What Went Wrong at Invitae

Invitae plowed through the easy-money era with a growth-at-all-costs business model. It worked – until it didn't.

CEO Sean George, who will step down immediately, admitted on quarterly conference calls to prioritizing revenue growth above all other metrics. Gross margin (the profitability of revenue), operating margin (the profitability of revenue plus overhead), and net margin (the profitability of revenue plus overhead plus financing costs) were secondary concerns. That backfired.

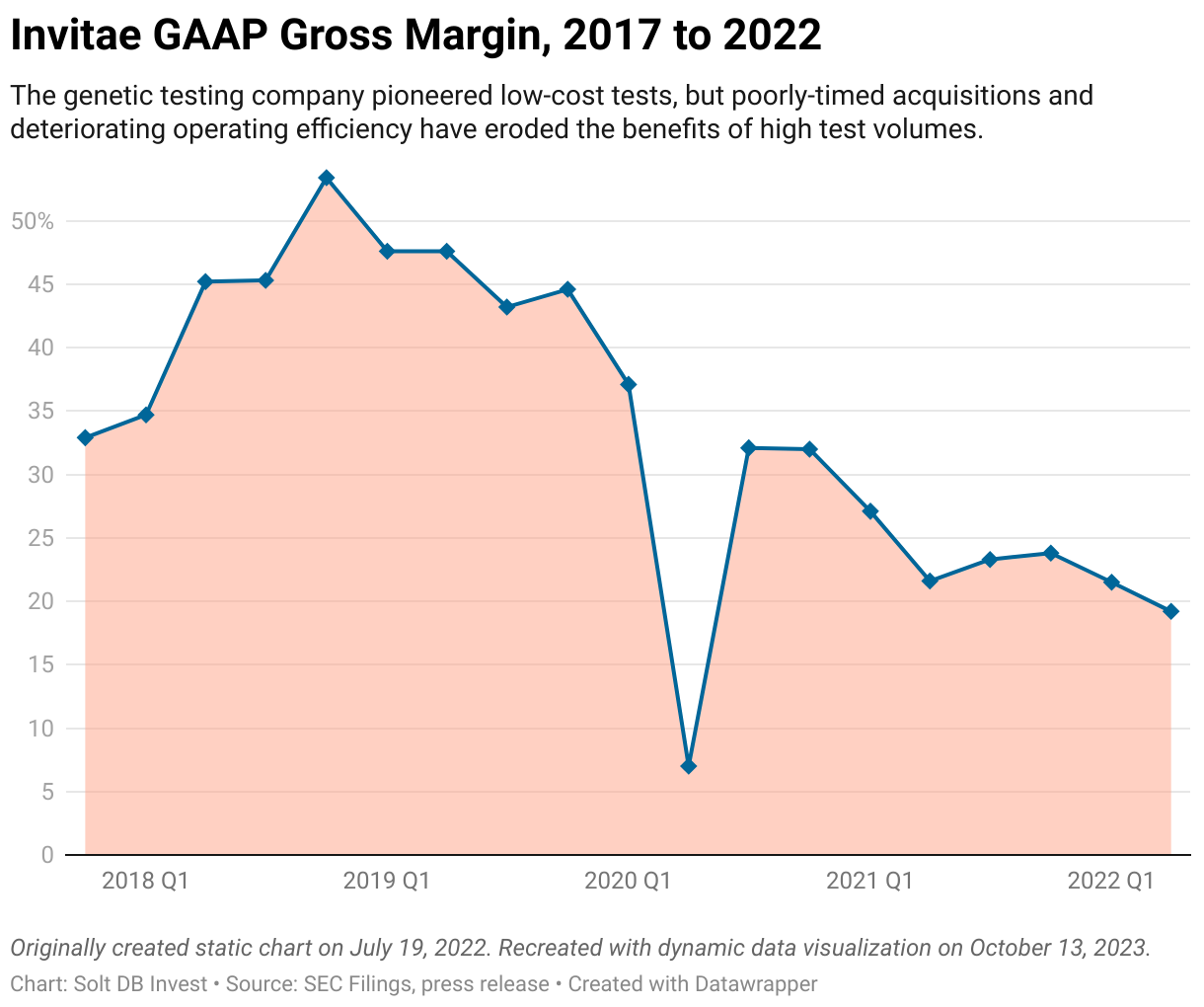

The business appeared to be on the right track in late 2018 and early 2019. Revenue was growing at a healthy clip compared to year-ago periods. Importantly, the business was benefitting from its scale. Gross margins were improving as the business grew larger. That may be taken for granted in software businesses, but it doesn't always happen in hard sciences when physical products are involved. As synthetic biology godfather Drew Endy puts it, software companies are primarily concerned with joules (energy) and bits (information). Biotech companies must focus on joules, bits, and atoms (matter).

