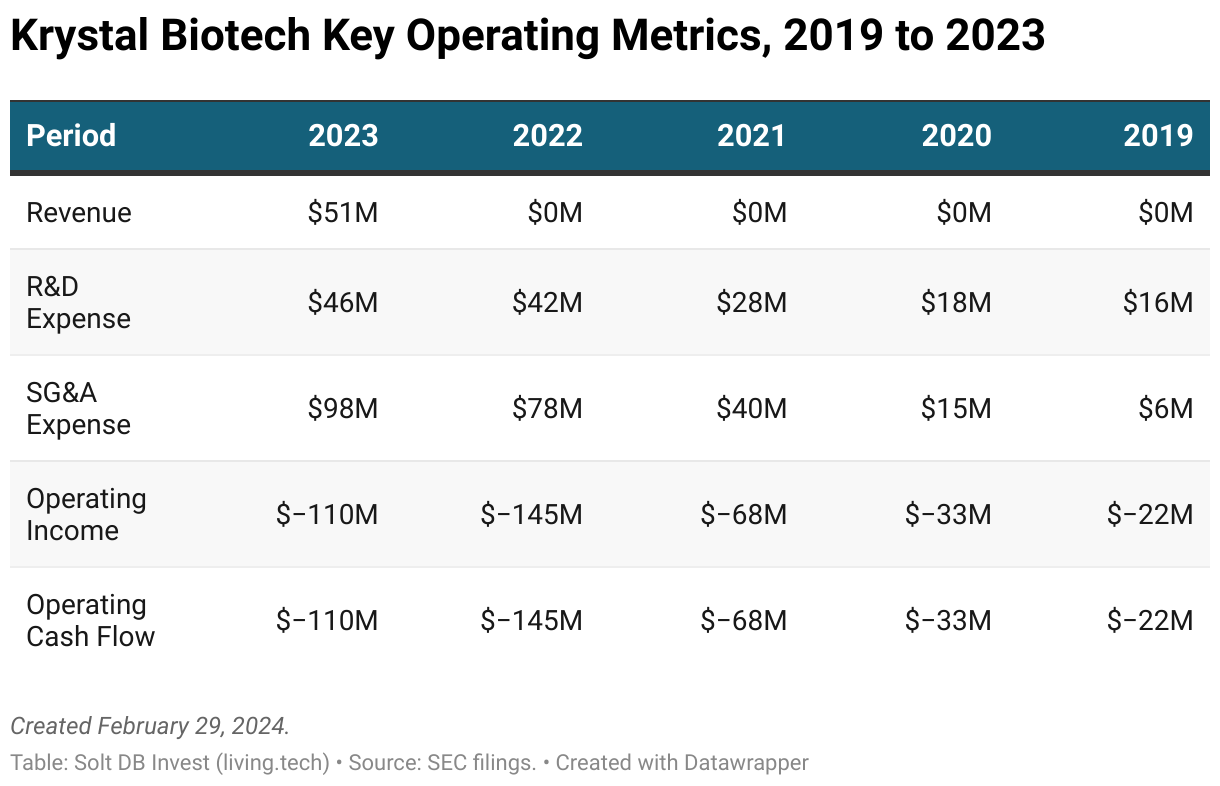

That propelled the herpes simplex virus (HSV-1) gene therapy to fourth-quarter 2023 revenue of $42.1 million and full-year 2023 revenue of $50.7 million. Wall Street expected just $28.6 million and $36.3 million, respectively, although drug launches are notoriously difficult to accurately model.

Here comes the nuance.

