.svg)

Want an email alert every time a Finch Trade goes live? Sign up in your profile.

An uncomfortably short cash runway and aggressive clinical posture makes 2026 a make or break year for Coherus Oncology. Can it generate enough buzz with early-stage data readouts to earn a higher valuation? Current guidance (prior to the full-year 2025 earnings call) expects five data readouts by the end of 2026. The first two will be important – and risky.

By the middle of the year, investors can expect preliminary data for the CCR8 inhibitor tagmokitug plus toripalimab in gastric cancer and head and neck squamous cell carcinoma (HNSCC). These two tumor types are predicted to be most dependent on CCR8 overexpression in the tumor microenvironment.

On the one hand, LaNova Medicine's competing asset has already generated promising data for a CCR8 inhibitor in gastric cancer. That's a good proof of concept for Coherus. On the other hand, that competing asset set a very high bar. Falling short with tagmokitug right out of the gate would raise questions about the company's development strategy and ability to survive.

LM-108 demonstrated an objective response rate (ORR) of 36% (13/36) in the overall patient population of its study. The hypothesis for CCR8 inhibition is that disrupting the tumor resistance mechanism can turn cold tumors hot, meaning patients who already stopped responding to PD-1 inhibitors could benefit from treatment again. That means later treatment lines might have different response rates.

Indeed, LM-108 demonstrated an ORR of 63% (7/11) in second-line patients. If only patients with high CCR8 expression are included, then the ORR jumps to 87.5% (7/8). These are small studies, but provide a glimpse of the clinical promise of the drug class.

To be fair, phase 1 data aren't interpretable for efficacy. Coherus might only report early signs of objective responses, or might not have evaluated patients for the same duration as LaNova's data cutoff. That won't stop investors from trying. If tagmokitug is assumed to be well behind LM-108, then the company's data-rich year might get off to a rocky start.

The Transaction

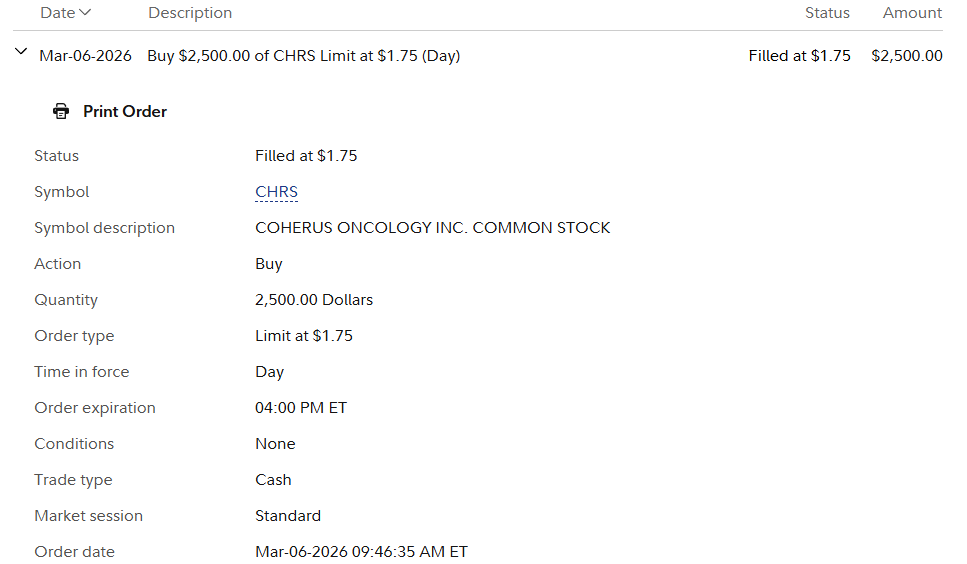

Coherus Oncology is considered a Future Compounder position. I purchased 1,428.6 shares at $1.75 per share on March 6, 2026. The total transaction value was $2,500.

Outperformance Scenarios

Investing in individual stocks can be reduced to a simple question: "If I invest $1 in this individual stock at this price, will it outperform an equal passive investment in the S&P 500 at this level?"

If you keep emotions and expectations in check, then you might be surprised to learn you don't need to swing for the fences.

Here's how shares of Coherus Oncology will need to perform for the money invested in this Finch Trade to outperform passive investing in the S&P 500 in the next five years.

Assumptions:

- The S&P 500 index gains 10% per year with dividends included – its historical average since 1990.

- Coherus Oncology averages 10.5% dilution per year in the next five years – equivalent to a standard 17.5% dilutive event every 18 months. This means shares need to gain 61% in the next five years, but the market cap would need to grow by 131% in that span from $261 million to $603 million.

- S&P 500 closing level on March 6, 2026 = 6,742

- Coherus Oncology purchase price on March 6, 2026 = $1.75 per share

Margin of Safety & Allocation

Coherus Oncology is considered a Future Compounder position. The estimated fair valuation based on my current model is below:

- Market close March 6: $1.82 per share

- Modeled Fair Valuation: $2.97 per share

- Allocation Range: Up to 10%

Coherus Oncology has at least 149.471 million shares outstanding as of late February 2026. The modeled fair valuation above (prior to the full-year 2025 earnings call) assumes 157.605 million shares outstanding, which is equivalent to 2.5% dilution.

Further Reading

- February 2026 Member Digest previewing Q4 2025 earnings season across the coverage ecosystem.

.svg)

.svg)

.avif)

.png)

.svg)

.svg)

.svg)