The synthetic biology pioneer has been chronically mismanaged in the decade since pivoting away from biofuels. Despite severely overpromising and underdelivering, the management team has faced almost no consequences.

Amyris keeps selling the dream. The little guy keeps paying the price.

The synthetic biology pioneer has chronically overpromised and underdelivered to investors and partners. This is not a bold observation, but it has become apparent that the depth, longevity, and seriousness of the problem is not fully appreciated by all stakeholders.

This behavior is enabled by many individual failures. The media failed to hold the business and its executives accountable, prioritizing pageviews and innovation porn over competent and critical reporting. Institutional investors failed to conduct proper due diligence in the business, extending legitimacy to an incompetent management team. The board of directors failed to remove a chief executive officer who has mismanaged the company for over a decade, delivering an all-time share loss of 99%. Securities regulators and financial investigators sat idle through it all.

Make no mistake: This is not due to the difficulty of bringing new technologies to market, or the inability to forecast the future with perfect accuracy. Amyris has knowingly and intentionally misled investors for years and, at times, manipulated financial numbers and markets.

There have been no consequences.

Need more finch? Here's our newsletter.

Welcome to The Voyage!

Oops! Something went wrong while submitting the form.

Selling the Dream

"The proper response to fakeness is not to ineffectually lob rocks at palace windows, but to coherently and ceaselessly articulate the problems with the dominant institutions. To stand for and not simply against."

Ryan Holiday, Trust Me, I'm Lying

Amyris is one of the pioneers of synthetic biology. The company's roots trace back to the Keasling lab and the development of a microbial bioprocess to produce artemisinic acid, a precursor to an anti-malarial ingredient typically harvested from plants. The team flexed its muscle by leveraging deep knowledge of isoprenoid metabolic pathways, which led to the company's flagship ingredient farnesene. The vertically integrated technology platform has yielded unique bioprocesses for ingredients across flavors and fragrances (F&F), emollients, and nutrition.

Whereas the technology platform helped to pioneer synthetic biology approaches for industrial biotech, the management team has pioneered the synbio shuffle.

Amyris' operations in the last decade have shifted from ingredient to ingredient, market to market, and partnership to partnership. Oftentimes, the defining characteristic of each new ingredient is the hype that can be generated for the next quarterly report.

Today the business primarily generates product revenue from wholly-owned consumer brands, a zero-calorie sweetener, and customer-contracted F&F molecules. There are grandiose promises for the current portfolio, just as there have been for each version of the portfolio in the last decade. Almost all ingredients and derivative products previously held up as the primary source of long-term revenue growth are no longer in development. Newer investors might not be aware of the exhaustive list:

malaria treatments, pharmaceutical ingredients, the microPharm technology platform, renewable transportation fuels, farnesene-based liquid rubber, hydrogenated styrenic farnesene copolymer, lubricants, solvents (Myralene), bulk ingredients for specialty markets, F&F molecules, direct-to-consumer hand cleaners (Muck Daddy), hand sanitizers, direct-to-consumer personal brands, vitamins, sweeteners, nutritional ingredients, RNA vaccines, cannabinoids, ... and more