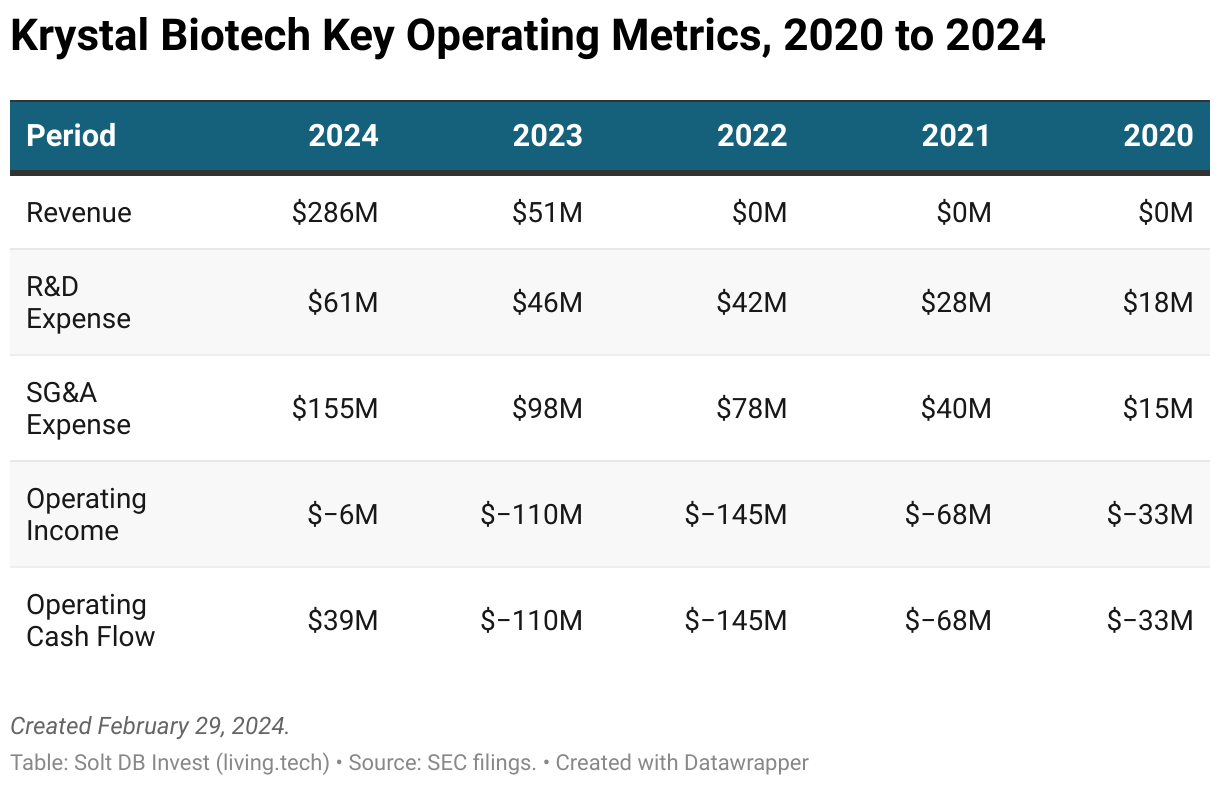

Wall Street analysts have since increased their expectations for full-year 2024 revenue from $200.3 million to $237.4 million. That's below our model of $286.3 million. Meanwhile, Wall Street now expects full-year 2025 revenue of $416.3 million, which is higher than our estimate of $411.0 million.

What gives? The mismatch is due to how we account for expected declining Vyjuvek demand from long-term customers, which could cut revenue by 25% to 50% per patient over time. The stunted trajectory will be partially masked by a large untapped pool of patients in the initial phase of the U.S. launch in 2024 and offset by the international expansion in Europe and Japan in 2025.

Investors can bask in the growth trajectory of Vyjuvek in the meantime, while Krystal Biotech remains one of the more obvious acquisition targets in drug development in the next 36 months. Good thing I sold my shares when CCO Andy Orth abruptly resigned last summer.

By the Numbers

It doesn't quite make sense to compare year-over-year numbers for a newly commercial drug developer such as Krystal Biotech. However, there are still important metrics for investors to follow.

One of the frustrating things about the business has been the slow pace of clinical development for programs, aside from Vyjuvek. On the one hand, that has limited the ability to price in future potential from emerging programs, including the entire lung portfolio. On the other hand, management has done so strategically to manage cash burn and allow Vyjuvek to self-fund the business. There was no guarantee that would've worked, but it's now working better than expected.

Consider how employee headcount, research and development (R&D) expense, and selling, general, and administrative (SG&A) expense have compared over the last five years. The company had 229 employees in February 2024, 210 employees in February 2023, 119 employees in February 2022, 75 employees in February 2021, and 51 employees in February 2020.

Krystal Biotech has a robust early-stage pipeline featuring six named programs, plus an eye drop formulation of Vyjuvek (we'll refer to it as "Vyjuvek Eye") and multiple unnamed programs. The most advanced program is only now just ramping patient enrollment in a phase 1 clinical trial. Vyjuvek Eye only needs to run one clinical trial to earn a supplemental approval, so that exists in a separate category.

Yet, the company has a very modest R&D spend at just $46.4 million in 2023 and $42.5 million in 2022. When investors account for stock-based compensation, which is a non-cash charge, then the business spent just $89 million of cash on R&D in the last two years. That's incredible.

For more perspective, consider that the HSV gene therapy pioneer reported operating cash burn of $282.1 million in the last five years combined. Compare that to the most recent full-year period totals for other drug developers in the Solt DB Invest ecosystem:

- Coherus BioSciences reported an operating cash outflow of $257 million in 2022.

- Relay Therapeutics reported an operating cash outflow of $300.3 million in 2023.

- Arrowhead Pharmaceuticals reported an operating cash outflow of $153.9 million in 2023.

Krystal Biotech expects to do it again this year. Management guided for full-year 2024 non-GAAP operating expenses (R&D plus SG&A) of $150 million to $175 million. The "non-GAAP" qualifier means this range excludes stock-based compensation expense.

This suggests another relatively slow year for pipeline progress despite plans for five active clinical programs in 2024. It also reflects the early-stage nature of the pipeline. R&D expenses will grow significantly as programs mature in 2025 and 2026, although spend could be relatively limited in 2025, too.

Despite the incredible potential of HSV gene therapy in lung disorders, the stock price all comes down to Vyjuvek. That's not such a bad thing given the faster-than expected ramp.

