.svg)

Necessity is the mother of invention. That's true in drug development, too.

If the goal of genetic medicines is to alter gene expression, then therapeutic payloads need to be delivered into the specific cells where gene expression occurs. It's tricky. Think about it: How does a drug administered into a patient's bloodstream find its way into the specific cell type required to have an effect – and avoid the "wrong" cell types that might result in dangerous side effects? That makes delivery the most important aspect of genetic medicines.

The problem of delivering genetic medicines to the liver has been solved thanks to Alnylam Pharmaceuticals. The RNA interference (RNAi) leader pioneered the use of GalNAc targeting ligands. The sugar binds to a special receptor on certain liver cells like a lock and key, which safely and selectively sneaks therapeutic cargoes into the liver.

The discovery of GalNAc was borne out of persistent safety issues for prior-generation genetic medicines. Alnylam Pharmaceuticals and its peers used to encapsulate RNAi payloads in lipid nanoparticles (LNP), but kept seeing worrying liver inflammation and even patient deaths. It found a way to stabilize RNAi payloads so they didn't need encapsulation, and then slapped GalNAc on it.

The key insight was that activating the receptor used by LNPs – low-density lipoprotein receptor (LDLR) – can trigger defense mechanisms that result in unacceptable side effects, whereas the receptor used by GalNAc sugars – asialoglycoprotein receptor (ASGPR) – does not.

It's curious, then, that Verve Therapeutics initially attempted to use outdated LNPs to deliver its PCSK9-disabling base editor into liver cells. Predictably, it led to worrisome side effects even at low doses. The company retooled the formulation of LNPs (to reduce safety issues of using LDLR docking) and slapped GalNAc on top (to enable ASGPR docking). Predictably, it appears to have worked.

.avif)

There are still some questions about how VERVE-102 will stack up in the competitive landscape. The data readout includes very immature data: 14 patients followed for up to 28 days and no data for higher-dose cohorts. The cohort held up by some analysts as potentially being competitive includes data from just four patients (or three patients if using a different time-value metric). For comparison, the three FDA-approved PCSK9 inhibitors have been administered to nearly 1,000,000 patients.

What does it all mean? Although early in the asset's development, early data for genetic medicines seems to translate into later-stage development relatively smoothly. That suggests VERVE-102 could eventually become another option for lowering LDL cholesterol ("bad cholesterol").

However, Verve Therapeutics is financially constrained. It cannot shepherd VERVE-102 from development through approval on its own. That makes a looming opt-in decision from Eli Lilly a key de-risking event for investors. The decision will determine if the base editing pioneer can develop additional assets, or must turn to layoffs and development pauses to push VERVE-102 through a phase 2 study. Even then it wouldn't be able to fund the required pivotal studies.

Preliminary Phase 1 Data for VERVE-102, Explained

Verve Therapeutics designed VERVE-102 to silence expression of the PCSK9 gene in the liver. The PCSK9 protein interferes with the body's ability to destroy LDL cholesterol (LDL-C), and humans with natural loss-of-function mutations are protected against the ill effects of high cholesterol.

.avif)

The April 2025 announcement includes an early look at dose escalation data for VERVE-102. Doctors administer a low dose to a group of patients, observe the effects, and then administer a higher dose to the next group of patients, observe the effects, and so on. The goal is to understand the therapeutic impact and safety across a range of doses, which helps to determine the recommended phase 2 dose (RP2D). A phase 1 study is designed to focus on safety, although early efficacy signals are often observed.

Although the phase 1 study is ongoing, the early results for safety and efficacy were promising. VERVE-102 appears to have so far avoided the worrisome side effects of its predecessor, VERVE-101. There were no grade 3 adverse events and, importantly, no cardiovascular side effects. There was also an early dose-dependent response, meaning higher doses led to greater reductions in LDL-C.

These results are generally in line with the competitive landscape, which offers patients LDL-C reductions between 50% to 60%.

It's important to understand that reductions in cholesterol are reported in different contexts. Some studies report LDL-C reductions for PCSK9 inhibitors administered to patients already receiving statins (these can make PCSK9 inhibitors appear to have less impact). Meanwhile, reductions are determined by the baseline level at the time a patient begins a study. Individuals with higher levels of LDL-C before beginning treatment can see greater reductions.

Studies of all three FDA-approved PCSK9 inhibitors designed for long-term follow-up or label expansions have demonstrated LDL-C reductions between 50% and 60%.