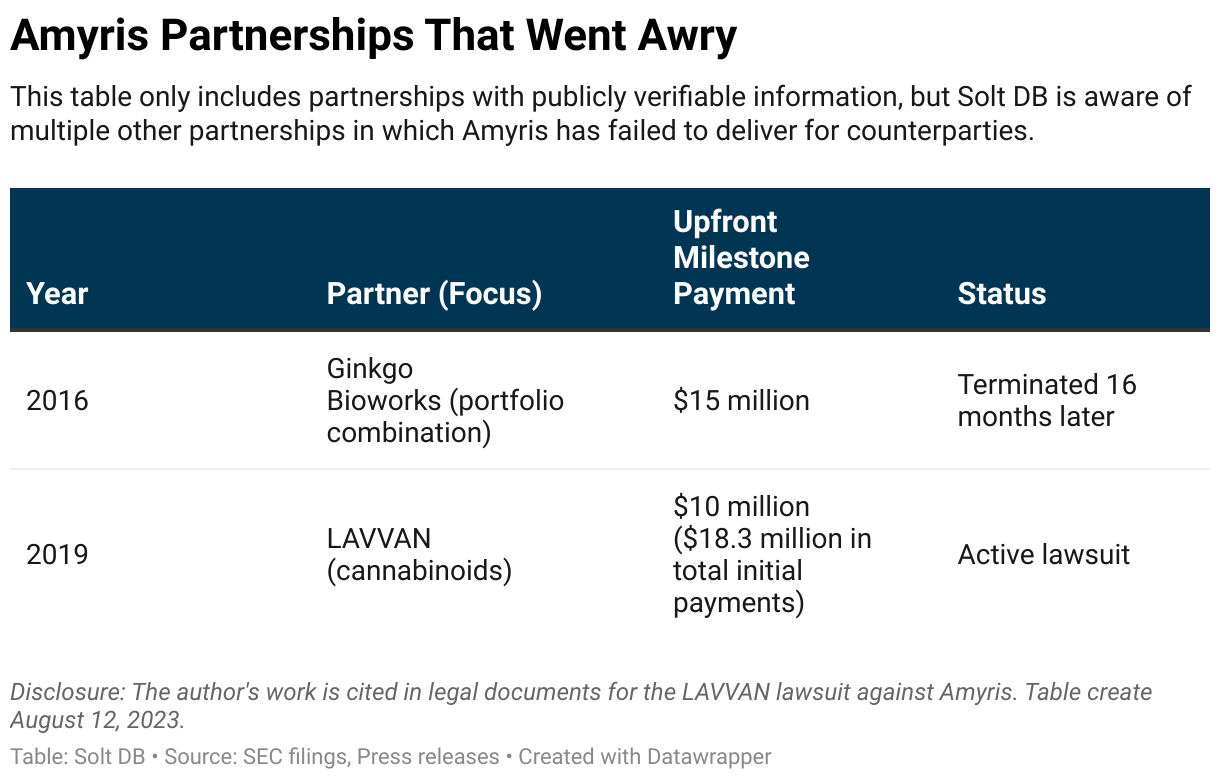

Management cannot pivot and redirect Wall Street's gaze alone. Partnerships for significant pivots or trendy molecules are sought for the ability to bring in an upfront milestone payment, but are often quickly deprioritized or discarded.

For example, Amyris and LAVVAN announced a partnership in 2019 to develop and commercialize cultured cannabinoids. Amyris continuously pointed investors to the $300 million in potential milestone payments as part of the collaboration. However, it never delivered on technical aspects within the partnership and has attempted to commercialize cannabinoids independently.

LAVVAN filed an $881 million lawsuit against Amyris alleging patent infringement and trade secret misappropriation relating to cannabinoids. For disclosure, my work is cited within legal documents related to the case. In September 2022, the United States Court of Appeals 2nd Circuit ruled against Amyris' attempt to send the litigation to arbitration. The company doesn't have enough cash to pay even a fraction of a potential fine or settlement.

Amyris' strategic drift within ingredients and partnerships is compounded by intentionally false and misleading statements from management.

These are not near misses. Nor are these intentionally false and misleading statements rare occurrences.