The progress in scale had fallen apart in recent years. Invitae went on an acquisition spree to round out the technology stack. However, a combination of poor integration, bloated payrolls, and lackluster reimbursements from insurance programs have weighed on gross margin. The company's preliminary second-quarter 2022 operating results suggest GAAP gross margin will be 18% to 19%, by far the lowest of the last five years when the pandemic quarter is excluded.

How does a deteriorating gross margin impact day-to-day operations, or your investment as an individual investor? Let's put it into perspective.

- Invitae expects Q2 2022 revenue of $136 million at a gross margin of 19%. That equates to a gross profit of $26 million.

- Invitae generated Q4 2018 revenue of $45 million at a gross margin of 53.5%. That equated to a gross profit of $24 million.

In other words, the growth-at-all-costs business model drove a 3x increase in revenue during the comparison period in the bullet points above, but only a 7% increase in gross profit. Investors clamored over revenue growth, but received no tangible, real-world benefits in return. The only thing driving the company's share price higher was the era of easy money and favorable coverage from FinTwit and Cathie Wood.

Gross profit is what trickles down the income statement to self-fund operating overhead. Invitae scaled expenses to focus on growing revenue. Of course, without a commensurate increase in gross profit, the business had to borrow money it didn't have to pay for that pursuit of growth. The money was borrowed from Softbank (the future), existing shareholders (dilutive public stock offerings), a noisy internet (publications that have anyone with a pulse write articles on topics they don't understand), and the Federal Reserve (money machine go brrrr). The bill always comes due.

What's Next For Invitae

Invitae was always going to have to eat shit. It's finally choosing to stop nibbling. A handful of announcements from July 18, 2022:

- CEO stepping down: Sean George will step down effective immediately. He'll be replaced by COO Kenneth Knight, while co-founder and former CEO Randy Scott will return as chairman of the board.

- Layoffs: If you cannot improve gross margin quickly, then you need to reduce expenses down the income statement. The genetic testing company announced it would cut 1,000 jobs from its bloated operations to save costs and reduce cash burn. Invitae reported 3,000 employees at the end of 2021, according to SEC filings.

- Reduced revenue guidance: Invitae previously guided to hit 40% annual revenue growth for the foreseeable future. It now expects roughly $520 million in full-year 2022 revenue, or year-over-year growth of 13%. It expects 2023 to be a "transition year" and for annual sales growth of 15% to 25% beginning in 2024. The difference between Wall Street estimates for 2023 revenue ($830 million) and the company's new expectations (~$520 million) is significant.

- Exiting non-core businesses: Invitae expects to deprioritize and exit non-core markets, which means focusing on hereditary cancer testing and building patient-centric genome management solutions.

The very last point is important for investors clinging on for dear life. Pre-pivot and post-pivot Invitae have both shared a vision for providing genome management solutions as a major source of future revenue growth. It's the stuff of investor presentation legend. Hockey stick chart stuff.

Before getting too carried away it's important to ask a simple question: Will it work? Perhaps another way to ask that, "Is Randy Scott wrong?" The rephrasing certainly tempers my answer.

But let's think about it objectively. At present, Invitae possesses genetic data of questionable value. Individuals who use the company's products or services generally have a handful of genes tested. They do not have their full genome sequenced. Is it valuable to have handfuls of gene clusters, for handfuls of diseases, for handfuls of patients? Is that valuable to, say, Merck or Roche or Johnson & Johnson? Probably not.