Next Steps for VERVE-102

Verve Therapeutics expects to share additional data from the phase 1 dose escalation study in late 2025. The data should include more patients in the reported cohorts, as well as initial data in the highest-dose cohort (0.7 mg/kg).

The company is already preparing to begin a phase 2 study of VERVE-102 in the second half of 2025. It can fund development through the mid-stage study with cash on hand, although it might need to turn to layoffs and pause development of other pipeline assets to do so.

Finally, the base editing pioneer will provide a data package to Eli Lilly, which will inform its opt-in decision. The world's largest drug developer can fund 33% of development costs for VERVE-102 and split future profits from U.S. sales 50/50. Given the size of pivotal studies required, investors shouldn't be surprised if Verve Therapeutics gives up more control in exchange for a more equitable split of development costs. It'll be difficult for the precommercial company to fund 67% of development costs.

Eli Lilly is expected to make a go/no-go decision in the second half of 2025. Investors can expect the decision to hinge on commercial dynamics in the PCSK9 market.

Commercial Landscape for PCSK9 Inhibitors

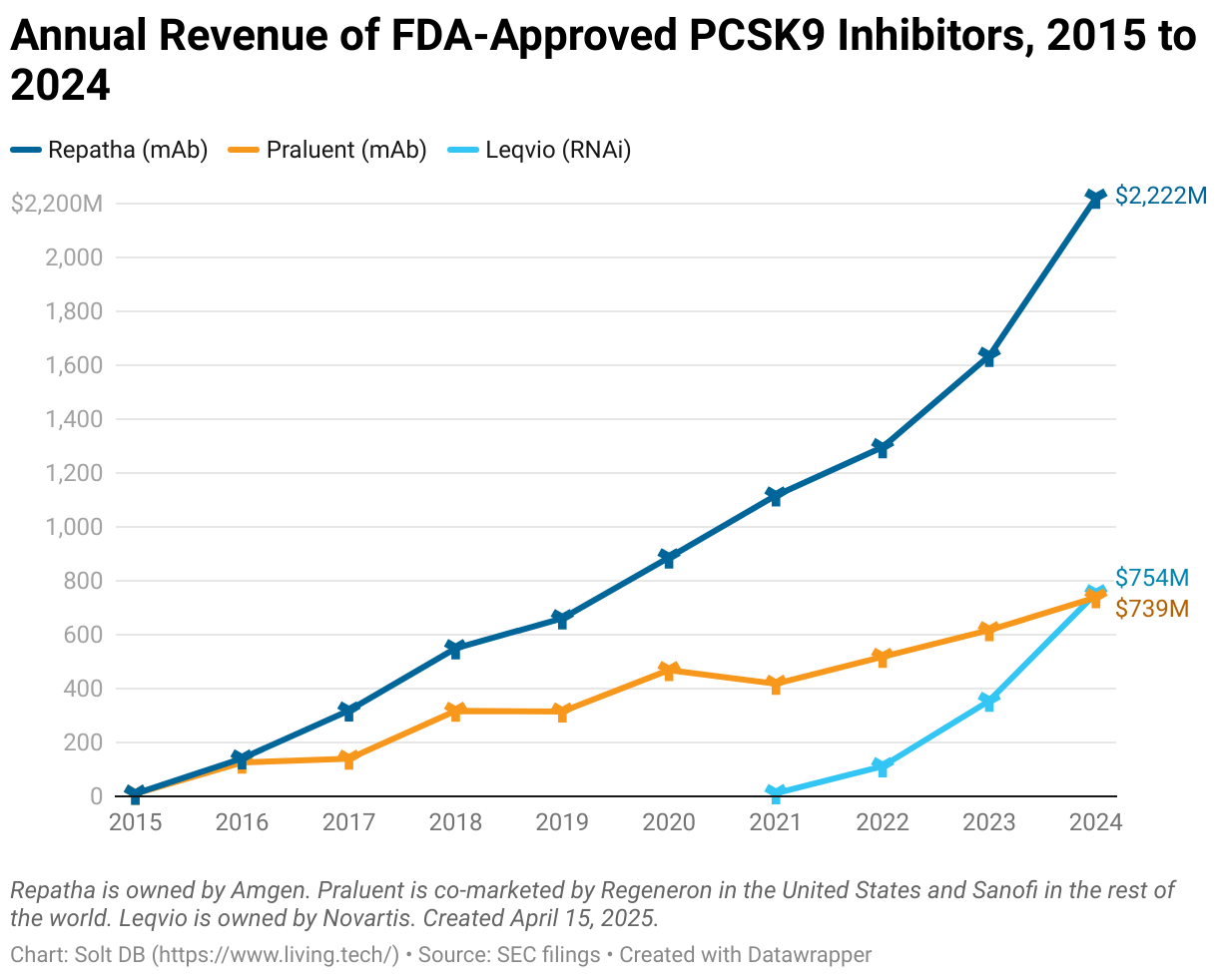

The market for PCSK9 inhibitors is relatively young, which has (so far) allowed all three approved drug products to consistently grow revenue in recent years. The trio combined for $3.7 billion in revenue in 2024, up from $2.6 billion in 2023 and roughly double the $1.9 billion generated in 2022.

The antibody drug Repatha from Amgen dominates the market. It generated $2.2 billion in global revenue last year. Fellow antibody drug Praluent from Regeneron (United States) and Sanofi (rest of world) delivered a respectable $739 million in 2024 sales, but it's grown "only" 42% since 2022.

Meanwhile, a favorably broad approval in heart disease for RNAi drug Leqvio from Novartis has catalyzed rapid growth in recent years. The genetic medicine generated $754 million in revenue last year, more than double the prior-year total. Leqvio will become the world's first blockbuster RNAi drug product.

In other words, there's a large and established market opportunity for PCSK9 inhibitors. That helps to reduce uncertainty that typically clouds an early-stage asset such as VERVE-102. But determining the commercial opportunity is a little trickier in this case.

The cardiometabolic pipeline of Verve Therapeutics – not just VERVE-102 – faces several unique commercial risks. These assets can likely only match the performance of existing treatments, the company cannot develop or commercialize these assets without a partner, and existing treatments are likely to have generic options before the first base editor earns regulatory approval.

