.svg)

Not everyone who hitched their wagon to NVIDIA is celebrating lately.

Oxford Nanopore signed an exclusive agreement to utilize NVIDIA's high-powered chips in its PromethION sequencers. It made sense. DNA sequencing (or, more accurately, the genome assembly part) is one of the few applications in biotech drowning in data. Integrating some of the world's most advanced chips directly into instruments simplified the workflow and time to results for scientists.

The downside is, if Uncle Sam bans exports of those advanced chips to certain countries, then you'll have to pause sales of your DNA sequencing instruments to customers in those countries. That little headwind forced Oxford Nanopore to limp out of 2023 and miss its revenue guidance. But it wasn't the only headwind.

The third-generation reader of genomes also announced the unceremonious end to the Emirati Genome Program (EGP). When the program began in 2021, the company expected it to generate £68 million over a three-year period. Instead, the EGP generated only £43.5 million in revenue for the business, or just 64% of its intended total.

Investors should be aware there's a significant discrepancy in revenue reported for the EGP. Official statements tally £55.8 million in lifetime revenue, whereas the company's preliminary full-year 2023 results show only £43.5 million. Solt DB Invest cannot make sense of the discrepancy at this time.

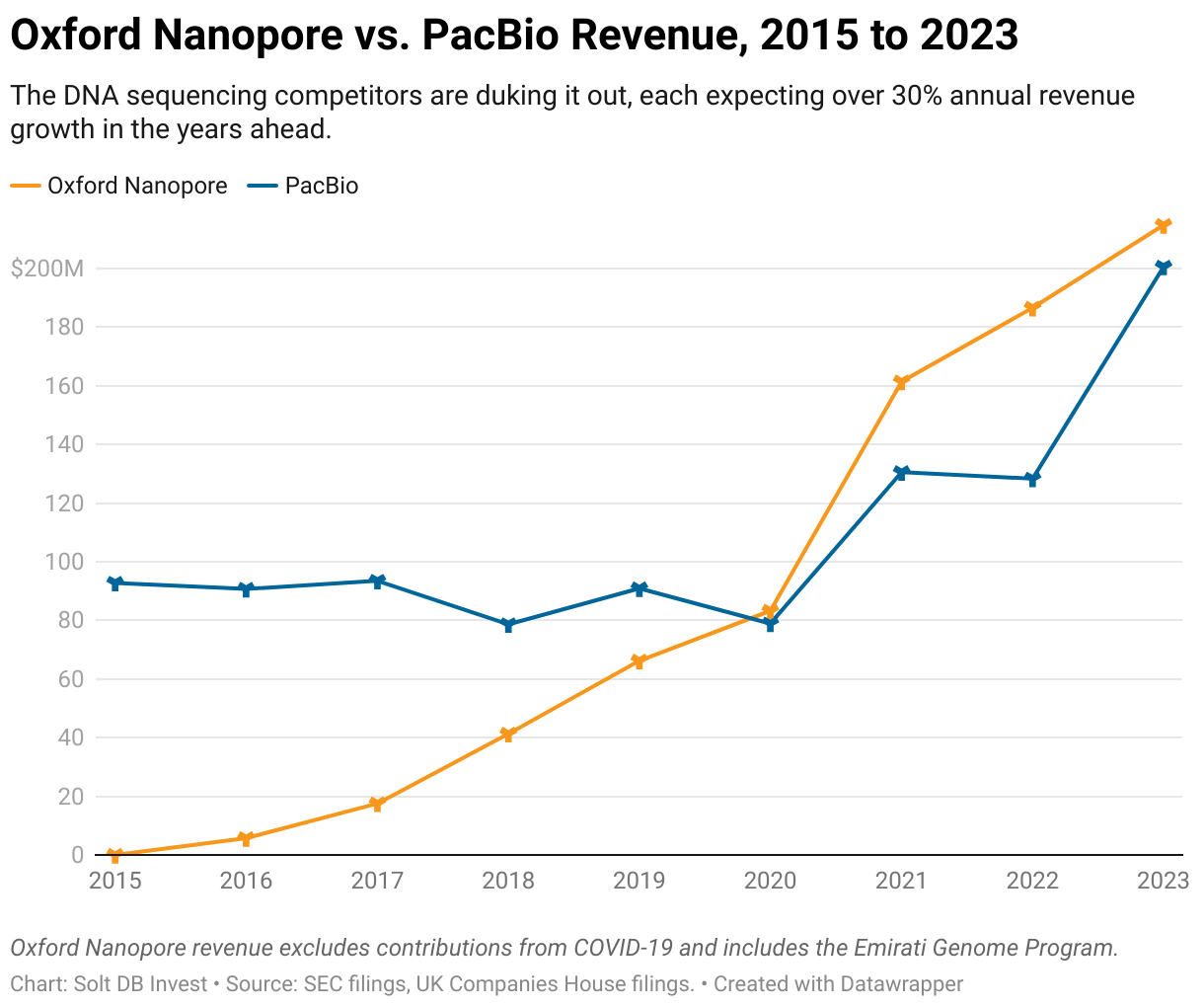

Oxford Nanopore always faced elevated geopolitical risks compared to Illumina and PacBio due to the geographic distribution of its revenue. The core business remains on relatively strong footing – surprisingly comparable to Illumina and well ahead of PacBio during the competitor's transition. Nonetheless, our modeled fair valuation has been reduced from our previous expectation.