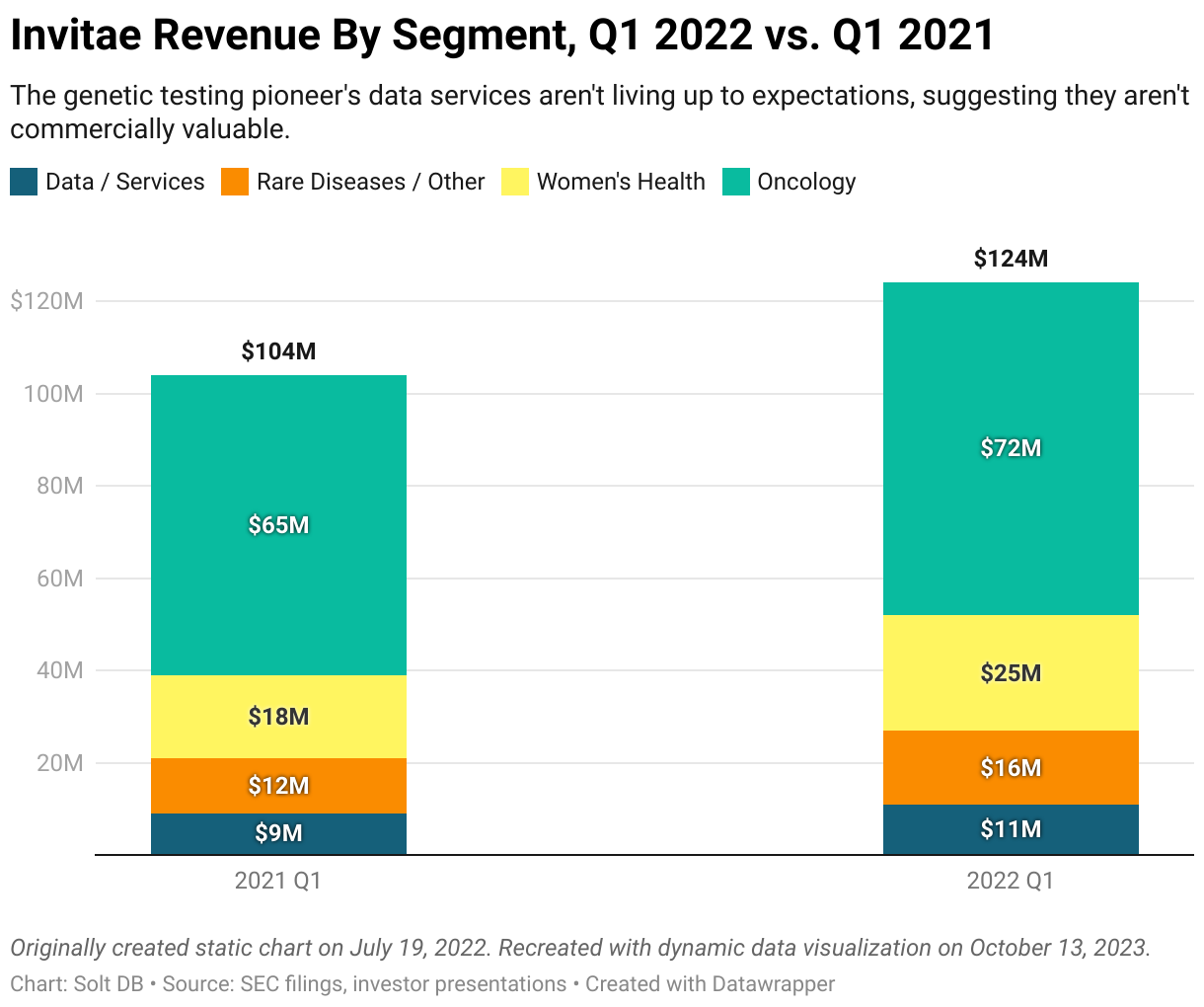

The data back up this sentiment. Invitae grew data services revenue from $9 million in Q1 2021 to only $11 million in Q1 2022. That's despite adding nearly 800,000 patient records to data sharing in that span. That's also despite increasing the number of commercial partners from 106 at the end of 2020 to 206 at the beginning of 2022. Genetic sequencing is increasingly being used to bin patient populations and subpopulations during clinical trials, so generating only $11 million per quarter from the data hoard isn't terribly impressive. That's likely because of the blunt reality that the data aren't that valuable, as explained above.

Can Invitae Survive?

The business called in some heavy hitters to right the ship. COO Kenneth Knight has a much deeper business background than did Sean George (who's a great scientist and had an admirable vision), while Randy Scott is one of the OGs of the genetic testing industry. Unfortunately, Invitae has a lot of ground to make up.

- GAAP gross margin is still terrible. It needs to increase from 20% to at least 60% for the business to become sustainable. It's important to point out Invitae reports non-GAAP gross margin, which makes certain adjustments and excludes certain costs. Investors shouldn't pay much attention to non-GAAP gross margin.