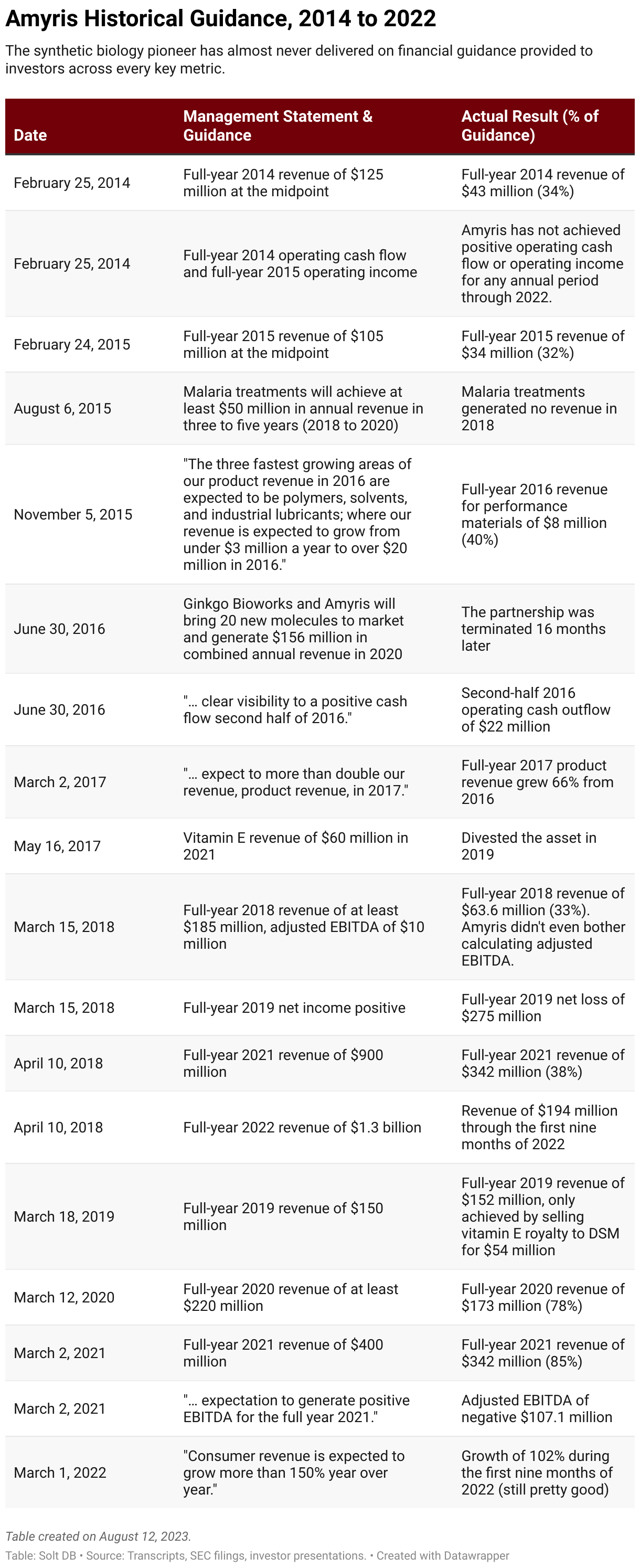

CEO John Melo has told investors the business would generate positive net income in the subsequent fiscal year, only to deliver a net loss of $275 million. Or guided for revenue of $190 million at the midpoint, only to deliver $63.6 million.

Consider historical guidance for revenue, adjusted EBITDA, cash flows, net income, and other metrics for each fiscal year dating back to 2014 when Amyris was first beginning to pivot away from biofuels.