Adjusting to a Year with No Adjustments

The business should be simpler to follow in 2024. That comes with lower overall revenue, but it still represents a solid base to build from in the next few years.

During the pandemic, investors had to do extra math to evaluate operations without the boost from COVID revenue. The same was true for the impact of the EGP, which was only expected to provide revenue for three years. It was smart and pragmatic for Oxford Nanopore to leverage these opportunities to fund the fledgling business, but these non-core activities complicated comparisons from one period to the next.

No more.

Investors will be able to focus solely on the core business in 2024. The company reports core operations as the life science research tools (LSRT) segment, which includes sales of instruments, consumables, and services. That's what matters for investors. The subtle shift will make it easier to gauge growth rates and progress for the underlying business.

Revenue growth is important for a growth-stage business. Obviously. But for a lab hardware company such as a DNA sequencing provider, it's important to see the quality of revenue improve as it scales. Oxford Nanopore is delivering.

The business expects roughly 75% of full-year 2023 revenue was generated from consumables. That's the highest-margin source of revenue for lab hardware companies, which typically generate low margins or lose money on instrument and services revenue. In fact, only Illumina, 10x Genomics, and Oxford Nanopore generate over 67% of total revenue from consumables. Only Oxford Nanopore is increasing that share.

Investors might expect the headwinds impacting the broader competitive landscape to hit the third-generation DNA sequencing provider, but Illumina is stumbling over mismanagement decisions (consumables were 68% of revenue in Q4 2024, down from over 71% historically) and 10x Genomics is taking its lumps to build its spatial imaging platform (consumables were 74% of revenue in Q4, down from 85% historically). In other words, Oxford Nanopore could exit 2024 as the lab hardware company with the most favorable revenue mix.

It expects to start 2024 with £467 million in cash, cash equivalents, and liquid investments ($593.5 million). Those "liquid investments" are doing some heavy lifting though, so expect dilution in 2025 or 2026 if market conditions improve or NVIDIA chooses to make an investment.

Forecast & Modeling Insights

(Reduced.)

Solt DB Invest is reducing its 2024 model to account for changes in expected EGP revenue and an industrywide slowdown in revenue growth. My model might be too pessimistic, but I'd rather err on the side of being too conservative.

Solt DB Invest now expects the following for its full-year 2024 model of Oxford Nanopore:

- Total revenue of £200.18 million ($254.410 million), down from a previous expectation of £217.760 million ($276.750 million).

- Total revenue growth of 27.5% from the prior-year period, which is significantly below the most recent growth rate of 39% for the core LSRT segment. This accounts for geopolitical headwinds and a temporary reduction in sales due to clinical challenges for nanopore sequencing tools.

- Gross margin of 57.5% for total revenue, down from a previous expectation of 60.0%. This reflects higher input costs and headwinds within the competitive landscape.

Oxford Nanopore continues to expect annualized growth of at least 30% through 2026. It expects to achieve LSRT gross margin of 65% in 2026, although that's expected to be driven by "improved manufacturing processes, recycling of electrical components and automation." That's certainly possible with scale, but investors need to see annual improvements before expecting such a leap. The Emirati Genome Program had lower margins, so the program's end will lead to an immediate boost of a few percentage points.

For reference, Illumina expects to achieve a gross margin of approximately 62% (down from a historical average near 70%) and 10x Genomics is currently delivering a gross margin of approximately 60% (down from a historical average of 75% or more).

PacBio is well behind and needs the new Revio platform to deliver significant improvements to consumables revenue generation. The peer has a historical gross margin of only 45% at its peak. That's a poor reference for the new technology platform, but it shows how far PacBio needs to go to earn its current valuation premium.

Margin of Safety & Allocation

Oxford Nanopore is considered a Growth (Quality) position. The current modeled fair valuation for the company based on our 2024 model is below:

- Market close January 26: p144.50 per share

- Modeled Fair Valuation: p169.50 per share

- Allocation Range: Up to 5%

Oxford Nanopore reported 7.762 million shares outstanding as of July 22, 2023. The modeled fair valuation above assumes 8.538 million shares outstanding, which is equivalent to 10% dilution.

Further Reading

- January 2024 press release announcing preliminary full-year 2023 operating results

- December 2022 research note providing modeling

- July 2022 research note introducing coverage of Oxford Nanopore, with an emphasis on the need to diversify from the Emirati Genome Program

- January 2021 press release announcing collaboration with NVIDIA

.svg)

.svg)

.png)

.svg)

.svg)

.svg)