- Massive write-offs are likely on the horizon. Invitae became bloated through numerous acquisitions as it hyped the flywheel model. And hey, I drank from that Kool-Aid during summer 2021, too. Investors can expect a multi-hundred-million dollar write-off or two in the next 12 to 18 months. Such a move would result in a one-time hit to earnings, but only on paper. It would also shrink the gap (pun intended) between GAAP and non-GAAP gross margin by removing some of those excluded items from the calculation for good. Painful, but necessary.

- Liquid biopsy tools for personalized cancer monitoring, minimal residual disease, and other related applications were always important for the future of the business. They may now dictate whether it survives. The bad news is Invitae is pretty late to a very crowded competitive landscape and has the wrong commercial infrastructure in place for those tools. The good news is it has some pretty good tools from the Archer Dx acquisition. Will that be enough? I think the objective answer is that Invitae will not become a leader here (it will be trampled by Guardant Health and Exact Sciences), but could become an important mid-tier player. Not the most invigorating best-case scenario I suppose.

The best read in the immediate aftermath of the pivot is that Invitae is positioning itself for an acquisition. Investors should temper their expectations, though. It's a Hail Mary attempt to salvage value from what was built in the last decade.

The business is reducing headcount by one-third, focusing on core products, and furiously attempting to reduce cash burn to make itself more attractive for a potential suitor. After all, who the hell wants to acquire a bloated business in a commodity space for the privilege of losing $150 million every three months?

Exact Sciences was rumored to be interested in acquiring Invitae in 2021, but that rumor was never confirmed. In fact, the company's own actions – acquiring the already-profitable PreventionGenetics, which could be easily slotted into existing commercial infrastructure and methodically scaled up – directly refute the idea it ever considered acquiring Invitae.

Exact Sciences may be interested for the right price, at the right time, in the next 36 months. But that price might be disappointing for investors. Invitae may not have many other options -- and it has virtually no bargaining power. Would-be acquirers understand that.

What's an Attractive Entry?

Invitae is not recommended for investment.

For those who brave the turbulent waters, it should be among the smallest positions in a portfolio.

There are certain milestones that investors can use to gauge progress in the upcoming turnaround. To be successful or become attractive for an acquisition, Invitae needs to:

- Sharply reduce cash burn. The new pivot plans to save $326 million per year in non-GAAP costs. The cost savings are expected to be fully realized by 2023. It's important to point out that non-GAAP cost savings include non-cash stock options, which is to be expected when you hand pink slips to one-third of your workforce. Invitae plans to burn $600 million to $650 million in cash in 2022 and another $225 million to $275 million in 2023. That may not be enough to attract a suitor – or survive beyond 2024.

- Improve gross margin. Invitae desperately needs to improve GAAP gross margin. Ideally, the business would achieve at least 60% gross margin, but that may not be possible in the competitive landscape. The blunt reality is there isn't anything special about the products or services offered by Invitae compared to the next-closest peer.

Investors should ground themselves either way. Invitae is unlikely to earn a sharply higher market valuation any time soon. It's a cash hungry business (and will remain one) during a period when financial conditions are tightening overnight by historical standards. That's not a good position to be in.

Take any valuation metrics you were clinging to and throw them out the window. Invitae is far enough from profitability and has lackluster growth ahead, which means it probably deserves to trade at less than 1x revenue. That means a market cap of less than $500 million, or a share price of $2 or less.

An acquisition in 2023 or 2024 may come at a surprisingly low multiple, too. Oh, and don't forget, Softbank gets paid before you. You almost certainly won't be making your money back in any acquisition scenario.

Ol' Maxxie's Position

Here's my attempt to not nibble: I whiffed on Invitae in May 2021. I caved to peer pressure after years of shunning the growth-at-all-costs business model. By investing days before Q1 2021 operating results were announced, I invested on the assumption the negative trend in GAAP gross margin was a temporary hangover from the pandemic. Instead, GAAP gross margin continued to deteriorate to multi-year lows in Q1 2021 and decline significantly in the next year. My timing was terrible.

Although it only amounted to a less than 3% allocation in my portfolio, I ate a roughly 80% loss on my cost basis for the position when I sold only 12 months later.

I'm a long-term investor, but sometimes you need to cut your losses and move on. This is why it's important to understand appropriate allocations and attractive entry points, which is information Solt DB Invest provides for biotech stocks. It matters now more than ever with turbulent markets bearing down upon us.

.svg)

.jpg)

.svg)

.svg)

%20(squoosh).jpg)

%20(squoosh).jpg)

.svg)

.svg)

.svg)