- Krystal Biotech has identified roughly 1,200 patients in the U.S. with either recessive dystrophic epidermolysis bullosa (RDEB) or dominant dystrophic epidermolysis bullosa (DDEB). There are an estimated 3,000 patients in the U.S. with any form of DEB, although many of these cases are less severe, potentially misdiagnosed, and will generate significantly less revenue than the identified population with more severe manifestations of the rare disease.

- As of February 2024, the company had patient start forms (PSFs) from 35% of identified patients, or roughly 420 patients. The total number of PSFs represents a signal of near-term revenue potential. That's up from 284 PSFs at the end of September 2023.

- As of February 2024, the total number of PSFs was split roughly 75% with RDEB and 25% with DDEB.

- As of February 2024, the company had reimbursement approvals for 228 patients, representing roughly 19% of the identified patient population.

It's still too early in Vyjuvek's launch to correlate many of these metrics, especially against a heavy dose of nuance.

For example, a vial of Vyjuvek sports a list price of roughly $24,250. The number of vials required per patient varies by severity, but it typically ranges from one (1) to four (4) vials per month. However, calculating and modeling the revenue potential isn't so simple. There's an annual reimbursement cap that patients with severe disease will run into. In other words, patients requiring four (4) vials per month won't drive $1.2 million in annual revenue ($24,250 per week x 52 weeks per year).

This is key to understanding the trajectory of Vyjuvek's launch.

Looking Ahead

Krystal Biotech's faster-than-expected ramp of Vyjuvek and strategically (albeit frustrating) slow pace for clinical programs bodes well for investors.

Management guided for full-year 2024 operating expenses (R&D plus SG&A) of $150 million to $175 million. That excludes our modeled $40 million in stock-based compensation for those two line items.

It also excludes the final $37.5 million in settlement payments to PeriphaGen, from which Krystal Biotech stole key elements of its HSV gene therapy technology platform. There are $12.5 million payments due for the first $100 million, $200 million, and $300 million in cumulative revenue from Vyjuvek. After that, no further payments are due.

There don't appear to be any meaningful data readouts on the horizon. Within the lung portfolio, Krystal Biotech has emphasized its alpha-1 antitrypsin (A1AT) program KB408 over its cystic fibrosis program KB407. That's a bit curious.

Although both could be very valuable, the cystic fibrosis program would be significantly more valuable – and a potential Vertex killer. That means KB407 could have over $10 billion in annual revenue potential. By comparison, KB408 could have annual revenue potential of roughly $2.5 billion to $5 billion.

Hey, maybe I'm splitting hairs. Success for either program would put each in the discussion of the world's bestselling drugs.

Krystal Biotech is also on track to earn regulatory approvals for Vyjuvek and launch in the European Union, United Kingdom, and Japan in 2025. The gross margin on sales in international markets would be noticeably lower, due to a combination of drug pricing regulations and the need to fly vials from a manufacturing facility in Pittsburgh to international markets. The Pittsburgh International Airport doesn't have direct flights to either region, although Krystal Biotech could charter special flights.

Management also stated it expects to launch Vyjuvek Eye as a separate product with a separate price point. That could add an additional $200 million to the franchise's estimated $1 billion peak annual revenue potential (company's estimate).

Forecast & Modeling Insights

(Increased.)

Solt DB Invest's current model makes the following assumptions:

- Full-year 2024 product revenue of $286.3 million vs. an updated Wall Street consensus of $237.4 million.

- Full-year 2024 gross margin of 86.4%.

- Full-year 2024 total operating expenses of $253 million, including R&D expense of $60.8 million, SG&A expense of $154.7 million, and settlement payments of $37.5 million.

- Full-year 2024 operating loss of $5.667 million.

Our price target and fair valuation is based on full-year 2026 revenue of at least $586 million. That is based on the following assumptions:

- Roughly half of individuals experience 100% target wound healing within 12 months, which reduces monthly vial consumption by nearly 50%.

- The peak annual revenue potential in the United States in 2024 dollars is $505.912 million.

- Launches in the European Union, United Kingdom, and Japan in 2025 and gradual ramp into 2026.

Our current model includes only marginal value from the remaining technology platform and pipeline.

As will be true for any biotech stock we cover, an acquisition can occur at a significant premium to the price target at any given time, since an acquisition accounts for future unrealized value.

If the HSV gene therapy platform fails to deliver meaningful results in lung programs, then that would swipe away a significant amount of value.

Margin of Safety & Allocation

Krystal Biotech is considered a Growth (Quality) position. The current modeled fair valuation for the company based on our 2024 model is below:

- Market close February 28: $163.08 per share

- Modeled Fair Valuation: $145.21 per share

- Allocation Range: Up to 10%

Krystal Biotech reported 28.293 million shares outstanding as of February 19, 2024. The modeled fair valuation above assumes 30.415 million shares outstanding, which is equivalent to 7.5% dilution.

Further Reading

- February 2024 press release announcing full-year 2023 results and business updates

- February 2024 regulatory filing (10-K) discussing full-year 2023 results and business updates

- February 2024 investor presentation

- November 2023 research note analyzing third-quarter 2023 operating results

- August 2023 research note discussing the departure of CCO Andy Orth and why I sold my position, previously 10% of my portfolio

.svg)

.svg)

.png)

.svg)

.svg)

.svg)