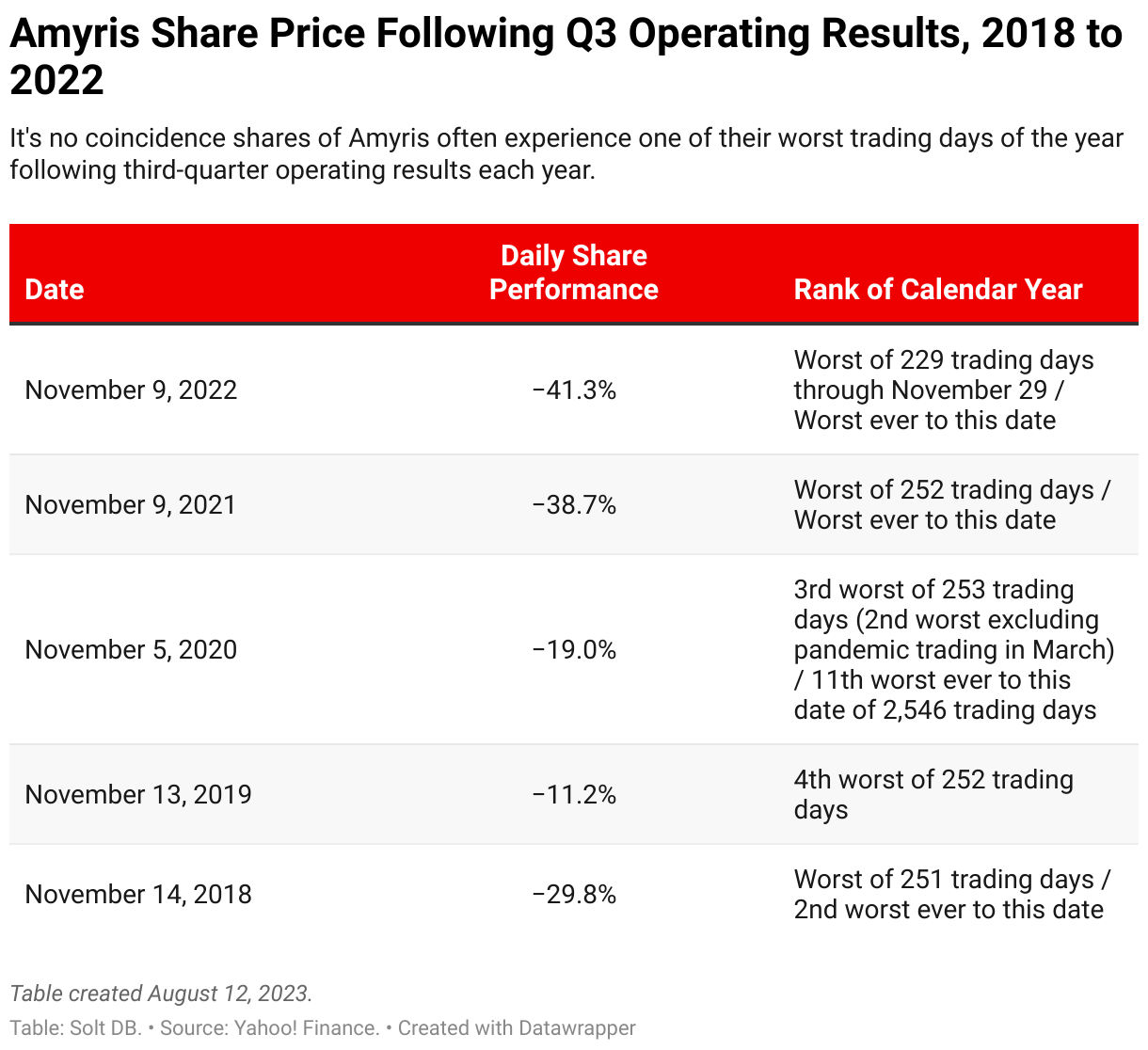

Management has perfected not only the announcement of misleading guidance, but maximizing its utility to the business. CEO John Melo strings investors along throughout the year regardless of how much ground the business needs to cover to meet guidance for the year. It always unravels in November when third-quarter operating results are announced. Without fail, some unforeseen event occurs, and guidance must be reduced, leaving markets with only a few weeks remaining in the calendar year to adapt.

If it wasn't enabled by intentionally misleading statements, then the ability to captivate investors would be quite impressive.

Nonetheless, it's no mistake Amyris shares plunge shortly after third-quarter operating results are announced every November – often experiencing their worst trading day of the year.