Loss-of-Function is about matching competition, not besting it

As explained in the March 2025 research note for Arrowhead Pharmaceuticals, genetic medicines designed to create loss-of-function (LoF) mutations have a ceiling. Unlike cancer treatments, where it's almost always possible to increase efficacy and reduce side effects compared to the competition, LoF treatments either recreate a beneficial genotype or they don't. It's more about matching the competition than besting it.

For example, the current crop of PCSK9 inhibitors can each reduce LDL cholesterol by between 50% and 60% depending on the context. Preliminary phase 1 results show VERVE-102 is hitting the same (predictable) level, which is good, but it will be difficult to beat that by a meaningful margin. Even if the asset did drive steeper reductions in bad cholesterol, it's not clear that it would lead to clinical benefit for patients.

Infrequently-dosed genetic medicines have one potential advantage: convenience. Whereas antibodies are dosed every two weeks (Praluent) or four weeks (Repatha), Leqvio is dosed every 24 weeks. Patients taking existing treatments can also stop showing up to appointments, which is counted as a discontinuation of treatment. That wouldn't be a problem for VERVE-102 – but it will complicate pricing dynamics.

Development and commercialization are prohibitively expensive

Investors are awaiting Eli Lilly's decision on its option to control VERVE-102 development, but partnering the asset might be the only option. That will be true for all the company's cardiometabolic programs.

As a general rule, the more common the disease the larger and the longer the pivotal clinical trial must be. High cholesterol is pretty common. Therefore, drug candidates need to be studied in thousands of patients for years before earning regulatory approval.

A pivotal study for a common cancer typically enrolls between 500 and 1,000 patients. The pivotal heart disease studies for Leqvio enrolled 3,178 patients. Praluent snagged an approval with a 2,341-patient study. The lead pivotal studies for Repatha enrolled 27,564 patients. Real-world studies to collect even longer-term data for these assets are enrolling up to 60,000 patients across 50 countries right now.

For comparison, Verve Therapeutics has released partial short-term data for 14 total patients given VERVE-102 for up to 28 days.

Precommercial drug developers simply don't have the financial heft to conduct megastudies on their own. In fact, it's never happened before. That means Verve Therapeutics needs Eli Lilly (or another large pharma) to help shoulder the financial burden of development for its cardiometabolic programs. Even then, successful development isn't guaranteed.