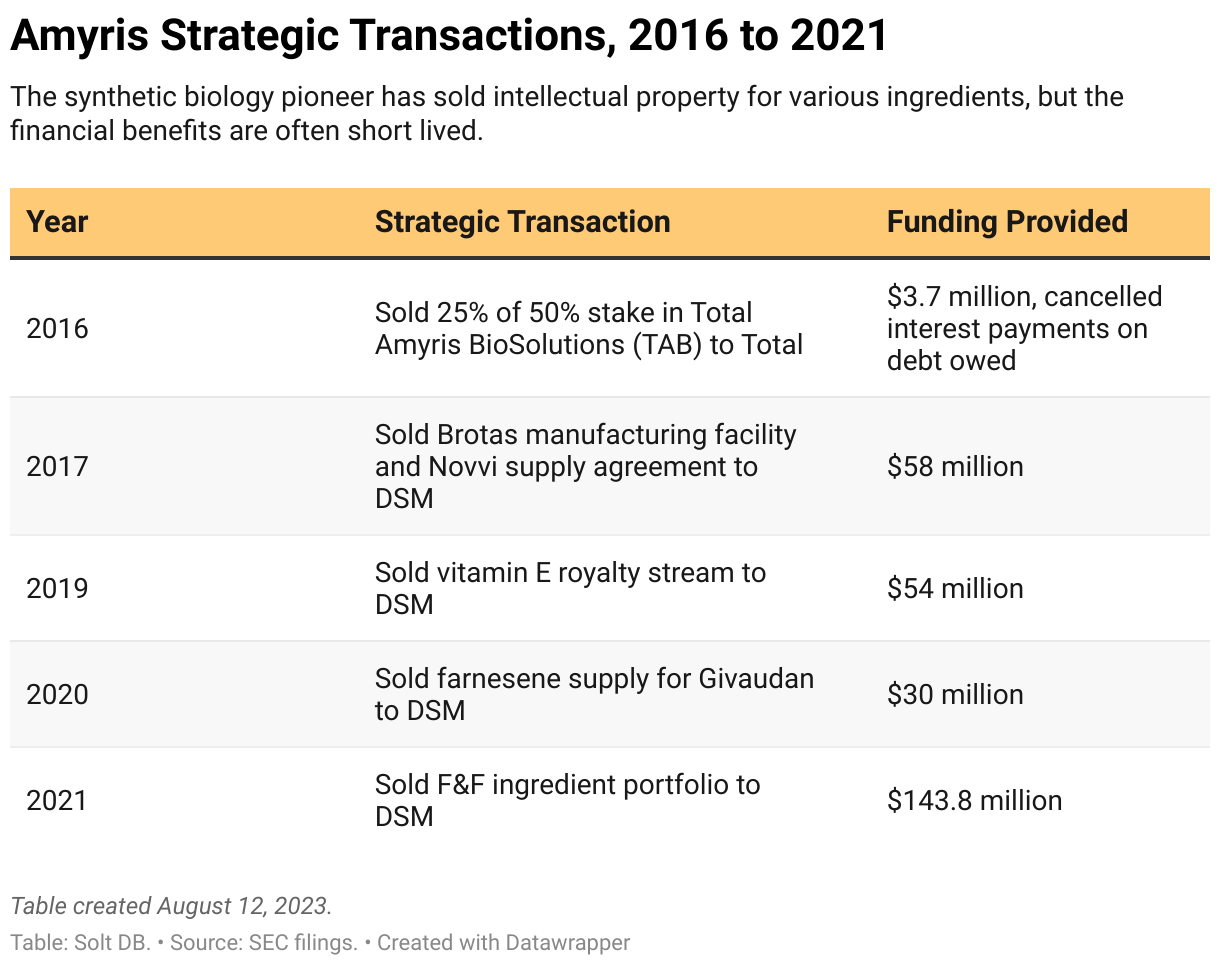

Hype in investor presentations can only take a business so far for so long. As a result of chronic mismanagement of finances, Amyris has been forced to divest non-core assets in "strategic transactions" multiple times to raise capital and keep the lights on. Management admitted in November 2022 that it will need to do so again before the end of the year to avoid bankruptcy.

Note: The following graphic was added on December 2, 2022 and updated on February 11, 2023, but illustrates the point more clearly.

Of course, selling non-core assets implies there are core assets. The business appears to have none given the constant reshuffling of ingredients, partnerships, and the constantly shifting definition of "non-core asset."

At times when "strategic transactions" are unavailable, Amyris resorts to reporting intentionally false and misleading financials.

In 2018, Amyris manipulated a change in accounting rules to report revenue that hadn't materialized. The Financial Accounting Standards Board (FASB) sets standards for the generally accepted accounting principles (GAAP) metrics used by all companies to standardize financial reporting. That year, a new rule called ASC 606 was implemented that altered the timing of revenue recognition. Companies from Tesla to Microsoft had to comply.

Amyris applied ASC 606 to royalty revenue related to the sale of vitamin E ingredients, using it to intentionally mislead investors about the value of the royalty stream. Investors didn't need the power of hindsight to see this unfolding. As I wrote at the time:

DSM licenses technology from Amyris to manufacture a chemical called farnesene, which is sold to a company called Nenter, which uses farnesene to manufacture vitamin E. When the resulting vitamin E is sold, a portion of the profit travels back to Amyris through DSM and gets recorded as licensing and royalty revenue.

Here's the problem: Amyris records royalty revenue at the time DSM sells farnesene to Nenter, not when Nenter sells vitamin E and records a profit. In other words, it's impossible to know the amount of royalties due at the time Amyris currently records them.

... As the [numbers] above show, the difference between royalty and licensing revenue reported by Amyris and what it has actually received in the first six months of this year is $15.7 million. That's 86% of the total reported. That's a huge red flag.

The manipulation allowed the company to report $46.2 million in first-half 2018 revenue when it had only received $28.2 million from customers and partners. The stock surged over 100% year-to-date on a seemingly positive growth trajectory. It all unraveled when – you guessed it – third-quarter 2018 operating results were announced in November.

It left a good mark on the business. Amyris didn't file its 2018 annual report (10-K) with the U.S. Securities and Exchange Commission (SEC) until October 2019. It would typically be filed in February or March. The business also had to restate 2017 financials.

If everything above wasn't bad enough, then brace yourself.

On April 7, 2020, Amyris applied for a $10 million Paycheck Protection Program (PPP) loan. The requested amount was granted in full on May 7, 2020. Although the loan was repaid in full on June 12, 2020, the company describes the loan in SEC filings as part of "a series of financial transactions to minimize cash outflows related to debt service payments and to increase operating cash." The business had a market valuation of $411 million on the day it submitted an application for funds.

Small businesses that couldn't secure funding in the initial tranche of PPP loans had to close their doors because companies like Amyris abused the program.

The arrogance goes further: It incorrectly refers to the liquidity program intended for small businesses as the "Paycheck Protection Plan." Perhaps it was a Freudian slip.

Paying the Price

As new investors flooded into markets during the liquidity bubble of 2020 and 2021, inexperience and naivety became a dangerous combination. The ability to insulate in the information silos of social media only fueled the excesses and amplified the inevitable pain. Many Amyris shareholders are likely innocent victims taking their lumps as novice investors, as we all must do.

One of the most important lessons for biotech and synthetic biology investors: You own businesses, not technologies.

Perhaps individuals new to investing or Amyris are simply unaware of the decade-plus of misleading statements from management provided above. The company's financial performance in 2022 provides plenty of additional red flags and few excuses for remaining in this abusive relationship.

Negative Gross Margin: Amyris generated a negative product gross margin for five consecutive quarters dating back to the third quarter of 2021. The business spent $1.13 to generate every $1 in product revenue during that time.

Operating Expenses: Amyris spent $358 million on sales, general, and administrative (SG&A) expenses in the first nine months of 2022. It spent only $81 million, or 77% less, on research and development in that span.

Operating Loss: Amyris generated an operating loss of $416 million in the first nine months of 2022, including a quarterly record $148 million in the third quarter.

Cash Burn: Amyris burned $433 million in cash from operations in the first nine months of 2022. That equates to $66,089 per hour or $18.36 per second. And no, Elon Musk didn't take it over.

Cash Balance: Amyris held $18.5 million in cash at the end of September 2022. That would only be enough to last until 3:35pm ET on October 11, which has forced the company to secure short-term loans and issue new shares to keep the lights on in the final months of the year.

No Accountability: Shares of Amyris have lost over 99% since their public debut in 2010, over 95% in the last decade, over 91% since their liquidity bubble peak in 2021, and over 73% in the last year. John Melo has been CEO since 2007.

These are not the financial metrics of a company on the cusp of success. A close interrogation of financial statements suggests the opposite: Amyris could be forced into bankruptcy any day.

The company's cost structure is misaligned with its stated business model. Amyris could've succeeded in consumer brands with a more intentional sales strategy, but instead chose a growth-at-all-costs approach that relies on growth hacking. That is, the company is hyperfocused on reporting the highest possible revenue growth rates regardless of the SG&A burden required to achieve it.

This growth is being achieved in part by adding new brands that weren't contributing revenue in prior-year periods. Amyris had three consumer brands at the beginning of 2021, then launched five more brands in the second half of 2021 and one more in the first half of 2022.

It's an unsustainable approach.

Amyris Needs to Be Held Accountable

What is particularly disturbing is this all occurred in plain sight. There's no obfuscation of poor financial performance. There's no shying away from misleading statements; if anything, management appears to lean into them. That's what happens when there are no consequences.

Perhaps the existence of tangible, real-world products lends just enough credibility to suppress doubts about the company's supernatural ability to survive. It's easy to doubt crypto. You can't hold a blockchain in your hands.

The business has somehow managed to survive despite all the financial shenanigans and terrible operating metrics. This time might be different though.

Amyris has never had to execute the synbio shuffle with interest rates above 4%, a cash balance of $18 million, and while burning $18.36 of cash per second from operations. There's a very real chance the business doesn't make it to the end of 2022 or fails to pay its surging debts coming due in early 2023.

If enough capital stops enabling management's bad behavior, then the business will be forced to change, perhaps through bankruptcy engineered by an activist investor. The field of synthetic biology would be stronger with an Amyris living up to its true potential. Unfortunately, the way to deliver that at this point could be quite painful.

Solt DB is a biotech equities research firm. We manage a real-money, long-term oriented, 100% transparent investment portfolio called Finch Trades. As of June 30, 2026 (updated quarterly), we're outperforming the S&P 500 by 97.7%, Nasdaq 100 by 83.7%, XBI by 60.5%, and Ark Genomic Revolution ETF by 64.4%.

Memberships to investment research fund our mission as a public benefit company and keep us fiercely independent – so we can keep giving tech bros the bird. No ads, no clickbait, no hype. Join today for $26.25 per month.

.svg)

.svg)

.svg)

%20(squoosh).jpg)

%20(squoosh).jpg)

.svg)

.svg)

.svg)