In September 2022, Ionis Pharmaceuticals was forced to terminate development of its PCSK9 inhibitor candidate ION449 after a successful phase 2 study. The reason: the reduction in LDL-C levels missed a prespecified benchmark AstraZeneca established to justify funding pivotal studies. The reduction demonstrated in the phase 2 study: 62.3% compared to placebo.

The same general rule also applies to commercial development of drug products. The more common the disease the larger the sales team needs to be. Everything about drug launch – manufacturing, labeling, distribution, reimbursement, sales – is more expensive. It's another good reason to find a partner before pivotal studies at the latest.

Generics (biosimilars) are on the way

The major patents protecting Repatha and Praluent expire in 2028 and 2029, respectively. Although Amgen and Sanofi might attempt to launch longer-lasting versions to extend brand life, investors and doctors can expect PCSK9 inhibitor biosimilars to launch by the end of the decade – well before VERVE-102 earns regulatory approval.

This creates an industry-first dynamic. Buckle up!

An infrequently-dosed genetic medicine has never launched into a market that had generic treatment options. That's because almost every genetic medicine approved to date has launched in rare diseases. There often weren't any treatment options, let alone generics.

How does this dynamic impact the pricing of VERVE-102? The bottom of the market would exert a strong gravitational pull. For reference, Leqvio and Repatha today cost less than $9,800 per year. Generics could launch at a 25% discount and gradually erode pricing over time.

This suggests to me that the $1 million to $3 million price tags slapped onto other gene therapies and gene editors are well outside the realm of possibility for VERVE-102. The base editor might need to be priced closer to $200,000 – and maybe half that eventually (in today's dollars anyway).

Verve Therapeutics is likely to argue a higher price is warranted because "one-and-done" base editors won't have discontinuation rates, which is a benefit for the healthcare system. Whether commercial insurance, government programs, and pharmacy benefit managers (PBMs) agree to cover a much higher-priced PCSK9 inhibitor given multiple effective options remains an open question.

The market opportunity is large enough to support a (relatively) low-cost, mass-produced genetic medicine. I might even favor adding it to the drinking water (something has to replace the fluoride). But Verve Therapeutics might have to launch in the heart disease market to justify the commercial costs, which might delay an approval by years.

Modeling Insights

(Refined.)

My model has been updated to reflect the most recent share count. The fair valuation of Verve Therapeutics hasn't changed – it's still $1.183 billion – as the prior model already factored in a successful phase 1 study for the lead drug candidate.

However, investors should acknowledge the company is uncomfortably binary ahead of the looming Eli Lilly decision.

It will hurt (a lot) if Eli Lilly decides not to pursue development of VERVE-102. Although Verve Therapeutics can fund development of the asset through a planned phase 2 study, it wouldn't be pretty. It would also be left with no cash and the need to fund an even more expensive slate of pivotal studies – a vulnerable position that management will try to avoid.

Other options include courting another large pharma interested in cardiometabolic disorders. That leaves a dwindling list of players in the PCSK9 landscape. In addition to companies with an approved treatment (Amgen, Sanofi, Novartis), others like Merck and AstraZeneca are developing oral treatment options that have also hit the 50% to 60% LDL-C reduction sweet spot.

That said, there's relatively little risk and expense for Eli Lilly to opt-in to VERVE-102 development ahead of the phase 2 study. A "go" decision is the most likely outcome. A new direct-to-patient distribution platform being tested by the large pharma, designed to navigate commercial dynamics for its obesity assets, could also be leveraged for VERVE-102 down the road.

It might still walk away before pivotal studies, but an opt-in decision would allow Verve Therapeutics to get another asset or two through early clinical trials. That would provide cover, if needed, to pivot away from VERVE-102.

Margin of Safety & Allocation

Verve Therapeutics is considered a Growth (Speculative) position. The estimated fair valuation based on my current model is below:

- Market close April 15: $4.97 per share

- Modeled Fair Valuation: $11.58 per share

- Allocation Range: Up to 2.5%

Verve Therapeutics reported 88.796 million shares outstanding as of February 20, 2025. The modeled fair valuation above assumes 102.115 million shares outstanding, which is equivalent to 15% dilution.

Further Reading

- April 2025 press release announcing preliminary phase 1 results

- February 2025 regulatory filing (10-K) detailing the state of the business

- April 2024 research note analyzing the decision to swap VERVE-101 with VERVE-102

.svg)

.svg)

.png)

.svg)

.svg)

.svg)